Investing in Care. Delivering Returns

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Download the X12 Timetable

Solihull to Birmingham X12 via Airport/NEC | Birmingham Business Park | Chelmsley Wood | Bromford Estate Monday to Friday from 30th August 2020 Solihull Rail Station 0310 0415 - 0517 - 0556 - 0624 0642 0702 0717 0732 0754 0814 0839 0859 Solihull Town Centre 0312 0417 - 0519 - 0558 - 0626 0644 0704 0719 0735 0757 0817 0842 0902 Damson Ln Land Rover Works 0322 0427 - 0529 - 0608 - 0638 0656 0716 0732 0749 0811 0833 0856 0916 International Station (NEC) 0332 0437 0512 0539 - 0619 - 0649 0707 0727 0743 0800 0822 0844 0907 0927 Birmingham Airport 0336 0441 0516 0543 - 0623 - 0653 0711 0731 0747 0804 0826 0848 0911 0931 Birmingham Business Park Waterside 0339 0444 0519 0546 - 0626 - 0656 0714 0734 0750 0807 0829 0851 0914 0934 Chelmsley Interchange (arr) 0348 0453 0528 0555 - 0635 - 0706 0724 0744 0801 0819 0841 0903 0925 0945 Chelmsley Interchange (dep) 0350 0455 0530 0557 0619 0637 0651 0708 0726 0746 0801 0821 0843 0905 0927 0947 Buckingham Rd Windward Way 0402 0507 0542 0609 0629 0648 0702 0720 0740 0801 0817 0837 0859 0918 0940 1000 Castle Bromwich Heathland Av. 0410 0515 0550 0618 0638 0657 0712 0730 0750 0811 0827 0847 0909 0928 0950 1010 Bromford Road - - 0558 0628 0648 0707 0722 0741 0801 0824 0839 0859 0920 0940 1000 1020 City Centre The Priory Q'way - - 0610 0640 0700 0720 0735 0755 0815 0840 0855 0915 0935 0955 1015 1035 Solihull Rail Station 0921 0941 03 23 43 1343 1359 1419 1438 1456 1516 1536 1559 1625 Solihull Town Centre 0924 0944 05 25 45 1345 1401 1421 1440 1459 1519 1539 1602 1628 Damson Ln Land Rover Works 0938 0958 18 -

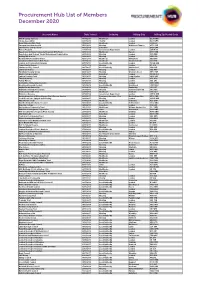

Procurement Hub List of Members December 2020

Procurement Hub List of Members December 2020 Account Name Date Joined Industry Billing City Billing Zip/Postal Code NHS Property Services 07/04/2017 Healthcare London EC2V 7NQ Stroke Association 30/07/2018 Charity London EC1V 2PR Royal Marsden NHS Trust 17/05/2017 Healthcare London SW3 6JJ Paragon Asra Housing Ltd 05/01/2018 Housing Walton-on-Thames KT12 1DZ East Sussex College Group 04/12/2019 Education BN21 2UF Homes England 21/10/2019 Government Department London SW1H 0TL Epsom and St Helier University Hospitals NHS Trust 09/01/2019 Healthcare Epsom KT17 1HB Kensington and Chelsea Tenant Management Organisation 28/06/2016 Housing London W10 5BE Notting Hill Genesis 12/01/2017 Housing London NW1 0DL Medway NHS Foundation Trust 30/11/2018 Healthcare Gillingham ME7 5NY Croydon Health Services NHS Trust 17/10/2018 Healthcare Thornton Heath CR7 7YE London and Continental Railways 26/07/2016 Local Authority London WC2B 4AN Tower Hamlet Homes 23/11/2016 Housing London E1 4FG Chelmsford City Council 18/07/2017 Local Authority Chelmsford CM1 1JE Lewisham Homes 14/09/2017 Housing London SE6 4RU Paradigm Housing Group 30/01/2017 Housing Wooburn Green HP10 0DF King's College London 09/01/2019 Education London WC2R 2LS Saffron Housing Trust 14/11/2017 Housing Long Stratton NR15 2XP The Hyde Group 09/11/2017 Housing London SE1 9EQ Family Mosaic 16/02/2017 Housing London SE1 2RJ Goldsmiths, University of London 02/05/2017 Education London SE14 6NW Brentwood Borough Council 13/12/2018 Local Authority Brentwood CM15 8AY Anglia Ruskin University 31/08/2018 -

Units 1 & 2, 200 Bromford Lane, Birmingham, B24

UNITS 1 & 2, 200 BROMFORD LANE, BIRMINGHAM, B24 8DL TO LET GROUND FLOOR SHOWROOM/WAREHOUSE ACCOMMODATION. 22,000 sq.ft/ 2,043.85 sq.m • Prominent corner position, enjoying an extensive frontage onto Bromford Lane (A4040 – main arterial route – considerable traffic flow). • Within close proximity to the Fort Shopping Park. • Within close proximity to the main A47 – Heartlands/Fort Parkway. • Circa 1 mile from Junction 6 of the M6 motorway, “Spaghetti Junction”. • Circa 2 ¾ miles north east of Birmingham City Centre. • Excellent off-street car parking. • Excellent off-street loading. Stephens McBride Chartered Surveyors & Estate Agents • Substantial roller shutter door access. One, Swan Courtyard, Coventry Road, Birmingham, B26 1BU • Open span. Tel: 0121 706 7766 Fax: 0121 706 7796 www.smbsurveyors.com UNITS 1 & 2, 200 BROMFORD LANE, BIRMINGHAM, B24 8DL LOCATION DESCRIPTION The subject premises occupies an extremely The subject premises provide open span, ground prominent corner position, enjoying a substantial floor industrial/warehouse accommodation, frontage onto Bromford Lane (A4040 – main including an extensive showroom facility. arterial route – considerable traffic flow), located Advantages include; within close proximity to the main island intersection with Heartlands/Fort Parkway (A47). a) Extensive forecourt parking. The area benefits from excellent communicational b) Off street loading/car parking to the rear. links; c) Two, substantial roller shutter doors to the rear a) Bromford Lane/Wheelwright Road/Tyburn (electric and manual) (door one – width 12ft Road (A38), provide direct dual carriageway 9ins/3.88 metres – height 16ft/4.88 metres, access to junction 6 of the M6 motorway, door two – width 21ft/6.4 metres, height “Spaghetti Junction” – circa 1 mile due west. -

Practical Advice for Families and Caregivers ❧ Tuesday, June 28, 2 P.M

Concordia University Chicago’s Center for Gerontology, The Scottish Home and the Alzheimer’s Association, Greater Illinois Chapter invite you to join us for a very special event When Someone You Know Has Dementia: Practical Advice for Families and Caregivers ❧ Tuesday, June 28, 2 p.m. – 4 p.m. | Concordia University Chicago Christopher Center, Room 200, 7400 Augusta Street, River Forest, Illinois June Andrews, RMN, RGN, FRCN Director, Dementia Services Development Centre Fellow, Royal College of Nursing United Kingdom Stirling University, Scotland Professor Andrews supports health and social care teams as a coach and mentor, and has led successful teams for three decades. In 2011, she gained recognition for her international work through the Robert Tiffany Award, and was presented in Philadelphia with the first-ever Founders' Award of the British American Project, of which she is a Fellow and advisory board member. She received the Chief Nursing Officers' Lifetime Professor Andrews will Achievement Award in 2012, and in 2013 she was listed in the discuss worldwide best care Health Services Journal as one of the 50 most inspirational practices for individuals with women in health care and separately as one of the 100 most dementia and Alzheimer’s influential clinicians in England. Most recently, she was made a disease. She will also discuss Fellow of the Royal College of Nursing of the United Kingdom, and sign her book, When the highest honor that the RCN can bestow. Someone You Know Has Event seating is limited – registration is required Dementia: Practical Advice To register, go to https://cuchicago.edu/juneandrews for Families and Caregivers. -

Innovation and Ambition: the Impact of Self-Financing Oncouncil Housing

Innovation and Ambition: the impact of self-financing oncouncil housing 2 based on an extrapolation of the survey data 1 2 Table of contents Foreword .......................................................................................................................................................... 4 Executive Summary ......................................................................................................................................... 5 Introduction ..................................................................................................................................................... 8 Councils have responded appropriately to the new self-financing framework ........................................... 10 Councils are investing responsibly ............................................................................................................... 13 Councils have the capacity to deliver more ................................................................................................. 15 Appendix 1 – Survey analysis ......................................................................................................................... 17 Appendix 2 – Southampton City Council: comprehensive investment underpinned by greater rent flexibility ........................................................................................................................... 26 Appendix 3 – Milton Keynes Council: increasing sustainability with greater ambition to invest in regeneration ........................................................................................................................ -

871 Bus Time Schedule & Line Route

871 bus time schedule & line map 871 Bromford Bridge - Castle Vale View In Website Mode The 871 bus line Bromford Bridge - Castle Vale has one route. For regular weekdays, their operation hours are: (1) Castle Vale: 7:38 AM Use the Moovit App to ƒnd the closest 871 bus station near you and ƒnd out when is the next 871 bus arriving. Direction: Castle Vale 871 bus Time Schedule 16 stops Castle Vale Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 7:38 AM Bromford Drive, Bromford Bridge Bromford Road, Birmingham Tuesday 7:38 AM Reynoldstown Rd, Bromford Wednesday 7:38 AM Sundew Croft, Bromford Thursday 7:38 AM Friday 7:38 AM Sandown Rd, Bromford Saturday Not Operational Chipperƒeld Rd, Bromford Collingbourne Avenue, Bromford Millington Rd, Hodgehill 871 bus Info Direction: Castle Vale Shawsdale Rd, Hodgehill Stops: 16 Trip Duration: 20 min Newport Rd, Buckland End Line Summary: Bromford Drive, Bromford Bridge, Reynoldstown Rd, Bromford, Sundew Croft, Bromford, Sandown Rd, Bromford, Chipperƒeld Rd, Berrandale Gardens, Buckland End Bromford, Collingbourne Avenue, Bromford, Millington Rd, Hodgehill, Shawsdale Rd, Hodgehill, Tameside Drive, Bromford Newport Rd, Buckland End, Berrandale Gardens, Buckland End, Tameside Drive, Bromford, Avery Avery Croft, Tyburn Croft, Tyburn, Drem Croft, Tyburn, Roundmoor Walk, Concorde Drive, Birmingham Castle Vale, Watton Green, Castle Vale, Reed Square, Castle Vale Drem Croft, Tyburn Sopwith Croft, Birmingham Roundmoor Walk, Castle Vale Cosford Crescent, Birmingham Watton Green, Castle Vale Reed Square, Castle Vale Mere Way, Birmingham 871 bus time schedules and route maps are available in an o«ine PDF at moovitapp.com. Use the Moovit App to see live bus times, train schedule or subway schedule, and step-by-step directions for all public transit in West Midlands. -

Women Mean Business in London and the UK

WOMEN mean BUSINESS and in LONDON theU.K. Women-led businesses all over the United Kingdom England & Scotland • Imperial Brands • Severn Trent • Whitbread • Halfords Group • Bromford London • Virgin Money • GlaxoSmithKline • BTG • Open Bionics • SSP Group • ITV • Kingsher • Grant Thornton • Blaze • Century Tech • Eporta • Peanut • Suitcase • Snap Tech • Seenit • Vida • Settled • Olio • Technology Will Save Us • Passion Capital • Provenance • Azimo • LiveBetterWith • Skimlinks • Move Guides • Wool and the Gang • Starling Bank • Unruly • Lantum • Seedcamp • TechHub • Badoo • Net-a-Porter • Entrepreneur First In 2016, women’s representation in senior management (21 percent) in the United Kingdom slightly declined from the previous year (22 percent), and over a third (36 percent) of U.K. businesses had no women in senior roles (the country’s highest recorded percentage). Source: Knowledge Center / Catalyst / February 7, 2017 Where Women-led Start-ups are in the U.K. North 33% West North 3% East West 74% Midlands South 7% East Source: Ben Chapman / The Independent / July 4, 2017 Based on a Royal Bank of Scotland Report in 2013, there are now 1.5 million women who are self-employed, representing an increase of 300,000 since before the economic downturn in 2008. Source: Tara Howard / Venus Voice / July 28, 2017 Advocacy The Women Version 2.0 in Business Network Communications Association The Grange, East End 500 Harrison Ave Everywoman Furneux Pelham Suite 401R Capital 3 Brad Street Nr Buntingford Boston, MA London, SE1 8TN Herts, SG9 OJT Education 617 426 2222 020 7981 2574 Mentorship Female Campus Entrepreneur for Mums British Association 4-5 Bonhill Street Association PO Box 164 London of Women Stockport, SK7 3WH EC2A 4BX Entrepreneurs Women 034 5257 8749 Entrepreneurs U.K. -

RIGHT PLACE, RIGHT TIME BETTER TRANSFERS of CARE: a CALL to ACTION ‘Doing the Obvious Thing Is the Radical Thing’ INTRODUCTION

RIGHT PLACE, RIGHT TIME BETTER TRANSFERS OF CARE: A CALL TO ACTION ‘Doing the obvious thing is the radical thing’ INTRODUCTION There is no simple solution to delays in transfers of care: no one individual to blame nor a magic bullet that will solve everything. Everyone in the health and social care system needs to act: commissioners and providers, physical and mental health, national and local organisations. However there are a number of practical steps we can take to understand the root causes of delayed transfers of care and build the partnerships needed to tackle them. Our starting point is three calls to action addressed to every part of the health and Rt Hon Paul Burstow Former care minister and chair, care system. Tavistock and Portman NHS Foundation Trust 1. Start with the person (the patient or service user). They are your common cause. 2. Ask yourself how do we help this person get back to where they want to be? 3. Agree what the data tells you. A shared understanding of the numbers can help with tracking down the root causes. No one working in the NHS or social care sets out to do harm. Having seen first hand the day to day pressures on a hospital ward and across different care settings what Saffron Cordery was most striking was the importance of these three calls Director of policy and strategy to action in both professional practice and system design. NHS Providers Hospitals, community, ambulance and mental health All NHS providers face the challenge of ensuring timely providers sit within a wider ecology of the health and patient discharge and managing the ‘flow’ of patients social care system and the interplay between people’s through their organisations. -

Website List Dec 11

Change 4 Life Volleyball Clubs - December 2011 School County School Address Postcode Challney Boys Bedfordshire County Area Stoneygate Road, Luton LU4 9TJ King Houghton Middle School Bedfordshire County Area Parkside Drive, Dunstable LU5 5PX Lincroft Middle School Bedfordshire County Area Station Road, Oakley, Bedford MK43 7RE Luton Sixth Form College Bedfordshire County Area Bradgers Hill Road, Luton, Beds LU2 7EW Cedars Upper School Bedfordshire County Area Mentmore Road, Leighton Buzzard LU7 2AE Vandyke Upper School Bedfordshire County Area Vandyke Road, Leighton Buzzard, Beds LU7 3DY Bracknell and Wokingham College Berkshire County Area Chruch Road, Bracknell, Berkshire RG12 1DJ Edgbarrow School Berkshire County Area Grant Road, Crowthorne, Surrey RG45 7HZ Newlands Girls School Berkshire County Area Farm Road, Maidenhead, Berkshire SL6 5JB Reading College Berkshire County Area Kings Road, Reading, Berkshire RG1 4HJ Kennet School Berkshire County Area Stoney Lane, Thatcham, Berks RG19 4LL St Josephs School Berkshire County Area Newport Road, Newbury, Berkshire RG14 2AW Hodge Hill SEC Birmingham County Area Hodge Hill Court, Bromford Road, Birmingham B36 8HB Turves Green Boys Birmingham County Area Northfield, Birmingham, West Midlands B31 4BS bordesley green girls school Birmingham County Area Bordesley Green Road, Birmingham B9 4TR Holte Birmingham County Area Wheeler Street, Lozells, Birmingham, West Midlands B19 2EP Kingsbury School & Sports College Birmingham County Area Kingsbury Road, Birmingham B24 8RE Birmingham Metropolitan -

Exploring Two Decades of Involvement, Voice and Activism by People with Dementia in Scotland Philly Hare, Innovations in Dementia June 2020 Contents

Loud and Clear! Exploring two decades of involvement, voice and activism by people with dementia in Scotland Philly Hare, Innovations in Dementia June 2020 Contents An accessible summary .................................................................................1 Foreword ............................................................................................................4 1. Introduction .................................................................................................5 2. Early days .................................................................................................. 14 3. Moving up a gear ...................................................................................... 42 4. DEEP in Scotland ...................................................................................... 57 5. Involvement in research ........................................................................ 74 6. Creativity and voice ................................................................................ 88 7. Scotland and the wider world .............................................................101 8. The motivations, costs and rewards of activism ...........................117 9. Reflections on impact and learning .................................................136 Appendix 1 ...................................................................................................168 Appendix 2 ...................................................................................................170 About the author -

The London Gazette, 22Nd June 1967 6945

THE LONDON GAZETTE, 22ND JUNE 1967 6945 (4) Land at Almonsbury, Glos; by Thornstoke H.M. LAND REGISTRY Limited. Lincoln's Inn Fields, London, W.C.2. FREEHOLD THE LYTHAM DISTRICT LAND REGISTRY, (1) Land adjoining 24 Claremont Road, Bickley, Lytham St. Annes, Lanes. Kent, by M. J. Crick, 7 Lapsewood, 121 Sydenham Hill, London S.E.26. FREEHOLD (2) 47 Temple Avenue, Shirley, Surrey, by V. Knight Rees of that address. (1) Essoldo Cinema, Ordsall Lane, Salford, Lanes; (3) 5 Greenhill, Sutton, Surrey, by L. E. and V. C. L. by Essoldo (Cinemas) Limited. Palmer of that address. (2) 6 Barnfield Street and 2 Ruskin Avenue, both Cheetham, Manchester; by F. Casket, 53 Riverside Court, Didsbury, Manchester. LOST CERTIFICATES (3) Land forming part of Eastbrook Cottage, Cardiff Road, Dinas Powis, Glam ; by George Wimpey It is proposed to issue new Certificates in place of & Co., Limited. those described below that are stated by the owners to have been lost. Anyone possessing the missing certificate or objecting to the issue of new ones should at once notify the Chief Land Registrar at the THE NOTTINGHAM DISTRICT LAND REGISTRY, appropriate Registry shown below: Chalf ont Drive, Nottingham. THE NOTTINGHAM DISTRICT LAND REGISTRY FREEHOLD Chalfont Drive, Nottingham (1) 8 Haymarket, Leicester; by G. R. (Holdings) 1. Leasehold Title WK47259 164 North Leigh Road, Limited. Ward End, Birmingham 8. (2) Land on S. Side of Negate Street, Bingham, Land Certificate to Messrs. Eyre & Co., 278 Notts ; by Fruxrealm Developments Limited. Washwood Heath Road, Birmingham 8. <3) Land on N.W. side of Hearsall Lane, Coventry, 2. -

The London Gazette, May 3, 1867

2590 THE LONDON GAZETTE, MAY 3, 1867. 1G69. And to William Robert Lake, of the "In- of Oldham, in the county of Lancaster, En- ternational Patent Office," No. 8, Southampton- gineer, for the invention of tl improvements in buildings, Chancery-lane, in the county of Mid- lithographic, zincographic, and typographic dlesex, Consulting Engineer, for the invention printing machines." of " improvements in breech-loading fire-arms."'1095. To Thomas Howard Head, of the Teesdale —A communication to him from abrond by Works, Sfcockton-on-Tees, for the invention of Henry Huntington Wolcott, of Yonkers, New "improvements in machinery for rolling iron York, United States of America. and steel." On their several petitions, recorded in the Office 1096. To William Clark, of 53, Chancery-lane, of the Commissioners on the 10th day of April, in the county of Middlesex, Engineer and 1867. Patent Agent, for the invention of " improve- ments in apparatus for propelling vessels."—A 1071. To Francis George Flcury, of Southward, communication to him from abroad by Eugene in the county of Surrey, Engineer, for the in- Bachelier, Machinist, of 29, Boulevart St. vention of "improvements in machinery or Martin, Paris. apparatus for measuring fluids." 1097. And to William Clark, of 53, Chancery- 1075.' To Samuel Smith, of Prince's-sfreot, Lei- lane, in the county of Middlesex, Engineer and cester-square, in the county of Middlesex, Gun Patent Agent, for the invention of " improve- Manufacturer, for the invention cf " improve- ments in apparatus for obtaining isochronous ments in breech loading sporting guns." movements applied to clocks and other time 1077.