8.5 X 11 Corporate Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

How Related Leased 7 Million Square Feet of Office Space at Hudson Yards

How Related leased 7 million square feet of office space at Hudson Yards March 19,2019 | by Rebecca Baird-Remba When Related Companies began searching for tenants to fill its first, 1.8-million-square-foot office tower at Hudson Yards in 2011, its leasing brokers had to convince companies to move to a neighborhood that was still a hole in the ground. The development firm was in the middle of decking over the 26-acre West Side rail yard and laying the foundations for the first phase of its sprawling, mixed-use development, which would eventually encompass 18 million square feet of commercial and residential space. Stephen Winter, a senior vice president at Related who has led much of the office leasing at Hudson Yards, had to show CEOs that their workers would one day have access to dozens of casual lunch options and restaurants. One day, the hole in the ground would be home to a million square feet of retail—luxury retailers, fast fashion stores, food halls, five star eateries and interactive art exhibits. But none of it was built yet, and back then, asking tenants to lease hundreds of thousands of square feet at Hudson Yards was a gamble. “Six, seven years ago, we had to break through doors and be as persistent as ever,” Winter explained. “It was a totally new place for everyone. It was a blank slate, an open piece of land with rail yards beneath it.” He gave “credit where credit was due” to the first crop of tenants who signed on to 10 Hudson Yards, including Coach, L’Oreal and SAP, which opened as the development’s first office building in 2016. -

COS Cure Notice

20-10990-mew Doc 218 Filed 07/28/20 Entered 07/28/20 17:40:32 Main Document Pg 1 of 7 S. Jason Teele, Esq. Gregory A. Kopacz, Esq. 101 Park Avenue, 28th Floor New York, New York 10178 (212) 643-7000 (Telephone) (212) 643-6500 (Facsimile) [email protected] [email protected] Counsel to the Debtors and Debtors in Possession UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re: Chapter 11 THE NORTHWEST COMPANY, LLC, et al.* Case No. 20-10990 (MEW) Debtors. (Jointly Administered) CERTIFICATION OF SERVICE Gregory A. Kopacz, of full age, certifies as follows: 1. I am not a party to the action, am over the age of eighteen, and am an associate with the firm Sills Cummis & Gross P.C., attorneys for Debtors and Debtors in Possession. 2. On July 24, 2020, I caused copies of the Notice of Proposed Assumption and Assignment of Certain Executory Contracts and Unexpired Leases (the “Notice”) to be served by Federal Express, priority overnight delivery, on the counterparties/addresses listed on Exhibit A attached hereto. Dated: July 28, 2020 New York, New York /s/ Gregory A. Kopacz Gregory A. Kopacz * The Debtors in these Chapter 11 Cases, along with the last four digits of each Debtor’s federal tax identification number, are: The Northwest Company LLC (8132) and The Northwest.com LLC (1339). The location of the Debtors’ service address is: 49 Bryant Avenue, Roslyn, New York 11576. 7390628 20-10990-mew Doc 218 Filed 07/28/20 Entered 07/28/20 17:40:32 Main Document Pg 2 of 7 Exhibit A Counterparty Name Address Marty H. -

CTBUH Journal

About the Council The Council on Tall Buildings and Urban Habitat, based at the Illinois Institute of Technology in CTBUH Journal Chicago and with a China offi ce at Tongji International Journal on Tall Buildings and Urban Habitat University in Shanghai, is an international not-for-profi t organization supported by architecture, engineering, planning, development, and construction professionals. Founded in 1969, the Council’s mission is to disseminate multi- Tall buildings: design, construction, and operation | 2014 Issue IV disciplinary information on tall buildings and sustainable urban environments, to maximize the international interaction of professionals involved Case Study: One Central Park, Sydney in creating the built environment, and to make the latest knowledge available to professionals in High-Rise Housing: The Singapore Experience a useful form. The Emergence of Asian Supertalls The CTBUH disseminates its fi ndings, and facilitates business exchange, through: the Achieving Six Stars in Sydney publication of books, monographs, proceedings, and reports; the organization of world congresses, Ethical Implications of international, regional, and specialty conferences The Skyscraper Race and workshops; the maintaining of an extensive website and tall building databases of built, under Tall Buildings in Numbers: construction, and proposed buildings; the Unfi nished Projects distribution of a monthly international tall building e-newsletter; the maintaining of an Talking Tall: Ben van Berkel international resource center; the bestowing of annual awards for design and construction excellence and individual lifetime achievement; the management of special task forces/working groups; the hosting of technical forums; and the publication of the CTBUH Journal, a professional journal containing refereed papers written by researchers, scholars, and practicing professionals. -

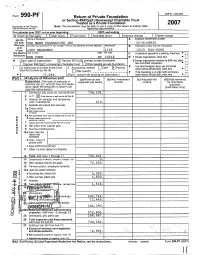

Return of Private Foundation

OMB No 1545.0052 Form 990 P F Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation 2007 Department of the Treasury Note : The foundation may be able to use a copy of this return to satisfy state Internal Revenue Service For calendar year 2007, or tax year be ginnin g , 2007 , and endin g I G Check all that apply Initial return Final return Amended return Address change Name change Name of foundation A Employer identification number Use the IRS label THE MANN FOUNDATION INC 32-0149835 Otherwise , Number and street (or P 0 box number if mail is not delivered to street address) Room/suite B Telephone number (see the instructions) print or type 1385 BROADWAY 1 1102 (212) 840-6266 See Specific City or town State ZIP code C If exemption application is pending, check here Instructions. ► NEW YORK NY 1 0 0 1 8 D 1 Foreign organizations , check here ► H Check type of organization Section 501 (c)(3exempt private foundation 2 Foreign organizations meeting the 85% test, check q here and attach computation Section 4947(a ) (1) nonexem p t charitable trust Other taxable p rivate foundation ► foundation status was terminated Accrual E If private ► Fair market value of all assets at end of year J Accounting method Cash X under section 507(b)(1 XA), check here (from Part ll, column (c), line 16) Other (s pecify) _ _ _ _ _ _ _ _ _ _ _ _ F If the foundation is in a 60-month termination (d) on cash basis) under section 507(b)(1)(B), check here ► $ -2,064. -

Seagram Building, First Floor Interior

I.andmarks Preservation Commission october 3, 1989; Designation List 221 IP-1665 SEAGRAM BUIIDING, FIRST FLOOR INTERIOR consisting of the lobby and passenger elevator cabs and the fixtures and interior components of these spaces including but not limited to, interior piers, wall surfaces, ceiling surfaces, floor surfaces, doors, railings, elevator doors, elevator indicators, and signs; 375 Park Avenue, Manhattan. Designed by Ludwig Mies van der Rohe with Philip Johnson; Kahn & Jacobs, associate architects. Built 1956-58. Landmark Site: Borough of Manhattan Tax Map Block 1307, Lot 1. On May 17, 1988, the landmarks Preservation Commission held a public hearing on the proposed designation as a Landmark of the Seagram Building, first floor interior, consisting of the lobby and passenger elevator cabs and the fixtures and interior components of these spaces including but not limited to, interior piers, wall surfaces, ceiling surfaces, floor surfaces, doors, railings, elevator doors, elevator indicators, and signs; and the proposed designation of the related I.and.mark Site (Item No. 2). The hearing had been duly advertised in accordance with the provisions of law. Twenty witnesses, including a representative of the building's owner, spoke in favor of designation. No witnesses spoke in opposition to designation. The Commission has received many letters in favor of designation. DFSCRIPI'ION AND ANALYSIS Summary The Seagram Building, erected in 1956-58, is the only building in New York City designed by architectural master Iudwig Mies van der Rohe. Constructed on Park Avenue at a time when it was changing from an exclusive residential thoroughfare to a prestigious business address, the Seagram Building embodies the quest of a successful corporation to establish further its public image through architectural patronage. -

Fairytale of New York: Hudson Yards

September 29th, 2017 Fairytale of New York: Hudson Yards At three times the size of the Rockefeller Center, when it is fully built out, some time around 2040, more than 27m sq ft of new class-A office space, 20m sq ft of new housing, 3m sq ft of hotels and 2m sq ft of retail will have been delivered by developers that include Related Companies, Oxford Properties, Brookfield and Tishman Speyer. Millions of square feet of space have already been completed and leased to blue-chip occupiers, and further significant deals are rumoured to be on the cards. No wonder the Hudson Yards district is one of the hottest property markets in New York City at the moment. So how did a development of this scale and ambition come about, who is doing what in the district and where is Hudson Yards’ new office occupier base being drawn from? Historically the Hudson Yards district consisted of warehousing and industrial space alongside the Manhattan waterfront. The area primarily acted as a rail hub that was fed 747 Third Avenue, Floor 18 New York, NY 10017 212.889.0808 [email protected] marinopr.com by the High Line - which closed years ago and has over the past decade been converted into green public spaces - as well as the Long Island Rail Road. But that all started to change when New York mayor Michael Bloomberg came to power in the early 2000s. “He noted that the average age of commercial office property in Manhattan was north of 75 years and with that in mind, he said, quite correctly, if we’re going to attract the best and brightest in the TAMI [technology, advertising, media and information] sectors, we’ve got to have some new product,” says Bruce Mosler, chairman of global brokerage at Cushman & Wakefield. -

Duane Morris LLP a Delaware Limited Liability Partnership 1540 Broadway New York, NY 10036 Tel: (212) 692.1000 Fax: (212) 208.4521 William C

12-12900-scc Doc 2 Filed 07/09/12 Entered 07/09/12 18:46:41 Main Document Pg 1 of 4 Duane Morris LLP A Delaware Limited Liability Partnership 1540 Broadway New York, NY 10036 Tel: (212) 692.1000 Fax: (212) 208.4521 William C. Heuer, Esq. and 190 South LaSalle Street Suite 3700 Chicago, IL 60603 Tel: (312) 499.6700 Fax: (312) 499.6701 John Robert Weiss, Esq. Counsel for Sovereign Bank, N.A. UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK ------------------------------------------------------------------- x In re: : Chapter 11 : PATRIOT COAL CORPORATION, : Case No. 12-12900 (SCC) : : Debtor. : ------------------------------------------------------------------- x NOTICE OF APPEARANCE AND REQUEST FOR SERVICE PLEASE TAKE NOTICE that Duane Morris LLP hereby appears in the above- referenced Chapter 11 case as attorneys for Sovereign Bank, N.A., and pursuant to Bankruptcy Rules 2002 and 9010(b) and § 1109(b) of the Bankruptcy Code, requests that copies of all notices and pleadings given or required in this case be given and served upon the following at the below addresses and facsimile numbers: John Robert Weiss William C. Heuer DUANE MORRIS LLP DUANE MORRIS LLP 190 South LaSalle Street, Suite 3700 1540 Broadway Chicago, IL 60603 New York, NY 10036 Tel: (312) 499-6700 Tel.: (212) 692.1000 Fax: (312) 499.6701 Fax: (212) 208.4521 DM3\2235074.1 12-12900-scc Doc 2 Filed 07/09/12 Entered 07/09/12 18:46:41 Main Document Pg 2 of 4 PLEASE TAKE FURTHER NOTICE that the foregoing request includes not only the notices and papers referred to in the Bankruptcy Rules specified above, but also includes without limitation, any notice, application, complaint, demand, motion, petition, pleading or request, whether formal or informal, written or oral, and whether transmitted or conveyed by mail, delivery, telephone, electronically or otherwise filed or made with regard to the above-captioned case and proceedings therein. -

Asking Rents Remain Stable Despite Faltering Leasing Activity

MARKETVIEW SNAPSHOT Midtown Manhattan Office, May 2020 Asking rents remain stable despite faltering leasing activity Figure 1: Midtown Market Activity Apr. 2020 Mar. 2020 Apr. 2019 YTD 2019 YTD 2020 Leasing Activity 0.40 MSF 0.85 MSF 1.85 MSF 5.77 MSF 4.50 MSF Renewals 0.28 MSF 0.22 MSF 0.48 MSF 1.47 MSF 1.56 MSF Absorption (0.11) MSF (0.25) MSF 0.20 MSF (1.22) MSF (1.27) MSF Availability Rate 11.8% 11.8% 10.7% Vacancy Rate 8.0% 7.9% 7.6% Average Asking Rent $87.77 PSF $87.00 PSF $88.20 PSF Taking Rent Index 92.8% 93.2% 94.0% Source: CBRE Research, May 2020. MARKET HIGHLIGHTS • Monthly leasing activity totaled 405,000 sq. ft., 72% below the five-year monthly average of 1.43 million sq. ft. • Year-to-date leasing activity was down 22% from the same period last year. • Renewals totaled 277,000 sq. ft. in April, bringing the year-to-date total to 1.56 million sq. ft. • The availability rate was flat month-over-month but up 110 basis points (bps) year-over-year. • Net absorption was negative 109,000 sq. ft. in April, bringing the year-to-date total to negative 1.27 million sq. ft. • The average asking rent was essentially flat both month-over-month and year-over-year. • Sublease availability was 2.5%, with an average asking rent of $66.63 per sq. ft., up 18% year-over-year. Figure 2: Top Lease Transactions Size (Sq. -

Who Are NYC's Most Active Developers?

Who are NYC’s most active developers? The Real Deal ranked the top 10 December 27, 2018 | By Kathryn Brenzel and Kevin Sun The companies behind two mega-developments on Manhattan’s far West Side are the city’s busiest developers — and will likely remain so for the next few years. Related Companies and Brookfield Property Partners are the top two most active developers in the city in terms of the scale of their ongoing projects. Related and Brookfield are respectively being kept busy by their massive mixed-use proj- ects, Hudson Yards and Manhattan West. The Real Deal compiled a list of the city’s busiest developers of new construction, based on building permits issued by the Department of Buildings. Only projects with active permits that have not yet been issued a temporary certificate of occupancy (TCO) as of Dec.19 were included. Alterations were not included in developers’ total square footages or project counts. Here are the top 10 most active developers by square footage, as represented in DOB filings. 1. Related Companies Square footage: 6 million Number of projects: 9 Related’s largest ongoing project is 415 10th Avenue, better known as 50 Hudson Yards. The 2.2 million-square-foot office tower has been the target of multiple protests over the past year, due to the developer’s decision to use both union and nonunion construction labor on the project. Related’s second-largest ongoing project is another office tower at 550 West 34th Street, better known as 55 Hudson Yards. 2. Brookfield Property Partners Square footage: 4 million Number of projects: 4 Brookfield’s largest ongoing project is One Manhattan West, a 2 million-square–foot-plus office tower on Ninth Avenue. -

Brochure Show the Situation During Formwork Assembly and Are Therefore Incomplete from the Safety Aspect

Understanding how to build high faster. Formwork solutions for your highrise project The Formwork Experts. _Understanding your highrise project as a partner _Understanding the construction process truly and being knowledgeable about it is the prerequisite for being a partner in the construction industry. We have this un- derstanding from the initial planning stage through to completion of construction. _Understanding such as this is based on more than 40 years' experience in self- climbing technology and more than 1,000 highrise projects successfully realised worldwide. Construction of the world’s tallest building, the Burj Khalifa in Dubai, 828 metres tall, is an outstanding example. With this comprehensive know-how, we are well-qualified to be your high- performing and reliable partner in highrise construction. 2 Doka is able to look back on a long history of _ understanding. Listening intently, understanding the world as seen through the eyes of our custom- ers, learning to understand all aspects and thinking ahead. We are passionate about not being satisfied with the first solution that might get the job done. Rather, we continue fine-tuning it until we come up with a true benefit for our customers. This is the only way a small woodworking shop could grow into a globally operating form- work company, known by the brand name Doka since 1956. "Thanks to the reliable technology and efficient on-site support provided by Doka, we were able to meet the schedule of Colombo Costruzioni S.p.A. with its detailed plan for completion of the Torre Isozaki build in Milan. As a result, we were able to shorten the original schedule for finishing the building shell by approximate- ly three months." Gianfranco Cesana, Engineering Manager for Colombo Important information: Always observe all relevant safety regulations (e.g. -

Hudson Yards 2019-30HY Mortgage Trust Table of Contents

JUNE 2019 STRUCTURED FINANCE: CMBS PRESALE REPORT Hudson Yards 2019-30HY Mortgage Trust Table of Contents Capital Structure 3 Transaction Summary 3 Rating Considerations 5 DBRS Viewpoint 5 Strengths 6 Challenges & Considerations 6 Property Description 8 Tenant and Lease Summary 9 Market Overview 10 Local Economy 10 Office Market 11 Office Submarket Description 12 Competitive Set 13 5 Manhattan West 13 55 Hudson Yards 13 10 Hudson Yards 13 441 Ninth Avenue 13 1 Manhattan West 14 The Farley Building 14 50 Hudson Yards 14 Sponsorship 14 DBRS Analysis 15 Site Inspection Summary 15 DBRS NCF Summary 16 DBRS Value Analysis 17 DBRS Sizing Hurdles 17 Loan Detail & Structural Features 18 Transaction Structural Features 19 Methodology 20 Surveillance 21 Chandan Banerjee Edward Dittmer Senior Vice President Senior Vice President +1 (212) 806 3901 +1 212 806 3285 [email protected] [email protected] Kevin Mammoser Erin Stafford Managing Director Managing Director +1 312 332 0136 +1 312 332 3291 [email protected] [email protected] HUDSON YARDS 2019-30HY JUNE 2019 Capital Structure Description Rating Action Class Amount Subordination DBRS Rating Trend Class A New Rating – Provisional 348,695,000 35.831% AAA (sf) Stable Class X New Rating – Provisional 389,169,000 -- AAA (sf) Stable Class B New Rating – Provisional 40,474,000 28.383% AA (high) (sf) Stable Class C New Rating – Provisional 38,758,000 21.507% A (high) (sf) Stable Class D New Rating – Provisional 147,887,000 10.621% A (low) sf Stable Class E New Rating – Provisional 144,286,000 0.000% BBB (sf) Stable Class RR NR 30,320,000 0 NR Stable RR Interest NR 7,580,000 0 NR Stable 1. -

PATHFINDERS DATA MAPS Chart Course to $100B Biz PAGE 4 CRAIN’S® NEW YORK BUSINESS

20150824-NEWS--0001-NAT-CCI-CN_-- 8/21/2015 6:18 PM Page 1 PATHFINDERS DATA MAPS chart course to $100B biz PAGE 4 CRAIN’S® NEW YORK BUSINESS VOL. XXXI, NOS. 34, 35 WWW.CRAINSNEWYORK.COM DOUBLE ISSUE AUGUST 24-SEPTEMBER 6, 2015 PRICE: $3.00 Tech jobs, Chinese tourism and speeding tickets—all up. Pedestrian deaths and hotel vacancies? Down. Our annual data deep-dive starts on PAGE 12 34 5 greg hall greg NEWSPAPER 71486 01068 0 B:11.125” T:10.875” S:10.25” Your business deserves B:14.75” the best T:14.5” S:14” network. Trade in your phone. Buy a Droid Turbo. Get $350. Until August 31st. New 2-yr. activation on $34.99+ plan req’d. $350=$200 bill credit + $150 smartphone trade-in credit (account credits applied within 2-3 billing cycles). Trade in must be in good working condition. $1999 (32 GB) New 2-yr. activation on $24.99+ plan req’d. Offer expires 9/30/15. findmyrep.vzw.com Bill credit will be removed from account if line is suspended or changed to non-qualifying price plan after activation. Activation fee/line: $40. IMPORTANT CONSUMER INFORMATION: Corporate Subscribers Only. Subject to Major Acct Agmt, Calling Plan, & credit approval. Up to $350 early termination fee/line. Offers & coverage, varying by svc, not available everywhere; see vzw.com. While supplies last. Restocking fee may apply. DROID is a trademark of Lucasfilm Ltd. and its related companies. Used under license. © 2015 Verizon Wireless. I7812 Project Title: New York Crains Team Proof Approval Job Number New York Crains Inks Side 1 CMYK Full Size (W” X H”) Reduced Size (W” X H”) (Initial and Date) Job Type Ad Inks Side 2 n/a Scale 1” 1” Art Director None Project New York Crains Finishing None Resolution 300 dpi 300 dpi Copywriter None Version Code None Template None Bleed 11.125” x 14.75” 11.125” x 14.75” Studio None 125 E.