How Did Too Big to Fail Become Such a Problem for Broker-Dealers?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Explanatory Notes of Flow of Funds

Explanatory Notes of Flow of Funds 1. The Principle and Purpose of Compilation The principle of flow of funds statistics is to break down the economy into sectors, classify transactions, and compile sources and uses of funds for each sector based on double-entry bookkeeping. Finally, the sectoral data are consolidated to draw up flow of funds accounts for the economy as a whole. The purpose of flow of funds statistics is to make up for the lack of financial transactions in national income statistics. Through sectoral breakdown and transaction classification, the flows of funds among various sectors are observed and the relationships between the real and the financial aspects of the economy are understood. Hence, flow of funds accounts has become a fundamental part of the System of National Accounts and Monetary Financial Statistics. 2. Overview of the Contents Flow of funds statistics comprises three tables, "Flow of Funds Matrix," "Financial Assets and Liabilities of All Sectors" and "Year-end Amounts Outstanding of Financial Transaction Items." All the three tables only show financial transactions or outstanding financial assets and liabilities. "Flow of Funds Matrix" (1) The economy is divided into several sectors. Under each sector, two columns, "uses of funds" and "sources of funds," are listed. (2) The "uses of funds" and "sources of funds" are transaction flows that preclude valuation and other changes. Due to insufficient data, these are mostly recorded as changes in the outstanding amounts of financial assets and liabilities for each sector between two specific points in time. For those items, financial transactions reflect changes in financial assets and liabilities of each sector, which are recorded in "uses of funds" and "sources of funds," respectively. -

11.50 Margin Constraints and the Security Market Line

Margin Constraints and the Security Market Line Petri Jylh¨a∗ June 9, 2016 Abstract Between the years 1934 and 1974, the Federal Reserve frequently changed the initial margin requirement for the U.S. stock market. I use this variation in margin requirements to test whether leverage constraints affect the security market line, i.e. the relation between betas and expected returns. Consistent with the theoretical predictions of Frazzini and Ped- ersen (2014), but somewhat contrary to their empirical findings, I find that tighter leverage constraints result in a flatter security market line. My results provide strong empirical sup- port for the idea that funding constraints faced by investors may, at least partially, help explain the empirical failure of the capital asset pricing model. JEL Classification: G12, G14, N22. Keywords: Leverage constraints, Security market line, Margin regulations. ∗Imperial College Business School. Imperial College London, South Kensington Campus, SW7 2AZ, London, UK; [email protected]. I thank St´ephaneChr´etien,Darrell Duffie, Samuli Kn¨upfer,Ralph Koijen, Lubos Pastor, Lasse Pedersen, Joshua Pollet, Oleg Rytchkov, Mungo Wilson, and the participants at American Economic Association 2015, Financial Intermediation Research Society 2014, Aalto University, Copenhagen Business School, Imperial College London, Luxembourg School of Finance, and Manchester Business School for helpful comments. 1 Introduction Ever since the introduction of the capital asset pricing model (CAPM) by Sharpe (1964), Lintner (1965), and Mossin (1966), finance researchers have been studying why the return difference between high and low beta stocks is smaller than predicted by the CAPM (Black, Jensen, and Scholes, 1972). One of the first explanation for this empirical flatness of the security market line is given by Black (1972) who shows that investors' inability to borrow at the risk-free rate results in a lower cross-sectional price of risk than in the CAPM. -

Frictional Finance “Fricofinance”

Frictional Finance “Fricofinance” Lasse H. Pedersen NYU, CEPR, and NBER Copyright 2010 © Lasse H. Pedersen Frictional Finance: Motivation In physics, frictions are not important to certain phenomena: ……but frictions are central to other phenomena: Economists used to think financial markets are like However, as in aerodynamics, the frictions are central dropping balls to the dynamics of the financial markets: Walrasian auctioneer Frictional Finance - Lasse H. Pedersen 2 Frictional Finance: Implications ¾ Financial frictions affect – Asset prices – Macroeconomy (business cycles and allocation across sectors) – Monetary policy ¾ Parsimonious model provides unified explanation of a wide variety of phenomena ¾ Empirical evidence is very strong – Stronger than almost any other influence on the markets, including systematic risk Frictional Finance - Lasse H. Pedersen 3 Frictional Finance: Definitions ¾ Market liquidity risk: – Market liquidity = ability to trade at low cost (conversely, market illiquidity = trading cost) • Measured as bid-ask spread or as market impact – Market liquidity risk = risk that trading costs will rise • We will see there are 3 relevant liquidity betas ¾ Funding liquidity risk: – Funding liquidity for a security = ability to borrow against that security • Measured as the security’s margin requirement or haircut – Funding liquidity for an investor = investor’s availability of capital relative to his need • “Measured” as Lagrange multiplier of margin constraint – Funding liquidity risk = risk of hitting margin constraint -

MAS362/MAS462/MAS6053 Financial Mathematics Problem Sheet 1

MAS362/MAS462/MAS6053 Financial Mathematics Problem Sheet 1 1. Consider a £100, 000 mortgage paying a fixed annual rate of 5% which is com- pounded monthly. What are the monthly repayments if the mortgage is to be repaid in 25 years? 2. You want to deposit your savings for a year and you have the choice of three accounts. The first pays 5% interest per annum, compounded yearly. The second pays 4.8% interest per annum, compounded twice a year. The third pays 4.9% interest per annum, compounded continuously. Which one should you choose? 3. Consider any traded asset whose value vT in T years is known with certainty. −rT Prove that the current value of the asset must be vT e where r is the continuously- compounded T -years interest rate. 4. A perpetual bond is a bond with no maturity, i.e., it pays a fixed payment at fixed intervals forever.1 Under the assumption of constant (continuously compounded) interest rates of 5%, what is the price of a perpetual bond with face value £100 paying annual coupon of 2.50% once a year and whose first coupon payment is due in three months? 5. The prices of zero coupon bonds with face value of £100 and maturity dates in 6, 12 and 18 months are £98, £96 and £93.5 respectively. The price of a 8% bond maturing in 2 years with semiannual coupons is £107. Use the bootstrap method to find the two-year discount factor and spot rates. 6. Consider the following zero-coupon bonds with face value of £100: Time to maturity Annual interest Bond price (in years) (in £) 0.5 0 97.8 1. -

The Contagion of Capital

The Jus Semper Global Alliance In Pursuit of the People and Planet Paradigm Sustainable Human Development March 2021 ESSAYS ON TRUE DEMOCRACY AND CAPITALISM The Contagion of Capital Financialised Capitalism, COVID-19, and the Great Divide John Bellamy Foster, R. Jamil Jonna and Brett Clark he U.S. economy and society at the start of T 2021 is more polarised than it has been at any point since the Civil War. The wealthy are awash in a flood of riches, marked by a booming stock market, while the underlying population exists in a state of relative, and in some cases even absolute, misery and decline. The result is two national economies as perceived, respectively, by the top and the bottom of society: one of prosperity, the other of precariousness. At the level of production, economic stagnation is diminishing the life expectations of the vast majority. At the same time, financialisation is accelerating the consolidation of wealth by a very few. Although the current crisis of production associated with the COVID-19 pandemic has sharpened these disparities, the overall problem is much longer and more deep-seated, a manifestation of the inner contradictions of monopoly-finance capital. Comprehending the basic parameters of today’s financialised capitalist system is the key to understanding the contemporary contagion of capital, a corrupting and corrosive cash nexus that is spreading to all corners of the U.S. economy, the globe, and every aspect of human existence. TJSGA/Essay/SD (E052) March 2021/Bellamy Foster, Jonna and Clark 1 Free Cash and the Financialisation of Capital “Capitalism,” as left economist Robert Heilbroner wrote in The Nature and Logic of Capitalism in 1985, is “a social formation in which the accumulation of capital becomes the organising basis for socioeconomic life.”1 Economic crises in capitalism, whether short term or long term, are primarily crises of accumulation, that is, of the savings-and- investment (or surplus-and-investment) dynamics. -

Effects of Estimating Systematic Risk in Equity Stocks in the Nairobi Securities Exchange (NSE) (An Empirical Review of Systematic Risks Estimation)

International Journal of Academic Research in Accounting, Finance and Management Sciences Vol. 4, No.4, October 2014, pp. 228–248 E-ISSN: 2225-8329, P-ISSN: 2308-0337 © 2014 HRMARS www.hrmars.com Effects of Estimating Systematic Risk in Equity Stocks in the Nairobi Securities Exchange (NSE) (An Empirical Review of Systematic Risks Estimation) Paul Munene MUIRURI Department of Commerce and Economic Studies Jomo Kenyatta University of Agriculture and Technology Nairobi, Kenya, E-mail: [email protected] Abstract Capital Markets have become an integral part of the Kenyan economy. The manner in which securities are priced in the capital market has attracted the attention of many researchers for long. This study sought to investigate the effects of estimating of Systematic risk in equity stocks of the various sectors of the Nairobi Securities Exchange (NSE. The study will be of benefit to both policy makers and investors to identify the specific factors affecting stock prices. To the investors it will provide useful and adequate information an understanding on the relationship between risk and return as a key piece in building ones investment philosophy. To the market regulators to establish the NSE performance against investors’ perception of risks and returns and hence develop ways of building investors’ confidence, the policy makers to review and strengthening of the legal and regulatory framework. The paper examines the merged 12 sector equity securities of the companies listed at the market into 4sector namely Agricultural; Commercial and Services; Finance and Investment and Manufacturing and Allied sectors. This study Capital Asset Pricing Model (CAPM) of Sharpe (1964) to vis-à-vis the market returns. -

The Capital Asset Pricing Model (Capm)

THE CAPITAL ASSET PRICING MODEL (CAPM) Investment and Valuation of Firms Juan Jose Garcia Machado WS 2012/2013 November 12, 2012 Fanck Leonard Basiliki Loli Blaž Kralj Vasileios Vlachos Contents 1. CAPM............................................................................................................................................... 3 2. Risk and return trade off ............................................................................................................... 4 Risk ................................................................................................................................................... 4 Correlation....................................................................................................................................... 5 Assumptions Underlying the CAPM ............................................................................................. 5 3. Market portfolio .............................................................................................................................. 5 Portfolio Choice in the CAPM World ........................................................................................... 7 4. CAPITAL MARKET LINE ........................................................................................................... 7 Sharpe ratio & Alpha ................................................................................................................... 10 5. SECURITY MARKET LINE ................................................................................................... -

The Federal Reserve's Commercial Paper Funding Facility

Tobias Adrian, Karin Kimbrough, and Dina Marchioni The Federal Reserve’s Commercial Paper Funding Facility 1.Introduction October 7, 2008, with the aim of supporting the orderly functioning of the commercial paper market. Registration for he commercial paper market experienced considerable the CPFF began October 20, 2008, and the facility became Tstrain in the weeks following Lehman Brothers’ operational on October 27. The CPFF operated as a lender- bankruptcy on September 15, 2008. The Reserve Primary of-last-resort facility for the commercial paper market. It Fund—a prime money market mutual fund with $785 million effectively extended access to the Federal Reserve’s discount in exposure to Lehman Brothers—“broke the buck” on window to issuers of commercial paper, even if these issuers September 16, triggering an unprecedented flight to quality were not chartered as commercial banks. Unlike the discount from high-yielding to Treasury-only money market funds. window, the CPFF was a temporary liquidity facility that was These broad investor flows within the money market sector authorized under section 13(3) of the Federal Reserve Act in severely disrupted the ability of commercial paper issuers to the event of “unusual and exigent circumstances.” It expired roll over their short-term liabilities. February 1, 2010.1 As redemption demands accelerated, particularly in high- The goal of the CPFF was to address temporary liquidity yielding money market mutual funds, investors became distortions in the commercial paper market by providing a increasingly reluctant to purchase commercial paper, especially backstop to U.S. issuers of commercial paper. This liquidity for longer dated maturities. -

Investment Banking Compliance

© Practising Law Institute Chapter 49 Investment Banking Compliance Russell D. Sacks* Partner, Shearman & Sterling LLP Richard B. Alsop Partner, Shearman & Sterling LLP [Chapter 49 is current as of June 15, 2018.] § 49:1 Information § 49:1.1 Insider Trading [A] Generally [B] Legal Framework [B][1] Securities Exchange Act § 10(b) [B][2] Insider Trading and Securities Fraud Enforcement Act § 49:1.2 Information Barriers [A] Generally [B] Effective Information Barriers: Minimum Elements [B][1] Written Policies and Procedures [B][2] Wall-Crossing Procedures [B][3] Restricted List and Watch List [B][4] Surveillance of Trading Activity * The authors gratefully acknowledge the contributions to this chapter of former co-author and former partner Robert Evans III, and the contribu- tions of Shearman & Sterling LLP associate Steven R. Blau for his work coordinating the chapter. (Broker-Dealer Reg., Rel. #14, 9/18) 49–1 © Practising Law Institute BROKER-DEALER REGULATION [B][5] Physical and Electronic Separation [B][6] Training and Education Programs [B][7] Employee Attestation § 49:1.3 Sales Practices; Testing-the-Waters and Gun-Jumping § 49:1.4 2012 OCIE Report on the Use of Material Nonpublic Information by Broker-Dealers [A] Sources of MNPI [B] Control Structure [B][1] Issues Identified [B][2] Control Room [B][3] “Above the Wall” Designations [B][4] Materiality Determinations [B][5] Oversight of Non-Transactional Sources of MNPI [B][6] Compliance with Oral Confidentiality Agreements [B][7] Personal Trading Problems [C] Access Controls [C][1] -

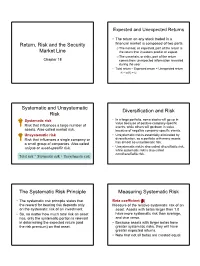

Return, Risk and the Security Market Line Systematic and Unsystematic

Expected and Unexpected Returns • The return on any stock traded in a Return, Risk and the Security financial market is composed of two parts. c The normal, or expected, part of the return is Market Line the return that investors predict or expect. d The uncertain, or risky, part of the return Chapter 18 comes from unexpected information revealed during the year. • Total return – Expected return = Unexpected return R – E(R) = U Systematic and Unsystematic Diversification and Risk Risk Systematic risk • In a large portfolio, some stocks will go up in value because of positive company-specific Risk that influences a large number of events, while others will go down in value assets. Also called market risk. because of negative company-specific events. Unsystematic risk • Unsystematic risk is essentially eliminated by Risk that influences a single company or diversification, so a portfolio with many assets a small group of companies. Also called has almost no unsystematic risk. unique or asset-specific risk. • Unsystematic risk is also called diversifiable risk, while systematic risk is also called nondiversifiable risk. Total risk = Systematic risk + Unsystematic risk The Systematic Risk Principle Measuring Systematic Risk • The systematic risk principle states that Beta coefficient (β) the reward for bearing risk depends only Measure of the relative systematic risk of an on the systematic risk of an investment. asset. Assets with betas larger than 1.0 • So, no matter how much total risk an asset have more systematic risk than average, has, only the systematic portion is relevant and vice versa. in determining the expected return (and • Because assets with larger betas have the risk premium) on that asset. -

Understanding Interest Rates Mishkin, Chapter 4:Part B (Pp. 80-89)

Understanding Interest Rates Mishkin, Chapter 4:Part B (pp. 80-89) Prof. Leigh Tesfatsion Economics Department Iowa State University Last Revised: 21 February 2011 Mishkin Chapter 4: Part B (pp. 80-89) Key In-Class Discussion Questions & Issues Reading bond pages in financial news outlets “Interest rate” versus “return rate” “Nominal rate” vs. “real rate” What is “interest rate risk”? Whose risk is it? Reading Bond Pages •• WeWe willwill taketake aa looklook atat aa typicaltypical bondbond pagepage appearingappearing inin financialfinancial sectionsection ofof aa newspapernewspaper •• TheseThese bondbond pagespages covercover – U.S. Treasury (“government”) bonds and notes – U.S. Treasury bills – Corporate bonds Example of a Bond Page of a Newspaper Wall Street Journal, Jan 12, 2006 Types of U.S. Government Bonds Treasury Bills (Zero-coupon) discount bonds Face value paid at maturity Maturities up to one year Treasury Notes Coupon bonds Coupon payments paid semiannually Face value paid at maturity Maturities from 1 to 10 years U.S. Government Bonds…Continued Treasury Bonds Coupon bonds Coupon payments paid semiannually Face value paid at maturity Maturities over 10 years The 30-year bond is called the long bond. Treasury Strips Collection of (zero-coupon) discount bonds Created by separately “stripping” the coupons and face value from a Treasury bond or note. U.S. Government Bonds … Continued • Low default risk. Considered to be risk-free. • Interest exempt from state and local taxes. • Initial issues sold in Treasury auctions (primary market) • Thereafter regularly traded (resold) in an OTC market (secondary market). Corporate Bonds • Corporate Coupon Bonds − Secured by real property − Ownership of the property reverts to the bondholders upon default. -

A Perspective on the South African Flow of Funds Compilation – Theory and Analysis

A perspective on the South African flow of funds compilation – theory and analysis Barend de Beer,1 Nonhlanhla Nhlapo2 and Zeph Nhleko3 1. Introduction The National Financial Account (NFA), also known as flow of funds (FoF), is a financial analysis system that shows the uses of savings and other sources of funds as well as borrowings of funds by institutions to finance real or financial investment through financial instruments. It represents the systematic recording of financial transactions between different sectors of the economy, with the aim of assisting policymakers in assessing the financial position of the national economy as well as subsectors of the economy. The NFA is an extension of the national income and production accounts, as it provides information on financial flows in addition to real economic activity. The South African Reserve Bank (SARB) is the official compiler of South Africa’s NFA. South Africa has a complex financial system4 that consists of several institutional sectors. For the purposes of compiling the FoF, economic activity and transactions between resident and non-resident units must be recorded. The rest of the world is defined as the foreign institutional sector while resident institutional units are grouped into the private sector and the public sector. The private sector consists of institutional units not controlled or owned by institutional units in the general government sector. The public sector consists of institutional units in the general government sector and corporate institutional units in the financial and non-financial sectors owned or controlled by units in the general government sector. The public sector therefore consists of the public financial business enterprises, public non- financial business enterprises and the general government.