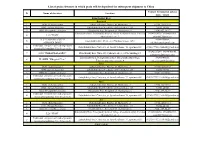

Specific Features of Regional Budget Policy Using the Example of Novosibirsk Oblast T

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Some Data on Zoophilic Flies of Siberia and the Russian Far East

Ukrainian Journal of Ecology Ukrainian Journal of Ecology, 2021, 11(6), 100-104, doi: 10.15421/2021_230 ORIGINAL ARTICLE Some data on zoophilic flies of Siberia and the Russian Far Ukrainian Journal of Ecology,2021, 11(4),,doi: 10.15421/2021_ East E.I. Sivkova All-Russian Scientific Research Institute of Veterinary Entomology and Arachnology-Branch of Federal State Institution Federal Research Centre Tyumen Scientific Centre of Siberian Branch of the Russian Academy of Sciences, 2 Institutskaya St, Tyumen 641025, Russia *Corresponding author E-mail: [email protected] Received: 23.07.2021. Accepted: 09.08.2021. In the vast territories of Siberia and the Russian Far East that include various landscapes and climatic zones of the country, flies play an important role as they are constantly present in the life of humans and animals. Flies belong to the Order Diptera, comprising of two-winged flies, the suborder Cyclorrapha (circular-seamed flies). Flies are vectors of many infectious and invasive diseases (they spread pathogens of microorganisms, protozoa, and fungi) and can also cause independent diseases in the larval phase. In this genus case, the flesh-fly family (Sarcophagidae), Wohlfahrtia magnifica genus, Schin.,1862, is a classic example of flies with a free- living pattern to a parasitic lifestyle. Species specificity of flies is weakly expressed, though they give the most significant preference to cattle. Traditional fly control methods include preventive and exterminating measures. Preventive steps are targeted at the elimination of potential fly breeding places by practicing routine sanitation. The advantage of preventive measures is their environmental friendliness. However, they do not significantly reduce the number of flies. -

THE RELIABILITY of RADIOCARBON DATING BURIED SOILS 630090 Russia Since the First 14C Age Determination of Soil Organic Matter (O

The Reliability of Radiocarbon Dating Buried Soils Item Type Article; text Authors Orlova, L. A.; Panychev, V. A. Citation Orlova, L. A., & Panychev, V. A. (1993). The reliability of radiocarbon dating buried soils. Radiocarbon, 35(3), 369-377. DOI 10.1017/S0033822200060379 Publisher Department of Geosciences, The University of Arizona Journal Radiocarbon Rights Copyright © by the Arizona Board of Regents on behalf of the University of Arizona. All rights reserved. Download date 02/10/2021 20:19:03 Item License http://rightsstatements.org/vocab/InC/1.0/ Version Final published version Link to Item http://hdl.handle.net/10150/653478 [RADIOCARBON, VOL. 35, No. 3, 1993, P. 369-377] THE RELIABILITY OF RADIOCARBON DATING BURIED SOILS L. A. ORLOVA and V. A. PANYCHEV United Institute of Geology, Geophysics and Mineralogy, Universitetsky pr., 3, Novosibirsk 90, 630090 Russia ABSTRACT. Variable 14C ages of paleosol organic matter (OM) cause difficulties in interpreting 14C data. We attempt to determine the reliability of OM 14C dates by examining different carbon-containing materials from soil horizons and paleosol fractions. INTRODUCTION Since the first 14C age determination of soil organic matter (OM) (Tamm and Ostlund 1960), the problems of 14C data interpretation have been widely discussed (Arslanov 1987; Arslanov et al. 1970; Arslanov and Kozyreva 1976; Gerasimov and Chichagova 1971; Zavelskiy 1975; Chichagova 1985; Scharpenseel 1971; Campbell et al. 1967; Costin and Polach 1969; Geyh, Bensler and Roeschman 1971; Polach and Costin 1971; Bowler and Polach 1971). These problems involve soil OM biodynamics in various landscape/climatic areas and soil types. Unlike wood and peat, where each annual tree ring and peat layer "conserves" the particular 14C content of the moment of growth, soil horizons are characterized by constant replacement of OM along the profile, which leads to redistribution of 14C ratios in different carbon-containing materials and soil fractions. -

Estimations of Undisturbed Ground Temperatures Using Numerical and Analytical Modeling

ESTIMATIONS OF UNDISTURBED GROUND TEMPERATURES USING NUMERICAL AND ANALYTICAL MODELING By LU XING Bachelor of Arts/Science in Mechanical Engineering Huazhong University of Science & Technology Wuhan, China 2008 Master of Arts/Science in Mechanical Engineering Oklahoma State University Stillwater, OK, US 2010 Submitted to the Faculty of the Graduate College of the Oklahoma State University in partial fulfillment of the requirements for the Degree of DOCTOR OF PHILOSOPHY December, 2014 ESTIMATIONS OF UNDISTURBED GROUND TEMPERATURES USING NUMERICAL AND ANALYTICAL MODELING Dissertation Approved: Dr. Jeffrey D. Spitler Dissertation Adviser Dr. Daniel E. Fisher Dr. Afshin J. Ghajar Dr. Richard A. Beier ii ACKNOWLEDGEMENTS I would like to thank my advisor, Dr. Jeffrey D. Spitler, who patiently guided me through the hard times and encouraged me to continue in every stage of this study until it was completed. I greatly appreciate all his efforts in making me a more qualified PhD, an independent researcher, a stronger and better person. Also, I would like to devote my sincere thanks to my parents, Hongda Xing and Chune Mei, who have been with me all the time. Their endless support, unconditional love and patience are the biggest reason for all the successes in my life. To all my good friends, colleagues in the US and in China, who talked to me and were with me during the difficult times. I would like to give many thanks to my committee members, Dr. Daniel E. Fisher, Dr. Afshin J. Ghajar and Dr. Richard A. Beier for their suggestions which helped me to improve my research and dissertation. -

List of Grain Elevators in Which Grain Will Be Deposited for Subsequent Shipment to China

List of grain elevators in which grain will be deposited for subsequent shipment to China Contact Infromation (phone № Name of elevators Location num. / email) Zabaykalsky Krai Rapeseed 1 ООО «Zabaykalagro» Zabaykalsku krai, Borzya, ul. Matrosova, 2 8-914-120-29-18 2 OOO «Zolotoy Kolosok» Zabaykalsky Krai, Nerchinsk, ul. Octyabrskaya, 128 30242-44948 3 OOO «Priargunskye prostory» Zabaykalsky Krai, Priargunsk ul. Urozhaynaya, 6 (924) 457-30-27 Zabaykalsky Krai, Priargunsky district, village Starotsuruhaytuy, Pertizan 89145160238, 89644638969, 4 LLS "PION" Shestakovich str., 3 [email protected] LLC "ZABAYKALSKYI 89144350888, 5 Zabaykalskyi krai, Chita city, Chkalova street, 149/1 AGROHOLDING" [email protected] Individual entrepreneur head of peasant 6 Zabaykalskyi krai, Chita city, st. Juravleva/home 74, apartment 88 89243877133, [email protected] farming Kalashnikov Uriy Sergeevich 89242727249, 89144700140, 7 OOO "ZABAYKALAGRO" Zabaykalsky krai, Chita city, Chkalova street, 147A, building 15 [email protected] Zabaykalsky krai, Priargunsky district, Staroturukhaitui village, 89245040356, 8 IP GKFH "Mungalov V.A." Tehnicheskaia street, house 4 [email protected] Corn 1 ООО «Zabaykalagro» Zabaykalsku krai, Borzya, ul. Matrosova, 2 8-914-120-29-18 2 OOO «Zolotoy Kolosok» Zabaykalsky Krai, Nerchinsk, ul. Octyabrskaya, 128 30242-44948 3 OOO «Priargunskye prostory» Zabaykalsky Krai, Priargunsk ul. Urozhaynaya, 6 (924) 457-30-27 Individual entrepreneur head of peasant 4 Zabaykalskyi krai, Chita city, st. Juravleva/home 74, apartment 88 89243877133, [email protected] farming Kalashnikov Uriy Sergeevich Rice 1 ООО «Zabaykalagro» Zabaykalsku krai, Borzya, ul. Matrosova, 2 8-914-120-29-18 2 OOO «Zolotoy Kolosok» Zabaykalsky Krai, Nerchinsk, ul. Octyabrskaya, 128 30242-44948 3 OOO «Priargunskye prostory» Zabaykalsky Krai, Priargunsk ul. -

The Influence of State-Confessional Policies on the Activities of Religious Communities in Western Siberia in the 1970S and Early 1980S

Advances in Social Science, Education and Humanities Research, volume 364 International Conference on Sustainable Development of Cross-Border Regions: Economic, Social and Security Challenges (ICSDCBR 2019) The influence of state-confessional policies on the activities of religious communities in Western Siberia in the 1970s and early 1980s N S Dvoryanchikova1* 1 Altai State University, 61 Lenina prosp., Barnaul Russia E-mail: [email protected] Abstract. The article is devoted to the study of the activities and position of religious organizations in the Novosibirsk region in the 1970s and early 1980s. In the period under review, there are changes in the state-confessional policy in the USSR in general and in the Novosibirsk region in particular. At this stage, the process of registration of organizations of the Russian Orthodox Church, Gospel Сhristian Baptists (adherents of the All-Union Council), Catholic, Lutheran communities was occurring. These registrations of Protestant communities were the first ones after the mass transfer of “sectarian” religious communities throughout the USSR to an illegal situation. In addition, the authorities tried to subordinate to control those religious organizations (the GCB Council of the Churches) which did not agree to register, allowing them to hold services in the same place and at the same time. The article shows the features of the situation with the Christian and Muslim communities, focusing on the registration process, economic, demographic changes within communities. The author argues that during the period under study, there was a change in the state-confessional policy with respect to religious organizations, the process of registering communities was resumed, property for the administration of religious cults was allowed to be acquired. -

Ash Content of Ornamental Plants in Urban Environment (Through the Example of the Cities of the Novosibirsk Region)

412 Chemistry for Sustainable Development 28 (2020) 412–417 UDC 581.192.1:635.92 DOI: 10.15372/CSD2020247 Ash Content of Ornamental Plants in Urban Environment (Through the Example of the Cities of the Novosibirsk Region) L. L. SEDEL’NIKOVA1, O. L. TSANDEKOVA2 1Central Siberian Botanical Garden, Siberian Branch of the Russian Academy of Sciences, Novosibirsk, Russia E-mail: [email protected] 2Federal Research Center for Coal and Coal Chemistry, Siberian Branch of the Russian Academy of Sciences, Kemerovo, Russia (Received August 07, 2019) Abstract The results of determining the ash content of perennial and annual plants growing near industrial zones, roads and in the urban environment of the administrative centres of the Novosibirsk Region (Iskitim, Berdsk, Novosi- birsk) are presented. These plant habitats differ in the degree of anthropogenic impact on the environment, with the greatest pollution in the city of Iskitim. It is noted that the ash content of the leaves of plants of different systematic groups is determined by many factors, including species and varietal belonging, anthropogenic pollu- tion of the environment, and the features of the growing season. A decrease in the content of ash substances in the leaves of herbaceous plants belonging to the families Hemerocallidaceae > Asteraceae > Iridaceae > Hosta- ceae > Laminaceae was established. Keywords: leaf, ash content, herbaceous plants, urban environment, Novosibirsk Region INTRODUCTION spectively [1]. The major effect on the state of vegetation in Novosibirsk is caused by the indus- The Novosibirsk urban agglomeration is dis- trial and road complex [2, 3]. The urban forestry tinguished by a large network of industrial zones in small towns is insufficient, especially in the that are situated in the suburbs or in small towns territories near industrial zones. -

Subject of the Russian Federation)

How to use the Atlas The Atlas has two map sections The Main Section shows the location of Russia’s intact forest landscapes. The Thematic Section shows their tree species composition in two different ways. The legend is placed at the beginning of each set of maps. If you are looking for an area near a town or village Go to the Index on page 153 and find the alphabetical list of settlements by English name. The Cyrillic name is also given along with the map page number and coordinates (latitude and longitude) where it can be found. Capitals of regions and districts (raiony) are listed along with many other settlements, but only in the vicinity of intact forest landscapes. The reader should not expect to see a city like Moscow listed. Villages that are insufficiently known or very small are not listed and appear on the map only as nameless dots. If you are looking for an administrative region Go to the Index on page 185 and find the list of administrative regions. The numbers refer to the map on the inside back cover. Having found the region on this map, the reader will know which index map to use to search further. If you are looking for the big picture Go to the overview map on page 35. This map shows all of Russia’s Intact Forest Landscapes, along with the borders and Roman numerals of the five index maps. If you are looking for a certain part of Russia Find the appropriate index map. These show the borders of the detailed maps for different parts of the country. -

2012 Novosibirsk, Russia

Regional Teaching Course 5-7 July, 2012 Novosibirsk, Russia Local Teaching Course organizer: Pavel Pilipenko, Prof., MD, PhD Department of Clinical Neurology Faculty of Postgraduate Education Novosibirsk State Medical University Krasny Prospect, 52 630091 Novosibirsk Russia 5-7 July, 2012 we had the second successful Teaching Course of EFNS in Novosibirsk! Registration desk The Teaching Course brought together leading neurologists of Germany, Russia, Greece, Czech Republic, Italy and Austria. More than 300 physicians were registered! - and that's just only part of our participants, because we did not perform registration during the scientific sessions (despite the fact that we were expecting only 150 members, but in Siberia scientific events of such a high level are rare, and the opportunity to participate in the international conferences for physicians is very limited, so the Siberian doctors were very interested in participating in the RTC of the EFNS). Participants and local translator. Physicians from Siberia came from: Voronezh, Novosibirsk, Barnaul, Ob, Barabinsk, Berdsk, Suzun, Toguchin, Nizhnevartovsk, Tomsk, Omsk, Kemerovo, Tatar, Iskitim, Kargath, Linevo, Cherepanovo, Novokuznetsk, Krivodanovka. Every day more than 200 people registered. At the end of the third day, which was a warm summer day (that is very rare for Siberia!!) we had more than 120 people, that indicated the interest of physicians in obtaining new knowledge. Welcoming remarks were made by the rector of Novosibirsk State Medical University - Prof. I.O. Marinkin and Prof. P. Kalvach - representative of the EFNS, and the Head of the local TC Committee – Prof. PI Pilipenko. They emphasized the practical significance and the importance of such training courses, with possible discussions and exchange of experiences. -

Download This Article in PDF Format

E3S Web of Conferences 210, 05018 (2020) https://doi.org/10.1051/e3sconf/202021005018 ITSE-2020 A technique for the estimation of the effect of investments in the digitalisation of the dairy subcomplex entities Mikhail Chernyakov1,*, Maria Chernyakova 2, Irina Chernyakova 1,2, Kamal Akberov3, Irina Kharlamova3, and Elena Sarycheva3 1Novosibirsk State Technical University, 630078, Karl Marx Ave.., 20, Novosibirsk, Russia 2Siberian Institute of Management – Branch of Russian Academy of National Economy and State Service Under the RF President, 630102, Nizhnegorskaya, 6, Novosibirsk, Russia 3Novosibirsk State University of Economics and Management, 630099, 56 Kamenskaya str., Novosibirsk, Russia Abstract. The paper outlines the results of the analysis made to study the possibilities of using digital technologies to estimate the effect of investments in the digitalisation of dairy subcomplex entities. A review of academic literature revealed an insufficient number of publications on the dairy subcomplex digitalisation. The technique used to estimate the index of dairy subcomplex entities engaged the principles for constructing composite information indicators recommended by the European Commission. The proposed approach connects the system of state programmes and the digitalisation level of the dairy subcomplex for the first time. Taking into account the industry specifics, an attempt has been made to integrally estimate the digitalisation in dairy cattle breeding. It is recommended to introduce two criteria to assess the informational support level of dairy cattle breeding entities: the share and the index of dairy cattle breeding digitalisation. The correlation between the digitalization index of dairy cattle breeding and the return on equity has been established. An author's technique has been developed for a preliminary estimation of the effect of investments in digitalisation. -

BR IFIC N° 2611 Index/Indice

BR IFIC N° 2611 Index/Indice International Frequency Information Circular (Terrestrial Services) ITU - Radiocommunication Bureau Circular Internacional de Información sobre Frecuencias (Servicios Terrenales) UIT - Oficina de Radiocomunicaciones Circulaire Internationale d'Information sur les Fréquences (Services de Terre) UIT - Bureau des Radiocommunications Part 1 / Partie 1 / Parte 1 Date/Fecha 22.01.2008 Description of Columns Description des colonnes Descripción de columnas No. Sequential number Numéro séquenciel Número sequencial BR Id. BR identification number Numéro d'identification du BR Número de identificación de la BR Adm Notifying Administration Administration notificatrice Administración notificante 1A [MHz] Assigned frequency [MHz] Fréquence assignée [MHz] Frecuencia asignada [MHz] Name of the location of Nom de l'emplacement de Nombre del emplazamiento de 4A/5A transmitting / receiving station la station d'émission / réception estación transmisora / receptora 4B/5B Geographical area Zone géographique Zona geográfica 4C/5C Geographical coordinates Coordonnées géographiques Coordenadas geográficas 6A Class of station Classe de station Clase de estación Purpose of the notification: Objet de la notification: Propósito de la notificación: Intent ADD-addition MOD-modify ADD-ajouter MOD-modifier ADD-añadir MOD-modificar SUP-suppress W/D-withdraw SUP-supprimer W/D-retirer SUP-suprimir W/D-retirar No. BR Id Adm 1A [MHz] 4A/5A 4B/5B 4C/5C 6A Part Intent 1 107125602 BLR 405.6125 BESHENKOVICHI BLR 29E28'13'' 55N02'57'' FB 1 ADD 2 107125603 -

Economic Potential of Novosibirsk Region

Economic Potential of Novosibirsk Region For the reference of foreign companies and associations of entrepreneurs Novosibirsk 2013 Table of contents: 1 General information 3-4 2 Economics of the region 5-7 3 Science and innovations 8-10 4 Foreign economic relations 11 5 Investment climate 12 6 Competitive capacity of the region 13 7 List of references 15 General information Novosibirsk Region established on the 28th of September 1937 belongs to the Siberian Federal District. The administrative center of Novosibirsk Region is Novosibirsk. Area of Novosibirsk Region is 177.8 square km. It is located in the south-east of the West Siberian Plain between the Ob and the Irtysh rivers. The region borders Kazakhstan, Altai Territory, Kemerovo Region, Omsk Region and Tomsk Region. The main river of Novosibirsk Region is the Ob. Novosibirsk Region consists of 5 urban districts, 30 municipalities and 455 municipal settlements (26 urban and 429 rural). As of 01.01.2013 according to the Novosibirskstat, population of Novosibirsk Region is 2 709 836 people, among them 2 110 240 are urban. The largest cities are: Novosibirsk, Berdsk, Iskitim, Kuibyshev. Regional authority The state power in Novosibirsk Region is exercised on the basis of its division into legislative, executive and judicial powers. The highest executive body of the region is the Government of Novosibirsk Region. Since September 2010 it is headed by the governor Vasiliy Yurchenko. The legislative body of the region is the Legislative Assembly of Novosibirsk Region. The Chairman of the Legislative Assembly is Ivan Moroz. The Regional authorities responsible for business and innovative development in Novosibirsk Region are the Ministry for Education, Science and Innovation Policies of Novosibirsk Region and the Ministry of Industry, Trade and Entrepreneurship Development of Novosibirsk Region. -

MEGA Novosibirsk Tomsk Region Market Overview Bolshevistskaya Str

MEGA Novosibirsk Tomsk region Market overview Bolshevistskaya str. y wa gh hi Welcome skoe od br no si u to MEGA Kemerovsk Catchment areas People Distance G region Novosibirsk Vatutina str. Novosibirsk Primary 476,000 < 17 km O b Krasnoobsk ’ ri Berdsk ve Secondary 960,000 17–21 km r Cherepanovo highway Berdskoe MEGA NOVOSIBIRSK IS THE LARGEST AND MOST POPULAR Tertiary 985,000 21–21 km Altai SHOPPING CENTRES IN THE CITY, territory THANKS TO ITS LOCATION, WELL- Kazakhstan Barnaul DESIGNED LAYOUT AND RETAIL MIX. Total area: 2,421,000 Surveys show that about 78% of MEGA Urban development of Novosibirsk shoppers visit MEGA at least once a month mainly focuses on areas close to MEGA. with women making up 60% of all visitors. Customer feedback is extremely favourable, MEGA stands to profit from a projected especially in terms of availability of parking, increase of residents within its direct the wide choice of stores and brands, and surroundings. Successful development the variety of food options. of the housing projects will bring 26,000 additional residents into the primary catch- MEGA Novosibirsk offers shopping and lei- ment area by 2015 and another 36,000 sure for the whole family, combining strong inhabitants by 2020 anchor tenants like IKEA, Auchan and Leroy Merlin and favourite international fashion For Novosibirsk, the planned city modern- brands with entertainment facilities, cafes izations will have strong effects on MEGA. and restaurants. The new bridge will directly link MEGA to the eastern parts of the city north of the river Ob. From 2015, MEGA is expected to increase its market shares within this area.