Business Review and Prospects

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Proposed Road Improvement Works in West Kowloon Reclamation Development Phase I

Proposed Road Improvement Works in West Kowloon Reclamation Development Phase I Project Profile (Report No. 276799/11.01/B) August 2011 Highways Department, HKSAR Government Proposed Road Improvement Works in West Kowloon276799 ReclamationTNI Development BRI 096/03 B P:\Hong Kong\ENL\PROJECTS\276799(BRI) West Kowloon Road Phase I Impr\reports\PP\Project Profile RevA doc 01 December 2009 Schemes H, I, J, Q (Interim Option) and Improvement Works at the Junction of Canton Road/ Ferry Street/ Jordan Road Project Profile August 2011 Highways Department 6/F., Homantin Government Offices, 88 Chung Hau Street, Homantin, Kowloon Mott MacDonald, 20/F, Two Landmark East, 100 How Ming Street, Kwun Tong, Kowloon, Hong Kong T +852 2828 5757 F +852 2827 1823 W www.mottmac.com.hk Phase I Project Profile Issue and revision record Revision Date Originator Checker Approver Description A June 2011 Various Eric Ching H. T. Cheng First Issue B August 2011 Various Eric Ching H. T. Cheng Second Issue This document is issued for the party which commissioned it We accept no responsibility for the consequences of this and for specific purposes connected with the above-captioned document being relied upon by any other party, or being used project only. It should not be relied upon by any other party or for any other purpose, or containing any error or omission used for any other purpose. which is due to an error or omission in data supplied to us by other parties This document contains confidential information and proprietary intellectual property. It should not be shown to other parties without consent from us and from the party which commissioned it. -

Completed Properties Properties Under Development Investment

Completed properties 1. Ocean View 2. The Cliveden 3. Parc Palais 4. Imperial Villas 5. Westin Centre 6. Central Park 7. Far East Finance Centre 8. Cambridge Plaza 9. Dynasty Heights 10. Island Resort 11. Anglers’ Bay 12. The Royal Oaks 13. St Andrews Place 14. Caldecott Hill 15. Majestic Park 16. Island Harbourview 17. Grand Dynasty View 18. Park Avenue 19. Sky Horizon 20. Horizon Place 21. Lincoln Centre 22. Pan Asia Centre 23. Residence Oasis 79 75 24. The Cairnhill 4 76 25. Oceania Heights 74 Properties under development 26. One SilverSea, Kowloon Inland Lot No. 11158 27. Mount Beacon, New Kowloon Inland Lot No. 6196 28. Tsuen Wan Town Centre Redevelopment Project, Tsuen Wan Town Lot No. 398 29. Yeung Uk Road, Tsuen Wan Town Lot No. 394 30. 53 Conduit Road, The Remaining Portion of Inland Lot No. 2138 and Inland Lot No. 2613 31. Ho Tung Lau (Site A), Shatin Town Lot No. 470 32. 464-474 Castle Peak Road, New Kowloon Inland Lot No. 1175-1177 33. Fuk Wing Street and Fuk Wa Street, New Kowloon Inland Lot No. 6425 34. 305 Castle Peak Road, New Kowloon Inland Lot No. 939 35. Junction of Sheung Yuet Road and Wang Chiu Road, New Kowloon Inland Lot No. 6310 78 36. Kwu Tung, Sheung Shui, Lot No. 2596 in DD92 81 37. Ma Wo, Tai Po, Tai Po Town Lot No. 179 38. KCR Wu Kai Sha Station Development, Shatin Town Lot No. 530 89 39. 256 Hennessy Road, Hong Kong Island Lot No. 2769 90 25 Investment properties 40. -

Property Management Revenue from Property Management for 2003 Increased by 11.0% Over 2002 to HK$94 Million

032 Executive management’s report Property review This caused revenue from investment properties for the year of our properties further and establishing them as a to decline slightly by 1% over 2002 to HK$888 million. benchmark for the industry in Hong Kong. Our staff performed outstandingly during the period of SARS For Two IFC, the quality of the office building and its to ensure shoppers’safety and mitigate the effects of the management enabled MTR to attract tenants despite the outbreak on public confidence. We also supported tenants lingering cautious sentiment resulting from SARS, the war in through aggressive promotion campaigns, including an Iraq and the weak economy. Considerable effort was taken attractive rebate promotion. Within this context, we took full to explain to potential tenants, agents and the business advantage of the relaxation of travel restrictions on tourists community the merits of the building, which is ideally suited from Mainland China through proactive, tailor-made to the sophisticated needs of multi-national corporations. programmes, such as organising shopping tours, designed The decision by Swiss banking giant UBS to lease seven floors to bring high spending Mainland visitors to our shopping represented one of the largest and highest profile relocations centres. These programmes proved successful in boosting of an office tenant in Hong Kong in 2003. UBS joined a growing the business turnover of our tenants. list of leading institutions in the building, including the Hong The Total Quality Service Regime, our pioneering customer Kong Monetary Authority, reinforcing Two IFC’s position as the service enhancement programme, and our computerised building of choice for top-tier corporations. -

Kowloon Area - West Kowloon

REPS Kowloon Area - West Kowloon West Kowloon West Kowloon Lai Chi Kok Tsing Yi Tsing Yi Lai Chi Kok Kai Tak Tai Kok Tsui Tseung Kwan O West Kowloon Olympic City Hung Hom Lohas Park Tsim Sha Tsui West Kowloon Kowloon Station West Kowloon Austin 개요: 1. Kowloon Station 2. Austin 3. Olympic 4. Lai Chi Kok 5. Tsing Yi 2 www. repshk.com Tel: 2997 4866 [email protected] Copyright © REPS HK All rights reserved REPS Kowloon 지역 – West Kowloon 1. Kowloon Station a. The Waterfront Transaction Records Address 가격 Saleable Area Reg. Date B Lower Floor TOWER 6 PHASE 2 (Lease)$41,000 1076s.f. 21/05/2020 B Upper Floor TOWER 3 PHASE 1 (Lease)$31,000 794s.f. 20/05/2020 D Middle Floor TOWER 7 PHASE 2 (Lease)$50,000 1127s.f. 15/05/2020 F Lower Floor TOWER 2 PHASE 1 (Lease)$32,500 794s.f. 15/05/2020 D Middle Floor TOWER 2 PHASE 1 (Lease)$33,000 934s.f. 1/5/2020 E Upper Floor TOWER 1 PHASE 1 (Lease)$35,000 948s.f. 1/5/2020 F Lower Floor TOWER 6 PHASE 2 (Lease)$34,000 943s.f. 8/4/2020 A Upper Floor TOWER 7 PHASE 2 (Lease)$37,000 936s.f. 1/4/2020 준공 년도: 2000 최고 층수: 43/F Unit Plan 크기 가격 범위 세대 수: 1,288 units 방 2, 화장실 2 630 35,000 렌트 가격대: 35k-180k 유닛 크기: 630-2,011 방3, 화장실 1-3 794-1127 38,000-65,000 방4- 5, 화장실 2-3 1,987-2,011 120,000-180,000 b. -

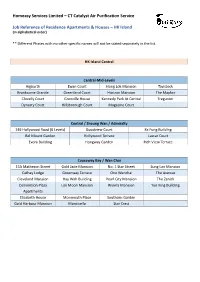

CT Catalyst Air Purification Service Job Reference of Residence

Homeasy Services Limited – CT Catalyst Air Purification Service Job Reference of Residence Apartments & Houses – HK Island (in alphabetical order) ** Different Phases with no other specific names will not be stated separately in the list. HK Island Central Central-Mid-Levels Aigburth Ewan Court Hong Lok Mansion Tavistock Branksome Grande Greenland Court Horizon Mansion The Mayfair Clovelly Court Grenville House Kennedy Park At Central Tregunter Dynasty Court Hillsborough Court Magazine Court Central / Sheung Wan / Admiralty 149 Hollywood Road (6 Levels) Goodview Court Ka Fung Building Bel Mount Garden Hollywood Terrace Lascar Court Evora Building Hongway Garden Rich View Terrace Causeway Bay / Wan Chai 15A Matheson Street Gold Jade Mansion No. 1 Star Street Sung Lan Mansion Cathay Lodge Greenway Terrave One Wanchai The Avenue Cleveland Mansion Hay Wah Building Pearl City Mansion The Zenith Convention Plaza Lok Moon Mansion Riviera Mansion Yue King Building Apartments Elizabeth House Monmouth Place Southorn Garden Gold Harbour Mansion Monticello Star Crest Happy Valley / East-Mid-Levels / Tai Hang 99 Wong Nai Chung Rd High Cliff Serenade Village Garden Beverly Hill Illumination Terrace Tai Hang Terrace Village Terrace Cavendish Heights Jardine's Lookout The Broadville Wah Fung Mansion Garden Mansion Celeste Court Malibu Garden The Legend Winfield Building Dragon Centre Nicholson Tower The Leighton Hill Wing On Lodge Flora Garden Richery Palace The Signature Wun Sha Tower Greenville Gardens Ronsdale Garden Tung Shan Terrace Hang Fung Building -

Financial Review

REVIEW OF OPERATIONS Financial Review TURNOVER PROFIT ATTRIBUTABLE TO SHAREHOLDERS Turnover for the Group for the year ended 31 HK$ MILLION December 2001 increased by 58% to HK$5,036 1,575 million (2000: HK$3,196 million). Turnover from both 1,600 rental and sales registered increases during the year. 1,400 Gross property sales income increased from 1,203 1,233 HK$1,664 million in 2000 to HK$3,159 million in 1,200 2001. Property rental income also increased to 1,000 HK$885 million (2000: HK$820 million) whilst 728 income from warehouse and logistics amounted to 800 HK$744 million (2000: HK$481 million). The 600 396 Group’s hotel operations contributed HK$204 million 400 to turnover during the year (2000: HK$176 million). 200 BREAKDOWN OF KPL’S TOTAL TURNOVER 0 HK$ MILLION 1997 1998 1999 2000 2001 5,500 5,036 decrease in the Group’s earnings in 2001 is due to losses incurred from the sales of Ocean Pointe, Kerry 5,000 Everbright City, Yuen Long 2 warehouse and a 4,500 specific provision of HK$360 million in respect of its 3,159 Constellation Cove project in Tai Po Kau. The Group’s 4,000 75% share of the provision amounted to HK$270 3,500 3,054 3,196 million. The Group also recorded a profit of 2,907 approximately HK$112 million from the disposal of 3,000 its 19.6% interest in the Hu-Ning Expressway in 1,664 2,500 2,342 December 2001. 1,921 1,747 2,000 44 FUNDING AND FINANCING 1,238 426 1,500 55 In order to achieve better control of treasury 410 318 74 47 operations and lower the average cost of funds, KPL 1,000 63 71 204 176 402 410 356 has centralised funding for all its operations at the 11 35 500 Group level. -

Growth Momentum

MTR Corporation Limited Annual Report 2010 Report Annual Limited Corporation MTR ANNUAL REPORT 2010 GROWTH MOMENTUM MTR Corporation Limited MTR Headquarters Building, Telford Plaza Kowloon Bay, Kowloon, Hong Kong GPO Box 9916, Hong Kong Telephone : (852) 2993 2111 Facsimile : (852) 2798 8822 www.mtr.com.hk Stock Code: 66 GROWTH MOMENTUM In 2010, the Company has ridden the economic recovery to post a strong set of results, with increases in revenue and profit. Looking ahead, our growth momentum continues, with our five major expansion projects in Hong Kong on track, and further progress in our growing portfolio of businesses in the Mainland of China and overseas. As a builder and operator of infrastructure assets, we try to ensure that our expansion plans benefit present and future generations, and our aim is to become a global leader in sustainable transportation. CONTENTS 2 MTR Corporation in Numbers – 2010 4 Hong Kong Operating Network with Future Extensions 6 MTR Corporation at a Glance 22 8 Chairman’s Letter Hong Kong Passenger 12 CEO’s Review of Operations Services and Outlook 19 Key Figures 20 Key Events in 2010 22 Executive Management’s Report 22 – Hong Kong Passenger Services 36 36 – Station Commercial and Station Commercial Rail Related Businesses and Rail Related 42 – Property and Other Businesses Businesses 54 – Hong Kong Network Expansion 60 – Mainland and Overseas Growth 66 – Human Resources 42 71 Financial Review Property 78 Ten-Year Statistics and Other Businesses 80 Investor Relations 82 Sustainability 83 Corporate Responsibility -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Sha Tin Block 1, La Costa 5915 Block 2, Lotus Tower, Kwun Tong Garden Kwun Tong 5916 Estate Tai Po Po Sam Pai Village 5917 Kowloon City Duchy Heights 5918 Kowloon City Duchy Heights 5919 Eastern Tower 8, Pacific Palisades 5920 Sham Shui Po Ping Yuen, Yau Yat Chuen 5921 Kowloon City Block C, On Lok Factory Building 5922 Kwai Tsing On Hoi House, Cheung On Estate 5923 Yau Tsim Mong Skyway Mansion 5924 Kowloon City Block C, On Lok Factory Building 5925 Sha Tin Kau To Village 5927 Kowloon City 61 Maidstone Road 5928 Kowloon City The Palace 5929 Kwai Tsing Tower 3A, Phase 1, Tierra Verde 5930 Eastern Tsui Shou House, Tsui Wan Estate 5931 Tuen Mun Lok Sang House, Kin Sang Estate 5932 Sham Shui Po Man Lok House, Tai Hang Sai Estate 5933 Yau Tsim Mong Lee Kwan Building 5934 Wan Chai Wing Way Court 5935 Eastern Hang Ying Building 5936 Sai Kung Block 2, Radiant Towers 5937 Central & Western 23 Wilmer Street 5938 Yau Tsim Mong Block 4, Metro Harbour View 5939 Kwun Tong Chi Tai House, On Tai Estate 5940 Kowloon City Tower 2, K City 5941 Tuen Mun Block 6, Po Tin Estate 5943 Yau Tsim Mong Wai Fat Building 5944 Tsuen Wan Tak Tai Building 5945 Sham Shui Po Tower 2, Nob Hill 5946 1 Related Confirmed / District Building Name Probable Case(s) Tsuen Wan Tower 6, Bellagio 5947 -

Muk Ning Street) – Tai Kok Tsui (Island Harbourview

TRAFFIC ADVICE Introduction of Air-Conditioned Urban Kowloon Route No. 20 Kai Tak (Muk Ning Street) – Tai Kok Tsui (Island Harbourview) Members of the public are advised that Air-Conditioned Urban Kowloon Route No. 20 Kai Tak (Muk Ning Street) – Tai Kok Tsui (Island Harbourview) will start operating with effect from 29 April 2018 (Sunday). Details are as follows: Routeing * KAI TAK (MUK NING STREET) to TAI KOK TSUI (ISLAND HARBOURVIEW) : via Muk Ning Street Bus Terminus, Muk Ning Street, Muk On Street, Shing Kai Road, Concorde Road, Prince Edward Road East , Prince Edward Road West, Argyle Street, Waterloo Road, Ngo Cheung Road, Hoi Wang Road, Cherry Street, Sham Mong Road, Hoi Fai Road, Roundabout, Hoi Fai Road, Hoi Fan Road and Tai Kok Tsui (Island Harbourview). TAI KOK TSUI (ISLAND HARBOURVIEW) to KAI TA K (MUK NING STREET) : via Tai Kok Tsui (Island Harbourview), Hoi Fan Road, Hoi Fai Road, Roundabout, Hoi Fai Road, Sham Mong Road, Cherry Street, Tai Kok Tsui Road, Cherry Street, Hoi Wang Road, Lai Cheung Road, Waterloo Road, Argyle Street, Prince Edward Road West, Prince Edward Road East, Slip Road, Roundabout, Luk Hop Street, Tsat Po Street, Kai San Road, Concorde Road, Roundabout, Concorde Road, Shing Kai Road, Muk Hung Street, Muk Chui Street, Shing Kai Road, Muk On Street, Muk Ning Street and Muk Ning Street Bus Terminus. Fare Kai Tak (Muk Ning Street) to Tai Kok Tsui (Island Harbourview) Full fare: $4.60 per single journey Section fare from Hoi Wang Road to Tai Kok Tsui (Island Harbourview): $3.50 Tai Kok Tsui (Island Harbourview) to Kai Tak (Muk Ning Street) Full fare: $4.60 per single journey Section fare from Concorde Road to Kai Tak (Muk Ning Street): $4.10 Operating Hours Mondays to Satur days: Hours Headway From Kai Tak 5.40 a.m. -

List of Buildings with Confirmed / Probable Cases of COVID-19

List of Buildings With Confirmed / Probable Cases of COVID-19 List of Residential Buildings in Which Confirmed / Probable Cases Have Resided (Note: The buildings will remain on the list for 14 days since the reported date.) Related Confirmed / District Building Name Probable Case(s) Islands Hong Kong SkyCity Marriott Hotel 11101 North Block 6, Belair Monte 11105 Kowloon City iclub Ma Tau Wai Hotel 11106 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11107 Wan Chai Best Western Hotel Causeway Bay 11108 Kowloon City Metropark Hotel Kowloon 11109 Kwun Tong IW Hotel 11110 Kwai Tsing Dorsett Tsuen Wan Hong Kong 11111 Eastern Ramada Hong Kong Grand View 11112 Kowloon City iclub Ma Tau Wai Hotel 11113 North Block 1, Dawning Views 11114 Islands Block 1, Coastal Skyline 11115 Central & Western Lan Kwai Fong Hotel@ Kau U Fong 11116 Central & Western Sing Fai Building 11118 Eastern Hoi Sing Mansion, Taikoo Shing 11120 Eastern Hoi Sing Mansion, Taikoo Shing 11121 Sai Kung Tak On House, Hau Tak Estate 11123 Sham Shui Po 15 Fuk Wing Street 11124 Kowloon City iclub Ma Tau Wai Hotel 11125 Yau Tsim Mong Dorsett Mongkok, Hong Kong 11127 Kwai Tsing Block 1, Regency Park 11128 Central & Western True Light Building 11129 Islands Hong Kong SkyCity Marriott Hotel 11130 Central & Western Yukon Court 11131 Central & Western Bishop Lei International House 11132 Central & Western 40 Conduit Road 11132 Sham Shui Po 15 Fuk Wing Street 11133 Central & Western May Tower I 11134 Kwai Tsing Yat King House, Lai King Estate 11135 Central & Western Yip Cheong Building, -

List of Projects Used in HKIA/ARB Professional Assessment 2007 - 2013

List of projects used in HKIA/ARB Professional Assessment 2007 - 2013 Date of Occupation No Year Name of Company Project Title Address Lot No BD File Ref. Permit / Practical Special Topic Completion (month/year) 1 2007 Aedas Ltd Satellite Earth Station Dai Hei Street at Tai Po Industrial Estate Section G Tai Po Town Lot BD 2/9141/01 (P) Jan 04 IL7076, IL7077, IL971, IL970 Proposed Hotel Development at 31E - 39 Wyndham 31E, 31F, 33-39 Wyndham Street, 2 2007 AGC Design Ltd SARP, IL970RP, BD3/2058/94 PT IV Jul 04 Street, Central Central, Hong Kong IL970SBSS1 RP Extension to the Church of Jesus Christ of Latter Day Tseung Kwan O Lot 45, Area II, Po Lam 3 2007 Aedas Ltd Tseung Kwan O Lot 45 BD 9106/04 31 Oct 2006 Saints at Tseung Kwan O Lane 4 2007 P & T Architects & Engineers Ltd Residential Development At 2 Lok Kwai Path Shatin, 2 Lok Kwai Path, Shatin, N.T. STTL 526 BD 9067/02 Jan 06 / May 06 5 2007 Leung King Partners Ltd Villa Rosa Residents 82 Peak Road, Hong Kong RBL 742 BD 2014/98 Aug 00 6 2007 Dennis Lau & Ng Chun Man Architects & Engineers (HK) Ltd Tuen Mun Area 4C, TMTL 384 King Fung Path, Tuen Mun, N.T. Lot No. 384, Area 4C BD 6/9260/97H (P) Aug 02 Service Apartment Building at Nos. 116-122, Yeung Uk 116-122 Yeung Uk Road, Tsuen Wan, 7 2007 MLA Architects (HK) Ltd TWTL 407 9325/93 28 Aug 06 Road (H-Cube) N.T. -

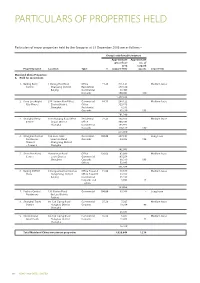

Particulars of Properties Held

PARTICULARS OF PROPERTIES HELD Particulars of major properties held by the Group as at 31 December 2006 are as follows:– Group’s attributable interest Approximate Approximate gross floor no. of area carpark Property name Location Type % (square feet) spaces Lease term Mainland China Properties A. Held for investment 1. Beijing Kerry 1 Guang Hua Road Office 71.25 711,121 Medium lease Centre Chaoyang District Residential 277,330 Beijing Commercial 98,406 Carparks 190,806 430 1,277,663 2. Kerry Everbright 218 Tianmu Road West Commercial 64.35 286,122 Medium lease City Phase I Zhabei District Office 323,675 Shanghai Residential 6,333 Carparks 85,250 155 701,380 3. Shanghai Kerry 1515 Nanjing Road West Residential 74.25 142,355 Medium lease Centre Jingan District Office 308,584 Shanghai Commercial 103,971 Carparks 118,129 180 673,039 4. Shanghai Central 166 Lane 1038 Residential 100.00 287,101 Long lease Residences Huashan Road Carparks 54,982 154 Phase II Changning District – Tower 3 Shanghai 342,083 5. Shenzhen Kerry Renminnan Road Office 100.00 82,099 Medium lease Centre Lowu District Commercial 107,256 Shenzhen Carparks 88,319 193 Others 53,885 331,559 6. Beijing COFCO 8 Jianguomennei Avenue Office Tower A 15.00 49,649 Medium lease Plaza Dongcheng District Office Tower B 53,895 Beijing Commercial 86,592 Carparks and 3,892 25 others 194,028 7. Fuzhou Central 139 Gutian Road Commercial 100.00 63,986 – Long lease Residences Gu Lou District Fuzhou 8. Shanghai Trade 88-128 Siping Road Commercial 55.20 7,567 Medium lease Square Hongkou District Carparks 19,264 48 Shanghai 26,831 9.