Excessive(?) Entry of National Telecom Networks, 1990–2001

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Telecom in the Time of Crash

INCIDENTAL PAPER Telecom in the Time of Crash Kas Kalba November 2002 Program on Information Resources Policy Center for Information Policy Research Harvard University The Program on Information Resources Policy is jointly sponsored by Harvard University and the Center for Information Policy Research. Chairman Managing Director Anthony G. Oettinger John C. B. LeGates Kas Kalba is President of Kalba International, Inc., a management consulting and research firm. He is writing a book on the telecom crash, from which this paper is derived, and has been a longstanding participant in PIRP activities. Copyright © 2002 by Kas Kalba. Not to be reproduced in any form without written consent from Kas Kalba, Kalba International. Inc., 23 Sandy Pond Road, Lincoln, 01773, USA. +1 (781) 259-9589. E-mail: [email protected] URL: http://www.kalbainternational.com ISBN 1-879716-85-2 I-02-2 November 2002 PROGRAM ON INFORMATION RESOURCES POLICY Harvard University Center for Information Policy Research Affiliates AT&T Corp. Nippon Telegraph & Telephone Corp Australian Telecommunications Users (Japan) Group PDS Consulting BellSouth Corp. PetaData Holdings, Inc. The Boeing Company Samara Associates Booz Allen Hamilton Skadden, Arps, Slate, Meagher & Flom Center for Excellence in Education LLP Commission of the European Sonexis Communities Strategy Assistance Services Critical Path TOR LLC CyraCom International United States Government: Ellacoya Networks, Inc. Department of Commerce Hanaro Telecom Corp. (Korea) National Telecommunications and Hearst Newspapers Information Administration Hitachi Research Institute (Japan) Department of Defense IBM Corp. National Defense University Korea Telecom Department of Health and Human Lee Enterprises, Inc. Services Lexis–Nexis National Library of Medicine John and Mary R. -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

Worldcom1 Ethics Case Study

fWorldCom1 By Dennis Moberg (Santa Clara University) and Edward Romar (University of Massachusetts- Boston) An update for this case is available. 2002 saw an unprecedented number of corporate scandals: Enron, Tyco, Global Crossing. In many ways, WorldCom is just another case of failed corporate governance, accounting abuses, and outright greed. But none of these other companies had senior executives as colorful and likable as Bernie Ebbers. A Canadian by birth, the 6 foot, 3 inch former basketball coach and Sunday School teacher emerged from the collapse of WorldCom not only broke but with a personal net worth as a negative nine-digit number.2 No palace in a gated community, no stable of racehorses or multi-million dollar yacht to show for the telecommunications giant he created. Only debts and red ink--results some consider inevitable given his unflagging enthusiasm and entrepreneurial flair. There is no question that he did some pretty bad stuff, but he really wasn't like the corporate villains of his day: Andy Fastow of Enron, Dennis Koslowski of Tyco, or Gary Winnick of Global Crossing.3 Personally, Bernie is a hard guy not to like. In 1998 when Bernie was in the midst of acquiring the telecommunications firm MCI, Reverend Jesse Jackson, speaking at an all-black college near WorldCom's Mississippi headquarters, asked how Ebbers could afford $35 billion for MCI but hadn't donated funds to local black students. Businessman LeRoy Walker Jr., was in the audience at Jackson's speech, and afterwards set him straight. Ebbers had given over $1 million plus loads of information technology to that black college. -

In Re: Global Crossing, Ltd. Securities Litigation 02-CV-00910-Notice Of

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK ________________________________________________ x IN RE GLOBAL CROSSING, LTD. : Case No. 02 Civ. 910 (GEL) SECURITIES LITIGATION : ________________________________________________ x NOTICE OF PROPOSED CLASS ACTION PARTIAL SETTLEMENT, MOTION FOR ATTORNEYS' FEES AND FAIRNESS HEARING IN CONNECTION WITH THE ANDERSEN SETTLEMENT If You Bought or Exchanged Global Crossing Ltd. Securities or Asia Global Crossing Ltd. Securities between February 1, 1999 and December 8, 2003, you might be a member of the class in this action entitling you to receive relief in connection with a partial settlement of the action. A federal court authorized this Notice. This is not a solicitation from a lawyer. ■ On July 7, 2005, a settlement between the plaintiffs and Arthur Andersen LLP (the “Settlement”) was preliminarily approved by the Court in the action captioned above. The Settlement partially resolves a lawsuit over whether the prices of common stock, convertible preferred stock and bonds of Global Crossing and Asia Global Crossing were artificially inflated as a result of alleged fraudulent misrepresentations and non-disclosures and violations of federal securities laws. ■ The Settlement provides for a Settlement Fund of approximately $25 million, less fees and costs. The amount to be distributed among the class members will be divided between Global Crossing and Asia Global Crossing securities purchasers, with Global Crossing securities purchasers getting 92% of the amount and Asia Global Crossing securities purchasers getting the remaining 8%. ■ As explained below, this is the third partial settlement in this lawsuit. If you qualify and have not filed a claim in either of the prior settlements and would like to submit one, you may do so. -

Certificate of Service

CERTIFICATE OF SERVICE I, Charlotte R. Graham, hereby certify that the persons on the attached list were served copies ofthe Public Notice ofNetwork Change Under Rule 51.329(a) filed on the 26th day of July, 2002, with the Secretary, Federal Communications Commission. Such notification was provided via U.S. First Class Mail, postage prepaid, or by electronic transmission at least five business days in advance of filing with the Commission. ~Q.~ Charlotte R. Graham _ ..__._-------------------------------------- 1-800-Reconex 1-800-Reconex 1-800-Reconex Bill Braun Jennifer Loewen Dale Merten 2500 Industrial Ave. 2500 Industrial Avenue 2500 Industrial Avenue Hubbard, OR 97032 Hubbard, OR 97032 Hubbard, OR 97032 1-800-Reconex 2-Infinity Access America Jennifer Sikes Lex Long Dan Barnett 2500 Industrial Ave 4828 Loop Central Dr. 315 W. Oakland Ave. Hubbard, OR 97032 Ste. 100 Johnson City, TN 37601 Houston, TX 77081 Access America Access Long Distance Access Long Distance Jack Coker Tammy Hampton Christina Moody 138 Fairbanks Plaza 215 S. State Street 3753 Howard Hughes Pkwy Oakridge, TN 37830 Salt Lake City, UT 84111 Suite 131 Las Vegas, NV 89109 Access One (The Other Phone Company) ACN Communications ACT (Alternate Communications Kevin Griffo S. Meyer Technology) 3427 NW. 55th 32991 Hamilton Benjamin Bickham Ft. Lauderdale, FL 33309 Farmington Hills, MI 48334 6253 W. 800 N. Fountaintown, IN 46130 Adams Communications Adelphia Business Solutions Adelphia Business Solutions Jimmy Adams Rebecca Baldwin Stacey Chick P.O. Box 487 1221 Lamar Street 121 Champion Way Marianna, FL 324470487 Ste. 1175 Canonsburg, PA 15317 Houston, TX 770I0 Adelphia Business Solutions Adelphia Business Solutions Adelphia Business Solutions Rod Fletcher Richard Kindred Janet Livengood 121 Champion Way 500 Atrium Drive 3000 K St., NW. -

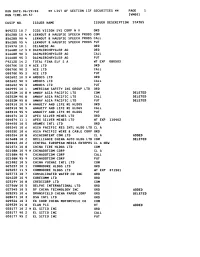

LIST of SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 Ivmool

RUN DATE:06/29/00 ** LIST OF SECTION 13F SECURITIES ** PAGE 1 RUN TIME:09:57 IVMOOl CUSIP NO. ISSUER NAME ISSUER DESCRIPTION STATUS B49233 10 7 ICOS VISION SYS CORP N V ORD B5628B 10 4 * LERNOUT & HAUSPIE SPEECH PRODS COM B5628B 90 4 LERNOUT & HAUSPIE SPEECH PRODS CALL B5628B 95 4 LERNOUT 8 HAUSPIE SPEECH PRODS PUT D1497A 10 1 CELANESE AG ORD D1668R 12 3 * DAIMLERCHRYSLER AG ORD D1668R 90 3 DAIMLERCHRYSLER AG CALL D1668R 95 3 DAIMLERCHRYSLER AG PUT F9212D 14 2 TOTAL FINA ELF S A WT EXP 080503 G0070K 10 3 * ACE LTD ORD G0070K 90 3 ACE LTD CALL G0070K 95 3 ACE LTD PUT GO2602 10 3 * AMDOCS LTD ORD GO2602 90 3 AMDOCS LTD CALL GO2602 95 3 AMDOCS LTD PUT GO2995 10 1 AMERICAN SAFETY INS GROUP LTD ORD G0352M 10 8 * AMWAY ASIA PACIFIC LTD COM DELETED G0352M 90 8 AMWAY ASIA PACIFIC LTD CALL DELETED G0352M 95 8 AMWAY ASIA PACIFIC LTD PUT DELETED GO3910 10 9 * ANNUITY AND LIFE RE HLDGS ORD GO3910 90 9 ANNUITY AND LIFE RE HLDGS CALL GO3910 95 9 ANNUITY AND LIFE RE HLDGS PUT GO4074 10 3 APEX SILVER MINES LTD ORD GO4074 11 1 APEX SILVER MINES LTD WT EXP 110402 GO4450 10 5 ARAMEX INTL LTD ORD GO5345 10 6 ASIA PACIFIC RES INTL HLDG LTD CL A G0535E 10 6 ASIA PACIFIC WIRE & CABLE CORP ORD GO5354 10 8 ASIACONTENT COM LTD CL A ADDED G1368B 10 2 BRILLIANCE CHINA AUTO HLDG LTD COM DELETED 620045 20 2 CENTRAL EUROPEAN MEDIA ENTRPRS CL A NEW G2107X 10 8 CHINA TIRE HLDGS LTD COM G2108N 10 9 * CHINADOTCOM CORP CL A G2108N 90 9 CHINADOTCOM CORP CALL G2lO8N 95 9 CHINADOTCOM CORP PUT 621082 10 5 CHINA YUCHAI INTL LTD COM 623257 10 1 COMMODORE HLDGS LTD ORD 623257 11 -

ZILLOW GROUP, INC. (Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A (Rule 14a-101) INFORMATION REQUIRED IN PROXY STATEMENT SCHEDULE 14A INFORMATION Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant ☒ Filed by a Party other than the Registrant ☐ Check the appropriate box: ☐ Preliminary Proxy Statement ☐ Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) ☒ Definitive Proxy Statement ☐ Definitive Additional Materials ☐ Soliciting Material under § 240.14a-12 ZILLOW GROUP, INC. (Name of Registrant as Specified in its Charter) N/A (Name of Person(s) Filing Proxy Statement, if Other Than the Registrant) Payment of Filing Fee (Check the appropriate box): ☒ No fee required. ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: ☐ Fee paid previously with preliminary materials. ☐ Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. -

PDF: 300 Pages, 5.2 MB

The Bay Area Council Economic Institute wishes to thank the sponsors of this report, whose support was critical to its production: The Economic Institute also wishes to acknowledge the valuable project support provided in India by: The Bay Area Council Economic Institute wishes to thank the sponsors of this report, whose support was critical to its production: The Economic Institute also wishes to acknowledge the valuable project support provided in India by: Global Reach Emerging Ties Between the San Francisco Bay Area and India A Bay Area Council Economic Institute Report by R. Sean Randolph President & CEO Bay Area Council Economic Institute and Niels Erich Global Business/Transportation Consulting November 2009 Bay Area Council Economic Institute 201 California Street, Suite 1450 San Francisco, CA 94111 (415) 981-7117 (415) 981-6408 Fax [email protected] www.bayareaeconomy.org Rangoli Designs Note The geometric drawings used in the pages of this report, as decorations at the beginnings of paragraphs and repeated in side panels, are grayscale examples of rangoli, an Indian folk art. Traditional rangoli designs are often created on the ground in front of the entrances to homes, using finely ground powders in vivid colors. This ancient art form is believed to have originated from the Indian state of Maharashtra, and it is known by different names, such as kolam or aripana, in other states. Rangoli de- signs are considered to be symbols of good luck and welcome, and are created, usually by women, for special occasions such as festivals (espe- cially Diwali), marriages, and birth ceremonies. Cover Note The cover photo collage depicts the view through a “doorway” defined by the section of a carved doorframe from a Hindu temple that appears on the left. -

1 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

1 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 13F FORM 13F COVER PAGE Report for the Calendar Year or Quarter Ended: September 30, 2000 Check here if Amendment [ ]; Amendment Number: This Amendment (Check only one.): [ ] is a restatement. [ ] adds new holdings entries Institutional Investment Manager Filing this Report: Name: AMERICAN INTERNATIONAL GROUP, INC. Address: 70 Pine Street New York, New York 10270 Form 13F File Number: 28-219 The Institutional Investment Manager filing this report and the person by whom it is signed represent that the person signing the report is authorized to submit it, that all information contained herein is true, correct and complete, and that it is understood that all required items, statements, schedules, lists, and tables, are considered integral parts of this form. Person Signing this Report on Behalf of Reporting Manager: Name: Edward E. Matthews Title: Vice Chairman -- Investments and Financial Services Phone: (212) 770-7000 Signature, Place, and Date of Signing: /s/ Edward E. Matthews New York, New York November 14, 2000 - ------------------------------- ------------------------ ----------------- (Signature) (City, State) (Date) Report Type (Check only one.): [X] 13F HOLDINGS REPORT. (Check if all holdings of this reporting manager are reported in this report.) [ ] 13F NOTICE. (Check if no holdings reported are in this report, and all holdings are reported in this report and a portion are reported by other reporting manager(s).) [ ] 13F COMBINATION REPORT. (Check -

4/Final Dst I/Iccp

Unclassified DSTI/ICCP(2005)4/FINAL Organisation de Coopération et de Développement Economiques Organisation for Economic Co-operation and Development ___________________________________________________________________________________________ English - Or. English DIRECTORATE FOR SCIENCE, TECHNOLOGY AND INDUSTRY COMMITTEE FOR INFORMATION, COMPUTER AND COMMUNICATIONS POLICY Unclassified DSTI/ICCP(2005)4/FINAL OECD INPUT TO THE UNITED NATIONS WORKING GROUP ON INTERNET GOVERNANCE (WGIG) English - Or. English Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format DSTI/ICCP(2005)4/FINAL TABLE OF CONTENTS MAIN POINTS............................................................................................................................................ 4 ICT/INTERNET-INDUCED BENEFITS .................................................................................................... 8 Leveraging ICT/the Internet in OECD countries ...................................................................................... 8 Growth in Internet usage in OECD countries........................................................................................ 8 Productivity impact and contribution to economic growth.................................................................. 10 Benefits of ICT/the Internet in non-OECD countries..............................................................................11 ICTs and development goals.............................................................................................................. -

The End of Bankruptcy

University of Chicago Law School Chicago Unbound Coase-Sandor Working Paper Series in Law and Coase-Sandor Institute for Law and Economics Economics 2002 The ndE of Bankruptcy Robert K. Rasmussen Douglas G. Baird Follow this and additional works at: https://chicagounbound.uchicago.edu/law_and_economics Part of the Law Commons Recommended Citation Robert K. Rasmussen & Douglas G. Baird, "The ndE of Bankruptcy" (John M. Olin Program in Law and Economics Working Paper No. 173, 2002). This Working Paper is brought to you for free and open access by the Coase-Sandor Institute for Law and Economics at Chicago Unbound. It has been accepted for inclusion in Coase-Sandor Working Paper Series in Law and Economics by an authorized administrator of Chicago Unbound. For more information, please contact [email protected]. CHICAGO JOHN M. OLIN LAW & ECONOMICS WORKING PAPER NO. 173 (2D SERIES) The End of Bankruptcy Douglas G. Baird and Robert K. Rasmussen THE LAW SCHOOL THE UNIVERSITY OF CHICAGO This paper can be downloaded without charge at: The Chicago Working Paper Series Index: http://www.law.uchicago.edu/Lawecon/index.html The Social Science Research Network Electronic Paper Collection: http://ssrn.com/abstract_id=359241 The End of Bankruptcy Douglas G. Baird* & Robert K. Rasmussen** ABSTRACT The law of corporate reorganizations is conventionally justified as a way to preserve a firm’s going-concern value: Specialized assets in a particular firm are worth more together in that firm than anywhere else. This paper shows that this notion is mistaken. Its flaw is that it lacks a well- developed understanding of the nature of a firm. -

Worldcom's Bankruptcy Crisis

Center for Ethical Organizational Cultures Auburn University http://harbert.auburn.edu WorldCom’s Bankruptcy Crisis INTRODUCTION The story of WorldCom began in 1983 when businessmen Murray Waldron and William Rector sketched out a plan to create a long-distance telephone service provider on a napkin in a coffee shop in Hattiesburg, Miss. Their new company, Long Distance Discount Service (LDDS), began operating as a long distance reseller in 1984. Early investor Bernard Ebbers was named CEO the following year. Through acquisitions and mergers, LDDS grew quickly over the next 15 years. The company changed its name to WorldCom, achieved a worldwide presence, acquired telecommunications giant MCI, and eventually expanded beyond long distance service to offer the whole range of telecommunications services. WorldCom became the second-largest long-distance telephone company in America, and the firm seemed poised to become one of the largest telecommunications corporations in the world. Instead, it became the largest bankruptcy filing in U.S. history at the time and another name on a long list of those disgraced by the accounting scandals of the early 21st century. ACCOUNTING FRAUD AND ITS CONSEQUENCES Unfortunately for thousands of employees and shareholders, WorldCom used questionable accounting practices and improperly recorded $3.8 billion in capital expenditures, which boosted cash flows and profit over all four quarters in 2001 as well as the first quarter of 2002. This disguised the firm’s actual net losses for the five quarters because capital expenditures can be deducted over a longer period of time, whereas expenses must be subtracted from revenue immediately. WorldCom also spread out expenses by reducing the book value of assets from acquired companies and simultaneously increasing the value of goodwill.