Fisher Communications, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

4. Spanish News and Talk Show Bookings 5

since 1996 2012 Map of Idaho Media Outlet Pickup* *A full list of outlets that picked up NRNS can be found in section 8. “In the current news landscape, PNS plays a critical role in bringing public- interest stories into communities around the country. We appreciate working with this growing network.” - Roye Anastasio-Bourke, Senior Communications Manager, Annie E. Casey Foundation 1. About Us 2. Our Reach Market Share Graph Issue Graph 3. Why Solution-Focused Journalism Matters (More Than Ever) 4. Spanish News and Talk Show Bookings 5. Member Benefits 6. List of Issues 7. PR Needs (SBS) 8. Media Outlet List Northern Rockies News Service • northernrockiesnewsservice.org page 2 1. About Us What is the Northern Rockies News Service? Launched in 1996, the Northern Rockies News Service is part of a network of independent public interest state-based news services pioneered by Public News Service. Our mission is an informed and engaged citizenry making educated decisions in service to democracy; and our role is to inform, inspire, excite and sometimes reassure people in a constantly changing environment through reporting spans political, geographic and technical divides. Especially valuable in this turbulent climate for journalism, currently 115 news outlets in Idaho and neighboring markets regularly pick up and redistribute our stories. Last year, an average of 44 media outlets used each Northern Rockies News Service story. These include outlets like the Ag Weekly, Associated Press ID Bureau, CBS ID Affiliates, DCBureau.org/Public Education Center, KIDK-TV CBS Idaho Falls, Sirius Satellite Radio, KEZJ-FM Clear Channel News Talk Twin Falls KFXD-AM Clear Channel News talk Boise. -

Shiloh Road Corridor Finding of No Significant Impact STPU 1031(2) CN 4666 May 2007

Finding of No Significant Impact Shiloh Road Corridor May 2007 STPU 1031(2) Control Number 4666 Shiloh Road Corridor Finding of No Significant Impact STPU 1031(2) CN 4666 May 2007 Table of Contents 1.0 Coordination Process.................................................................................................... 1 1.1 Press Release and Advertising....................................................................................... 1 1.2 Availability of EA.......................................................................................................... 1 1.3 Public Hearing and Comments ...................................................................................... 2 1.4 Other Federal Requirements ......................................................................................... 8 1.5 Availability of FONSI .................................................................................................... 8 2.0 Clarifications to the EA ................................................................................................. 8 2.1 Summary .................................................................................................................... 8 2.2 Purpose and Need ......................................................................................................11 2.3 Alternatives................................................................................................................12 2.4 Impacts .....................................................................................................................12 -

Derek Decker, Senior Offensive

Derek Decker, senior offensive gua Other area attractions include “A Carousel for Missoula” (one of the first fully hand-carved carousels to be built in America since the Great Depression), Garnet Ghost Town, the National Bison Range, the Ninemile Remount Depot and Ranger Station, the Rocky Mountain Elk Foundation Wildlife Visitor Center, and the Smokejumper Visitor Center. Missoula Parks and Recreation and the YMCA provide a variety of recreational opportunities in basketball, soccer, softball, tennis, volleyball, and ice skating. Missoula also serves as a center for education, health care, retail, and the arts. The University of Montana provides educa tional opportunities for more than 13,000 college students. Com munity Medical Center and St. Patrick Hospital, along with many clinics, make Missoula one of the state’s premier health care com munities. The Missoula community supports the arts in all its forms: the Summertime in Missoula, the Downtown Association’s Out to Lunch ater productions, dance, art, and music. The Missoula Children’s weekly series. Theater, founded in 1970, moved into a renovated building near Birthplace and hometown of author Norman McLean, who wrote campus and produces plays and musicals by national and local A River Runs Through It, Missoula is also known as the “Garden playwrights for both adults and children. The theater also has an City” for its dense trees and lush green landscape. Missoula is International Tour Project, taking theatrical productions to audi nestled in the heart of the Northern Rockies in western Montana. ences outside the Missoula area. The Garden City Ballet and A community of approximately 66,000 residents, Missoula lies in a Missoula Symphony, which is in its 50th season, bring performances mountain forest setting where five valleys converge. -

Issue 736 with So Much Happening at a Breakneck Pace the Last Several Weeks, It Would Be Easy to Overlook the State of the Format in the Month of November

W E E K L Y PPM: A November Not To Remember December 21, 2020, Issue 736 With so much happening at a breakneck pace the last several weeks, it would be easy to overlook the state of the format in the month of November. In fact, it might be for the best if you did. Even with a record poor showing overall, however, Country also had its share of notably strong performances on the station level. The November survey started Oct. 8 and concluded the day after Election Day. For that period, aggregate Country shares in PPM markets stood at its lowest total (excluding Holiday books) since the start of PPM measurement, with four stations setting new low water marks. And for the first time in the PPM era, the format experienced a non-Holiday month without a single market being led by a Country station. The apparent culprit: News-Talk. Just how big were News-Talk’s gains for the month? The aggregate 6+ share for all PPM subscribing News-Talk stations in September was 577.5. October rose to 623.0 and, by November, that number had jumped to 658.0 – a 14% increase over two Happy Holi-Glaze: Country Aircheck months. Conversely, the corresponding congratulates Capitol staffers on their 12th aggregate for Country trended 360.4 consecutive label of the year win. Pictured to 350.8 to 339.2 for a 5.8% decrease (clockwise) are Royce Risser, Donna over the same span. Country wasn’t Hughes, Annie Sandor, Bobby Young, alone: AC and Classic Hits were down Rod Phillips Megan O’Gara, Megan Youngblood, 2% each during the same span, and Top Ashley Knight, Chris Schuler, David 40 was off 3%. -

Delinquent Tax Report Penalties, Interest, and Costs Will Be Added to Delinquent Taxes

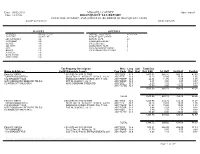

Date: 08/02/2018 MISSOULA COUNTY Oper: toneal Time: 14:17:05 DELINQUENT TAX REPORT PENALTIES, INTEREST, AND COSTS WILL BE ADDED TO DELINQUENT TAXES. AS OF 08/02/2018 REAL ESTATE RANGES OPTIONS TAX YEAR: (R) 2012 - 2017 DELINQ. AS OF DATE: 08/02/2018 TAX TYPE: (R) RE - RE REPORT SORT ORDER: A LEVY DISTRICT: (A) REPORT TYPE: D3 TOWNSHIP: (A) COMPLETE LEGAL?: Y RANGE: (A) INCLUDE P&I?: Y SECTION: (A) ASSESSMENT YEAR: C LOT: (A) INCL RANGES/OPTIONS?: Y BLOCK: (A) INCLUDE BANKRUPTCIES: N PARCEL#: (A) BANK CODE: (A) MISC CODE: (A) Tax Property Description Misc Levy Sub Total Due Name & Address Cert# (Complete Legal) Year Code Dist Dist (Incl P&I) 1st Half 2nd Half Pen/Int Parcel # 100003 1 04-2095-08-3-04-11-0000 2017 0000 32.3 1,415.52 666.32 666.31 82.89 TURNER DOLORES A Sn:08 Twn:12 N Rng:17 W Blk:5 Lot:11 2017 FFP 32.3 23.13 10.89 10.88 1.36 C/O BRADLEY FAAS DONOVAN CREEK ACRES, S08, T12 N, 2017 FMRP 32.3 24.84 11.70 11.69 1.45 6670 DONOVAN CREEK RD TRLR 6 R17 W, BLOCK 5, Lot 11 2017 ROSP 32.3 6.37 3.00 3.00 0.37 CLINTON, MT 59825-9724 6670 DONOVAN CREEK RD 2017 SOC 32.3 3.23 1.52 1.52 0.19 2017 TLFEE 32.3 75.00 0.00 75.00 0.00 1,548.09 693.43 768.40 86.26 TOTAL 1,548.09 693.43 768.40 86.26 Parcel # 100107 2 04-2095-08-3-04-12-0000 2017 0000 32.3 1,220.92 574.72 574.72 71.48 TURNER DOLORES A Sn:08 Twn:12 N Rng:17 W Blk:5 Lot:13 2017 FFP 32.3 23.13 10.89 10.88 1.36 C/O BRADLEY FAAS DONOVAN CREEK ACRES, S08, T12 N, 2017 FMRP 32.3 21.43 10.09 10.09 1.25 6670 DONOVAN CREEK RD TRLR 6 R17 W, BLOCK 5, Lot 13 2017 ROSP 32.3 5.48 2.59 2.58 0.31 -

PUBLIC NOTICE Washington, D.C

REPORT NO. PN-2-210511-01 | PUBLISH DATE: 05/11/2021 Federal Communications Commission 45 L Street NE PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 ACTIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. City, State Applicant or Licensee Status Date Status 0000143610 Minor FX W261AX 150026 100.1 PITTSBURGH, PA Radio Power Inc. 05/07/2021 Granted Modification From: To: 0000127963 Renewal of FM KIKF 22280 Main 104.9 CASCADE, MT STARADIO CORP. 05/07/2021 Granted License From: To: 0000127966 Renewal of FM KWGF 164134 Main 101.7 VAUGHN, MT STARADIO CORP. 05/07/2021 Granted License From: To: 0000140589 Assignment LPD K14SW- 187273 Main 14 JONESBORO, AR DTV AMERICA 05/07/2021 Granted of D CORPORATION Authorization From: DTV AMERICA CORPORATION To: Jonesboro TV, LLC 0000136294 Transfer of AM KLMX 31888 Main 1450.0 CLAYTON, NM JIMMY MCCOLLUM 05/07/2021 Dismissed Control From: MELBA MCCOLLUM To: MELBA MCCOLLUM Comment #1 Dismissed - Inadvertently accepted for filing. 0000127958 Renewal of AM KXGF 63878 Main 1400.0 GREAT FALLS, MT STARADIO CORP. 05/07/2021 Granted License From: To: Page 1 of 7 REPORT NO. PN-2-210511-01 | PUBLISH DATE: 05/11/2021 Federal Communications Commission 45 L Street NE PUBLIC NOTICE Washington, D.C. 20554 News media info. (202) 418-0500 ACTIONS File Number Purpose Service Call Sign Facility ID Station Type Channel/Freq. City, State Applicant or Licensee Status Date Status 0000144657 License To DCA KEFN- 9375 Main 20 ST. LOUIS, MO MOTV LLC 05/07/2021 Granted Cover CD From: To: 0000144568 License To LPD W17DU- 187451 17 DUBOIS, PA LANDOVER 2 LLC 05/07/2021 Granted Cover D From: To: 0000094418 Renewal of FM WTRJ- 47425 Main 91.7 ORANGE PARK, FL DELMARVA 05/07/2021 Granted License FM EDUCATIONAL Amendment ASSOCIATION From: To: Comment #1 Granted 5/7/2021 per letter ref 1800B3-DB. -

Cross-Platform Measurement Helps Local Stations Add Value to Broadcast and Digital

Case Study Cross-Platform Measurement Helps Local Stations Add Value to Broadcast and Digital Ecosystem The local game is changing. Daily deal sites like Groupon and LivingSocial.com in the U.S. have altered the way businesses reach out to consumers. For years, traditional local media – TV, radio and newspapers – has struggled with how to use their websites to complement their offerings and provide more to local businesses. Local TV stations, for example, have typically put video of reports or entire newscasts on their sites. As gateways to local news and events, websites for TV stations typically attract large numbers of visitors, yet it has been difficult to determine the effects and value of those visitors. The challenge has been leveraging “digital touchpoints,” quantifying their benefits and creating new models to attract more from local and national businesses who advertise and encourage those who otherwise might not advertise online at all. As new technology, such as location-based couponing, measurement capabilities, and integrated TV and Internet audience measurement, brings precision to local advertising, marketers are gaining the ability to better package local ad inventory to reach customers and amplify local TV audience value, combining TV and Online. In turn, the precision enables greater efficiency, meaning the opportunity to attract advertisers to spend more, locally. In other words, there’s a fortune to be made in your own backyard. Background Working with this valuable information, Fisher Communications Inc., an innovative local media company with TV, radio, Internet and mobile operations, found themselves positioned to provide their advertiser clients one-stop TV and digital local exposure. -

Broadcast Syndication Broadcast Syndication

Broadcast Syndication Broadcast Syndication SYNDICATION SYNDICATIONStations Clearances SYNDICATION182 stations / 78.444% DMA %US MARKET HouseHolds Stations Affiliates Channel Air Time 1 6.468 NEW YORK 6,701,760 WVVH Independent 50 SUN 2PM 1 NEW YORK WMBC Independent 18 SUN 2PM 1 NEW YORK WRNN Independent 48 SUN 2PM 2 4.917 LOS ANGELES 5,113,680 KXLA Independent 44 SUN 2PM 3 3.047 CHICAGO 3,142,880 WBBM CBS 2 3 CHICAGO WSPY Independent 32 SUN 2PM 4 2.611 PHILADELPHIA 2,715,440 WACP Independent 4 4 PHILADELPHIA WPSJ Independent 8 SUN 2PM 4 PHILADELPHIA WZBN Independent 25 SUN 2PM 5 2.243 DALLAS 2,332,720 KHPK Independent 28 SUN 2PM 5 DALLAS KTXD Independent 46 6 2.186 SAN FRANCISCO 7 2.076 BOSTON 2,159,040 WBIN Independent 35 7 BOSTON WHDN Independent 26 8 2.059 WASHINGTON DC 2,141,360 WJAL Independent 68 9 2.000 ATLANTA 2,080,000 WANN Independent 32 SUN 2PM 10 1.906 HOUSTON 1,953,120 KUVM Independent 34 SUN 2PM 10 HOUSTON KHLM Independent 43 SUN 2PM 10 HOUSTON KETX Independent 28 SUN 2PM 11 1.607 DETROIT 12 1.580 SEATTLE 1,681,680 KUSE Independent 46 SUN 2PM 12 SEATTLE KPST Independent 66 SUN 2PM 13 1.580 PHOENIX 1,643,200 KASW CW 49 SUN 5AM 13 PHOENIX KNJO Independent 15 SUN 2PM 13 PHOENIX KKAX Independent 36 SUN 2PM 13 PHOENIX KCFG Independent 32 SUN 2PM 14 1.560 TAMPA 1,622,400 WWSB ABC 24 15 1.502 MINNEAPOLIS 1,562,080 KOOL Independent 21 16 1.381 MIAMI 1,332,240 WHDT Independent 9 17 1.351 DENVER 1,405,040 KDEO Independent 23 SUN 2PM 17 DENVER KTED Independent 25 SUN 2PM 18 1.321 CLEVELAND 1,373,840 WBNX CW 30 18 CLEVELAND WMFD Independent 12 SUN 2PM 19 1.278 ORLANDO 1,329,120 WESH NBC 11 19 ORLANDO WHDO Independent 38 20 1.211 SACRAMENTO 1,259,440 KBTV Independent 8 SUN 2PM 21 1.094 ST. -

104494 FB MG Text 125-232.Id2

COUGAR RADIO-TV NETWORK THE COUGAR SPORTS RADIO NETWORK 2004 OUTLLOK Cougar football games are broadcast live on the radio throughout the Pacific THE COUGAR SPORTS NETWORK Northwest via The Cougar Sports Radio Network. The 27-station network - one of (Subject to Change) the largest in the Pac-10 - reaches from British Columbia to Nevada and can be heard Location Station Frequency worldwide via the internet. Aberdeen KXRO 1320 AM The KXLY Broadcast Group produces The Cougar Sports Network, which also Bellingham KPUG 1170 AM features radio coverage of WSU men’s basketball, baseball, women’s basketball and Boise, Idaho KCID 1490 AM women’s volleyball, and 30-minute coaches show in the fall and winter seasons. Centralia KELA 1470 AM Cougar football broadcasts begin an hour before kick-off, carry through the game and conclude with post-game interviews with players and coaches and a live call-in Clarkston KCLK 1430 AM 2004 OUTLOOK talk show. Colfax KCLX 1450 AM KXLY, which began a five-year partnership with the Cougars in 2001, also publishes Colville KCVL 1240 AM Crimson & Gray Magazine, the official game-day publication of Cougar football and Everett KRKO 1380 AM WSU COACHES basketball. Grand Coulee KEYG 1490 AM Las Vegas, Nev. KLAV 1230 AM Longview KBAM 1270 AM Moscow, Idaho KZFN 106.1 FM Moscow, Idaho KRPL 1400 AM Moses Lake KBSN 1470 AM Mount Vernon KAPS 660 AM Olympia KGY 96.9 FM Omak KNCW 92.7 FM WSU COACHES Portland, Oregon KFXX 1080 AM Prosser/Sunnyside KZXR 1310 AM Robertson Walden Nameck Quincy KWNC 1370 AM PROFILES PLAYER Seattle KYCW 1090 AM THE BROADCAST TEAM Spokane KXLY 920 AM Bob Robertson Sr. -

Pensacola Newspapers

" .'- .. PENSACOLA NEWSPAPERS Pensacola News Journal Susan Catron One News Journal Plaza 4 days Pensacola, FL 32501 (904) 435-8621 UWF Voyager Editor 11,000 University Pkwy Monday for following week's Pensacola, FL 32514 Tuesday publication (904) 474-2191 PJC Corsair Editor 1000 College Blvd. Pensacola, FL 32504 (904) 484-1458 The Beacon Bill Phifer, Editor 301 W. Government St. Tuesday for Friday publication Pensacola, FL 32501 (904) 432-5313 Escambia Sun Press Denise Messer 3610 Barrancas Ave. Monday for Thursday publication Pensacola, FL 32507 (904 ) 4 56-3121 The Pensacola New Ameri can Editor 521 W. Cervantes St. Monday for Thursday publication Pensacola, FL 32501 (904) 432-8410 Pensacola Voice Les Hump h rey 213 E. Yonge St. Monday fo r Thu rsday publ ica tion Pensacola, FL 32503 (904) 434-6963 The Sentinel Duane Cook, Editor 1200 Gulf Breeze Pkwy Monday for Thu rsday publica tion Gulf Breeze, FL 32561 (904) 934-1200 The Islander Newspaper Elizabeth Waters, Editor P.O. Box 292 Tuesday for Friday p u blication Gulf Breeze, FL 32562 ( 904) 934-3417 Santa Rosa Press Gazette Ray Murphy 262 Gulf Breeze Pkwy #8 Monday for Thursday publication Gulf Breeze, FL 32561 (904) 934-3300 · " PENSACOLA RADIO STATIONS C. QNTA.C.T. ..... &c ...... P.J;:.A.P.k.. ;r.: N~ WAVH 96 .1 FM Branch Office 3000 Langley Ave. Call (800) 634-2615 Pensacola, FL 32504 (904) 478-2143 WBLX AM-FM Pat P.O. Box 1967 3 days Mobile, AL 36633 (904) 434-4311 (Mobile) WBSR 1450 AM / WM EZ 9 4 . 1 FM Gene Phalzer P.O. -

Fisher Communications, Inc

UNITEDSTATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON D.C 20549-3010 DIVISION OF CORPORATION FINANCE December 19 2007 Andrew Bor Perkins Coie 1201 Third Avenue Suite 4800 Seattle WA 98101-3099 Re Fisher Communications Inc Incoming letter dated November 29 2007 Dear Mr Bor This is in response to your letters dated November 29 2007 and December 11 2007 concerning the shareholder proposal submitted to Fisher Communications by GAMCO Asset Management Inc We also have received letter from the proponent dated December 2007 Our response is attached to the enclosed photocopy of your correspondence By doing this we avoid having to recite or summarize the facts set forth in the correspondence Copies of all of the correspondence also will be provided to the proponent In connection with this matter your attention is directed to the enclosure which sets forth brief discussion of the Divisions informal procedures regarding shareholder proposals Sincerely Jonathan Ingram Deputy Chief Counsel Enclosures cc Peter Goldstein Director of Regulatory Affairs GAMCO Asset Management Inc One Corporate Center Rye NY 10580-1435-1422 December 19 2007 Response of the Office of Chief Counsel Division of Corporation Finance Re Fisher Communications Inc Incoming letter dated November 29 2007 The proposal relates to acquisitions for view that Fisher Communications There appears to be some basis your may Fisher Communications received it exclude the proposal under rule 14a-8e2 because after the deadline for submitting proposals We note in particular your representations -

Download the SCEC Final Report (Pdf Format)

Seattle Commission on Electronic Communication Steve Clifford Michele Lucien Commission Chair Fisher Communications/KOMO-TV Former CEO, KING Broadcasting Betty Jane Narver Rich Lappenbusch University of Washington Commission Vice Chair Microsoft Amy Philipson UWTV David Brewster Town Hall Vivian Phillips Family Business Margaret Gordon University of Washington Josh Schroeter Founder, Blockbuy.com Bill Kaczaraba NorthWest Cable News Ken Vincent KUOW Radio Norm Langill One Reel Jean Walkinshaw KCTS-TV Commission Staff City Staff Anne Fennessy Rona Zevin Cocker Fennessy City of Seattle Kevin Evanto JoanE O’Brien Cocker Fennessy City of Seattle Table of Contents Final Report Letter from the Commission Chair ......................................................................... 2 Executive Summary .................................................................................................. 3 Diagram of TV/Democracy Portal.......................................................................... 4 Commission Charge & Process ............................................................................... 6 Current Environment................................................................................................. 8 Recommended Goal, Mission Statement & Service Statement...................... 13 Commission Recommendations ............................................................................ 14 Budget & Financing ................................................................................................ 24 Recommended