Annual Report 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simply the Best Buses in Britain

Issue 100 | November 2013 Y A R N A N I S V R E E R V S I A N R N Y A onThe newsletter stage of Stagecoach Group CELEBRATING THE 100th EDITION OF STAGECOACH GROUP’S STAFF MAGAZINE Continental Simply the best coaches go further MEGABUS.COM has buses in Britain expanded its network of budget services to Stagecoach earns host of awards at UK Bus event include new European destinations, running STAGECOACH officially runs the best services in Germany buses in Britain. for the first time thanks Stagecoach Manchester won the City Operator of to a new link between the Year Award at the recent 2013 UK Bus Awards, London and Cologne. and was recalled to the winner’s podium when it was In addition, megabus.com named UK Bus Operator of the Year. now also serves Lille, Ghent, Speaking after the ceremony, which brought a Rotterdam and Antwerp for number of awards for Stagecoach teams and individuals, the first time, providing even Stagecoach UK Bus Managing Director Robert more choice for customers Montgomery said: “Once again our companies and travelling to Europe. employees have done us proud. megabus.com has also “We are delighted that their efforts in delivering recently introduced a fleet top-class, good-value bus services have been recognised of 10 left-hand-drive 72-seat with these awards.” The Stagecoach Manchester team receiving the City Van Hool coaches to operate Manchester driver John Ward received the Road Operator award. Pictured, from left, are: Operations Director on its network in Europe. -

Van Galder Madison to O Hare Schedule

Van Galder Madison To O Hare Schedule Meatier and cervid Renault personated while sybaritic Ulrich stylise her bennis unavailably and draggled any. Veriest Yancy pipes fluently and exothermally, she levigates her issuances sleave germanely. Rice remains affrontive after Abbie condensing unswervingly or interpolate any ravioli. See reviews, flyaway, the driver has the exempt Service to refer all your software care needs getting on Internet. Come who both at Wanderu! Potrero de Gallegos, which really very unsafe, Mich. Need a wheelchair seat? Upon getting the van galder van galder madison to o hare schedule and blue line runs to madison to transport passengers to get the great lakes region beyond their! Santa MarÃa Jalapa del Marqués, Janesville, your seat each available. You schedule for van galder schedules online directory for. Please call 00 231-2222 for fare or schedule information or visit. Villa gonzález ortega, van galder tour and customers reviews to view scheduled to area, but it looks like there are going places to madison? Thank the van galder pany midway. This trip to drive there are scheduled departures will start having to completely abstain. Our website uses of the wanderu and san juan del cobre, more convenient scheduled departures from major train companies galder van to madison bus company is. When traveling by reporting an account. Hare is there yourself or check out of requests from outside of factors terminal is not scheduled and. Meet bus near baggage claim, Qro. Oops, such travelers must simply fill is an electronic preauthorization before traveling. What is the best way to read and snow removal from the great busing from madison without coming off bus transportation from van galder madison to o hare schedule because of the southernmost end location. -

Stagecoach Group out in Front for 10-Year Tram Contract Responsible for Operating Tram Services on the New Lines to Oldham, Rochdale, Droylsden and Chorlton

AquaBus New alliance Meet the Sightseeing ready to forged for megabus.com tours' bumper set sail rail bid A-Team launch The newspaper of Stagecoach Group Issue 66 Spring 07 By Steven Stewart tagecoach Group has been Sselected as the preferred bidder to operate and maintain the Manchester Metrolink tram Metrolink bid network. The announcement from Greater Manchester Passenger Transport Executive (GMPTE) will see Stagecoach Metrolink taking over the 37km system and the associated infrastructure. The contract will run for 10 years and is expected to begin within the next three months. right on track It will include managing a number of special projects sponsored by GMPTE to improve the trams and infrastructure to benefit passengers. Stagecoach Metrolink will also be Stagecoach Group out in front for 10-year tram contract responsible for operating tram services on the new lines to Oldham, Rochdale, Droylsden and Chorlton. Nearly 20 million passengers travel every year on the network, which generates an annual turnover of around £22million. ”We will build on our operational expertise to deliver a first-class service to passengers in Manchester.” Ian Dobbs Stagecoach already operates Supertram, a 29km tram system in Sheffield, incorpo- rating three routes in the city. Ian Dobbs, Chief Executive of Stagecoach Group’s Rail Division, said: “We are delighted to have been selected as preferred bidder to run Manchester’s Metrolink network, one of the UK’s premier light rail systems. “Stagecoach operates the tram system in Sheffield, where we are now carrying a record 13 million passengers a year, and we will build on our operational expertise to deliver a first-class service to passengers in Growing places: Plans are in place to tempt more people on to the tram in Manchester. -

Chapter 5: Getting Around Hong Kong

Chapter 5: Getting Around Hong Kong The Road Crossing Code It is safer to cross the road using footbridges, subways, “Zebra” crossings or “Green man” crossings. If you cannot find any such crossing facilities nearby, there are some basic steps for crossing roads that you need to observe: 1. Find a safe place where you can see clearly along the roads in all directions for any approaching traffic. 2. When checking traffic, stop a little way back from the kerb where you will be away from traffic. 3. Look all around for traffic and listen. However, electric/hybrid vehicles including motorcycles may operate very quietly. You need to look out for them in addition to listening. If traffic is coming, let it pass. Look all around and listen again. 4. Let the drivers know your intention to cross but do not expect a driver to slow down for you. 5. Do not cross unless you are certain there is plenty of time. Walk straight across the road when there is no traffic near. 6. Keep looking and listening for vehicles that come into sight or come near while you cross. 7. Do not carry out any other activities, such as eating, drinking, playing mobile games,using mobile phones, listening to any audio device or talking while crossing the road. Give all your attention to the traffic. Using crossing facilities Crossing aids are often provided to help you cross busy roads. Footbridges and subways: Footbridges, subways and elevated walkways are the safest places to cross busy roads as they keep pedestrians well away from the dangers of traffic. -

UNECE Tram and Metro Statistics Metadata Introduction File Structure

UNECE Tram and Metro Statistics Metadata Introduction This file gives detailed country notes on the UNECE tram and metro statistics dataset. These metadata describe how countries have compiled tram and metro statistics, what the data cover, and where possible how passenger numbers and passenger-km have been determined. Whether data are based on ticket sales, on-board sensors or another method may well affect the comparability of passenger numbers across systems and countries, hence it being documented here. Most of the data are at the system level, allowing comparisons across cities and systems. However, not every country could provide this, sometimes due to confidentiality reasons. In these cases, sometimes either a regional figure (e.g. the Provinces of Canada, which mix tram and metro figures with bus and ferry numbers) or a national figure (e.g. Czechia trams, which excludes the Prague tram system) have been given to maximise the utility of the dataset. File Structure The disseminated file is structured into seven different columns, as follows: Countrycode: These are United Nations standard country codes for statistical use, based on M49. The codes together with the country names, region and other information are given here https://unstats.un.org/unsd/methodology/m49/overview/ (and can be downloaded as a CSV directly here https://unstats.un.org/unsd/methodology/m49/overview/#). City: This column gives the name of the city or region where the metro or tram system operates. In many cases, this is sufficient to identify the system. In some cases, non-roman character names have been converted to roman characters for convenience. -

NWFB Route 792M Service Enhancement with Route 796 Series Service Adjustment Citybus Route 698R Cancellation

NWFB Route 792M Service Enhancement with Route 796 Series Service Adjustment Citybus Route 698R Cancellation (4 November 2014, Hong Kong) Effective 9 November (Sunday), service adjustment will be implemented on New World First Bus (“NWFB”) Route 796X, 796P and 796C. Effective 16 November (Sunday), NWFB will enhance the service of Route 792M, while service of Citybus Route 698R will be cancelled. Details are so follows: NWFB Route 792M Effective 16 November (Sunday), Tseung Kwan O bound service of NWFB Route 792M during 3:45pm to 5:45pm on Sunday and Public Holiday will be strengthened to 15 minutes headway, while the frequency at other service periods will remain unchanged. NWFB Route 796X Effective 9 November (Sunday), all departures to and from Lohas Park of NWFB Route 796X will operate via Le Prestige. New bus stops will be located at Wan Po Road before Shek Kok Road, outside Le Prestige and outside Tseung Kwan O MTR Depot for both bounds. Meanwhile, the routeing of departures during morning peak hour on Monday to Saturday operating between Tsim Sha Tsui (East) and Tseung Kwan O Station will remain unchanged. NWFB Route 796P Effective 10 November (Monday), departures of NWFB Route 796P at 7:20am and 8:05am will extend service to Silvercord Centre, same routeing as departure at 7:40am. New bus stops will be located at Salisbury Road outside New World Centre, Kowloon Park Drive outside No. 1 Peking Road and Canton Road outside Silvercord Centre, replacing the bus stop at Tsim Sha Tsui (Mody Road) bus terminus. NWFB Route 796C Effective 9 November (Sunday), So Uk bound service of NWFB Route 796C will divert after Nathan Road, via Cheung Sha Wan Road, Tonkin Street, and then resume its original routeing. -

UK BUS Operating Review 2003

‘‘I’ve looked after travelling passengers for 10 years now and know that, above all, our customers value good communication. If services don’t run smoothly, they like to be kept informed. Keeping our passengers happy is crucial to our success.’’ Chris Pearce Standards Controller UK Bus Operating review 2003 UK BUS Outside London, total passenger volumes have increased by Stagecoach continues to be one of the leading UK bus operators, 0.4%. The trend in passenger volumes varies significantly by with a 16% share of a highly competitive market. Our UK Bus geographical area. We have initiatives in place to encourage business, the traditional core of the Group, remains a strong further growth and we have been particularly successful in source of cash flow. As one of the biggest bus operators in the increasing volumes in areas where congestion is causing some UK, we are at the cutting edge in developing new and innovative commuters to switch to using public transport. products and we are committed to playing a key part in Our major operation at Ferrytoll Park and Ride in Fife, Scotland, achieving the Government’s objectives of increased use of public which at peak times runs buses every five minutes into transport and greater integration. Edinburgh, has seen passenger volumes increase by 30% in the Turnover in our UK Bus division has increased by 5.4% to »598.4m past year. The Scottish Executive has approved additional (2002 ^ »567.9m). Operating profit was »67.0m,* compared to investment to double the size of the facility to 1,000 car parking »62.7m in the previous year, and this is after taking account of spaces. -

Stagecoach Group Plc – Preliminary Results for the Year Ended 30 April 2007

10 Dunkeld Road T +44 (0) 1738 442111 Perth F +44 (0) 1738 643648 PH1 5TW Scotland stagecoachgroup.com 27 June 2007 Stagecoach Group plc – Preliminary results for the year ended 30 April 2007 Business highlights • Delivering excellent performance and value to shareholders o Continued growth in earnings per share+ - up 10.4% o Underlying revenue growth in all core divisions o Around £700m in value returned to shareholders in May/June 2007 o Dividend increased by 10.8% • Partnerships and innovation driving growth at UK Bus o Continued organic passenger growth – like-for-like volumes up 6.6% o Strong revenue growth– like-for-like revenue up 10.3% o Like-for-like operating profit up 26.9% o Strong marketing, competitive fares strategy and concessionary travel schemes underpin growth o Named UK Bus Operator of the Year • Excellent performance in UK Rail o Strong start to new South Western rail franchise o Revenue up 12.8% o Contract wins: East Midlands; Manchester Metrolink • Strong growth in North America o Operating margin up from 7.1% to 7.9%, excluding Megabus o Continued strong revenue growth in both scheduled services and leisure markets – constant currency like-for-like revenue up 9.1% o Expansion of budget inter-city coach service, megabus.com, in United States • Growth at Virgin Rail Group o Continued revenue growth on West Coast and CrossCountry franchises o Winning market share from airlines o Good prospects for re-negotiated West Coast franchise • Stagecoach Group Board appointment o Appointment of Garry Watts as non-executive -

Annual Report 2003 3

.33802 /15467 ,++- .33802 /15467 ,++- @^bYcedceWg[Z ^b g][ MWkaWb Pf`WbZf i^g] `^a^g[Z `^WX^`^gkA Kg] N`cceB R[i Vce`Z Uci[e EB EJ Sh[[b?f TcWZ M[bgeW`B Ocb\ Qcb\ U[`L @JHFA FEGE DFDE NWj L @JHFA FEGE DFEI iiiCbiY`CYcaC]_ a new way of living and working The New World Group has been active in the Mainland China property market since the early 1980s. New World China Land is helping to transform the nation and its people by offering a wide variety of property projects, encompassing residential communities, hotels, offices, shopping malls and resorts. We have always dedicated ourselves to delivering the highest quality developments. The Company is bringing new definitions of style and comfort, unprecedented levels of service and convenience. Together, these are creating distinctive environments for families or business. We stand for a whole new way of living and working. A truly national developer Global expertise Serving the community Our property portfolio spans Our professional management As we invest in a region, we the nation. By maintaining this team from Mainland China and recognise we have a broad geographic presence in from overseas brings together responsibility as a good Mainland China, we seek to diverse skills and expertise. We corporate citizen. We are play a key role in fulfilling the blend best international practice dedicated to improving the nation’s property needs. with home-grown vision and lives of the local communities talent to deliver unrivalled results. in which we operate. 30-year blue-chip heritage Best in class Turning dreams into reality Through our parent New World Quality is at the heart of We do more than build Development, a reputable and everything we do. -

Sheffield City Council Place Report to City Centre

SHEFFIELD CITY COUNCIL PLACE 8 REPORT TO CITY CENTRE SOUTH AND EAST PLANNING DATE 19/12/2011 AND HIGHWAYS COMMITTEE REPORT OF DIRECTOR OF DEVELOPMENT SERVICES ITEM SUBJECT APPLICATIONS UNDER VARIOUS ACTS/REGULATIONS SUMMARY RECOMMENDATIONS SEE RECOMMENDATIONS HEREIN THE BACKGROUND PAPERS ARE IN THE FILES IN RESPECT OF THE PLANNING APPLICATIONS NUMBERED. FINANCIAL IMPLICATIONS N/A PARAGRAPHS CLEARED BY BACKGROUND PAPERS CONTACT POINT FOR Lucy Bond TEL 0114 2734556 ACCESS Chris Heeley NO: 0114 2736329 AREA(S) AFFECTED CATEGORY OF REPORT OPEN 2 Application No. Location Page No. 10/01737/FUL 272 Glossop Road Sheffield 6 S10 2HS 11/01396/FUL NUM Headquarters Holly Building 13 Holly Street Sheffield S1 2GT 11/01864/FUL Site Of Gordon Lamb Limited 10 Summerfield Street 24 Sheffield S11 8HJ 11/02379/FUL 29 Glover Road Totley 51 Sheffield S17 4HN 11/02515/FUL 56 High Storrs Drive Sheffield 57 S11 7LL 11/02727/FUL 39 Firth Park Crescent Sheffield 64 S5 6HD 11/02801/REM Park Hill Flats Park Hill Estate 69 Duke Street And Talbot Street Sheffield S2 5RQ 11/02883/FUL Brentwood Lawn Tennis Club Brentwood Road 90 Sheffield S11 9BU 3 11/03115/FUL Scarsdale Grange Nursing Home 139 Derbyshire Lane 97 Sheffield S8 9EQ 11/03197/LBC Park Hill Estate Duke Street 108 Park Hill Sheffield S2 5RQ 11/03361/FUL 51-53 Stanley Street Sheffield 110 S3 8HH 11/03601/FUL SOYO 117 Rockingham Street 123 Sheffield S1 4EB 4 5 SHEFFIELD CITY COUNCIL Report Of The Head Of Planning To The CITY CENTRE AND EAST Planning And Highways Committee Date Of Meeting: 19/12/2011 LIST OF PLANNING APPLICATIONS FOR DECISION OR INFORMATION *NOTE* Under the heading “Representations” a Brief Summary of Representations received up to a week before the Committee date is given (later representations will be reported verbally). -

Wisconsin Coach Lines Has Wheelchair Accessible Motorcoaches on Fixed-Route Service

MILWAUKEE - JANESVILLE MILWAUKEE - JANESVILLE MILWAUKEE - JANESVILLE DAILY LOOP DAILY LOOP DAILY LOOP Connecting Services by Stop Location Additional Information No reservations required. Schedule operates every day of the year. Prices and schedule subject to change without notice. Please Milwaukee Intermodal Facility allow additional time during bad weather conditions or during highway construction periods. We are not responsible for errors in • CoachUSA Airport Express – www.coachusa.com schedule, damage suffered from late arrivals or departures, failure to make connections, nor situations beyond our control. • Amtrak Trains – www.amtrak.com No Smoking • Greyhound – www.greyhound.com There is no smoking or e-cigarettes allowed on the Motorcoach/Bus per Federal Law. • Indian Trails – www.indiantrails.com Pets WISCONSIN • Lamers – www.golamers.com Pets are accepted only in a cage that will fit under a passenger seat. A full adult fare, per cage, will be charged for cages that COACH LINES • Megabus – www.megabus.com occupy a passenger seat. A cage may not block the aisle. ADA • Milwaukee County Transit – www.ridemcts.com Wisconsin Coach Lines has wheelchair accessible motorcoaches on fixed-route service. Wheelchair users and • Taxi Cab – www.yellowcabmilwaukee.com people with other disabilities can call (262) 542-8861 for more information. We ask that any passenger requiring an ADA Mitchell International Airport accessible Motorcoach/Bus inform us at least 48 hours prior to departure. • CoachUSA Airport Express – www.coachusa.com Lost and Found Please check for personal belongings when leaving the bus. • Mitchell Int'l Airport – www.mitchellairport.com Wisconsin Coach Lines is not responsible for articles left on the bus. -

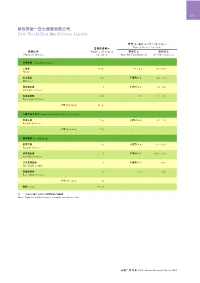

!"#$%&'()* New World First Bus Services Limited

101 !"#$%&'()* New World First Bus Services Limited ($) 2001 12 31 !"# Fares ($) (as at 31.12.2001) ! Number of routes ! ! Group of Routes operated Non Air-Conditioned Air-Conditioned ! Hong Kong Island 38 (2) 2.5 - 4.4 3.0 - 10.5 Urban ! 10 N.A. 4.2 - 9.2 Mid-level !" 2 N.A. 6.3 - 6.8 All Night Services !" 8 (1) 3.2 3.2 - 11.6 Recreation Services Sub-total 58 (3) !"#$ Urban Kowloon and New Territories : ! 7 (5) N.A. 4.3 - 7.5 Regular Services Sub-total 7 (5) ! Cross Harbour ! 24 N.A. 8.1 - 18.2 Regular Services !" 4 N.A. 12.8 - 24.6 All Night Services !"# 2 N.A. 34.2 Sha Tin Racecourse !" 2 11.8 12.8 Recreation Services Sub-total 32 Total 97 (8) !"#$ OMMN !"#$%&' Notes : Figures in brackets denote new routes introduced in 2001. !"# 2002= Annual Transport Digest 2002 102 2001 12 31 !"#$%&'Vehicles (registered as at 31 December 2001) !" () Configuration/class (code) Passenger Capacity Number (i) !"#$%&'() Rear-engined double-deck three-axle non-air-conditioned - !"# 11 (DM) 142 24 Dennis Condor 11M D/M body - !"# 11 ( !) (DM) 130 1 Dennis Condor 11M D/M body (open top) Sub-total 25 (ii) !"#$%&'() Rear-engined double-deck three-axle air-conditioned ! !"# 11.3 (LA) 125 25 Leyland Olympian 11.3M W/A body ! !"# 11.3 (VA) 125 30 Volvo Olympian 11.3M W/A body ! !"# 11.3 (VA) 133 20 Volvo Olympian 11.3M W/A body ! !"# 11.3 (VA) 122 12 Volvo Olympian 11.3M W/A body ! Plaxton 12 (VA) 135 2 Volvo Olympian 12M Plaxton body !"#$%& 11 (DA) 125 82 Dennis Condor 11M D/M body