Barwa Investor Presentation Q1 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cerimã³nia Partida Regresso.Xlsx

Date: 2020-02-21 Time: 09:00 Subject: CoC COMMUNICATION No: 1 Document No: 3:1 From: The Clerk of the Course To: All competitors / crew members Number of pages: 4 Attachments: 1 Notes: FIA SR = 2020 FIA Cross-Country Rally Sporting Regulations QCCR SR = 2020 Manateq Qatar Cross-Country Rally Supplementary Regulations 1. TIMECARD 0 At the reception of administrative checks each crew will receive a timecard which must be used for the following controls: • Administrative checks • Scrutineering • Ceremonial Start holding area IN • Rally Start holding area IN 2. ON-BOARD CAMERAS See article 11 of FIA SR. Competitors wishing to use a camera must supply the following information to the Organizer, in writing, during administrative checks: • Car number • Competitor’s name • Competitor’s address • Use of footage All camera positions and mountings used must be shown and approved during pre-event scrutineering. It is forbidden to mount cameras on the outside of the car. 3. ELECTRONIC EQUIPMENT See article 9 of FIA SR. Any numbers of telephones, mobile phones or satellite phones carried on board must be given to the Organiser during the administrative checks. 4. EQUIPMENT OF THE VEHICLES / “SOS/OK” sign Each competing vehicle shall carry a red “SOS” sign and on the reverse a green “OK” sign measuring at least 42 cm x 29.7 cm (A3). The sign must be placed in the vehicle and be readily accessible for both drivers. (article 48.2.5 of FIA SR). 5. CEREMONIAL START HOLDING AREA (Saturday / Souq Waqif) See article 10.2 of QCCR SR. Rally cars must enter the holding area at Souq Waqif during the time window shown in the rally programme (18.15/18.45h). -

THE QATAR GEOLOGIC MAPPING PROJECT Randall C

LINKING GEOLOGY AND GEOTECHNICAL ENGINEERING IN KARST: THE QATAR GEOLOGIC MAPPING PROJECT Randall C. Orndorff U.S. Geological Survey, 12201 Sunrise Valley Drive, Reston, Virginia, 20192, USA, [email protected] Michael A. Knight Gannett Fleming, Inc., P.O. Box 67100, Harrisburg, Pennsylvania, 17106, USA, [email protected] Joseph T. Krupansky Gannett Fleming, Inc., 1010 Adams Avenue, Audubon, Pennsylvania, 19403, USA, [email protected] Khaled M. Al-Akhras Ministry of Municipality and Environment, Doha, Qatar, [email protected] Robert G. Stamm U.S. Geological Survey, 12201 Sunrise Valley Drive, Reston, Virginia, 20192, USA, [email protected] Umi Salmah Abdul Samad Ministry of Municipality and Environment, Doha, Qatar, [email protected] Elalim Ahmed Ministry of Municipality and Environment, Doha, Qatar, [email protected] Abstract During a time of expanding population and aging urban Introduction infrastructure, it is critical to have accurate geotechnical Currently, the State of Qatar does not have adequate and geological information to enable adequate design geologic maps at regional and local scales with detailed and make appropriate provisions for construction. This descriptions, proper base maps, GIS, and digital geoda- is especially important in karst terrains that are prone to tabases to adequately support future development. To sinkhole hazards and groundwater quantity and quality better understand the region’s geological and geotech- issues. The State of Qatar in the Middle East, a country nical conditions influencing long term sustainability of underlain by carbonate and evaporite rocks and having future development, the Infrastructure Planning Depart- abundant karst features, has recognized the significance ment (IPD) of the Ministry of Municipality and Environ- of reliable and accurate geological and geotechnical ment (MME) of the State of Qatar has commenced the information and has undertaken a project to develop a Qatar Geologic Mapping Project (QGMP). -

Annual Report 2016

ANNUAL REPORT 2016 CONTENTS 3 - 8 BOARD OF DIRECTORS 9 - 10 BOARD OF DIRECTORS REPORT 11 SHARI’A SUPVERVISORY BOARD REPORT 13 - 14 MESSAGE FROM THE GROUP CHIEF EXECUTIVE OFFICER 15 - 16 FINANCIAL HIGHLIGHTS 17 - 18 COMPANY VISION AND STRATEGY 19 CORPORATE GOVERNANCE 21 BARWA REAL ESTATE GROUP 23 - 34 REAL ESTATE PROJECTS IN QATAR 35-36 AL AQARIA REAL ESTATE PROJECTS 37 - 38 INTERNATIONAL INVESTMENTS 39 INDEPENDENT SUBSIDIARIES 40 HELPING PEOPLE FIND THEIR DREAMS 41-42 COMMITMENT TO COMMUNITY 43 OUR EMPLOYEES 1 H.H. SHEIKH TAMIM BIN HAMAD AL THANI THE EMIR OF THE STATE OF QATAR 2 H.H. SHEIKH HAMAD BIN KHALIFA AL THANI THE FATHER EMIR 3 BOARD OF DIRECTORS HIS EXCELLENCY MR. SALAH BIN GHANEM BIN NASSER AL ALI CHAIRMAN OF THE BOARD OF DIRECTORS H.E. Mr. Salah Bin Ghanem Bin was appointed as a consultant in the Nasser Al Ali was appointed as Qatar’s office of the Heir Apparent till 2013. Minister of Sports and Culture on He was also appointed as the General January 27th, 2016 after more than Manager of the Sheikh Jasim Bin two years as Minister of Youth and Mahmoud Bin Thani Foundation Sports. His Excellency held a number for Social Care; a private institute of public positions such as Chief of for public interest established by the State Audit Bureau between His Highness The Father Emir 2006 and 2011, during which Sheikh Hamad Bin Khalifa Al H.E participated in developing a Thani. In 2012, H.E. participated in strategic plan for the Bureau aimed the launch of Al Rayyan TV with a at assisting in achieving sustainable mission to support the renaissance development for the Qatari society of Qatar, consolidate its national and to strengthen accountability. -

District Energy Space2014

■■ North America District Energy Space 2014 Spotlighting Industry Growth More than 120 million square feet reported District■■ North America Energy Space 2014 Industry Growth around the World Dedicated to the growth and utilization of district energy as a means to enhance energy efficiency, provide more sustainable and reliable energy infrastructure, and contribute to improving the global environment. Established in 1909, the International District Energy Association (IDEA) serves as a vital commu- nications and information hub for the district energy industry, connecting industry professionals and advancing the technology around the world. With headquarters just outside of Boston, Mass., IDEA comprises over 2,000 district heating and cooling system executives, managers, engineers, consultants and equipment suppliers from 23 countries. IDEA supports the growth and utilization of district energy as a means to conserve fuel, increase energy efficiency and resilience, and reduce emissions. The publication of District Energy Space has become an annual tradition for the International District Energy Association since 1990. Each year, IDEA asks all of its member systems in North America (compilation initiated in 1990) and beyond North America (compilation initiated in 2004) to provide information on the number of buildings and their area in square feet that committed or recommitted to district energy service during the previous calendar year. This issue compiles growth that was reported for the calendar year 2014, or previously unreported for recent years. To qualify for consideration in District Energy Space, a renewal would have to be a contracted building or space that had been scheduled to expire and was subject to renewal under a contract with a duration of 10 years or more. -

Cool Waterfronts and Coastal Cities: How Qatar’S Peninsula Develops a Resilient Future?

Alraouf, Ali & Al Nuaimi, Mubarak Cool Waterfronts in Qatar 54th ISOCARP Congress 2018 Cool Waterfronts and Coastal Cities: How Qatar’s Peninsula Develops a Resilient Future? Ali A. Alraouf, Ph.D. Mubarak Al Nuaimi, BSc., MA. Eng. Prof. of Architecture and Urbanism Advisor of Urban Planning Affairs Head of CB, Training & Development at Head of Central Doha Project QNMP - MME QNMP - MME Doha, Qatar Doha, Qatar [email protected] [email protected] Abstract The coast is one of the most complex systems on earth as it is the result of the continuous interaction between people, land and water. These physical processes shape the geomorphology of the coast, which sustains specific ecosystems that provide crucial services to human societies to flourish. This paper aims at expanding the understanding on the functioning of the waterfronts, which are crucial factor to increase the awareness regarding the challenges of developing and governing coastal areas and waterfronts. Evidently, climate change represents the major human-induced source of natural risks. Understanding the risks associated to the coast is crucial to provide safe and resilient human environment. Planners must address the challenges of waterfronts and coastal areas’ planning approaches. Coastal cities are facing the challenge not only by providing high quality services for its inhabitants but also to integrate specific coastal and waterfront uses that demand a large quantity of space and requires highly specialized services. Ports, dwellings, beaches, promenades, protectorates, industry, logistics, resorts, restaurants, are just few of the uses that characterized most coastal cities and waterfronts and need to be integrated into the urban fabric and smartly diminish the consequences of climate change. -

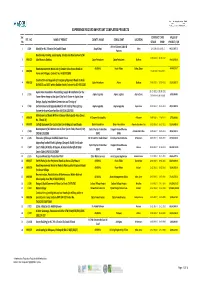

Experience Record Important Completed Projects

EXPERIENCE RECORD IMPORTANT COMPLETED PROJECTS Ser. CONTRACT DATE VALUE OF REF . NO . NAME OF PROJECT CLIENT'S NAME CONSULTANT LOCATION No STRART FINISH PROJECT / QR Artline & James Cubitt & 1 J/149 Masjid for H.E. Ghanim Bin Saad Al Saad Awqaf Dept. Dafna 12‐10‐2011/31‐10‐2012 68,527,487.70 Partners Road works, Parking, Landscaping, Shades and Development of Al‐ 22‐08‐2010 / 21‐06‐2012 2 MRJ/622 Jabel Area in Dukhan. Qatar Petroleum Qatar Petroleum Dukhan 14,428,932.00 Road Improvement Works out of Greater Doha Access Roads to ASHGHAL Road Affairs Doha, Qatar 48,045,328.17 3 MRJ/082 15‐06‐2010 / 13‐06‐2012 Farms and Villages, Contract No. IA 09/10 C89G Construction and Upgrade of Emergency/Approach Roads to Arab 4 MRJ/619 Qatar Petroleum Atkins Dukhan 27‐06‐2010 / 10‐07‐2012 23,583,833.70 D,FNGLCS and JDGS within Dukhan Fields,Contract No.GC‐09112200 Aspire Zone Foundation Dismantling, Supply & Installation for the 01‐01‐2011 / 30‐06‐2011 5 J / 151 Aspire Logistics Aspire Logistics Aspire Zone 6,550,000.00 Tower Flame Image at the Sport City Torch Tower in Aspire Zone Extension to be issued Design, Supply, Installation.Commission and Testing of 6 J / 155 Enchancement and Upgrade Work for the Field of Play Lighting Aspire Logestics Aspire Logestics Aspire Zone 01‐07‐2011 / 25‐11‐2011 28,832,000.00 System for Aspire Zone Facilities (AF/C/AL 1267/10) Maintenance of Roads Within Al Daayen Municipality Area (Zones 7 MRJ/078 Al Daayen Municipality Al Daayen 19‐08‐2009 / 11‐04‐2011 3,799,000.00 No. -

Medical Booklet

Al Khor Community Medical Centre Medical Book TABLE OF CONTENTS MessageM from the Chief Employee Development & Welfare Officer 2 MessageM from the Manager (Medical Services) 3 Important contacts 4 What is Primary Health Care 6 Dependent Eligibility 8 Dental Services 10 Medical Clinic information 12 Specialty Clinic Times 16 What do I do when I arrive? 18 Immunisation clinic 19 Specialty Clinics 30 Pharmacy 31 Laboratory 32 Medical and Dental Claims 32 Authorized sick leave 33 Patients’ Bill of Rights and Responsibilities 35 Suggestions and Complaints 36 AKCMC Medical Team We hhaveave mamaded every effort to keep the information in this booklet accurate. Any changes, updates or circulars will be notified on the share point company web page which employees can access. http://portal/SitePages/Home.aspx MESSAGE From the CHIEF EMPLOYEE DEVELOPMENT & WELFARE OFFICER The continuing success of any community is dependent on the health of its residents. Al Khor Community Medical Centre (AKCMC) offers free, comprehensive medical and dental care to the community. In addition to treating employees and their families, health care indicators are monitored to development preventative strategies to maintain an active, healthy community, and a productive workforce. It has been my pleasure to witness and contribute to the development and expansion of AKCMC, the first JCI accredited Primary Healthcare facility in Qatar. AKCMC maintains bench marked standards and are committed to continuous improvement. Mr Erhama Al Kaabi As you will see in this booklet, AKCMC offers a wide range of services to meet Chief Employee Development & Welfare Officer the ever growing and changing needs of the community. -

LUSAIL Rising from the Heart of the Arabian Peninsula, Qatar Has Become a Beacon of Sustainable and Continuous Growth Over the Past Two Decades

MAISONS BLANCHES LUSAIL Rising from the heart of the Arabian Peninsula, Qatar has become a beacon of sustainable and continuous growth over the past two decades. Led by an ambitious Vision 2030, the country offers unparalleled investment opportunities. And with the World Cup 2022 in its sights, the future is progressively looking brighter for Qatar. It has become the oasis that promises to quench the thirst of thinkers, dreamers and investors. Qatar is an international hub connected to the rest of the world through the Hamad International Airport QATAR where business and lifestyle merge into one cohesive environment, a place that moves ahead of the time, but one that remains always true to its heritage and identity. Major projects currently under development such as Lusail City and Qatar Rail will play a significant role in further boosting the country’s position as a global leader in the fields of urban architecture and property Where Luxury is Reinvented development. Maisons Blanches - Lusail Qatar’s ambitious vision to build a new, sustainable city that reflects its modern times resulted in one of the most grandiose projects today: Lusail City. Lusail City, located on the coast, in the northern part of the municipality of Al Daayen, is a city built for the future, introducing a modern, contemporary lifestyle while embracing the environment. The city is expected to accommodate up to 260,000 people and is a key attraction as part of Qatar’s 2022 FIFA World Cup. Lusail City is only 15 km away from the centre of Doha, and will be connected to the capital via the Qatar Rail LUSAIL CITY project, making commuting between the two cities convenient and efficient. -

Hazm Mebaireek Hospital to Treat Covid-19 Cases

BUSINESS | Page 1 QATAR | Page 20 Ashghal implements preventive Qatar Airways Cargo to measures resume belly-hold cargo to combat operations to China virus spread published in QATAR since 1978 TUESDAY Vol. XXXXI No. 11504 March 31, 2020 Sha’ban 7, 1441 AH GULF TIMES www. gulf-times.com 2 Riyals Hazm Mebaireek Hospital to treat Covid-19 cases QNA Kaabi said that this decision is part of Doha the pre-emptive plan that the health- care sector is implementing to ensure that any possible increase in the number amad Medical Corporation of Covid-19 patients is managed. (HMC) has announced the des- He pointed out that Hazm Mebai- Hignation of Hazm Mebaireek reek General Hospital was specifi cally General Hospital as a facility for treat- chosen to treat Covid-19 patients be- ing coronavirus patients, with the aim cause the hospital will provide a mod- of providing high-quality care for such ern and advanced environment for the patients in an integrated facility. treatment of patients, both men and HE the Minister of Public Health Dr women of all nationalities. Hanan Mohamed al-Kuwari said that the Hazm Mebaireek General Hospital rapid transformation of Hazm Mebaireek has 147 beds, including 42 intensive General Hospital into a facility for treating care beds and 105 inpatient beds. coronavirus patients is an example of the The hospital’s capacity can be in- proactive approach in the healthcare sec- creased to 471 beds (221 beds for inten- tor in the face of this epidemic. sive care and 250 beds for inpatients). She added that the ministry started If needed in the future, it can also pro- to move quickly from the beginning vide a Covid-19 emergency depart- and worked to set standards through ment with a capacity of 150 beds. -

Patient Experience Forum to Be Held on November 16 and 17 Sidra Medicine, Qatar University, Safety

BUSINESSBU | 01 SPORT | 10 QQIIB optimistic Doha events have on growth, become a benchmark expansion for other venues to in 2019 rival: QGF President Monday 25 March 2019 | 18 Rajab 1440 www.thepeninsula.qa Volume 24 | Number 7841 | 2 Riyals New Ooredoo tv Play like a pro Google, Android, Android TV, Chromecast and other related marks and logos are trademarks of Google LLC. Amir to patronise opening of Umm Al Houl Power Plant today THE PENINSULA The project will generate As Qatar is focusing on completion DOHA of strategic projects to meet goals set a daily production under Qatar National Vision 2030, Amir H H Sheikh Tamim bin Hamad Al capacity of 136m gallons H H the Amir in December last year Thani will patronise today the opening of water and 2,520MW also inaugurated the Water Security ceremony of the Umm Al Houl power of electricity. Its full Mega Reservoirs Project, which is the plant, in Umm Al Houl area, south of Al largest of its kind in the world in Umm Wakrah. production capacity will Salal Ali. The QR14.5bn project has a The QR11bn Umm Al Houl Power supply Qatar’s 30 percent total water storage capacity of about project is one of the largest desalination of electricity needs and 1,500m gallons, and was implemented and power generation plants in the 40 percent of water by Qatar General Electricity and Water region. Corporation (Kahramaa). The project will generate a daily requirements. The project is the largest in the production capacity of 136m gallons of world and contains a huge strategic water and 2,520MW of electricity. -

Qatar Real Estate Market Report

QATAR REAL ESTATE MARKET REPORT CONTENTS IN THIS ISSUE ISSUE 1 - MAY 2018 12 Property Trends TRENDS 16 Long Term Price Trends 1 18 Performance Review 30 The Case for Market Transparency 31 Qatar’s Commission Conundrum CONTRIBUTORS 32 Benefits of Property Management Services 2 33 Is Your Property Always Rent-Ready? CONSUMER 36 Top Searched Areas SEARCHES 38 Top Searched Keywords 3 EXPLAINED 39 User Behaviour 42 What Sets Us Apart WE ARE 44 Our Performance 4 PROPERTYFINDER 45 Awesome Agent Winners CONTRIBUTORS Sam Youssef Jeffrey Asselstine Adrian Camps James Townsend Managing Director, Managing Director, Country Director, Managing Director, Better Homes Qatar NelsonPark Property LCC Colliers Absolute Qatar BACKGROUND Sam established BACKGROUND Jeffrey founded BACKGROUND Adrian has BACKGROUND With a decade Better Homes Qatar in 2009 and NelsonPark Property nine years over 35 years’ experience, with of experience in the real estate has over 15 years of experience ago and has continued to lead 11 years spent in the GCC of market in Qatar and the GCC, in the real estate market. He has as its Managing Director. Armed which the last six years were James has know-how in both been instrumental in leading with a BBA from Wilfrid Laurier Qatar based. Heading the the residential and commercial Better Homes Qatar through University, and as a Chartered Colliers Qatar country team, fields. For seven years, he was remarkable growth and has Financial Analyst (CFA), he has he provides key property running his own agency, prior spearheaded the introduction of spearheaded the development advice to corporations and to launching Absolute Qatar. -

Karwa Smartcard - Merchant Name, Area and Tel No

Karwa Smartcard - Merchant Name, Area and Tel No: 1.Doha Bus StationAl Ghanim 44366053 2.Royal Mobile (Food World)Industrial (Food World) 77339666 3.Abdulla Ali Food StuffCentral Market 44683736 4.Safari Shopping ComplexUm Salal Mohamad 44792840 5.Kabayan SupermarketSouq Asiri (Pilipino Souq) 55712164 6.Al Isma trading Co. W.L.L.Musherib St 44327360 7.Landmart HyperStreet 49 Industrial 44504400 8.Faz SupermarketStreet 36, Industrial Area 44600538 9.AL-Harabi Trading CentreAl Khor 44720542 10.Family Shopping ComplexMuaither Str 44509726 11.Farhana Studio Shahaniya 77459300 12.Danube SupermarketIndustrial Area 44606285 13.Al-Rawabi ElectronicsRayyan 77987738 14.G-Mart Mansoura 44214756 15.Safwa Super MarketMusiereb 44310224 16.Safari HypermarketAin Khalid, Salwa Road 44696196 17.Regency HypermarketAbu Hamour 44505500 18.Trendz Doha CentreAl Khor 77372171 19.Top GroceryAl Ghanim Bus station 55857990 20.Skynet Co. W.L.L.Wathana Mall (Maiether) 66562010 21.Jassela SupermarketUmn Qarn 44729513 22.Al Fida GroceryBin Omran 44873036 23.Sana GroceryBin Omran 44886364 24.Absad CaferteriaAl Ghanim Bus station 44432819 25.Foto GulfIndustrial 77475505 26.United TelecomAl Meera – Muntaza 77463007 27.Qatar Forsan ComplexSt. 33, Industrial Area 44604756 28.Skynet Food Salwa 55212365 29.Al Raya GroceryAl Laqta 44883845 30.Doha Colour studioArab Roundabout 33534474 31.Al Falah SupermarketNew Wakra 55195049 32.New Abudhabi SupermarketBin Mammoud 44431772 33.Foto GulfBarwa Village (Wakra) 44425044 34.Dubai StudioMatar Qadem 44650730 35.Al Saniya Mobile CenterAlsaad