2020 European Esports Market Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dopuna 19.04 Nedelja

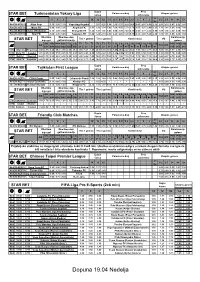

Dupla Prvo Poluvreme-kraj Ukupno golova STAR BET Turkmenistan Yokary Liga šansa poluvreme 2+ 1 X 2 1X 12 X2 1-1 X-1 X-X X-2 2-2 1 X 2 0-2 2-3 3+ 4+ 5+ 1p. Ned 14:00 5232 Altyn Asyr 1.15 5.90 13.0 Kopetdag Asgabat - 1.07 4.25 1.54 3.90 9.75 28.0 24.0 1.49 2.65 8.50 2.12 2.55 2.15 1.41 2.12 3.65 Pon 13:30 5709 Merw FK 2.90 3.00 2.25 Asgabat FK 1.51 1.29 1.31 5.00 7.00 4.55 5.70 3.70 3.55 1.97 2.80 2.95 1.70 1.91 1.96 3.60 7.60 Pon 14:00 5707Nebitci (FK Balkan) 2.15 2.80 3.40 Energetik FK 1.24 1.33 1.56 3.65 5.00 3.80 7.40 6.10 2.90 1.77 4.25 3.90 1.39 1.96 2.62 5.60 13.0 Pon 15:30 5708 Ahal FK 1.60 3.30 5.45 Sagadam FK 1.09 1.24 2.10 2.50 4.25 4.85 12.0 9.75 2.15 2.03 5.20 2.90 1.70 1.91 1.95 3.55 7.50 Oba tima Oba tima daju Kombinacije Tim 1 golova Tim 2 golova Kombinacije VG STAR BET daju gol gol kombinacije golova GG GG GG1& GG1/ 1 & 2 & T1 T1 T1 T2 T2 T2 1 & 2 & 1 & 2 & 1-1& 2-2& 1-1& 2-2& 1+I& 1+I& 2+I& GG 1>2 2>1 &3+ &4+ GG2 GG2 GG GG 2+ I 2+ 3+ 2+ I 2+ 3+ 3+ 3+ 4+ 4+ 3+ 3+ 4+ 4+ 1+II 2+II 2+II 5232 Altyn As Kopetdag 2.08 2.35 3.20 18.0 2.30 2.80 23.0 2.80 1.21 1.80 20.0 6.60 28.0 1.49 28.0 2.22 60.0 1.96 50.0 2.75 80.0 3.00 1.85 1.37 2.10 3.70 5709 Merw FK Asgabat 1.76 2.25 3.80 17.0 2.25 6.10 4.55 9.25 2.85 8.00 7.00 2.22 5.35 5.35 4.00 11.0 9.00 9.00 6.50 18.0 13.0 3.10 2.00 1.74 3.20 6.80 5707 Nebitci Energeti 2.22 3.10 5.90 29.0 2.90 5.80 9.00 9.00 2.62 7.00 14.0 4.15 14.0 4.75 7.90 13.0 19.0 7.70 14.0 17.0 35.0 3.25 2.07 2.15 4.50 11.0 5708 Ahal FK Sagadam 2.00 2.55 4.15 21.0 2.45 3.75 11.0 5.10 1.73 3.45 15.0 4.75 18.0 2.75 12.0 5.60 27.0 3.95 21.0 7.10 55.0 3.10 2.00 1.73 3.15 6.75 Dupla Prvo Poluvreme-kraj Ukupno golova STAR BET Tajikistan First League šansa poluvreme 2+ 1 X 2 1X 12 X2 1-1 X-1 X-X X-2 2-2 1 X 2 0-2 2-3 3+ 4+ 5+ 1p. -

There Are No Women and They All Play Mercy

"There Are No Women and They All Play Mercy": Understanding and Explaining (the Lack of) Women’s Presence in Esports and Competitive Gaming Maria Ruotsalainen University of Jyväskylä Department of Music, Art and Culture Studies Pl 35, 40014 University of Jyväskylä, Finland +358406469488 [email protected] Usva Friman University of Turku Digital Culture P.O.Box 124 FI-28101 Pori, Finland [email protected] ABSTRACT In this paper, we explore women’s participation in esports and competitive gaming. We will analyze two different types of research material: online questionnaire responses by women explaining their reluctance to participate in esports, and online forum discussions regarding women’s participation in competitive Overwatch. We will examine the ways in which women’s participation – its conditions, limits and possibilities – are constructed in the discussions concerning women gamers, how women are negotiating their participation in their own words, and in what ways gender may affect these processes. Our findings support those made in previous studies concerning esports and competitive gaming as fields dominated by toxic meritocracy and hegemonic (geek) masculinity, and based on our analysis, women’s room for participation in competitive gaming is still extremely limited, both in terms of presence and ways of participation. Keywords Gender, esports, hegemonic geek masculinity, toxic meritocracy, Overwatch INTRODUCTION "Why do the female humans always play the female characters?" Acayri wondered soon thereafter. "Like, they're always playing Mercy." "They can't play games and be good at them —" Joel responded. "That's true, so they just pick the hottest girl characters," Acayri said. The previous is an excerpt of an article published on a digital media site Mic on May 11th 2017 (Mulkerin, 2017). -

Gridiron Football League Draft Results 06-Feb-2007 12:51 PM Eastern

www.rtsports.com Gridiron Football League Draft Results 06-Feb-2007 12:51 PM Eastern Gridiron Football League Draft Sun., Aug 27 2006 5:52:00 PM Rounds: 20 Time Limit: Unlimited Round 1 Round 6 #1 St. Louis River Rats - Larry Johnson, RB, KAN #1 Boston Bulldogs - Plaxico Burress, WR, NYG #2 Reno Reservoir Dogs - LaDainian Tomlinson, RB, SDG #2 Minnesota Leftovers - Randy McMichael, TE, MIA #3 New York Mafia - Shaun Alexander, RB, SEA #3 Houston Outlaws - Matt Hasselbeck, QB, SEA #4 Oklahoma Wildcats - Tiki Barber, RB, NYG #4 Las Vegas Aces - Musa Smith, RB, BAL #5 Atlanta Grillz - Edgerrin James, RB, ARI #5 Miami Swamp Stompers - Alge Crumpler, TE, ATL #6 Miami Swamp Stompers - Ronnie Brown, RB, MIA #6 Atlanta Grillz - Jason Witten, TE, DAL #7 Las Vegas Aces - Carnell Williams, RB, TAM #7 Oklahoma Wildcats - Dallas Clark, TE, IND #8 Houston Outlaws - Rudi Johnson, RB, CIN #8 New York Mafia - Joey Galloway, WR, TAM #9 Minnesota Leftovers - Peyton Manning, QB, IND #9 Reno Reservoir Dogs - Donovan McNabb, QB, PHI #10 Boston Bulldogs - Steven Jackson, RB, STL #10 St. Louis River Rats - Braylon Edwards, WR, CLE Round 2 Round 7 #1 Boston Bulldogs - Reggie Bush, RB, NOR #1 St. Louis River Rats - Vince Young, QB, TEN #2 Minnesota Leftovers - LaMont Jordan, RB, OAK #2 Reno Reservoir Dogs - Warrick Dunn, RB, ATL #3 Houston Outlaws - Steve Smith, WR, CAR #3 New York Mafia - Tony Gonzalez, TE, KAN #4 Las Vegas Aces - Torry Holt, WR, STL #4 Oklahoma Wildcats - Jerramy Stevens, TE, SEA #5 Miami Swamp Stompers - Randy Moss, WR, OAK #5 Atlanta Grillz - Keyshawn Johnson, WR, CAR #6 Atlanta Grillz - Willie Parker, RB, PIT #6 Miami Swamp Stompers - Matt Jones, WR, JAC #7 Oklahoma Wildcats - Brian Westbrook, RB, PHI #7 Las Vegas Aces - Terry Glenn, WR, DAL #8 New York Mafia - Marvin Harrison, WR, IND #8 Houston Outlaws - Pittsburgh Steelers, Def, PIT #9 Reno Reservoir Dogs - Clinton Portis, RB, WAS #9 Minnesota Leftovers - Laurence Maroney, RB, NWE #10 St. -

Sports & Esports the Competitive Dream Team

SPORTS & ESPORTS THE COMPETITIVE DREAM TEAM JULIANA KORANTENG Editor-in-Chief/Founder MediaTainment Finance (UK) SPORTS & ESPORTS: THE COMPETITIVE DREAM TEAM 1.THE CROSSOVER: WHAT TRADITIONAL SPORTS CAN BRING TO ESPORTS Professional football, soccer, baseball and motor racing have endless decades worth of experience in professionalising, commercialising and monetising sporting activities. In fact, professional-services powerhouse KPMG estimates that the business of traditional sports, including commercial and amateur events, related media as well as education, academic, grassroots and other ancillary activities, is a US$700bn international juggernaut. Furthermore, the potential crossover with esports makes sense. A host of popular video games have traditional sports for themes. Soccer-centric games include EA’s FIFA series and Konami’s Pro Evolution Soccer. NBA 2K, a series of basketball simulation games published by a subsidiary of Take-Two Interactive, influenced the formation of the groundbreaking NBA 2K League in professional esports. EA is also behind the Madden NFL series plus the NHL, NBA, FIFA and UFC (Ultimate Fighting Championship) games franchises. Motor racing has influenced the narratives in Rockstar Games’ Grand Theft Auto, Gran Turismo from Sony Interactive Entertainment, while Psyonix’s Rocket League melds soccer and motor racing. SPORTS & ESPORTS THE COMPETITIVE DREAM TEAM SPORTS & ESPORTS: THE COMPETITIVE DREAM TEAM In some ways, it isn’t too much of a stretch to see why traditional sports should appeal to the competitive streaks in gamers. Not all those games, several of which are enjoyed by solitary players, might necessarily translate well into the head-to-head combat formats associated with esports and its millions of live-venue and online spectators. -

Draft Harris County – Houston Sports Authority

DRAFT HARRIS COUNTY – HOUSTON SPORTS AUTHORITY MINUTES OF THE BOARD OF DIRECTORS MEETING JUNE 24, 2020 STATE OF TEXAS } HARRIS COUNTY – HOUSTON } SPORTS AUTHORITY } A meeting of the Board of Directors (the “Board”) of the Harris County – Houston Sports Authority (the “Authority”), a sports and community venue district, was held virtually commencing at 10:00 a.m. on Wednesday, June 24, 2020. Written notices of the meeting, including the date, hour, place, agenda, and detailed instructions for connecting to the virtual meeting using Zoom Meetings, were posted in Harris, Fort Bend and Montgomery Counties in accordance with the Texas Open Meetings Act, and an electronic copy of the Agenda was posted on the Authority’s website, as well. Due to health and safety concerns related to COVID-19, this meeting was conducted virtually in accordance with the provisions of Section 551.127 of the Texas Government Code that have not been suspended by order of the Governor. The following Directors participated in the meeting: Chairman J. Kent Friedman, Directors Willie Alexander, Chad Burke, Joseph Callier, Lawrence Catuzzi, Cindy Clifford, Zina Garrison, Martye Kendrick, Dr. Juan Sanchez Munoz, Dr. Laura Murillo, Bruce Oakley, Tom Sprague and Robert Woods. Ms. Janis Burke, CEO for the Authority; Mr. Tom Waggoner, Controller for the Authority; Mr. Mark Arnold, Hunton Andrews Kurth LLP, Counsel for the Authority; Mr. Trey Cash and Ms. Tina Peterman, Masterson Advisors LLC, Financial Advisors for the Authority, were also present. Guests in attendance were: Commissioner Adrian Garcia, Harris County Precinct 2; Mr. Robert Belt, Mr. Mike Brotherton and Mr. Daniel Hebert from Belt Harris Pechachek LLLP, the Authority’s audit firm; Mr. -

Esports Live Broadcast: an Appealing Media for Business-To-Consumer Communication

Internationale Betriebswirtschaft B.A. Hochschule Furtwangen University, Business School Supervised by Prof. Dr. Christoph Mergard eSports live broadcast: An appealing media for business-to-consumer communication A thesis submitted in fulfillment of the requirements for the degree of Bachelor’s of Arts in the faculty of economy by Daniel Fritz Matriculation number 248343 IBW 7 Pestalozzistr. 21 78176 Blumberg [email protected] June 2018 Table of contents Sworn Statement........................................................................................................................... II List of Figures ............................................................................................................................... III Abstract ........................................................................................................................................ IV Introduction .................................................................................................................................. 1 Scope of study ....................................................................................................................... 2 Literature review ........................................................................................................................... 4 Methodology ................................................................................................................................. 7 1. Examination of the eSports industry and eSport live broadcasts ............................................ -

ESL Announces European Grassroots Initiative Expanding Path to Pro League for CS:GO

Jun 26, 2017 16:00 BST ESL Announces European Grassroots Initiative Expanding Path to Pro League for CS:GO The world’s largest esports company, ESL, is today proud to reveal a new initiative to expand its path for aspiring Counter-Strike: Global-Offensive (CS:GO) players to rise through the ranks from the National Championship level onto the amateur ranks in order to qualify for the largest CS:GO league in the world, the ESL Pro League. Starting with ESEA Season 26, the winners of the ESL UK Premiership and the ESL Mistrzostwa Polski, the official national leagues of the UK & Ireland and Poland respectively, will claim a place to compete in the Mountain Dew League (MDL). This unique partnership provides a clear pathway for CS:GO players to progress from amateur ranks to compete on the world stage linking the national leagues to the Pro League through MDL. The investment in the path-to-pro system will continue from Season 27 with ESL’s French, Spanish and German leagues providing qualification spots to the MDL, establishing ESL’s national leagues as the leading grassroots CS:GO leagues in each territory. The already-established ESEA League will continue to run alongside this new initiative. To achieve this, ESL is set to move its European National Championships to be part of ESEA’s system creating promotion spots up to MDL, the only league that feeds directly into the Pro League. The team that wins the National Championship will qualify for the MDL, creating a clear path from there to the Pro League. -

ANNEXURE A: Sanction Outcomes Findings As at 28 September 2020

ANNEXURE A: Sanction Outcomes Findings as at 28 September 2020 # Concessions Net ban Total rounds # Coach Sanction Tier Team Enemy Team Tournament Date Map Round Start Round End Match Link Video Link cases applied (%) (months) triggered iGame.com Tricked Europe Minor Closed Qualifier - PGL Major Krakow 2017 19-Jul-2017 Nuke 0 - 0 22 - 25 47 Match Link Video Link 1 Twista 2 Tier 1 12.50% 15.75 iGame.com Spirit Academy Hellcase Cup 6 6-Sep-2017 Nuke 18 - 18 20 - 22 6 Match Link Video Link maquinas Ambush ESEA Season 32 Advanced Playoffs 14-Nov-2019 Mirage 0 - 0 16 - 7 23 Match Link Video Link 2 casle 2 Tier 2 0 10 maquinas North WESG 2019 North Europe Closed Qualifier 27-Nov-2019 Overpass 4 - 9 16 - 19 22 Match Link Video Link Furious Gaming Latingamers La Liga Pro Trust 2019 - Apertura 25-Aug-2019 Mirage 0 - 0 0 - 1 1 Match Link Video Link 3 dinamito 2 Tier 2 0 10 Furious Gaming Sinisters Aorus League 2019 #3 Southern Cone 6-Sep-2019 Inferno 0 - 0 11 - 16 27 Match Link Video Link 4 ArnoZ1K4 1 Tier 2 0 10 Evidence Reapers Dell Gaming Liga Pro Season 1 - #4 APR/19 12-Apr-2019 Train 0 - 0 16 - 10 26 Match Link Video Link Tricked pro100 LOOT.BET Cup 2 - cs_summit 2 Qualifier 13-Dec-2017 Mirage 0 - 0 11 - 7 18 Match Link Video Link Tricked EURONICS United Masters League 21-Nov-2018 Dust2 0 - 0 4 - 2 6 Match Link Video Link Tricked LDLC United Masters League 28-Nov-2018 Mirage 0 - 0 16 - 12 28 Match Link Video Link Tier 1 5 Rejin 7 45% 19.8 Tricked HAVU Kalashnikov CUP 29-Nov-2018 Train 0 - 0 10 - 15 25 Aggravated Match Link Video Link Tricked -

Comunicacion Y Videojuegos.Pdf

COMUNICACIÓN Y VIDEOJUEGOS. REFLEJANDO LA SOCIEDAD A TRAVÉS DEL OCIO INTERACTIVO — Colección Comunicación y Pensamiento — COMUNICACIÓN Y VIDEOJUEGOS. REFLEJANDO LA SOCIEDAD A TRAVÉS DEL OCIO INTERACTIVO Editor Guillermo Paredes-Otero Autores (por orden de aparición) Guillermo Paredes-Otero Antonio César Moreno Cantano Carlos Álvarez Barroso Jesús Albarrán Ligero Antonio Fco. Campos Méndez Sergio Jesús Villén Higueras Augusto David Beltrán Poot Fernando Martínez López Rafael Jaén Pozo COMUNICACIÓN Y VIDEOJUEGOS. REFLEJANDO LA SOCIEDAD A TRAVÉS DEL OCIO INTERACTIVO Ediciones Egregius www.egregius.es Diseño de cubierta y maquetación: Francisco Anaya Benítez © de los textos: los autores © de la presente edición: Ediciones Egregius N.º 65 de la colección Comunicación y Pensamiento 1ª edición, 2020 ISBN 978-84-18167-35-5 NOTA EDITORIAL: Las opiniones y contenidos publicados en esta obra son de responsabilidad exclusiva de sus autores y no reflejan necesariamente la opinión de Ediciones Egregius ni de los editores o coordinadores de la publicación; asimismo, los autores se responsabilizarán de obtener el permiso correspondiente para incluir material publicado en otro lugar. Colección: Comunicación y Pensamiento Los fenómenos de la comunicación invaden todos los aspectos de la vida cotidiana, el acontecer contemporáneo es imposible de comprender sin la perspectiva de la comu- nicación, desde su más diversos ámbitos. En esta colección se reúnen trabajos acadé- micos de distintas disciplinas y materias científicas que tienen como elemento común la comunicación y el pensamiento, pensar la comunicación, reflexionar para com- prender el mundo actual y elaborar propuestas que repercutan en el desarrollo social y democrático de nuestras sociedades. La colección reúne una gran cantidad de trabajos procedentes de muy distintas partes del planeta, un esfuerzo conjunto de profesores investigadores de universidades e ins- tituciones de reconocido prestigio. -

Esports Yearbook 2017/18

Julia Hiltscher and Tobias M. Scholz eSports Yearbook 2017/18 ESPORTS YEARBOOK Editors: Julia Hiltscher and Tobias M. Scholz Layout: Tobias M. Scholz Cover Photo: Adela Sznajder, ESL Copyright © 2019 by the Authors of the Articles or Pictures. ISBN: to be announced Production and Publishing House: Books on Demand GmbH, Norderstedt. Printed in Germany 2019 www.esportsyearbook.com eSports Yearbook 2017/18 Editors: Julia Hiltscher and Tobias M. Scholz Contributors: Sean Carton, Ruth S. Contreras-Espinosa, Pedro Álvaro Pereira Correia, Joseph Franco, Bruno Duarte Abreu Freitas, Simon Gries, Simone Ho, Matthew Jungsuk Howard, Joost Koot, Samuel Korpimies, Rick M. Menasce, Jana Möglich, René Treur, Geert Verhoeff Content The Road Ahead: 7 Understanding eSports for Planning the Future By Julia Hiltscher and Tobias M. Scholz eSports and the Olympic Movement: 9 A Short Analysis of the IOC Esports Forum By Simon Gries eSports Governance and Its Failures 20 By Joost Koot In Hushed Voices: Censorship and Corporate Power 28 in Professional League of Legends 2010-2017 By Matthew Jungsuk Howard eSports is a Sport, but One-Sided Training 44 Overshadows its Benefits for Body, Mind and Society By Julia Hiltscher The Benefits and Risks of Sponsoring eSports: 49 A Brief Literature Review By Bruno Duarte Abreu Freitas, Ruth S. Contreras-Espinosa and Pedro Álvaro Pereira Correia - 5 - Sponsorships in eSports 58 By Samuel Korpimies Nationalism in a Virtual World: 74 A League of Legends Case Study By Simone Ho Professionalization of eSports Broadcasts 97 The Mediatization of DreamHack Counter-Strike Tournaments By Geert Verhoeff From Zero to Hero, René Treurs eSports Journey. -

The Best Ever? SK Gaming's Coldzera Looks to Claim His Place in CS:GO History

12/1/2017 Counter-Strike Global Offensive star coldzera looks to cement his legacy CS:GO -- coldzera looks to cement legacy 140d - Samuel Delorme Valve must solve two Dota 2 Pro Circuit problems 11h - Alan Bester Lessons from Samsung: Sticking to the script 14h - Emily Rand KSV acquires Samsung Galaxy's League of Legends team 20h - Young Jae Jeon The 2017-2018 League of Legends Roster Shuffle 9d - ESPN Esports A year in review: Lessons from 2017 League of Legends 2d - Kelsey Moser From Overwatch to PUBG: A conversation with the king of games 4d - Young Jae Jeon How the first ever F1 Esports championship was won 5d Trine University builds esports into its plans 7d - Sean Morrison Pulling in Pobelter is Liquid's best move 8d - TheTyler Erzberger best ever? SK Gaming's Seoul Dynasty coach Hocury: 'People are underrcoldzating all theer non-Kaore anlook teams' s to claim his place in 10d - Young Jae Jeon CS:GO history Sources: Zaboutine joins OpTic as head coach 12d - Jacob Wolf Meet the woman behind RunAway 15d Rachel Gu http://www.espn.co.uk/esports/story/_/id/20055264/counter-strike-global-offensive-star-coldzera-looks-cement-legacy 1/13 12/1/2017 Counter-Strike Global Offensive star coldzera looks to cement his legacy CS:GO -- coldzera looks to cement legacy 140d - Samuel Delorme Valve must solve two Dota 2 Pro Circuit problems 11h - Alan Bester Lessons from Samsung: Sticking to the script 14h - Emily Rand SK Gaming swept Cloud9 3-0 to take home the finals victory at ESL One Cologne. -

Esports Marketer's Training Mode

ESPORTS MARKETER’S TRAINING MODE Understand the landscape Know the big names Find a place for your brand INTRODUCTION The esports scene is a marketer’s dream. Esports is a young industry, giving brands tons of opportunities to carve out a TABLE OF CONTENTS unique position. Esports fans are a tech-savvy demographic: young cord-cutters with lots of disposable income and high brand loyalty. Esports’ skyrocketing popularity means that an investment today can turn seri- 03 28 ous dividends by next month, much less next year. Landscapes Definitions Games Demographics Those strengths, however, are balanced by risk. Esports is a young industry, making it hard to navigate. Esports fans are a tech-savvy demographic: keyed in to the “tricks” brands use to sway them. 09 32 Streamers Conclusion Esports’ skyrocketing popularity is unstable, and a new Fortnite could be right Streamers around the corner. Channels Marketing Opportunities These complications make esports marketing look like a high-risk, high-reward proposition. But it doesn’t have to be. CHARGE is here to help you understand and navigate this young industry. Which games are the safest bets? Should you focus on live 18 Competitions events or streaming? What is casting, even? Competitions Teams Keep reading. Sponsors Marketing Opportunities 2 LANDSCAPE LANDSCAPE: GAMES To begin to understand esports, the tra- game Fortnite and first-person shooter Those gains are impressive, but all signs ditional sports industry is a great place game Call of Duty view themselves very point to the fact that esports will enjoy even to start. The sports industry covers a differently.