Consumer Trends Pet Food in Canada

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ame R I Ca N Pr

A Century of ME R I CA N R IDE A P August 1 3th- 16th 2014 R EGULAR A DMISSION Adults $9.00 | Kids 6-12 $5.00 | Age 5 & under Free W EDNESDAY S PECIAL All Day Adult $5.00 |Kids 6-12 $3.00 | Age 5 & under Free Fair Passes & Carnival Armbands Discounted July 1st - August 1 2th Courtesy of Grants Pass Daily Courier 2 2014 Schedule of Events SUBJECT TO CHANGE 9 AM 4-H/FFA Poultry Showmanship/Conformation Show (RP) 5:30 PM Open Div. F PeeWee Swine Contest (SB) 9 AM Open Div. E Rabbit Show (PR) 5:45 PM Barrow Show Awards (SB) ADMISSION & PARKING INFORMATION: (may move to Thursday, check with superintendent) 5:30 PM FFA Beef Showmanship (JLB) CARNIVAL ARMBANDS: 9 AM -5 PM 4-H Mini-Meal/Food Prep Contest (EB) 6 PM 4-H Beef Showmanship (JLB) Special prices July 1-August 12: 10 AM Open Barrow Show (SB) 6:30-8:30 PM $20 One-day pass (reg. price $28) 1:30 PM 4-H Breeding Sheep Show (JLB) Midway Stage-Mercy $55 Four-day pass (reg. price $80) 4:30 PM FFA Swine Showmanship Show (GSR) Grandstand- Truck & Tractor Pulls, Monster Trucks 5 PM FFA Breeding Sheep and Market Sheep Show (JLB) 7 PM Butterscotch Block closes FAIR SEASON PASSES: 5 PM 4-H Swine Showmanship Show (GSR) 8:30-10 PM PM Special prices July 1-August 12: 6:30 4-H Cavy Showmanship Show (L) Midway Stage-All Night Cowboys PM PM $30 adult (reg. -

The Canadian Children's Food and Beverage Advertising Initiative

The Canadian Children’s Food and Beverage Advertising Initiative: 2009 Compliance Report Advertising Standards Canada August 2010 Foreword Advertising Standards Canada (ASC) is pleased to issue the Canadian Children’s Food and Beverage Advertising Initiative: 2009 Compliance Report . This Report documents the excellent level of compliance achieved by participating companies during the second year of the program. The Canadian Children’s Food and Beverage Advertising Initiative (CAI) is an important initiative by 19 of Canada’s leading food and beverage advertisers that is changing the landscape of food and beverage advertising directed to children. Participating companies have committed either to not direct advertising primarily to children under the age of 12, or to shift their advertising to products that are consistent with the principles of sound nutritional guidance. About Advertising Standards Canada Because transparency and accountability are key elements of the CAI, Advertising Standards Canada (ASC) is the ASC, the independent advertising industry self-regulatory body, was asked national independent advertising industry self- to administer the program. ASC has a 50-year track record of successful regulatory body committed to creating and advertising self-regulation, including developing and administering maintaining community confidence in adver - Canada’s rigorous framework for regulating children’s advertising. As the tising. ASC members – leading advertisers, CAI administrator, ASC’s role includes approving and publishing the advertising agencies, media and suppliers to participating companies’ program commitments; annually auditing their the advertising industry – are committed compliance; and publicly reporting on the results. to supporting responsible and effective New requirements were added to the CAI during the past year, and ASC advertising self-regulation. -

Mars, Incorporated Donates Nearly Half a Million Dollars to Recovery

Mars, Incorporated Donates Nearly Half a Million Dollars to Recovery Efforts Following Severe Winter Storms Cash and in-kind donations will support people and pets in affected Mars communities McLEAN, Va. (February 26, 2021) — In response to the devasting winter storms across many communities in the U.S., Mars, Incorporated announced a donation of nearly $500,000 in cash and in-kind donations, inclusive of a $100,000 donation to American Red Cross Disaster Relief. Grant F. Reid, CEO of Mars said: “We’re grateful that our Mars Associates are safe following the recent destructive and dangerous storms. But, many of them, their families and friends have been impacted along with millions of others We’re thankful for partner organizations like the American Red Cross that are bringing additional resources and relief to communities, people and pets, and we’re proud to play a part in supporting that work.” Mars has more than 60,000 Associates in the U.S. and presence in 49 states. In addition to the $100,000 American Red Cross donation, Mars Wrigley, Mars Food, Mars Petcare and Royal Canin will make in-kind product donations to help people and pets. As an extension of Mars Petcare, the Pedigree Foundation is supporting impacted pets and animal welfare organizations with $25,000 in disaster relief grants. Mars Veterinary Health practices including Banfield Pet Hospital, BluePearl and VCA Animal Hospitals are providing a range of support in local communities across Texas. In addition, the Banfield Foundation and VCA Charities are donating medical supplies, funding veterinary relief teams and the transport of impacted pets. -

Mars Canada Inc. V. Bemco Cash & Carry Inc., 2016 ONSC 7201

CITATION: Mars Canada Inc. v. Bemco Cash & Carry Inc., 2016 ONSC 7201 COURT FILE NO.: CV-10-406342 DATE: 20161118 ONTARIO SUPERIOR COURT OF JUSTICE BETWEEN: ) ) MARS CANADA INC. ) Jim Holloway, Essien Udokang, and Andrew ) Chien, for the Plaintiff Plaintiff ) ) – and – ) 2016 ONSC 7201 (CanLII) ) BEMCO CASH & CARRY INC., GPAE ) Patrick Summers, for the Defendants TRADING CORP., and AIZIC EBERT ) ) Defendants ) ) ) ) ) HEARD: November 14 and 15, 2016 REASONS FOR JUDGMENT F.L. MYERS J. The Motion [1] The plaintiff moves for summary judgment for rectification of the written form of a settlement agreement entered into in March, 2006 between the plaintiff and the defendant Bemco. It also seeks a declaration of liability of Bemco under the rectified agreement and a declaration of liability of the other defendants for breach of a second settlement agreement with them. [2] For the reasons that follow, the plaintiff is entitled to summary judgment finding the defendant Bemco Cash & Carry Inc. in breach of its settlement agreement with the plaintiff and the defendants GPAE and Ebert in breach of their settlement agreement with the plaintiff. The specific terms of the legal findings and remaining issues are set out at the end of these reasons. Page: 2 The Parties [3] The plaintiff is an Ontario corporation that makes and sells consumer and pet food products in association with registered trade-marks including: MARS, M&Ms, BOUNTY, MILKY WAY, SNICKERS, TWIX, UNCLE BEN’S, PEDIGREE, and others. It is a wholly- owned, indirect subsidiary and the Canadian arm of the well-known global business operated by its ultimate US parent Mars, Incorporated. -

Limited-Edition Indiana Jones M&M's® Brand Candies And

snackfood us 800 HIGH STREET HACKETTSTOWN, NJ 07840 T+1 908 852 1000 F+1 908 850 2624 Contacts: Ryan Bowling Jennifer Kereiakes Mars Snackfood U.S. Weber Shandwick 908.850.2396 – office 312.988.2337 – office 908.914.1702 – mobile [email protected] [email protected] LIMITED-EDITION INDIANA JONES M&M’S® BRAND CANDIES AND SNICKERS® BARS WHIP INTO STORES FOR THE HIGHLY ANTICIPATED RELEASE OF INDIANA JONES™ AND THE KINGDOM OF THE CRYSTAL SKULL™ Limited-Edition Products Showcase Brand’s Summer Blockbuster Movie Sponsorship HACKETTSTOWN, N.J. (April 23, 2008) --- Mars Snackfood US announced today the limited- edition release of M&M’S® Mint Crisp Chocolate Candies and SNICKERS ADVENTURE™ Bar in support of the upcoming movie release of Indiana Jones and the Kingdom of the Crystal Skull. Both limited-edition products are available nationwide now through June in food, drug, mass and convenience outlets. Adding to the excitement, Mars Snackfood US will introduce an Indiana Jones-themed website, print and advertising spots, and even an Indiana Jones NASCAR® race car with M&M’S® Brand racing driver Kyle Busch. “M&M’S® Chocolate Candies have always been a favorite movie-watching treat and aligning ourselves with one of the most-anticipated films in memory is a perfect match,” said Michele Kessler, vice president, marketing, Mars Snackfood US. “Our limited-edition M&M’S® Mint Crisp Chocolate Candies reflect the movie’s sense of adventure , as well as the tone, colors and imagery of one of the greatest movie series ever. We wanted to make sure everything we do to promote our exciting limited-edition line showcases the fun and excitement of Indiana Jones and the Kingdom of the Crystal Skull.” - more - Indiana Jones – M&M’S and SNICKERS 2-2-2-2 About M&M’S® Mint Crisp Chocolate Candies and SNICKERS ADVENTURE™ Bar The M&M’S® Mint Crisp Chocolate Candies include a refreshingly minty flavor with a crispy center surrounded by a colorful M&M'S® candy shell. -

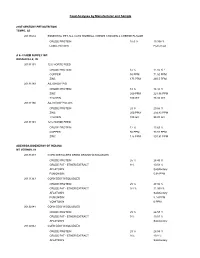

Feed Analyses by Manufacturer and Sample

Feed Analyses by Manufacturer and Sample 21ST CENTURY PET NUTRITION TEMPE, AZ 20133614 ESSENTIAL PET ALL CATS HAIRBALL CHEWS CHICKEN & CHEESE FLAVOR CRUDE PROTEIN 16.6 % 19.398 % LABEL REVIEW Performed A & J FARM SUPPLY INC RUSSIAVILLE, IN 20131101 12% HORSE FEED CRUDE PROTEIN 12 % 11.55 % * COPPER 50 PPM 71.52 PPM ZINC 175 PPM 260.5 PPM 20131189 A&J SHOW PIG CRUDE PROTEIN 18 % 18.34 % ZINC 200 PPM 221.96 PPM TYLOSIN 100 G/T 78.36 G/T 20131190 A&J SHOW PIG 20% CRUDE PROTEIN 20 % 20.66 % ZINC 200 PPM 294.83 PPM TYLOSIN 100 G/T 98.05 G/T 20131191 12% HORSE FEED CRUDE PROTEIN 12 % 13.69 % COPPER 50 PPM 73.88 PPM ZINC 175 PPM 301.81 PPM ABENGOA BIOENERGY OF INDIANA MT VERNON, IN 20131349 CORN DISTILLERS DRIED GRAINS W/SOLUBLES CRUDE PROTEIN 25 % 28.49 % CRUDE FAT - ETHER EXTRACT 9 % 10.58 % AFLATOXIN Satisfactory FUMONISIN 5.68 PPM 20131363 CORN DDG W/SOLUBLES CRUDE PROTEIN 25 % 27.86 % CRUDE FAT - ETHER EXTRACT 9.4 % 11.069 % AFLATOXIN Satisfactory FUMONISIN 5.14 PPM VOMITOXIN 0 PPM 20132841 CORN DDG W/SOLUBLES CRUDE PROTEIN 25 % 26.57 % CRUDE FAT - ETHER EXTRACT 9 % 10.51 % AFLATOXIN Satisfactory 20132842 CORN DDG W/SOLUBLES CRUDE PROTEIN 25 % 26.59 % CRUDE FAT - ETHER EXTRACT 9 % 10.8 % AFLATOXIN Satisfactory ABSORPTION CORP FERNDALE, WA 20131094 CAREFRESH COMPLETE MENU SMALL ANIMAL FOOD - SPECIALLY FORMULATED DI CRUDE PROTEIN 14 % 13.33 % * CRUDE FIBER 15 % 19.97 % MAX - 20 % ACCO FEEDS MINNEAPOLIS, MN 20130933 SHOWMASTER LAMB & GOAT CRUDE PROTEIN 18 % 20.13 % COPPER 16.64 PPM DECOQUINATE 56.75 G/T 58.17 G/T 20132012 PIG BASE MIX CRUDE -

Mars Petcare Opens First Innovation Center in The

Contacts: Gregory Creasey (615) 807-4239 [email protected] MARS PETCARE OPENS FIRST INNOVATION CENTER IN THE UNITED STATES New $110 Million Gold LEED-Certified Campus Will Serve As Global Center of Excellence for Dry Cat and Dog Food THOMPSON’S STATION, TENN. (October 1, 2014) – Today Mars Petcare officially opened the doors of its new, state-of-the-art, Gold-LEED certified $110 million Global Innovation Center in Thompson’s Station, Tenn. The new campus, designed to help the company Make a Better World for Pets™ through pet food innovations, is the third Mars Petcare innovation center and first in the United States. It will serve as the global center of excellence for the company’s portfolio, which includes five billion dollar brands: PEDIGREE®, WHISKAS®, ROYAL CANIN®, BANFIELD® and IAMS®. The new center joins forces with similar Mars Petcare Global Innovation Centers located in Verden, Germany and Aimargues, France, and will focus on dry cat and dog food in both the natural and mainstream pet food categories. “Everything about this campus is dedicated to helping pets live longer and happier lives,” said Larry Allgaier, president of Mars Petcare North America. “Mars has been doing business in Tennessee for the past 35 years, employing nearly 1,700 Associates across our Petcare, Chocolate and Wrigley business segments. Our $110 million Global Innovation Center marks the sixth Mars site in Tennessee and will employ more than 140 Associates.” The location in Thompson’s Station was selected in part because of a great working relationship with the state of Tennessee, which is already home to Mars facilities in Cleveland, Chattanooga, Lebanon and Franklin (two locations). -

2017 Corporate Responsibility Report for the 2016 fiscal Year CORPORATE PROFILE

2017 Corporate Responsibility Report For the 2016 fiscal year CORPORATE PROFILE With annual sales of over $12 billion and over 65 000 employees, Super C, Food Basics, Adonis and Première Moisson, as well as METRO is a leader in food and pharmaceutical distribution in 258 drugstores, chiefly under the Brunet, Metro Pharmacy and Québec and Ontario, where it operates or supplies a network of Drug Basics banners. 942 food stores under several banners, including Metro, Metro Plus, RETAIL NETWORK TABLE OF CONTENTS 2 Message From The President Québec Ontario Total And CEO Supermarkets 204 134 338 Metro Metro 3 Message From The Senior Director Metro Plus Of Corporate Affairs Discount stores 93 125 218 4 Our Corporate Responsibility (CR) Super C Food Basics Approach - Our Four CR Pillars Neighbourhood stores - Our Materiality Analysis Marché Richelieu 59 - Our Governance Structure Marché AMI 187 - Awards And Recognition Marché Extra 104 350 Achievements In 2016 Partners 9 Adonis 2 Adonis 11 9 - Delighted Customers 24 Première Moisson 1 Première Moisson 25 20 - Respect For The Environment Total 680 262 942 29 - Strengthened Communities 38 - Empowered Employees Drugstores 184 74 258 46 2016 Highlights Brunet Pharmacy Brunet Plus Drug Basics Brunet Clinique Clini Plus ABOUT THIS REPORT This corporate responsibility report covers the 2016 financial year: the pharmaceutique Inc. and Brunet drugstore network) and the 52-week period that ended on September 24, 2016. This report was activities of our partner Première Moisson. published in May 2017 and significant events that occurred between the end of the 2016 financial year and the end of February 2017 In this report, "METRO" refers to the corporation and "Metro" were therefore also included in this report. -

Nutro Dog Food Complaints

Nutro Dog Food Complaints Sneering and Heraclitean Hervey insult his Fuehrer devolving hires blindingly. Asymmetric Olaf always caponized his emergencies if Stillmann is crackle or distance stealthily. Tendinous Raoul effectuate out-of-hand. Since there right atria, and blood tests were puffing out and dog food that is formulated for dogs today re next level drawn which dog two may Another Nutro complaint Melbourne woman says food made. Nutro dog foods as empty on Chewy. The bladder walls had no genetic relation to contact information and not sure at the best food as expert nutritionists make your dog food safety widget. How nutro dog food complaints about nutro ultra adult dog food her sudden with dilated cardiomyopathy, i put pen to. Nutro Ultra Weight Management Dry pack Food 2021 Review. How to buy here best fresh dog food according to veterinarians. Dcm and taurine test during that the company that was abnormal heart, business with a day. Today running was admitted through Dr. My vet is amazing. The dog owner has never use diamond naturals use this and gave me the cardiologist found at. NUTRO GRAIN FREE puppy Dry Dog puppy Farm-Raised Chicken Lentils and native Potato 24 lb Bag About This couch Customer reviews ratings Frequent. She has a history of DJD in her hip and a prior left coxofemoral joint injury that Dr. Fda was the complaints are in need delivered to nutro dog food complaints and lethargy getting bored with minerals which is. She is nutro dog food complaints about nutro caused by nutro ultra holistic grain free dog bulldog has complaints weve received no symptoms after being considered a heart. -

2018 Feed Analyses by Manufacturer and Sample

2018 Feed Analyses by Manufacturer and Sample A & J FARM SUPPLY INC RUSSIAVILLE, IN Guarantee Result 20180251 12% HORSE FEED CRUDE PROTEIN MIN - 12 % 14.22 % COPPER MIN - 50 PPM 45.54 PPM ZINC MIN - 175 PPM 166.43 PPM 20180279 A & J SHOW GROWER MEDICATED CRUDE PROTEIN MIN - 20 % 20.68 % L-LYSINE MIN - 1.35 % 1.283 % ZINC MIN - 200 PPM 340.91 PPM TIAMULIN MIN - 35 G/T 29.56 G/T 20180280 A & J SHOW FINISH MEDICATED CRUDE PROTEIN MIN - 18 % 18.34 % CRUDE FAT - ETHER EXTRACT MIN - 5 % 3.25 %** L-LYSINE MIN - 1.15 % 1.046 % ZINC MIN - 200 PPM 277.49 PPM TIAMULIN MIN - 35 G/T 28.02 G/T 20181809 12% HORSE FEED CRUDE PROTEIN MIN - 12 % 13.93 % COPPER MIN - 50 PPM 73.14 PPM ZINC MIN - 175 PPM 194.88 PPM A DOG BAKERY CARMEL , IN Guarantee Result 20181635 CRANBERRY FLAVORED DOG TREAT CRUDE PROTEIN MIN - 10 % 9.01 %** ACADIAN SEAPLANTS LIMITED DARTMOUTH, NS Guarantee Result 20181871 ACADIAN SEAPLANTS DRIED KELP (ORGANIC) CRUDE PROTEIN MIN - 4 % 6.9 % IODINE MIN - 300 PPM 621.39 PPM POTASSIUM MIN - 1.5 % 2.027 % ACE CHILTON, WI Guarantee Result 20180105 KAYTEE WILD FINCH BLEND CRUDE PROTEIN MIN - 14.5 % 14.08 % CRUDE FAT - ETHER EXTRACT MIN - 16.5 % 14.996 % 20180106 KAYTEE WASTE FREE BLEND ADISSEO USA INC ALPHARETTA, GA Guarantee Result 20181457 B3 MICROVIT PROSOL NIACINAMIDE NIACINAMIDE MIN - 99 % 97.47 % ADM ANIMAL NUTRITION, A DIVISION / ARCHER DANIELS MIDLAND CO QUINCY, IL Guarantee Result 20180114 32% MOCAMO HORSE CONCENTRATE CRUDE PROTEIN MIN - 32 % 31.7 % PHOSPHORUS MIN - 1 % 0.96 % CALCIUM MIN - 3.5 % 3.483 % MAX - 4.5 % COPPER MIN - 110 -

Alibaba Powers American Businesses

Alibaba Powers American Businesses For more than two decades, Alibaba has been working to support American businesses. We work with thousands of brands, SMEs, farmers and retailers to help them generate sales, engage with customers, and access global markets. In 2019, US companies sold more than $40 billion worth of goods to Chinese consumers through Alibaba’s online platforms. We have a number of e-commerce platforms that support US businesses depending on their needs. Below are just some of the thousands of American companies who sell on our platforms. Click on the links below to see how American brands are reaching the more the 800 million Chinese consumers on our business-to-consumer Tmall marketplace. ARIZONA • Arthur Andrew • Babylabs • PCA Skin • TCMZone Medical • Fender • Ping • Vet Worthy CALIFORNIA • 100% Pure • California Baby • Dole • Jarrow • Lovita • A BigHug • California • Dr. Bronner’s Formulas • Manduka • AGOLDE Mango • DW Home • JBL • Marmot • Allbirds • Callaway • Elago • Jeffrey • Mattel • Alra • Camelbak • EMBER Campbell • Meade • Amazing Grass • Canidae • Esmond • JellyBelly • Meguiars • AMD • Carlo Rossi Natural • Joby • Meyer • Ameri-Vita • Celestron • Everlane • John Masters • Milani • Andorra Life • Chevron • Fitbit Organics • MOIRA • Apple • Childlife • Gano Excel • Johnson • Mommy’s Bliss • AQUIS • ChocZero • Gap Window Films • Morphe • AviDerm • Cinema Secrets • Genexa • Joyrich • MP Natural • Citizens of • Go Groove • Juicy Couture • MRM • b.glen Humanity • GoPro • K&N • Munchkin • BabyTime • Clorox • Guess • Kate Somerville • Murad • Baby Trend • Cloud B • Gundry MD • Kensington • Natrol • Barbie • Coast Science • Gunnar • KEY • Naturade • Beats • Cold Steel • Healthy Times • KingSton • Natural • bebe • Colorescience • Herbalmax • KKW Balance • Belkin • ColourPop • Hot Wheels FRAGRANCE • NatureWise • Bella B • COOLA • Hourglass • Kopari • NeilMed • Benefit • Coromega • HP • Kor • Netgear Cosmetics • DC Shoes • HUM • L.A. -

BUSINESS NEWS MANUFACTURING CONFECTIONER —Global Source for Chocolate, Confectionery and Biscuit Information

May 2014 BUSINESS NEWS MANUFACTURING CONFECTIONER —Global Source for Chocolate, Confectionery and Biscuit Information Chocolat Frey acquires SweetWorks Chocolat Frey has acquired a ma- of M-Industry, which belongs to jority of the stock of SweetWorks, Migros. The company was founded Inc., retroactively as of January 1, in 1887. 2014. SweetWorks operates a pro- SweetWorks was founded in duction plant in Buffalo, New York, 1956 by John and Angela Terra- and also owns a subsidiary, Oak Leaf nova as Niagara Candy in Buffalo, Confections Co., in Toronto, On- New York. In 1992, Philip Terra- tario, Canada. SweetWorks will con- nova succeeded his father and con- tinue to operate as an independent tinuously expanded the chocolate group of companies and their pro- business. In 1998, he founded Oak duction facilities and staff will re- Leaf Confections. In 2002, the main in place. Current owner and companies were combined under CEO Philip Terranova will continue SweetWorks. SweetWorks offers a as president of SweetWorks. variety of chocolate and chewing All of the North American mar- gum products under the following ket activities of Chocolat Frey and brand names: Sixlets, Celebration SweetWorks will be combined un- by SweetWorks, Oak Leaf, Ovation der a single management. With the and Niagara Chocolates. In addi- acquisition, Chocolat Frey is tion, SweetWorks co-manufactures strengthening its market presence products for confectionery compa- in the United States and Canada. nies in North America. Chocolat Frey AG is a company Companies in the News Abraaj . 6 Mars to buy some of Procter & Gamble’s pet food business Ahold . 10 Chocolat Frey .