Building New Perspectives

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Clinics in Downtown Core Open on Friday 24 Jan 2020

LIST OF CLINICS IN DOWNTOWN CORE OPEN ON FRIDAY 24 JAN 2020 POSTAL S/N NAME OF CLINIC BLOCK STREET NAME LEVEL UNIT BUILDING TEL OPENING HOURS CODE 1 ACUMED MEDICAL GROUP 16 COLLYER QUAY 02 03 INCOME AT RAFFLES 049318 65327766 8.30AM-12.30PM 2 AQUILA MEDICAL 160 ROBINSON ROAD 05 01 SINGAPORE BUSINESS FEDERATION CENTER 068914 69572826 11.00AM- 8.00PM 3 AYE METTA CLINIC PTE. LTD. 111 NORTH BRIDGE ROAD 04 36A PENINSULA PLAZA 179098 63370504 2.30PM-7.00PM 4 CAPITAL MEDICAL CENTRE 111 NORTH BRIDGE ROAD 05 18 PENINSULA PLAZA 179098 63335144 4.00PM-6.30PM 5 CITYHEALTH CLINIC & SURGERY 152 BEACH ROAD 03 08 GATEWAY EAST 189721 62995398 8.30AM-12.00PM 6 CITYMED HEALTH ASSOCIATES PTE LTD 19 KEPPEL RD 01 01 JIT POH BUILDING 089058 62262636 9.00AM-12.30PM 7 CLIFFORD DISPENSARY PTE LTD 77 ROBINSON ROAD 06 02 ROBINSON 77 068896 65350371 9.00AM-1.00PM 8 DA CLINIC @ ANSON 10 ANSON ROAD 01 12 INTERNATIONAL PLAZA 079903 65918668 9.00AM-12.00PM 9 DRS SINGH & PARTNERS, RAFFLES CITY MEDICAL CENTRE 252 NORTH BRIDGE RD 02 16 RAFFLES CITY SHOPPING CENTRE 179103 63388883 9.00AM-12.30PM 10 DRS THOMPSON & THOMSON RADLINK MEDICARE 24 RAFFLES PLACE 02 08 CLIFFORD CENTRE 048621 65325376 8.30AM-12.30PM 11 DRS. BAIN + PARTNERS 1 RAFFLES QUAY 09 03 ONE RAFFLES QUAY - NORTH TOWER 048583 65325522 9.00AM-11.00AM 12 DTAP @ DUO MEDICAL CLINIC 7 FRASER STREET B3 17/18 DUO GALLERIA 189356 69261678 9.00AM-3.00PM 13 DTAP @ RAFFLES PLACE 20 CECIL STREET 02 01 PLUS 049705 69261678 8.00AM-3.00PM 14 FULLERTON HEALTH @ OFC 10 COLLYER QUAY 03 08/09 OCEAN FINANCIAL CENTRE 049315 63333636 -

Press Release July 2017 Manchester's Five-Star Hotel

Press release July 2017 Manchester’s five-star hotel bolsters management team with two major senior appointments After the sale of Manchester’s five star Lowry Hotel in May to Singapore-based CDL Hospitality Trusts, the hotel is moving full steam ahead with the appointment of a new operations director and a sales director. Simon Harding has been appointed as the director of operations and Scott Brown as the new head of sales, both joined the hotel’s management team in June. Simon Harding will use his 18-years’ experience working with high end luxury hotel groups to help propel the hotel forward into 2018. Prior to his role at the Lowry Hotel, Simon worked as operations manager and Deputy General Manager at a number of luxury hotels and groups across the North of England and North Wales including Qhotels , Handpicked Hotels and Exclusive Hotels , properties include Rookery Hall , Deganwy Quay, Storrs Hall and the Lion Quays Hotel & Spa and the Cottons Thwaites Hotel in Knutsford. Discussing his appointment Simon says: “I am very proud to be joining the Lowry Hotel at such a pivotal point. During my career, I have had the opportunity work in luxury hotels across Cheshire, the Midlands and North Wales and always take great pride in my approach to customer relations. I look forward to working with the Lowry Hotel team to maintain the impeccable level of service it already has and to ensure all guests have a positive and memorable stay with us.” With over 10 years of commercial experience in the hospitality sector, Scott Brown will help drive the hotel’s local, national and increasingly international sales strategy. -

Astoria Mood Cover 100 Years 2013.Indd

Berlin, Hotel de Rome Brussels, Hotel Amigo Edinburgh, The Balmoral Florence, Hotel Savoy Frankfurt, Villa Kennedy London, Brown’s Hotel Manchester, The Lowry Hotel ST PETERSBURG Munich, The Charles Hotel Rome, Hotel de Russie Sicily, Verdura Golf & Spa Resort St Petersburg, Hotel Astoria Future Openings: Jeddah Marrakech Luxor Cairo ST PETERSBURG www.roccofortehotels.com 100 YEARS OF HISTORY For more information about Hotel Astoria or our other properties and to book online, please visit www.roccofortehotels.com Built by the architect Lidval in 1912, Hotel Astoria is a monument to St Petersburg’s famed Art Nouveau movement. The hotel boasts some of the fi nest views in the city, overlooking St Isaac’s Cathedral and only a moment’s walk from the Hermitage and many of St Petersburg’s historic sights. My sister Olga Polizzi has weaved her usual magic in updating the hotel and giving it a more stylish and contemporary feel. As with all our hotels you will fi nd the staff at the Astoria warm and friendly, professional and ready to please. Sir Rocco Forte Cairo Future Opening Luxor Future Opening Future Openings: Jeddah, Marrakech, Luxor, Cairo. Jeddah Future Opening Marrakech Future Opening St Isaac’s Cathedral, a fi ne example of St Petersburg’s architecture, facing Hotel Astoria. Where contemporary meets classic. Deluxe Suite Junior Suite The new Junior Suite, one of many recently refurbished rooms at Hotel Astoria. The stairs have seen many famous guests since 1912. The Presidential Suite Author HG Wells found inspiration in the timeless elegance of Hotel Astoria. Discover contemporary Russian cuisine at the Astoria Café. -

Office Listing & Rental Price

Office Listing & Rental Price Subject to availability, survey, approval and contract Asking rents are subject to revision without any notice Francis Goh (65) 97305200 [email protected] CEA Reg. No: R041398H TYPE DISTRICT LOCATIONS ADDRESS SIZE (SQFT) PSF (S$) PRICE (S$) AVAILABLE REMARKS Retail (F&B) 1 Crown at Robinson 140 Robinson Road 068907 2,508 13.00 32,604 Immediate Fitted Office 1 Crown at Robinson 140 Robinson Road 068907 592 9.00 5,328 Immediate Bare Office 1 Crown at Robinson 140 Robinson Road 068907 592 9.00 5,328 Immediate Bare Office 1 Crown at Robinson 140 Robinson Road 068907 592 9.00 5,328 Immediate Partially fitted Office 1 Crown at Robinson 140 Robinson Road 068907 926 9.00 8,334 Immediate Partially fitted Office 1 Crown at Robinson 140 Robinson Road 068907 6,792 9.00 61,128 Immediate Fitted Office 1 Crown at Robinson 140 Robinson Road 068907 1,485 9.00 13,365 Immediate Penthouse office (Furnished and fitted) Office 1 UOB Plaza 1 No. 80 Raffles Place 1,862 11.00 20,482 Immediate Bare Office 1 UOB Plaza 1 No. 80 Raffles Place 5,253 11.00 1,500 Immediate Fitted Office 1 UOB Plaza 1 No. 80 Raffles Place 5,963 11.00 1,500 Immediate Bare Office 1 UOB Plaza 1 No. 80 Raffles Place 12,206 11.00 134,266 Immediate Bare Office 1 UOB Plaza 1 No. 80 Raffles Place 2,099 11.00 23,089 Immediate Fitted Office 1 UOB Plaza 1 No. 80 Raffles Place 2,454 11.00 26,994 1-May-21 Fitted Office 1 UOB Plaza 1 No. -

A Review of the Singapore Office Market

Singapore Q1/Q2 2019 Published 1st March 2019 Singapore | Hong Kong The Office A review of the Singapore office market Index P2 Building Rental Table (Islandwide) P3 Leasing Options – New Downtown & Economy Range P4 Demand – who is moving where P5 Featured New Development – 9 Penang Road P6 Special Feature – Co-working space P7 Leasing Options – Raffles Place & Tanjong Pagar P8 Supply / Rentals / Forecast Corporate Locations (S) Pte Ltd License No. L3010044A Marina One T +65 6320 8355 / [email protected] / www.corporatelocations.com.sg RENTAL GUIDE 1st March 2019 Summary of Asking Rates Raffles Place / New Downtown Bangkok Bank Building TBA City Hall / Marina Centre / Beach Rd Chinatown / River Valley Road BEA Building $7.50 18 Robinson $12.00 Capital Tower $10.00 11 Beach Road Full Central Mall $7.00 20 Collyer Quay $11.00-$13.00 Cecil Court $5.80 30 Hill Street Full CES Centre $5.50+ 55 Market Street $7.00 China Square Central $8.50 Beach Centre $7.80 Chinatown Point $6.50 6 Battery Road $14.00 City House $7.80+ Bugis Junction Towers $7.80 Great World City $7.00 Asia Square T1 & T2 $14.00 Far East Finance Bldg $7.00 Centennial Tower $14.80 Kings Centre $7.00 Bank of China Building Full Far Eastern Bank Bildg Full Duo Tower $10.50 The Central $9.80 Bank of Singapore Centre $9.50 GB Building $6.00+ Funan $9.00 UE Square $8.00 Bharat Building $6.50 Keck Seng Tower $6.00 Manulife Centre $10.00+ Valley Point $7.00 CapitaGreen $13.50 Manulife Tower $9.50 Millenia Tower $14.80 Capital Square Full MYP Plaza $7.00 Odeon Tower -

Presented by Travel Impressions

Europe Presented by Travel Impressions Best Tour Operator, Sales & Service 2005, 2006, 2007 & 2008 Best Tour Operator, Domestic 2006, 2007 & 2008 2009 2 Trust Travel Impressions for a Smooth Vacation. hether you’re going Travel Impressions has a dedicated MAKE THE MOST OF to the beach, the team of Group Travel Consultants who will YOUR TRAVELS mountains or a help you create memorable group travel Planning your trip through cosmopolitan city, experiences. Our Group Travel Consultants a travel agent is the best there’s nothing that will professionally handle all aspects of way to book your vacation. equals the thrill of your group, from the planning stages Agents have a wealth of experience and feedback Wanticipating your next vacation. Choosing through post trip follow up. They will to draw upon when Travel Impressions ensures you’ll be taken recommend the travel itineraries and travel scheduling your trip, care of every step of the way – from partners that best meet your group specific and they can help the planning stages through travel needs. Additionally, you find the best deals. your return. our outstanding benefits To make your vacation and programs, such as our even more memorable, For over 30 years we’ve optional Cancel For Any Reason be sure to ask about been leading the travel reserving a tour before Travel Protection Plan and industry with comfort and your trip (see the selection 24/7 Customer Care, set convenience. Because we’re in this brochure). This Travel Impressions apart allows you to arrive taken a travel leader having served from the competition. -

Lowry Hotel Offers Five Star Fly Fishng on the Irwell to Guests

LOWRY HOTEL OFFERS FIVE STAR FLY FISHNG ON THE IRWELL TO GUESTS Champion Angler to introduce guests to Manchester’s rivers FLY fishing for trout has the image of a very expensive country pursuit for business execs in the Scottish Highlands. But now the luxury Lowry Hotel is offering fly fishing trips and tuition in Greater Manchester’s rivers for its residents. The Lowry Hotel’s location on the Irwell, which divides Salford and Manchester, has inspired new General Manager Adrian Ellis to team up with fishing champion John Tyzack, who is a member of the oldest angling club in the world, Salford Friendly Anglers which, founded in 1817 has just celebrated its 198 th anniversary. Only 30 years ago the Irwell was considered one of the most polluted rivers in Europe, Now, after a huge clean-up operation led by the Environment Agency, brown trout, grayling, roach, perch, bream and pike can be caught in the waters. The river also supports wildlife, including kingfishers and otters. Says Mr Ellis: “The River Irwell is really making a comeback along with the rest of the area. It is such a marvellous asset and we want to celebrate its rejuvenation.” He adds: “Our guests are increasingly coming from all four corners of the world and expect top-class packages. They can now enjoy superb fishing trips to go with the retail therapy, sports events and fine dining they can experience during their stay here.” The fishing trips, for both beginners and experienced anglers, will be led by full-time professional fly fishing guide and instructor John Tyzack, of Heaton Moor. -

Capitaland Retail China Trust Annual Report 2017 Optimising Growth

OPTIMISING GROWTH CAPITALAND RETAIL CHINA TRUST ANNUAL REPORT 2017 OPTIMISING GROWTH At CapitaLand Retail China Trust (CRCT), we strive to enrich lives through high- quality real estate products and services. Inspired by CapitaLand’s credo of ‘Building People. Building Communities.’, the design for this year’s annual report employs the creative use of mosaic to recreate Rock Square – a new addition to our portfolio. Just as different mosaic pieces come together to form a big picture, this is symbolic of how CRCT will continue to build on our strengths to propel our growth journey and create greater value for the future. We continue to build on the momentum from our milestone decade of growth by sharpening our competitiveness, extracting value and strengthening the quality of our portfolio. Through our strategy of investing in high-quality income-producing retail assets, coupled with proactive asset management and disciplined capital management, we remain focused in creating sustainable long-term value for our Unitholders. VISION MISSION Sustainable and resilient REIT with a Deliver sustainable income growth to our professionally managed portfolio of quality Unitholders and value-add to the community retail real estate across China. and stakeholders by enhancing organic growth through proactive asset management; creating new value through innovative asset enhancement strategies; and capitalising on yield-accretive acquisitions growth. 1 ANNUAL REPORT 2017 CORPORATE PROFILE OVERVIEW FIRST CHINA SHOPPING MALL REAL ESTATE INVESTMENT TRUST IN SINGAPORE CapitaLand Retail China Trust (CRCT) is the first China shopping mall real estate investment trust (REIT) in Singapore. Listed on the Singapore Exchange Securities Trading Limited (SGX-ST) on 8 December CORPORATE GOVERNANCE & TRANSPARENCY GOVERNANCE CORPORATE 2006, CRCT is established with the objective of investing on a long-term basis in a diversified portfolio of income-producing real estate used primarily for retail purposes and located primarily in China, Hong Kong and Macau. -

Www .Mercura.Com

Paul Coupez – CEO Mercura IndustrIes Is a specIalIzed anodIzed aluMInIuM Manufacturer of hIgh qualIty MobIle equIpMent for the hospItalIty sector. our InnovatIve teaM puts Its expertIse at your dIsposal to taIlor the optIMuM www.mercura.com solutIon to your specIfIc needs. We offer a full range of Manoeuvrable, ergonoMIc and durable products froM the front to the back of the house. Mercura Industries s.a. Tel: +32 (0)2 482 11 30 Rue Bois des Îles 15 Fax: +32 (0)2 468 18 48 Eilandenhoutstraat 15 www.mercura.com B-1082 Brussels [email protected] Maquette_Mercura_Hotellerie_HD_3bis_2018 - collin.indd 1 2/10/18 10:44 www.mercura.com www.mercura.com 2 Maquette_Mercura_Hotellerie_HD_3bis_2018 - collin.indd 2 2/10/18 10:44 7 luggage 21 housekeepIng 49 MInI-bar • rooM servIce • caterIng 71 handlIng www.mercura.com 3 Maquette_Mercura_Hotellerie_HD_3bis_2018 - collin.indd 3 2/10/18 10:44 www.mercura.com 4 Maquette_Mercura_Hotellerie_HD_3bis_2018 - collin.indd 4 2/10/18 10:44 www.mercura.com 5 Maquette_Mercura_Hotellerie_HD_3bis_2018 - collin.indd 5 2/10/18 10:44 www.mercura.com 6 Maquette_Mercura_Hotellerie_HD_3bis_2018 - collin.indd 6 2/10/18 10:44 luggage www.mercura.com 7 Maquette_Mercura_Hotellerie_HD_3bis_2018 - collin.indd 7 2/10/18 10:44 optIon Palazzio ● Polished disk with personalised custom logo specIfIcatIons luggage ● Prestigious 'bird-cage' luggage trolley ● In anodised aluminium, robust and light ● Durable anodised gloss fi nish, tarnishfree, low maintenance, no oxidation ● Available in 2 colours: silver or gold ● Hanging rail for garment bags optIon ● Motorized 5th wheel ● Round shaped birdcage or ● Angular shaped birdcage ● Round tube frame Exceptional durability No maintenance www.mercura.com optIon ● Flexible non-marking ● Hoop to retain luggage full wrap-around bumper which can also be used as to protect interior a handle to lift trolley over pavements ● Pneumatic wheels Ø 225 mm Ref. -

MUSLIM VISITOR GUIDE HALAL DINING•PRAYERHALAL SPACES • CULTURE • STORIES to Singapore Your FOREWORD

Your MUSLIM VISITOR GUIDE to Singapore HALAL DINING • PRAYER SPACES • CULTURE • STORIES FIRST EDITION | 2020 | ENGLISH VERSION EDITION | 2020 FIRST FOREWORD Muslim-friendly Singapore P18 LITTLE INDIA Muslims make up 14 percent of Singapore’s population As a Muslim traveller, this guide provides you and it is no surprise that this island state offers a large with the information you need to enjoy your stay variety of Muslim-friendly gastronomic experiences. in Singapore — a city where your passions in life MASJID SULTAN P10 KAMPONG GLAM Many of these have been Halal certified by MUIS, are made possible. You may also download the P06 ORCHARD ROAD also known as the Islamic Religious Council of MuslimSG app and follow @halalSG on Twitter for Singapore (Majlis Ugama Islam Singapura). Visitors any Halal related queries while in Singapore. can also consider Muslim-owned food establishments throughout the city. Furthermore, mosques and – Majlis Ugama Islam Singapura (MUIS) musollahs around the island allow you to fulfill your P34 ESPLANADE religious obligations while you are on vacation. TIONG BAHRU P22 TIONGMARKET BAHRU P26 CHINATOWN P34 MARINA BAY CONTENTS 05 TIPS 26 CHINATOWN ORCHARD 06 ROAD 30 SENTOSA KAMPONG MARINA BAY & MAP OF SEVEN 10 GLAM 34 ESPLANADE NEIGHBOURHOODS This Muslim-friendly guide to the seven main LITTLE TRAVEL P30 SENTOSA neighbourhoods around 18 INDIA 38 ITINERARIES Singapore helps you make the best of your stay. TIONG HALAL RESTAURANT 22 BAHRU 42 DIRECTORY Tourism Court This guide was developed with inputs from writers Nur Safiah 1 Orchard Spring Lane Alias and Suffian Hakim, as well as CrescentRating, a leading Singapore 247729 authority on Halal travel. -

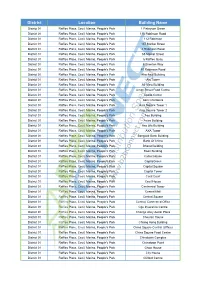

District Location Building Name

District Location Building Name District 01 Raffles Place, Cecil, Marina, People's Park 1 Finlayson Green District 01 Raffles Place, Cecil, Marina, People's Park 110 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 112 Robinson District 01 Raffles Place, Cecil, Marina, People's Park 137 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 4 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park 55 Market Street District 01 Raffles Place, Cecil, Marina, People's Park 6 Raffles Quay District 01 Raffles Place, Cecil, Marina, People's Park 6 Shenton Way District 01 Raffles Place, Cecil, Marina, People's Park 80 Robinson Road District 01 Raffles Place, Cecil, Marina, People's Park Afro-Asia Building District 01 Raffles Place, Cecil, Marina, People's Park Aia Tower District 01 Raffles Place, Cecil, Marina, People's Park Air View Building District 01 Raffles Place, Cecil, Marina, People's Park Amoy Street Food Centre District 01 Raffles Place, Cecil, Marina, People's Park Apollo Center District 01 Raffles Place, Cecil, Marina, People's Park Asia Chambers District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 1 District 01 Raffles Place, Cecil, Marina, People's Park Asia Square Tower 2 District 01 Raffles Place, Cecil, Marina, People's Park Aso Building District 01 Raffles Place, Cecil, Marina, People's Park Aviva Building District 01 Raffles Place, Cecil, Marina, People's Park Axa Life Building District 01 Raffles Place, Cecil, Marina, People's Park AXA Tower District 01 -

Europe Nominee List Updated 26 Aug 2010

Europe Europe Europe's Leading Airline Air France Alitalia British Airways Iberia KLM Lufthansa SAS Scandinavian Airlines Swiss International Air Lines TAP Portugal Turkish Airlines Europe's Leading Airport Amsterdam Airport Schiphol, Netherlands Barcelona International Airport, Spain Copenhagen Airport, Denmark Domodedovo International Airport, Russia Hamburg Airport, Germany Heathrow Airport, London, England HelsinkiVantaa, Finland Leonardo da Vinci International Airport, Italy Lisbon Airport, Portugal Madrid Barajas International Airport, Spain Munich International Airport, Germany Zurich Airport, Switzerland Europe's Leading Airport Hotel Hilton Copenhagen Airport Hotel, Denmark Hilton London Heathrow Airport Hotel, England Kempinski Airport Hotel Munich, Germany Radisson SAS Hotel London Stansted Airport, England Renaissance Barcelona Airport Hotel, Spain Sheraton Amsterdam Airport Hotel and Conference Center, Netherlands Sheraton Paris Airport Hotel & Conference Centre, France Europe's Leading All-inclusive Resort Aldemar Rhodos Paradise Village, Greece Aska Costa Holiday Club, Turkey Club Hotel Riu Chiclana, Spain Club Hotel Riu Gran Canaria, Spain Club Hotel Riu Paraiso Lanzarote Resort, Spain Club Hotel Riu Vista Mar, Spain Concorde De Luxe Resort,Turkey Da Balaia Club Med, Portugal Kemer Resort Hotel, Turkey Rixos Premium Belek, Turkey Titanic Hotel Antalya, Turkey Europe's Leading Beach Cannes, France Corfu, Greece Costa de la Luz, Spain Costa Smeralda, Sardinia, Italy Dona Ana, Lagos, Portugal Formentera Island, Ibiza Marbella,