Product Intervention Analysis Binary Options

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

V. Black-Scholes Model: Derivation and Solution

V. Black-Scholes model: Derivation and solution Beáta Stehlíková Financial derivatives, winter term 2014/2015 Faculty of Mathematics, Physics and Informatics Comenius University, Bratislava V. Black-Scholes model: Derivation and solution – p.1/36 Content Black-Scholes model: • Suppose that stock price follows a geometric ◦ S Brownian motion dS = µSdt + σSdw + other assumptions (in a moment) We derive a partial differential equation for the price of ◦ a derivative Two ways of derivations: • due to Black and Scholes ◦ due to Merton ◦ Explicit solution for European call and put options • V. Black-Scholes model: Derivation and solution – p.2/36 Assumptions Further assumptions (besides GBP): • constant riskless interest rate ◦ r no transaction costs ◦ it is possible to buy/sell any (also fractional) number of ◦ stocks; similarly with the cash no restrictions on short selling ◦ option is of European type ◦ Firstly, let us consider the case of a non-dividend paying • stock V. Black-Scholes model: Derivation and solution – p.3/36 Derivation I. - due to Black and Scholes Notation: • S = stock price, t =time V = V (S, t)= option price Portfolio: 1 option, stocks • δ P = value of the portfolio: P = V + δS Change in the portfolio value: • dP = dV + δdS From the assumptions: From the It¯o • dS = µSdt + σSdw, ∂V ∂V 1 2 2 ∂2V ∂V lemma: dV = ∂t + µS ∂S + 2 σ S ∂S2 dt + σS ∂S dw Therefore: • ∂V ∂V 1 ∂2V dP = + µS + σ2S2 + δµS dt ∂t ∂S 2 ∂S2 ∂V + σS + δσS dw ∂S V. Black-Scholes model: Derivation and solution – p.4/36 Derivation I. -

Computation of Binomial Option Pricing Model with Parallel

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by KHALSA PUBLICATIONS I S S N 2 2 7 8 - 5 6 1 2 Volume 11 Number 5 International Journal of Management and Information T e c h n o l o g y Computation Of Binomial Option Pricing Model With Parallel Processing On A Linux Cluster Harya Widiputra Faculty of Information Technology, Perbanas Institute Jakarta, Indonesia [email protected] ABSTRACT Binary Option Pricing Model (BOPM) is one approach that can be utilized to calculate the value of either call or put option. BOPM generally works by building a binomial tree diagram, also known as lattice diagram to explore all possible option values that occur based on the intrinsic price of the underlying asset in a range of specific time period. Due to its basic characteristics BOPM is renowned for its longer lead times in calculating option values while also acknowledged as a technique that can provide an assessment of the most fair option value. Therefore, this study aims to shorten the BOPM completion time of calculating the value of an option by building a computer cluster and presently implement the BOPM algorithm into a form that can be run in parallel processing. As an outcome, a Linux-based computer cluster has been built and conversion of BOPM algorithm so that it can be executed in parallel has been performed and also implemented using Python in this research. Conclusively, results of conducted experiments confirm that the implementation of BOPM algorithm in a form that can be executed in parallel and its application on a computer cluster was able to limit the growth of the completion time whilst at the same time maintain quality of calculated option values. -

Opposition, CFTC V. Banc De Binary

Case 2:13-cv-00992-MMD-VCF Document 37 Filed 08/08/13 Page 1 of 30 Kathleen Banar, Chief Trial Attorney (IL Bar No. 6200597) David Slovick, Senior Trial Attorney (IL Bar No. 6257290) Margaret Aisenbrey, Trial Attorney (Mo Bar No. 59560) U.S. Commodity Futures Trading Commission 1155 21 St. NW Washington, DC 20581 [email protected], [email protected], [email protected] (202) 418-5335 (202) 418-5987 (facsimile) Blaine T. Welsh (NV Bar No. 4790) Assistant United States Attorney United States Attorney’s Office 333 Las Vegas Boulevard, Suite 5000 Las Vegas, Nevada 89101 [email protected] (702) 388-6336 (702) 388-6787 (facsimile) UNITED STATES DISTRICT COURT DISTRICT OF NEVADA ) U.S. COMMODITY FUTURES TRADING ) COMMISSION, ) ) Case No. 2:13-cv-00992-MMD-VCF Plaintiff, ) ) PLAINTIFF’S OPPOSITION TO v. ) DEFENDANT’S MOTION TO ) DISMISS COUNTS ONE, THREE ) AND FOUR OF THE COMPLAINT BANC DE BINARY LTD. (A/K/A E.T. ) BINARY OPTIONS LTD.), ) ) Defendant. ) ) 1 Case 2:13-cv-00992-MMD-VCF Document 37 Filed 08/08/13 Page 2 of 30 The United States Commodity Futures Trading Commission (“CFTC” or “Commission”) opposes Banc de Binary’s Motion to Dismiss Counts I, III and IV of the Complaint (“Defendant’s Motion”),1 and states as follows: I. SUMMARY Since at least May 2012 Banc de Binary Ltd. (A/K/A E.T. Binary Options) (“Banc de Binary” or “Defendant”) has been violating the CFTC’s long-standing ban on trading options contracts with persons located in the United States off of a contract market designated by the CFTC for that purpose (i.e., “off-exchange”). -

What Are Binary Options?

PA R T I Introduction to Binary Options his section will provide you with an overview and discussion of the T main benefi ts of binary option trading. What You Will Learn: • What are binary options? • How do binary options differ from traditional options? • Which underlying instruments are binary options available to trade on? • Where can youhttp://www.pbookshop.com trade binary options? • What are the benefi ts of trading binary options? • What makes binary options unique compared to other instruments and options? COPYRIGHTED MATERIAL When you complete this section you should have a basic understand- ing of what binary options are and be familiar with their main advantages. 1 c01.indd 1 11/8/2012 4:12:44 PM http://www.pbookshop.com c01.indd 2 11/8/2012 4:12:44 PM CH A P T E R 1 What Are Binary Options? inary options are also known as digital options or all‐or‐nothing options. They are derivative instruments that can be considered a B yes‐or‐no proposition—either the event happens or it does not. Binary options are considered binary because there are only two po- tential outcomes at expiration: 0 or 100; 0 and 100 refer to the settlement value of a binary option and could be viewed in dollars. At expiration, if you are incorrect, you do not make anything ($0), and if you are correct, you make up to $100. The next section will go into further detail on the set- tlement value of binary options. ON WHAT ASSEThttp://www.pbookshop.com CLASSES ARE BINARY OPTIONS AVAILABLE? Binary options are available on four different asset classes. -

How to Trade Binary Options Successfully

How to Trade Binary Options Successfully A Complete Guide to Binary Options Trading By Meir Liraz ___________________________________________________________________ Revealed At Last! The Best Kept Secret Among Successful Binary Options and Forex Traders The Easiest Way to Make Money Trading Online ___________________________________________________________________ Published by BizMove Binary Options Trading Center Copyright © Meir Liraz. All Rights Reserved. Our Preferred Binary Options Broker We currently trade at this broker. After testing several Binary Options and Forex platforms we find this one to be the best. What made the difference is a unique feature that allow us to watch and copy the strategies and trades of the best performing traders on the platform. You can actually see each move the "Guru" traders make. This method works nicely for us. Since we started trading at this broker we noticed an increase of our successful trades and profits when compared to our former brokers. Having said that, please note that all trading involves risk. Only risk capital you're prepared to lose. Past performance does not guarantee future results. This post is for educational purposes and should not be considered as investment advice. Table of Contents 1. The Single Most Critical Factor to Binary Options Trading Success 2. What are Binary Options 3. The Flow of Decisions in a Binary Options Trade 4. Advantages and Disadvantages of Binary Options Trading 5. Binary Trading Risk Management 6. What You Need to Succeed in Binary Options 7. How Much Money You Need to Start Trading 8. Technical Analysis As a Tool for Binary Trading Success 9. Developing a Binary Options Strategy and Entry Signals 10. -

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Chi Gao 12/15/2013 Abstract: I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II. The Black-Scholes Formula (the price of European call option is calculated) is calculated using two methods: (1) risk-neutral pricing formula (expected discounted payoff) (2) directly solving the Black-Scholes equation with boundary conditions III. The two methods in II are proved to be essentially equivalent. The Black-Scholes formula for European call option is tested to be the solution of Black-Scholes equation. IV. The value of digital options and share digitals are calculated. The European call and put options are be replicated by digital options and share digitals, thus the prices of call and put options can be derived from the values of digitals. The put-call parity relation is given. 1. The derivation(s) of Black-Scholes Equation Black Scholes model has several assumptions: 1. Constant risk-free interest rate: r 2. Constant drift and volatility of stock price: 3. The stock doesn’t pay dividend 4. No arbitrage 5. No transaction fee or cost 6. Possible to borrow and lend any amount (even fractional) of cash at the riskless rate 7. Possible to buy and sell any amount (even fractional) of stock A typical way to derive the Black-Scholes equation is to claim that under the measure that no arbitrage is allowed (risk-neutral measure), the drift of stock price equal to the risk-free interest rate . That is (usually under risk-neutral measure, we write Brownian motion as , here we remove Q subscript for convenience ) (1) Then apply Ito’s lemma to the discounted price of derivatives , we get [ ] [( ) ] (2) Still, under risk-neutral measure we can argue that is martingale. -

Introduction Section 4000.1

Introduction Section 4000.1 This section contains product profiles of finan- Each product profile contains a general cial instruments that examiners may encounter description of the product, its basic character- during the course of their review of capital- istics and features, a depiction of the market- markets and trading activities. Knowledge of place, market transparency, and the product’s specific financial instruments is essential for uses. The profiles also discuss pricing conven- examiners’ successful review of these activities. tions, hedging issues, risks, accounting, risk- These product profiles are intended as a general based capital treatments, and legal limitations. reference for examiners; they are not intended to Finally, each profile contains references for be independently comprehensive but are struc- more information. tured to give a basic overview of the instruments. Trading and Capital-Markets Activities Manual February 1998 Page 1 Federal Funds Section 4005.1 GENERAL DESCRIPTION commonly used to transfer funds between depository institutions: Federal funds (fed funds) are reserves held in a bank’s Federal Reserve Bank account. If a bank • The selling institution authorizes its district holds more fed funds than is required to cover Federal Reserve Bank to debit its reserve its Regulation D reserve requirement, those account and credit the reserve account of the excess reserves may be lent to another financial buying institution. Fedwire, the Federal institution with an account at a Federal Reserve Reserve’s electronic funds and securities trans- Bank. To the borrowing institution, these funds fer network, is used to complete the transfer are fed funds purchased. To the lending institu- with immediate settlement. -

Pricing Credit Default Swaps with Parisian and Parasian Default Mechanics

University of Wollongong Research Online Faculty of Engineering and Information Faculty of Engineering and Information Sciences - Papers: Part B Sciences 2019 Pricing credit default swaps with Parisian and Parasian default mechanics Wenting Chen Jiangnan University, [email protected] Xinjiang He University of Wollongong, [email protected] Sha Lin Zhejiang Gongshang University, [email protected] Follow this and additional works at: https://ro.uow.edu.au/eispapers1 Part of the Engineering Commons, and the Science and Technology Studies Commons Recommended Citation Chen, Wenting; He, Xinjiang; and Lin, Sha, "Pricing credit default swaps with Parisian and Parasian default mechanics" (2019). Faculty of Engineering and Information Sciences - Papers: Part B. 3189. https://ro.uow.edu.au/eispapers1/3189 Research Online is the open access institutional repository for the University of Wollongong. For further information contact the UOW Library: [email protected] Pricing credit default swaps with Parisian and Parasian default mechanics Abstract This paper proposes Parisian and Parasian default mechanics for modeling the credit risks of the CDS (credit default swap) contracts. Unlike most of the structural models used in the literature, our new model assumes that the default will occur only if the price of the reference asset stays below a certain level for a pre-described period of time. To work out the corresponding CDS price, a general pricing formula containing the unknown no-default probability is derived first. It is then shown that the determination of such a probability is equivalent to the valuation of a Parisian or Parasian down-and-out binary options, depending on how the time is recorded. -

AP-15-12 BINARY ACADEMICS, ) ) Respondents

STATE OF MISSOURI OFFICE OF SECRETARY OF STATE IN THE MATTER OF: ) ) SPOTFN.COM, SPOT FN, LLC; ) JAMES KINGSLEY; BINARY HOLDINGS; and ) Case No. AP-15-12 BINARY ACADEMICS, ) ) Respondents. ) FINAL ORDER TO CEASE AND DESIST AND ORDER AWARDING COSTS, RESTITUTION, AND CIVIL PENALTIES Now on the 11th day of February, 2016, the Commissioner, having reviewed this matter, issues the following findings and order: I. PROCEDURAL BACKGROUND 1. On March 27, 2015, the Enforcement Section of the Securities Division of the Office of Secretary of State (the “Enforcement Section”), through Director of Enforcement John Phillips, submitted a Petition for Order to Cease and Desist and Order to Show Cause why Restitution, Civil Penalties, and Costs Should not be Imposed in the above- referenced matter. 2. On April 2, 2015, the Commissioner issued an Order to Cease and Desist and Order to Show Cause why Restitution, Civil Penalties, and Costs Should not be Imposed (“Order”) in the above-referenced matter. On that same day, a copy of the Order and Notice of Right to Request a Hearing were sent via registered mail, return receipt requested, to Respondents at the following addresses: a. SpotFN.com, Spot FN, LLC, and James Kingsley at 25 Old Broad Street, 6th Floor, London, EC2N 1HN, United Kingdom; and b. Binary Holdings and Binary Academics at 405 Lexington Ave., 26th Floor, New York, NY 10174. 3. On or around April 2, 2015, a copy of the Order was made available to the general public 1 on the Missouri Secretary of State’s website. 1 http://www.sos.mo.gov/cmsimages/securities/orders/AP-15-12.pdf. -

12 CFR Ch. I (1–1–21 Edition)

Comptroller of the Currency, Treasury Pt. 3 be consistent with the requirements agreeing to compensate the bank for and principles of this section. the use of its premises, employees, or (b) It is an unsafe and unsound prac- good will. However, the employee, offi- tice for any director, officer, employee, cer, director, or principal shareholder or principal shareholder of a national shall turn over to the bank as com- bank (including any entity in which pensation all income received from the this person owns an interest of more sale of the credit life insurance to the than ten percent), who is involved in bank’s loan customers. the sale of credit life insurance to loan (b) Income derived from credit life in- customers of the national bank, to surance sales to loan customers may be take advantage of that business oppor- credited to an affiliate operating under tunity for personal profit. Rec- the Bank Holding Company Act of 1956, ommendations to customers to buy in- surance should be based on the benefits 12 U.S.C. 1841 et seq., or to a trust for of the policy, not the commissions re- the benefit of all shareholders, pro- ceived from the sale. vided that the bank receives reasonable (c) Except as provided in §§ 2.4 and compensation in recognition of the role 2.5(b), and paragraph (d) of this section, played by its personnel, premises, and a director, officer, employee, or prin- good will in credit life insurance sales. cipal shareholder of a national bank, or Reasonable compensation generally an entity in which such person owns an means an amount equivalent to at interest of more than ten percent, may least 20 percent of the affiliate’s net in- not retain commissions or other in- come attributable to the bank’s credit come from the sale of credit life insur- life insurance sales. -

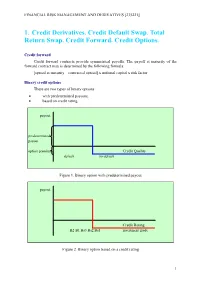

1. Credit Derivatives. Credit Default Swap. Total Return Swap. Credit Forward

FINANCIAL RISK MANAGEMENT AND DERIVATIVES [235221] 1. Credit Derivatives. Credit Default Swap. Total Return Swap. Credit Forward. Credit Options. Credit forward Credit forward contracts provide symmetrical payoffs. The payoff at maturity of the forward contract may is determined by the following formula: [spread at maturity – contracted spread] x notional capital x risk factor Binary credit options There are two types of binary options with predetermined payouts, based on credit rating. payout predetermined payout option premium Credit Quality default no default Figure 1. Binary option with predetermined payout payout Credit Rating B2 B1 Ba3 Ba2 Ba1 investment grade Figure 2. Binary option based on a credit rating 1 FINANCIAL RISK MANAGEMENT AND DERIVATIVES [235221] Credit Swaps Cash Payment if Credit risky Investment Credit Default Dealer Z assets protection (credit buyer protection (bank Y) seller) Total return Swap Premium Figure 3. Credit Default Swap with a Cash Payment Upon Default Credit risky Investment Credit LIBOR + spread Dealer Z assets protection (credit buyer protection (bank Y) seller) Total return Total return Figure 4. Credit Default Swap with a Periodic Payment Investor 1 Payment for a credit event associated Investor 2 Bond A with bond A Bond B Payment for a credit event associated with bond A 2 FINANCIAL RISK MANAGEMENT AND DERIVATIVES [235221] Figure 5. Reciprocal Credit Default Swap Total Return Swap Credit risky Investment Credit LIBOR + spread Investor Y assets protection (credit risk buyer buyer) (dealer Z) Total return Total return Figure 6. Total Return Credit Swap 3 FINANCIAL RISK MANAGEMENT AND DERIVATIVES [235221] Problem 1. Credit Forward Bank Y buys a credit spread forward. -

Giant.Exchange White Paper

Giant.Exchange White Paper Giant.Exchange White Paper 2 Introduction 3 Binary Options Industry 5 What is Giant.Exchange 8 Giant.Exchange Platform 10 Giant.Exchange Underlying Asset 15 Giant.Exchange Use Cases 17 Giant.Exchange Budget 20 Giant.Exchange Reputation System 21 Giant.Exchange Voting System 22 Giant.Exchange Airdrop 23 Summary 24 Reference 25 Giant.Exchange White Paper version 1.2 11 September 2018 2 Introduction A Binary Option is a contract which provides either a fixed amount of payoff or no payoff at all depending on the fulfillment of the agreed terms at a specified time. Usually, an option is bought in advance at a fixed price and the result of this purchase is either positive (the difference between the reward and the cost of the option) or negative (the cost of the option). Commonly, the size of the reward is several times the size of an option. Usually, the substance of a binary option is whether the stock price of the underlying asset will be above or below the certain level. Herewith, the reward is paid in case when option wins, regardless of the degree of a price change. In order to receive a payoff it is enough to specify the correct price movement. Binary options provide an opportunity to accurately calculate the amount of payments and potential risks before the option is purchased. This gives an opportunity to easily manage a large portfolio of such contracts. There are three main types of Binary Options: ● Call and put options. Betting on the price fixed in a certain time point.