Case Study of Vail Resorts, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

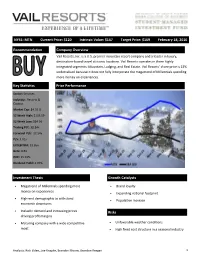

Recommendation Company Overview Key Statistics Price Performance

NYSE: MTN Current Price: $120 Intrinsic Value: $147 Target Price: $169 February 18, 2016 Recommendation Company Overview Vail Resorts, Inc. is a U.S. premier mountain resort company and a leader in luxury, destination-based travel at iconic locations. Vail Resorts operates in three highly integrated segments: Mountain, Lodging, and Real Estate. Vail Resorts’ share price is 22% undervalued because it does not fully incorporate the megatrend of Millennials spending more money on experiences. Key Statistics Price Performance Sector: Services Industry: Resorts & Casinos Market Cap: $4.35 B 52 Week High: $133.59 52 Week Low: $84.56 Trailing P/E: 38.84x Forward P/E: 27.54x P/S: 3.01x EV/EBITDA: 13.85x Beta: 0.83 ROE: 15.74% Dividend Yield: 2.07% Investment Thesis Growth Catalysts Megatrend of Millennials spending more Brand loyalty money on experiences Expanding national footprint High-end demographic to withstand Population increase economic downturns Inelastic demand and increasing prices Risks driving profit margins Maturing company with a wide competitive Unfavorable weather conditions moat High fixed cost structure in a seasonal industry Analysts: Rick Eldee, Zoe Knapke, Brandon Moore, Brandon Reagan 1 Investment Thesis Megatrend of Millennials spending more money on experiences Based on our research, 78% of Millennials would choose to spend their money on an experience over buying a product and 55% are more willing to spend more on experiences than ever before. Skiing, snowboarding, mountain biking, hiking, golfing, rafting and kayaking are among the most popular experiences Vail Resorts has to offer. The megatrend should continue into our investment horizon because approximately 72% of Millennials admitted that they will increase their spending on experiences next year. -

Destination Colorado

WELCOME WELCOME DESTINATION COLORVADO DESTINATION COLORADO Steamboat Springs Fort Collins Estes Loveland Park Greeley Longmont Northeast FRONT RANGE REGION: Northwest Granby Boulder Front Visit www.destinationcolorado.com for more information Winter Park Range BLACK HAWK, BOULDER, ESTES Beaver Black Hawk on all of our members. Keystone PARK, FORT COLLINS, GREELEY, Creek Vail Golden Aurora Palisade Snowmass Breckenridge Denver Colorado is a paradise for meeting planners and incentive buyers, combining the most magnificent natural beauty LONGMONT, LOVELAND Copper Mtn Grand Aspen Denver in the world with first-class accommodations, state-of-the-art meeting space and convenient access. We have North of Denver, this region combines some Junction of Colorado’s finest college communities with Buena Vista Colorado organized our 2018 Meeting Planner Guide into state regions, beginning with our Front Range just north of Denver Gateway Crested Butte Springs some of its most spectacular scenery. Boulder, Pueblo and ending with information on transportation in the state. We have included a map illustrating each of our Fort Collins and Greeley, home to the state’s regions and a brief descriptor of some of the features they represent. Rest assured, no matter where you plan finest public universities, also offer charming South Southwest Central your meeting in Colorado, all of our members can provide you with the type of quality and services you communities with an abundance of meeting space, dining, accommodations and activities. Telluride Southeast have grown to expect. Estes Park is situated in one of the state’s most spectacular backdrops, Rocky Mountain National Colorado is located in the western half of the United States and is easily accessible from both coasts. -

Beaver Creek CWPP

BEAVER CREEK, COLORADO Wildland Urban Interface: Community Wildfire Protection Plan Prepared for: Beaver Creek Resort Company Avon, Colorado Submitted By: Anchor Point Group Fire Management Boulder, Colorado December, 2007 TABLE OF CONTENTS PURPOSE ...................................................................................................................................................... 1 INTRODUCTION ............................................................................................................................................ 1 THE NATIONAL FIRE PLAN AND THE HEALTHY FOREST RESTORATION ACT ...................................... 2 GOALS AND OBJECTIVES ............................................................................................................................ 3 COLLABORATION: COMMUNITY/AGENCIES/FIRE SAFE COUNCILS ....................................................... 4 STUDY AREA OVERVIEW ............................................................................................................................. 5 VALUES .......................................................................................................................................................... 9 LIFE SAFETY AND HOMES ...................................................................................................................... 9 COMMERCE AND INFRASTRUCTURE .................................................................................................... 9 RECREATION AND LIFE STYLE ........................................................................................................... -

Loyalty Programs Hit the Ski Hills Industry Analysis from Ideaworks

Issued: December 3, 2004 Contact: Jay Sorensen For inquiries: 414-961-1939 Powder and Points – Loyalty Programs Hit the Ski Hills Industry Analysis from IdeaWorks The ski industry embraces airline-style frequent customer programs at 11 of the 20 largest U.S. ski areas. Frequent-skier programs offered by major ski areas are far more generous and consumer friendly than their airline industry counterparts: • Squaw Valley offers a free lift ticket for every four purchased - - an amazing return of 25%. • The PEAK Rewards program associated with Breckenridge Ski Resort allows up to 8 family members to pool their points into one account. • PEAK Rewards also allows the exchange of points and airline miles with Frontier’s EarlyReturns frequent flier program. • The Vertical Plus program offered by the Northstar-at-Tahoe ski area is most unusual because its members accrue benefits based upon the vertical feet on ski runs taken by its members. Each program has its unique qualities – - yet they are very similar on the issue of reward restrictions. Leaving the inventory restrictions and black-out dates of the airline industry behind, these frequent skier programs allow members to redeem rewards for free lift tickets on the busiest of holiday weekends. Where the programs seem to lag their airline-industry counterparts is in areas involving bonus partners, co-branded credit cards, elite customer recognition and year-round participation. Frequent-Skier Programs at the 20 Largest U.S. Ski Areas IdeaWorks reviewed the frequent-skier programs associated with the 20 largest U.S. ski areas as determined by “2003 season skier visits” data compiled by the National Ski Areas Association (NSAA). -

Squaw Valley |Alpine Meadows Base-To-Base Gondola Project Final EIS/EIR Apdx C

Appendix C Squaw Valley | Alpine Meadows Base-to-Base Gondola Final Visitation and Use Assessment SQUAW VALLEY | ALPINE MEADOWS BASE-TO-BASE GONDOLA FINAL VISITATION AND USE ASSESSMENT February 2018 Prepared by: SE Group and RRC Associates Squaw Valley | Alpine Meadows Gondola Visitation and Use Assessment BACKGROUND Squaw Valley Ski Holdings, LLC (SVSH) has applied to the U.S. Forest Service and Placer County, California for permission to construct a gondola connecting the Squaw Valley and Alpine Meadows ski areas.1 The U.S. Forest Service and Placer County are analyzing the potential environmental impacts of this project through a joint Environmental Impact Statement (EIS)/Environmental Impact Report (EIR). The EIS/EIR will analyze direct and indirect effects of the Proposed Action and alternatives to the Proposed Action that would occur on both National Forest System (NFS) lands as well as private lands within Placer County, California. Past, present, and reasonably foreseeable future activities that could affect, or could be affected by, implementation of the Proposed Action and alternatives will be analyzed cumulatively. This assessment is designed to inform the analysis of potential direct impacts of the proposed Base-to- Base Gondola by evaluating the anticipated changes to annual snowsports visitation at Squaw Valley | Alpine Meadows as a result of the proposed project. This analysis evaluates the anticipated impact on total snowsports visits (i.e., skier visits) and potential changes in the Squaw Valley | Alpine Meadows market share expected to specifically result from the installation and operation of the proposed Base-to-Base Gondola. METHODOLOGIES AND DATA Amenities and Attractions At the root of this assessment is the consideration of whether the proposed Base-to-Base Gondola would principally provide an added amenity at Squaw Valley | Alpine Meadows or if the added resort connectivity that it would provide would be sufficiently unique to act as an attractant to increased visitation. -

The Osprey at Beaver Creek, a Rockresort, Ranked #1 Top Resort in the Continental United States in the Travel + Leisure 2012 World's Best Awards Readers' Survey

July 6, 2012 The Osprey at Beaver Creek, A RockResort, Ranked #1 Top Resort in the Continental United States in the Travel + Leisure 2012 World's Best Awards Readers' Survey BEAVER CREEK, Colo., July 6, 2012 /PRNewswire/ -- Travel + Leisure announced today that The Osprey at Beaver Creek, A RockResort, is the #1 Top Resort in the Continental United States according to the Travel + Leisure 2012 World's Best Awards readers' survey. The Osprey received a score of 94.75 and was ranked #1. Additionally, The Osprey's sister resort, The Pines Lodge, A RockResort, also located in Beaver Creek, was rated the #3 Top Resort in the Continental United States. Conveniently located in the heart of Beaver Creek Village, The Osprey is the closest hotel to a ski resort in North America - a mere 26 feet from the hotel's ski valet entrance to Beaver Creek's Strawberry Park Express chair lift. The Osprey combines contemporary design and luxury amenities, including an award-winning gourmet tapas bar and restaurant. Each year, Travel + Leisure readers vote on thousands of hotels, ranking properties all over the world in a variety of categories including rooms and facilities, location, service, restaurants and food, and value. The winning resorts are listed on www.TravelandLeisure.com now, will be featured in the August digital editions on iPad®, NOOK Color™, and Kindle Fire™, and in the August issue of the magazine, on newsstands July 20. James O'Donnell, chief operating officer of RockResorts, said, "We are honored to have two of our RockResort properties at the top of the Travel + Leisure 2012 World's Best Awards readers' survey. -

Proposed Hotel Breckenridge

FEASIBILITY STUDY Proposed Hotel Breckenridge SOUTH PARK AVENUE BRECKENRIDGE, COLORADO SUBMITTED TO:PR OPOSED PREPARED BY: Town of Breckenridge HVS Consulting and Valuation Services Mr. Peter Grosshuesch Division of TS Worldwide, LLC 150 Ski Hill Road 413 South Howes Street Breckenridge, Colorado, 80424 Fort Collins, CO 80521 +1 (970) 453-3162 +1 (720) 877-1376 Lowe Enterprises Real Estate Services, Inc. PO Box 5600 Snowmass Village, CO 81615 May-2013 May 19, 2013 Mr. Peter Grosshuesch Town of Breckenridge 150 Ski Hill Road Breckenridge, Colorado, 80424 HVS DENVER Re: Proposed Hotel Breckenridge 413 South Howes Street Breckenridge, Colorado Fort Collins, CO 80521 Error! Not a valid link. HVS Reference: 2013020203 +1 (970) 493-2919 FAX www.hvs.com Dear Mr. Grosshuesch: Atlanta Boston Pursuant to your request, we herewith submit our feasibility study pertaining to Boulder the above-captioned property. We have inspected the real estate and analyzed the Chicago hotel market conditions in the Breckenridge, Colorado area. We have also Dallas conducted interviews with the community key stakeholders and business leaders, Denver Houston have studied the site and its constraints, and the results of our fieldwork and Las Vegas analysis are presented in this report. We have also reviewed several development Los Angeles plan options for the proposed improvements for this site and have selected what Mexico City we believe to be the best-suited plan and program for the analysis. Our report was Miami prepared in collaboration with Oz Architecture and is in accordance with the Minneapolis Uniform Standards of Professional Appraisal Practice (USPAP), as provided by the Nassau Appraisal Foundation. -

Shannon Warren*

LEFT OUT IN THE COLD: EXPLORING THE VULNERABILITIES OF SEASONAL WORKERS IN THE SKI INDUSTRY Shannon Warren* TABLE OF CONTENTS I. Introduction ................................................................................. 1 II. An Overview of the Ski Industry, Its Workers, and Their Vulnerabilities ................................................................................. 5 A. The ski industry relies on a seasonal workforce. ................... 5 B. Ski-industry employers' reliance on temporary visas for foreign seasonal workers makes both foreign and domestic workers more vulnerable. ............................................................ 7 C. The compensation and benefits seasonal ski workers receive is inadequate to protect their particular vulnerabilities. ............ 10 III. Ski-industry employers' Obligations to Seasonal Workers ..... 12 A. Generally, the law provides no additional protections for seasonal workers. ...................................................................... 13 1. The At-Will Doctrine ........................................................ 13 2. Contingent Employment and General Legal Protections for Employees ............................................................................. 14 3. Legal Protections and Vulnerabilities Particular to Seasonal Workers ................................................................................. 18 B. Unlike most seasonal workers, migrant and seasonal agricultural workers are protected under the Migrant and Seasonal Agricultural Workers Protection -

Beaver Creek 2010 Master Development Plan Update / 2015

Beaver Creek Resort 2010 Master Development Plan Update 2015 Addendum Prepared For: Prepared By: BEAVER CREEK 2010 MASTER DEVELOPMENT PLAN UPDATE 2015 ADDENDUM P R E P A R E D F OR: B E A V E R C REEK , C OLORADO P R E P A R E D B Y : T AB L E O F CONTENTS 1. INTRODUCTION ......................................................................................................................................1 C. BACKGROUND ....................................................................................................................................... 1 E. STATEMENT OF GOALS AND OBJECTIVES ............................................................................................... 2 2. DESIGN CRITERIA ...................................................................................................................................3 E. APPLICABLE FOREST SERVICE POLICY DIRECTION .................................................................................. 4 1. Management Policies and Direction .............................................................................................................. 4 2. Ski Area Recreation Opportunity Enhancement Act of 2011 ................................................................... 5 3. EXISTING SKI RESORT FACILITIES ....................................................................................................7 H. ALTERNATIVE EXPERIENCE ..................................................................................................................... 7 3. Summer Programs .......................................................................................................................................... -

Vail Resorts 2004 Annual Report Just Another Day in Paradise

Vail Resorts 2004 Annual Report Just another day in paradise... Vail Resorts is the premier mountain resort company in North America, with six distinctive mountain resorts: Vail® Breckenridge™ Keystone® Heavenly® Beaver Creek® Vail Resorts is committed to providing world-class facilities and service for our customers, an attractive workplace for our employees, sensitivity to our surroundings and profitable growth for our shareholders. ማሜምሞ Grand Teton ® In addition, RockResorts, a luxury hotel operator, has been part of the Vail Resorts portfolio since fiscal 2002. Cover Photo: The majesty of Vail Mountain radiates under the night sky as the moonlight cascades down upon the ski slopes. While the charm and grace of Vail Village and Lionshead have long been icons of the Vail Valley, with the start of Vail’s New Dawn, the magic will be intensified. The beauty of this land can be attributed to the dedicated and tireless work of the United States Forest Service. Vail Resorts’ companies operate in and around the White River National Forest in Colorado, under the management of the Lake Tahoe Basin Management Unit in the Eldorado National Forest in California and the Humboldt- Toiyabe National Forest in Nevada, and on lands managed by the National Park Service in the Grand Teton National Park in Wyoming. To Our Shareholders: Fiscal 2004 was truly an outstanding year for Vail Resorts, as we enjoyed a robust and healthy rebound from the difficult operating environment post 9/11. Although still fresh in all of our minds, this year the threat of terrorism and ongoing military conflict abroad did not put a chill in visitation at our mountain resorts and luxury hotels. -

25Th National Avalanche School Classroom Session Beaver Run Resort, CO October 22-26, 2017 Attendee List

25th National Avalanche School Classroom Session Beaver Run Resort, CO October 22-26, 2017 Attendee List (as of 10/18/17) Brad Acker Ian Bolliger Angie Cameron Soldier Mountain Ski Area Tahoe Backcountry Ski Patrol Sun Valley Resort 4516 W Freemont Street 1621 Josephine Street PO Box 852 Boise, ID 83706 Berkeley, CA 94703-1320 Ketchum, ID 83340 Kyle Armstrong Keith Bosscher Samuel Capenter Breckenridge Ski Area Aspen Mountain Mt. Hood Meadows PO Box 1058 37925 Highway 82 1229 SW Grover Street Breckenridge, CO 80424 Aspen, CO 81611 Apt. 111 Portland, OR 97239 Michael Arnold Richard Bothwell Soldier Mountain Ski Area AIARE Matt Chaffin 2551 E Boise Ave 11260 Donner Pass Road Park City Mountain Resort Boise, ID 83706 Ste. C1, PMB 275 PO Box 39 Truckee, CA 96161 Park City, UT 84060 Nick Barlow Colorado Avalanche Information Stephanie Boyd David Childs Center Yellowstone Mountain Club Thunderbolt Patrol 342 Brook Circle PO Box 161097 PO Box 140 Boulder, CO 80302 Big Sky, MT 59716 Lanesboro, MA 01237 Nathan Bash Dan Brinkman Melis Coady Winter Park Resort Park City Mountain Resort Alaska Avalanche School PO Box 1502 PO Box 39 HC 89 Box 8013 Fraser, CO 80442 Park City, UT 84060 Talkeetna, AK 99676 Michael Benning Jeremy Brodney Kolina Coe Alpental Solitude Mountain Resort Northstar California PO Box 1068 11999 Big Cottonwood Canyon 429 Serene Ave, #204 100 SR906 Road Tahoe Vista, CA 96148 Snoqualmie Pass, WA 98068 Salt Lake City, UT 84109 Rebecca Cowell Ryan Bentley Matt Burke Beaver Creek Resort Soldier Mountain Ski Area Aspen Highlands PO -

Vail Resorts Media News

Vail Resorts Media News 2016-2017 Image: Breckenridge Mountain Season Highlights 2015 - 2016 Corporate 3 Vail 6 Beaver Creek 8 Breckenridge 10 Keystone 11 Park City 13 Northstar 14 Heavenly 15 Kirkwood 16 Perisher 16 Contact Us 17 Image: Vail Mountain Image: Vail Mountain Vail Resorts and Whistler Blackcomb Agree To Strategic Combination Vail Resorts, Inc. and Whistler Blackcomb Holdings, Inc. announced that they have entered into a strategic business combination joining Whistler Blackcomb with Vail Resorts. Under the transaction, Vail Resorts would acquire 100 percent of Vail Resorts commits US$100 million in the stock of Whistler Blackcomb. resort improvements Whistler Blackcomb is the largest resort in Vail Resorts will invest approximately North America (8,100 acres; 3,278 US$100 million in resort improvements for hectares) and one of the most iconic the upcoming winter, bringing its six-year mountain resorts in the world with an resort investment total to more than incredible history, passionate employees US$600 million. Scheduled improvements and a strong community. The mountain include building a new, 490-seat restaurant resort is located 75 miles (121 km) north of at the top of the Peak 7 chairlift in Vancouver in British Columbia, Canada. Breckenridge, an area not currently served with a major food and beverage venue. Famous for hosting the alpine skiing events of the 2010 Vancouver Winter Olympics, The Sun Up chairlift at Vail Mountain (Chair Whistler Blackcomb is also well known for 17), will also be replaced and upgraded its Peak 2 Peak Gondola, the longest and from a fixed grip triple to a high-speed four- highest lift in the world.