Single Audit Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Firu,Tvozzr+ Ot, +O Pu

SU}1}4ARY REPT.GROUP DETAIL PENNINGTON COUMTY, SD REPORT-EL4sA PAGE OOi GENEML ELECTIOI{ NOVEMBER 4, 2014 firu,tvozzr+ ot, +o pu TOTAL VOTES Z ABSENTEE ELECTION DAY PROVI SIOML PRECINCTS COUNTED (OF 471 47 100.00 REGISTERED VOTERS . TOTAL 64,419 MLLOTS CAST . TOTAL. 34.004 8,996 25.004 MLLOTS CAST . ELAI{K. 2 .01 0 VOTER TURI'IOUT . TOTAL 52.79 VOTER TURI{O{JT . BTAIIK United States Senator PENNINGToN couNTY You nay vote for up to 1 Rick l,liei land ( DEH) 8,2M 24.45 2,L90 6,054 0 llike Rounds (REP). 18.812 55.79 13,583 2 Gordon Howie ( IND) 1,223 3.63 226 995 2 Larry Pressl er (IND). 5,439 16.13 L.289 4,150 0 United States ReDresentative PENNINGToN CoUNTY You nay vote for up to I Corinna Robinson (DEM) L0.L25 30.25 2,780 7 ,345 Kri sti Noem (REP). 23,350 69.75 6,094 r7 ,252 Governor and Lieutenant Governor PENNINGIoN CoUllTY You tnay vote for up to 1 Susan wismer / Susy Elake (DEtl) 7,551 22.57 2,089 5,462 0 Dennis Daugaard / l.latt tlichels (REP) 24.340 72.75 6,409 L7 ,927 4 Aeel J. Myers / Lora Hubbel (IND) 1.564 4.67 361 1,203 0 Secretary of State PENNII{GToN CoUNW You may vote for up to 1 Lori Stacey (CoN). 1,349 4.29 297 1,051 1 Ennnett Reistroffer (LIB) r,206 3.83 270 936 0 Angel ia Schultz (DEM) 8.541 27.r3 2.393 6,148 0 Shantel Krebs (REP) . -

TABLE 4.30 State Comptrollers, 2019

AUDITORS AND COMPTROLLERS TABLE 4.30 State Comptrollers, 2019 Elected Civil service Legal Method Approval or Length comptrollers or merit basis for of confirmation, of maximum system State Agency or office Name Title office selection if necessary term consecutive terms employee Alabama Office of the State Comptroller Kathleen Baxter State Comptroller S (c) AG (b) . « Alaska Division of Finance Dan BeBartolo Acting Division Director S (d) AG (a) . « Arizona General Accounting Office D. Clark Partridge State Comptroller S (d) AG (b) . Dept. of Finance and Larry Walther Chief Fiscal Officer, Arkansas Administration Director S G . (a) . Office of the State Auditor Andrea Lea State Auditor Office of the State Controller Betty Yee (D) State Controller California C E . 4 yrs. 2 terms . Department of Finance Todd Jerue Chief Operating Officer Department of Personnel and Colorado Bob Jaros State Controller S (d) AG (o) . « Administration Connecticut Office of the Comptroller Kevin P. Lembo (D) Comptroller C E . 4 yrs. unlimited . Director, Division of Delaware Dept. of Finance Jane Cole S G AL (a) . Accounting Florida Dept. of Financial Services Jimmy Patronis Chief Financial Officer C,S E . 4 yrs. 2 terms . State Accounting Georgia State Accounting Office Alan Skelton S G . (a) . Officer Dept. of Accounting and General Hawaii Curt Otaguro State Comptroller S G AS 4 yrs. Services Idaho Office of State Controller Brandon Woolf State Controller C E . 4 yrs. 2 terms . Illinois Office of the State Comptroller Susana Mendoza (D) State Comptroller C E . 4 yrs. unlimited . Indiana Office of the Auditor of State Tera Klutz Auditor of State C E . -

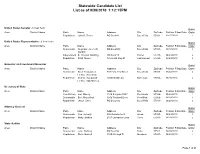

Statewide Candidate List List As of 9/30/2010 1:12:15PM

Statewide Candidate List List as of 9/30/2010 1:12:15PM United States Senator - 6 Year Term Ballot Area District Name Party Name Address City ZipCode Petition Filing Date Order Republican John R. Thune PO Box 841 Sioux Falls 57101- 03/17/2010 2 United States Representative - 2 Year Term Ballot Area District Name Party Name Address City ZipCode Petition Filing Date Order Democratic Stephanie Herseth PO Box 2009 Sioux Falls 57101- 03/17/2010 3 Sandlin Independent B. Thomas Marking PO Box 219 Custer 57730- 04/29/2010 4 Republican Kristi Noem 18575 US Hwy 81 Castlewood 57223- 03/23/2010 2 Governor and Lieutenant Governor Ballot Area District Name Party Name Address City ZipCode Petition Filing Date Order Democratic Scott Heidepriem 503 East 21st Street Sioux Falls 57105- 03/04/2010 3 Lt. Gov - Ben Arndt Republican Dennis Daugaard 24930 480th Ave Garretson 57030- 03/15/2010 2 Lt. Gov - Matt Michels Secretary of State Ballot Area District Name Party Name Address City ZipCode Petition Filing Date Order Constitution Lori Stacey 1109 S. Lyons #327 Sioux Falls 57104- 06/23/2010 1 Democratic Ben Nesselhuf 1016 Westend Drive Vermillion 57069- 06/29/2010 3 Republican Jason Gant PO Box 2012 Sioux Falls 57101- 06/28/2010 2 Attorney General Ballot Area District Name Party Name Address City ZipCode Petition Filing Date Order Democratic Ron Volesky 592 Dakota Ave S. Huron 57350- 06/29/2010 3 Republican Marty Jackley 2101 Lancaster Loop Pierre 57501- 06/28/2010 2 State Auditor Ballot Area District Name Party Name Address City ZipCode Petition Filing Date Order Democratic Julie Bartling PO Box 256 Burke 57523- 06/29/2010 3 Republican Steve Barnett 1010 N. -

NASACT News, November 2014

KEEPING STATE FISCAL OFFICIALS INFORMED VOLUME 34, NUMBER 11 | NOVEMBER 2014 NASACT WEATHERS 2014 ELECTION SEASON With 48 member seats in question, the November worked on legislation that eventually became 2014 elections carried the potential for signifi cant Act 1088, which regulates the state’s treasury change within NASACT’s member ranks. management practices and procedures to ensure Elections results aff ecting member offi ces are prudent investment and management of public funds outlined below by state. Questions about this article entrusted to the state treasurer. Milligan will replace may be directed to Neal Hutchko, policy analyst, at Charles Robinson, who was named temporarily [email protected] or (202) 624-5451. in May 2013 to replace former treasurer Martha Shoff ner and was not eligible for re-election. ALABAMA CALIFORNIA Treasurer: Young Boozer, III (R), running unopposed, retained his seat. Th is will be his second Comptroller: Betty Yee (D) won her race to become term as state treasurer. the new state controller. She previously served as the chief deputy director for budget with the California ARIZONA Department of Finance. She earned her bachelor Treasurer: Jeff DeWit (R), who ran unopposed, is of arts degree in sociology from the University of Arizona’s new state treasurer. DeWit is an investment California, Berkeley, and her master’s degree in public professional and soft ware company owner with a administration from Golden Gate University, San degree from the University of Southern California Francisco. She replaces John Chiang, who was term in business administration and a minor in fi nance. limited. He will replace Doug Ducey, who ran a successful Treasurer: John Chiang (D) won the state treasurer campaign for governor. -

2017 Annual Report (Pdf)

OFFICE OF THE STATE TREASURER FISCAL YEAR 2017 ANNUAL REPORT RICHARD L. SATTGAST STATE TREASURER OF SOUTH DAKOTA STATEMENT OF PURPOSE SUMMARY --- The South Dakota State Treasurer shall be the custodian of all monies paid into the state treasury; keep an accurate account of the receipts and disbursements of the various accounts within the state’s accounting system; monitor the investments of cash by the State Investment Office; secure the deposits of all public funds; and administer the South Dakota Uniform Unclaimed Property Act. SELECT LEGAL CITATIONS-----Election ----powers and duties. S.D. Const. art. IV, § 7. General duties, SDCL 1-10-1. Annual report to Governor, SDCL 1-10-2. Appointment of deputy, SDCL 1-10-4. Public officers and employees, SDCL title 3. Official bonds, SDCL 3-5-3. Full-time devoted to duties of office, SDCL 3-8-1. State Board of Finance, SDCL ch. 4-1. Funds maintained in treasury – Local bank accounts, SDCL 4-4-3. Funds, SDCL 4-5-1. Custody and investment of state funds, SDCL titles 4 and 5. Depositories of public funds, SDCL ch. 4-6. Insurance of public deposits, SDCL ch. 4-6A. Authority for state expenditures, acceptance and disbursement of federal funds, SDCL chs. 4-8 and 4-9. Accounts of receipts and disbursements, SDCL 4-10-1. Reconciliation of accounts – adjustments and transfers, SDCL 4-10-4. Uniform Unclaimed Property Act, SDCL ch. 43- 41B. STATE TREASURY STAFF Richard L. Sattgast State Treasurer Rik Drewes Deputy State Treasurer Sandy Tillman Banking Operations Manager Marianne Gabriel Finance Officer/Deposits -

NASACT News, September 2014

KEEPING STATE FISCAL OFFICIALS INFORMED VOLUME 34, NUMBER 9 | SEPTEMBER 2014 ONE HUNDRED YEARS OF SERVICE BY WILLIAM G. HOLLAND, PRESIDENT OF NASACT, 2014-15 I’m honored to be president of the National remained valuable for the simple reason that, from its Association of State Auditors, Comptrollers and beginning, it has risen above the present to envision Treasurers during its centenary celebration. In its the future. early years, NASACT’s mission was to “promote As members of NASACT, we could, at this juncture, economy, effi ciency and uniformity in public look back and be satisfi ed with the contributions auditing and handling public funds.” A century we have made to governmental accountability and later our mission continues to be to assist state transparency. I think it’s appropriate to indulge that leaders to “enhance and promote eff ective and inclination for a few congratulatory handshakes. effi cient management of governmental resources.” Th en, let’s return our focus to the years ahead. Th ere Unchanged is the underlying commitment to is still much to be done. responsible public service. Involvement in NASACT will enhance your Imagine, in an era when transcontinental phone professional knowledge on salient topics like pension service was just getting started and automobile reform, federal/state oversight, cybercrime, evolving travel between New York and California took information technologies and data sharing, debt weeks, NASACT had the vision to embrace fi nancial management, tax policies and professional standards. management professionals—treasurers, comptrollers Mark your calendars for the 2015 NASACT Annual and auditors—from all across the United States. -

State Pages 2011

sTaTe Pages Alabama Alaska Nickname .....................................................................The Heart of Dixie Nickname .......................................................................The Last Frontier Motto ......................................................Aldemus Jura Nostra Defendere Motto ............................................................................North to the Future (We Dare Defend Our Rights) Flower ................................................................................ Forget-Me-Not Flower ...........................................................................................Camellia Bird ................................................................................ Willow Ptarmigan Bird .....................................................................................Yellowhammer Tree ..........................................................................................Sitka Spruce Tree ................................................................... Southern (Longleaf) Pine Song ........................................................................................Alaska’s Flag Song ...............................................................................................Alabama Entered the Union ............................................................ January 3, 1959 Entered the Union ......................................................December 14, 1819 Capital ............................................................................................. -

Oct. 25, 2018 A-2 Pastor’S Perspective This Week’S Pastor’S Perspective Is Provided by Pastor Del Neumeister of Belle Fourche and St

PRSRT STD U.S. POSTAGE PAID BELLE FOURCHE, SD ECRWSS Belle Fourche Beacon Permit No. 23 100th Black Hills Roundup 252 DAYS to July 4th, 2019 *********ECRWSSEDDM**** Postal Customer VOL. 1 ISSUE 10 Belle Fourche, SD Thursday October 25, 2018 $1.25 BELLE FOURCHEBeacon - Today, October 25, 2018, We enjoy reading.” Each Week with this tenth issue of the Belle Fourche Beacon Beacon, “We’ve found the paper to be ‘outstand- we mark the beginning of weekly publication. It ing’. So far-” has always been the goal of the Beacon to become Beacon, “We thoroughly enjoy the paper! Keep a weekly paper. A task found to be easier said than up the good work!!” done. The paper owes the accomplishment of that Beacon, “The Beacon is exactly what a paper task to you, the readers. We totally underestimated should be. Local news and events. I believe that the overwhelming response and support that you promoting what is coming up is what sells papers have given and continue to give the Beacon. and brings people to town.” The kind and generous comments we receive Parallel to reader/subscriber support has been daily would fill a book. the response of the business community. Their Below is a representative sample of the many use of the Beacon as an advertising tool is again comments you have sent: proving that good local newspapers work. It works Beacon, “Hi! We have been enjoying the paper for them because you, the readers, shop locally very much and decided we should get a subscrip- and support your local businesses. -

Sota Per Copy STANDARD Inside This Sota U.S

PRESORTED Sota Per Copy STANDARD Inside this Sota U.S. POSTAGE From the office of Tribal Chairman Flute: SWST acts to stop meth epidemic PAID WILMOT, SD Tribal Self-Governance of IHS public meeting next Wednesday, Aug. 16th PERMIT NO. 1 Special feature: Trauma Informed Training comes to Lake Traverse Reservation Change service requested Update on Dakota Crossing grocery store project, Dakota Magic, and Dakota Connection Sota Iya Ye Yapi, P.O. Box 5, Wilmot, SD 57279 ¢ Sisseton Public Schools Superintendent resigns Contents – Time-Dated News/Do Not Delay June 2017 Tribal Council proceedings Mailed at Wilmot, SD, Monday, Aug. 7, 2017 75 Reminder: Deadline to submit copy for consideration in the Sota is Friday noon Publication of the Sisseton-Wahpeton Sioux Tribe of the Lake Traverse Reservation since 1968 Vol. 48 August - Canpa Sapa Wi - “Moon of Black Chokecherries” - Anpetu Iyamni - August 9, 2017 No. 32 Agency Village, SD – Aug. 2, 2017 – In 2013 people from our Reservation that contribute to the newly elected 2017 Tribal leadership. However, upon completion of serving time, and 2014, many headlines were created that recognized methamphetamine problem. Today, the Sisseton-Wahpeton Sioux Tribe’s completion of treatment, completion of community the methamphetamine problem in Indian country. In 2016, Tribal leadership took an active Tribal Council passed a new Tribal law, the Controlled service hours and all fines paid in full the Tribal member The Lake Traverse Reservation also created headlines and aggressive approach against hard drugs in our Substance Act. will be given an opportunity to be accepted back into that echoed the problem and there was an attempt to community by requesting assistance from the Bureau of This new law will give SWST Tribal Justice the Tribal community and allowed on Tribal properties. -

NAST State Treasury Profiles 2013

NAST State Treasury Profiles 2013 www.nast.org Copyright 2013 NatioNal assoCiatioN of state treasurers the Council of state Governments 2760 research Park Drive P.o. Box 11910 lexington, KY 40578-1910 www.nast.org special thanks treasury profile information for this publication was submitted by treasury office staff. Table of Contents IntroDuCtioN ............................................................................................................................iv About NAST ..................................................................................................................................v NAST affiliates ..........................................................................................................................vi 2013 NAST CoNferences ...................................................................................................... vii 2013 NAST exeCutive Committee ................................................................................... viii alPhaBetiCal list .................................................................................................................... 1 treasurY Profiles, alaBama – WYoming .................................................................... 2 AppendiCes treasurY CoNtaCt InformatioN ..........................................................................................................103 state treasurers, 1976–PreseNt ...........................................................................................................107 NAST staff memBers....................................................................................................................................