Inter-Office Memo Reno-Tahoe Airport Authority

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hull Loss Accidents

Hull Loss Accidents Western Built Commercial Jets (>60,000 lbs) 1960 thru 2005 10 . 0 0 8.00 5.64 6.00 es per million departures 4.00 2.16 1.47 2.00 1.29 0.89 Hull Loss Rate in loss 0.00 60's 70's 80's 90's 2000's Source: Boeing, AvSoft Figure 1 The Fleet - 2006 Type Western Built Eastern Built Total Turbojets 17,609 1,839 19,448 Turboprops 4,774 1,710 6,484 Business Jets 12,724 Figure 2 Major Accidents Business Jets 1 January to 31 December 2006 Date Operator Aircraft Location Phase Fatal 2 January Avcom Hawker 700 Kharkov, Ukraine Approach 3 24 January Goship Air Citation V Carlsbad, CA, USA Landing 4 15 February Jet 2000 Falcon 20 Kiel, Germany Landing 0 16 February Lech Air Citation I Busckin, Iraq Descent 6 2 June International Jet Charter Lear 35 Groton, CT, USA Approach 2 26 June Great Ideas Corp Hawker F3 Barcelona, Venezuela Landing 0 5 July Vigojet Sabreliner Mexico City, Mexico Landing 0 19 July Tomco II Citation Encore Cresco, IA, USA Landing 2 28 August Netjets Hawker 800 Carson City, NV, USA Descent 0 30 December Fact Air Sabreliner Culiacan, Mexico Approach 2 Source: Ascend Figure 3 Major Accidents Commercial Turboprops (> 14 seats) 1 January to 31 December 2006 Date Operator Aircraft Location Phase Fatal 2 January Ruenzori Airways Antonov 26 Fataki, DR Congo Climb 0 24 January Aerolift Antonov 12 Mbuji Mayi, DR Congo Landing 0 5 February Air Cargo Carriers Shorts 360 Watertown, WI, USA Enroute 3 8 February Tri Coastal Airlines Metro II Paris, TN, USA Enroute 1 11 March Air Deccan ATR 72 Bangalore, India Landing 0 18 March -

INTERNATIONAL CONFERENCE on AIR LAW (Montréal, 20 April to 2

DCCD Doc No. 28 28/4/09 (English only) INTERNATIONAL CONFERENCE ON AIR LAW (Montréal, 20 April to 2 May 2009) CONVENTION ON COMPENSATION FOR DAMAGE CAUSED BY AIRCRAFT TO THIRD PARTIES AND CONVENTION ON COMPENSATION FOR DAMAGE TO THIRD PARTIES, RESULTING FROM ACTS OF UNLAWFUL INTERFERENCE INVOLVING AIRCRAFT (Presented by the Air Crash Victims Families Group) 1. INTRODUCTION – SUPPLEMENTAL AND OTHER COMPENSATIONS 1.1 The apocalyptic terrorist attack by the means of four hi-jacked planes committed against the World Trade Center in New York, NY , the Pentagon in Arlington, VA and the aborted flight ending in a crash in the rural area in Shankville, PA ON September 11th, 2001 is the only real time example that triggered this proposed Convention on Compensation for Damage to Third Parties from Acts of Unlawful Interference Involving Aircraft. 1.2 It is therefore important to look towards the post incident resolution of this tragedy in order to adequately and pro actively complete ONE new General Risk Convention (including compensation for ALL catastrophic damages) for the twenty first century. 2. DISCUSSION 2.1 Immediately after September 11th, 2001 – the Government and Congress met with all affected and interested parties resulting in the “Air Transportation Safety and System Stabilization Act” (Public Law 107-42-Sept. 22,2001). 2.2 This Law provided the basis for Rules and Regulations for: a) Airline Stabilization; b) Aviation Insurance; c) Tax Provisions; d) Victims Compensation; and e) Air Transportation Safety. DCCD Doc No. 28 - 2 - 2.3 The Airline Stabilization Act created the legislative vehicle needed to reimburse the air transport industry for their losses of income as a result of the flight interruption due to the 911 attack. -

Florida's Geographic Advantage Aircraft Range

Florida Air Cargo System Plan - Task 4 Appendix G FLORIDA’S GEOGRAPHIC ADVANTAGE Airports with historically significant air cargo activity typically have geographic locational advantages which have made them successful in supporting the air cargo industry. Airports with air cargo hub activity typically are in a central location and may vary in scale from regional hubs to national and international hubs. In addition, airports with air cargo hub activity benefit from dense populations and manufacturing activity in the hub airport’s market area to bolster additional cargo tonnages. A few of the world’s largest cargo airports, however, function as intercontinental air cargo hubs but are located in relatively remote parts of the world away from dense populations. As discussed in a previous section, airports with air cargo activity may have a functional role as either gateways to international destinations, intercontinental national or regional hubs or as origin and destination cargo airports. In some instances the airport may function in more than one functional role. An airport’s location on the globe, as well as available customer base, are key factors air cargo carriers consider when choosing which airports to operate at. Attracting cargo carriers to airports is a difficult challenge fraught with competition from other airports, ensuring sufficient cargo demand and having adequate facilities and services. This section of the report discusses the following: • Aircraft range • Great circle route by aircraft • Polar routes by aircraft • Remote intercontinental air cargo hubs • International gateways • Potential Intercontinental Air Cargo Hub Scenarios AIRCRAFT RANGE Improvements in aircraft manufacturing and design have led to aircraft that can fly longer distances and still transport a significant amount of payload. -

Spatial Network Configurations of Cargo Airlines

Spatial network configurations of cargo airlines by Aaron B. Scholz No. 20 | APRIL 2011 WORKING PAPER SERIES IN ECONOMICS KIT – University of the State of Baden-Wuerttemberg and National Laboratory of the Helmholtz Association econpapers.wiwi.kit.edu Impressum Karlsruher Institut für Technologie (KIT) Fakultät für Wirtschaftswissenschaften Institut für Wirtschaftspolitik und Wirtschaftsforschung (IWW) Institut für Wirtschaftstheorie und Statistik (ETS) Schlossbezirk 12 76131 Karlsruhe KIT – Universität des Landes Baden-Württemberg und nationales Forschungszentrum in der Helmholtz-Gemeinschaft Working Paper Series in Economics No. 20, April 2011 ISSN 2190-9806 econpapers.wiwi.kit.edu Spatial network configurations of cargo airlines Author: Aaron B. Scholz Institute for Economic Policy Research (IWW) Karlsruhe Institute of Technology (KIT) Kaiserstr. 12, 76131 Karlsruhe (Germany) Tel.: (+49) 721 608 44226 Fax: (+49) 721 608 48923 Email: [email protected] Abstract The paper evaluates the spatial dimension of air cargo networks by means of concentration and centrality measures. Three groups of carriers are analyzed, namely combined carriers, their pure freighter operations and pure cargo airlines. Differences in their spatial network configuration are observed between the three groups. Combined carriers operate very centralized networks with high concentrations at a small number of airports. Hub-and-spoke schemes are their predominant network configuration. The freighter fleets of combined carriers have lower centrality and concentration scores but hub-and-spoke schemes are still the predominant network configuration. Pure cargo airlines operate the least concentrated and centralized networks. Round-trip configurations are wide spread among pure cargo airlines to cope with imbalances of demand. Keywords: Air cargo transport, network configuration, centrality, spatial network configuration. -

LOUISVILLE REGIONAL AIRPORT AUTHORITY AVIATION STATISTICS 2018 2017 % Change 2018 2017 % Change 2018 2017 % Change 2018 2017

LOUISVILLE REGIONAL AIRPORT AUTHORITY AVIATION STATISTICS January-18 CURRENT MONTH FISCAL YEAR TO DATE CALENDAR YEAR TO DATE TWELVE MONTHS TO DATE 2018 2017 % Change 2018 2017 % Change 2018 2017 % Change 2018 2017 % Change PASSENGERS: Scheduled: Enplaned 122,523 115,467 6.11% 1,027,554 964,226 6.57% 122,523 115,467 6.11% 1,742,424 1,667,900 4.47% Scheduled: Deplaned 122,210 117,852 3.70% 1,026,470 967,673 6.08% 122,210 117,852 3.70% 1,737,875 1,671,796 3.95% Total Scheduled Passengers 244,733 233,319 4.89% 2,054,024 1,931,899 6.32% 244,733 233,319 4.89% 3,480,299 3,339,696 4.21% Charters: Enplaned 248 303 -18.15% 1,615 1,651 -2.18% 248 303 -18.15% 2,664 2,117 25.84% Charters: Deplaned 65 153 -57.52% 1,476 1,512 -2.38% 65 153 -57.52% 2,648 1,977 33.94% Total Charter Passengers 313 456 -31.36% 3,091 3,163 -2.28% 313 456 -31.36% 5,312 4,094 29.75% Total Enplaned Passengers 122,771 115,770 6.05% 1,029,169 965,877 6.55% 122,771 115,770 6.05% 1,745,088 1,670,017 4.50% Total Deplaned Passengers 122,275 118,005 3.62% 1,027,946 969,185 6.06% 122,275 118,005 3.62% 1,740,523 1,673,773 3.99% Total All Passengers 245,046 233,775 4.82% 2,057,115 1,935,062 6.31% 245,046 233,775 4.82% 3,485,611 3,343,790 4.24% *CARGO (lbs): Mail: Enplaned 13,718,726 10,214,569 34.31% 85,618,903 63,893,113 34.00% 13,718,726 10,214,569 34.31% 150,411,779 116,460,334 29.15% Mail: Deplaned 10,976,199 8,299,734 32.25% 68,864,243 53,286,131 29.23% 10,976,199 8,299,734 32.25% 122,206,381 96,930,563 26.08% Total Mail 24,694,925 18,514,303 33.38% 154,483,146 117,179,244 31.83% -

FAA DOT/TSC CY1997 ACAIS Database Report Date : 12/18/97 Page : 1

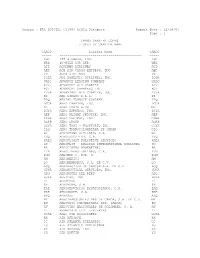

Source : FAA DOT/TSC CY1997 ACAIS Database Report Date : 12/18/97 Page : 1 CARGO CARRIER CODES LISTED BY CARRIER NAME CARCD Carrier Name CARCD ----- ------------------------------------------ ----- KHC 135 AIRWAYS, INC. KHC WRB 40-MILE AIR LTD. WRB ACD ACADEMY AIRLINES ACD AER ACE AIR CARGO EXPRESS, INC. AER VX ACES AIRLINES VX IQDA ADI DOMESTIC AIRLINES, INC. IQDA UALC ADVANCE LEASING COMPANY UALC ADV ADVANCED AIR CHARTER ADV ACI ADVANCED CHARTERS INT ACI YDVA ADVANTAGE AIR CHARTER, INC. YDVA EI AER LINGUS P.L.C. EI TPQ AERIAL TRANSIT COMPANY TPQ DGCA AERO CHARTER, INC. DGCA ML AERO COSTA RICA ML DJYA AERO EXPRESS, INC. DJYA AEF AERO FLIGHT SERVICE, INC. AEF GSHA AERO FREIGHT, INC. GSHA AGRP AERO GROUP AGRP CGYA AERO TAXI - ROCKFORD, INC. CGYA CLQ AERO TRANSCOLOMBIANA DE CARGA CLQ G3 AEROCHAGO AIRLINES, S.A. G3 EVQ AEROEJECUTIVO, C.A. EVQ XAES AEROFLIGHT EXECUTIVE SERVICES XAES SU AEROFLOT - RUSSIAN INTERNATIONAL AIRLINES SU AR AEROLINEAS ARGENTINAS AR LTN AEROLINEAS LATINAS, C.A. LTN ROM AEROMAR C. POR. A. ROM AM AEROMEXICO AM QO AEROMEXPRESS, S.A. DE C.V. QO ACQ AERONAUTICA DE CANCUN S.A. DE C.V. ACQ HUKA AERONAUTICAL SERVICES, INC. HUKA ADQ AERONAVES DEL PERU ADQ HJKA AEROPAK, INC. HJKA PL AEROPERU PL 6P AEROPUMA, S.A. 6P EAE AEROSERVICIOS ECUATORIANOS, C.A. EAE KRE AEROSUCRE, S.A. KRE ASQ AEROSUR ASQ MY AEROTRANSPORTES MAS DE CARGA, S.A. DE C.V. MY ZU AEROVAIS COLOMBIANAS LTD. (ARCA) ZU AV AEROVIAS NACIONALES DE COLOMBIA, S. A. AV ZL AFFRETAIR LTD. (PRIVATE) ZL UCAL AGRO AIR ASSOCIATES UCAL RK AIR AFRIQUE RK CC AIR ATLANTA ICELANDIC CC LU AIR ATLANTIC DOMINICANA LU AX AIR AURORA, INC. -

The Trans-Texas Corridor and the Texas Airport System: Opportunities and Challenges (FHWA/TX-06/0-4644-1)

Technical Report Documentation Page 1. Report No. 2. Government 3. Recipient’s Catalog No. FHWA/TX-06/0-4644-1 Accession No. 4. Title and Subtitle 5. Report Date The Trans-Texas Corridor and the Texas Airport System: October 2004; Revised May 2006 Opportunities and Challenges 6. Performing Organization Code 7. Author(s) 8. Performing Organization Report No. Kelsey A. Thompson, Michael S. Bomba, C. Michael Walton, 0-4644-1 Jordan E. Botticello 9. Performing Organization Name and Address 10. Work Unit No. (TRAIS) Center for Transportation Research 11. Contract or Grant No. The University of Texas at Austin 0-4644 3208 Red River, Suite 200 Austin, TX 78705-2650 12. Sponsoring Agency Name and Address 13. Type of Report and Period Covered Texas Department of Transportation Technical Report Research and Technology Implementation Office August 2003–August 2004 P.O. Box 5080 Austin, TX 78763-5080 14. Sponsoring Agency Code 15. Supplementary Notes Project performed in cooperation with the Texas Department of Transportation and the Federal Highway Administration. Project Title: Evaluation and Integration of Texas Airports into the Trans-Texas Corridor 16. Abstract The proposed Trans-Texas Corridor (TTC) will allow for faster and safer movement of people and goods throughout Texas, relieve congestion on existing roadways, divert hazardous materials away from urban areas, and stimulate economic growth and development along its path. However, to become fully integrated with the Texas transportation network, the TTC must also consider connections with the state’s extensive airport system. While the TTC could produce significant opportunities for commercial services and general aviation airports, many of its planners and engineers are not familiar with the special land-use and connectivity needs of airports. -

The World Bank Group

ANNEX A: ADDITIONAL TABLES Table A-1. Top ten air cargo carriers (million FTK) 2006 2005 1 FedEx 15,145 14,408 5.1% 2 UPS 9,341 9,075 2.9% 3 Korean Air 8,764 8,072 8.6% 4 Lufthansa 8,091 7,680 5.4% 5 Singapore 7,991 7,603 5.1% 6 Cathay Pacific 6,914 6,458 7.1% 7 China Airlines 6,099 6,037 1.0% 8 Air France-KLM 5,868 5,532 6.1% 9 Cargolux 5,237 5,149 1.7% 10 Eva Air 5,160 5,285 -2.4% Source: Air Cargo World Table A-2. Ranking of US cargo carriers Rank Carrier 2005 1 FedEx 10,028 2 Atlas/Polar 5.890 3 UPS 5,776 4 Northwest 2,257 5 American 2,216 6 United 2,020 7 Kalitta 1,562 8 Delta 1,341 9 Continental 941 10 Evergreen 829 11 Gemini 826 12 World 680 13 ABX 618 14 Tradewinds 489 15 US Airways 344 16 Omni 344 Source : Air Cargo Worldwide 63 64 AIR FREIGHT: A MARKET STUDY WITH IMPLICATIONS FOR LANDLOCKED COUNTRIES Table A-3. Ranking of airfreight carriers, 2005 Cat Company Country Millions % Change FTKs 2005 -2004 1 I Federal Express United States 14,408 -1.2 2 I United Parcel Service United States 9,075 23.4 3 C Korean Air South Korea 8,072 -2.3 4 C Lufthansa Germany 7,680 -4.5 5 C Singapore Singapore 7,603 6.4 6 C Cathay Pacific Hong Kong 6,458 9.9 7 C China Airlines Taiwan 6,037 7.0 8 F Atlas Air United States 6,002 8.4 9 C Air France France 5,532 2.7 10 C EVA Air Taiwan 5,285 -3.5 11 F Cargolux Luxembourg 5,149 10.3 12 C JAL Japan 4,817 -2.2 13 C British United Kingdom 4,767 -0.2 14 C KLM Netherlands 4,646 2.4 15 C Emirates UAE 4,192 14.5 16 C Northwest United States 3,210 4.6 17 C Martinair Netherlands 3,026 -3.5 18 C American United -

Aviation Job Fair Spring 2019 Fox Valley Technical College

Aviation Job Fair Spring 2019 Fox Valley Technical College ORGANIZATION NAME COMPANY PROFILE POSITIONS RECRUITING Air Cargo Carriers, LLC In business since 1986. Cargo 135 airline with numerous location A&P Technicians 4940 S Howell Ave. throughout the US and Puerto Rico. Fleet of 26 Turboprop aircraft. Milwaukee, WI 53207 Terri Peterson [email protected] (414) 482-1711 Air Wisconsin Airlines In the Air Airman trainees, First Officers, A&P 8770 West Bryn Mawr Ave Operating as a regional airline in the United States since 1965, Air Technicians, Avionics, Inspectors Suite 705 Wisconsin Airlines performs flying services for United Airlines as United Chicago, IL 60631 Express throughout the Midwest and East Coast, operating CRJ-200 regional jets. With service to approximately 70 cities throughout North Fernando Mendoza America, we carry an estimated 6 million passengers a year and help [email protected] unite the world by bringing passengers from their hometowns large and (773) 706-8794 small to hubs that provide them with a gateway to countless travel destinations. Headquarters Air Wisconsin Airlines W6390 Challenger Drive Suite 203 Appleton, WI 54914 Safety At Air Wisconsin, the safety of our customers, crews and coworkers matter most. Every employee takes responsibility for promoting safety in all aspects of his/her work. Our safety record is exemplary and we continuously look for ways to enhance our safety programs. Smart Choices We take pride in striving to build a stable airline within an industry that’s traditionally filled with highs and lows. Rather than focusing on the fast dollar, we focus on our future. -

Air Cargo Market Analysis Central Florida Regional Freight Study

Air Cargo Market Analysis Central Florida Regional Freight Study technical report prepared for MetroPlan Orlando FDOT District 5, Lake-Sumter MPO, Space Coast TPO, and Volusia TPO prepared by Aviation Analytics Cambridge Systematics July 16, 2012 www.camsys.com Air Cargo Market Analysis Central Florida Regional Freight Study prepared for MetroPlan Orlando DOT District 5, Lake-Sumter MPO, Space Coast TPO and Volusia TPO prepared by Aviation Analytics with Cambridge Systematics date March 2013 Air Cargo Market Analysis Table of Contents 1.0 Introduction ............................................................................................................ 1 2.0 Air Cargo Profile .................................................................................................... 2 2.1 Air Cargo Airports......................................................................................... 2 2.2 Air Cargo Service Providers ......................................................................... 4 Integrated Express Carriers .......................................................................... 4 All-Cargo Carriers ......................................................................................... 5 Commercial Service Passenger Carriers ..................................................... 5 Freight Forwarders ........................................................................................ 6 2.3 Regional Air Cargo Facilities and Activity ................................................ 8 Air Cargo Facilities ....................................................................................... -

Final Report

Baltimore/Washington International Airport Air Cargo Assessment final report prepared for Maryland Department of Transportation prepared by Cambridge Systematics, Inc. with Economic Development Research Group November 2003 www.camsys.com final report Baltimore/Washington International Airport Air Cargo Assessment prepared for Maryland Department of Transportation prepared by Cambridge Systematics, Inc. 4445 Willard Avenue, Suite 300 Chevy Chase, Maryland 20815 November 2003 Baltimore/Washington International Airport Air Cargo Assessment Table of Contents About This Report ................................................................................................................. vii 1.0 Role of Air Cargo in the Nation’s Freight Movement System.............................. 1-1 1.1 Introduction ............................................................................................................ 1-1 1.2 Evolution of the Intermodal Freight Transportation System........................... 1-1 1.3 Modal Specialization and the Air Cargo Market............................................... 1-3 1.4 Changing Market Requirements.......................................................................... 1-9 1.5 Air Cargo Gateways .............................................................................................. 1-15 2.0 BWI Air Cargo Activity and Market Potential......................................................... 2-1 2.1 Introduction ........................................................................................................... -

Air Cargo Alliances: Walking on a Thin Line

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by DSpace at Open Universiteit Nederland Air cargo alliances: Walking on a Thin Line A study on the impact of air cargo alliances Open University of the Netherlands Faculty : Management Major : Master of Science in Management First supervisor : dr. C.J. Gelderman Second supervisor : dr. P.W. Th. Ghijsen N.S.C. van Vliet Student number: 85 01 98 029 May 2010 Air cargo alliances; walking on a thin line. 1 Content Summary 3 1 Introduction 5 1.1 Purpose of this study and research questions 5 1.2 Methodology 6 2 Literature study 7 2.1 The air cargo industry 7 2.2 Theoretical foundation of the creation of strategic alliances 8 2.3 Definition 9 2.4 Alliances within the air cargo industry 9 2.5 Reasons for the foundation of air passenger alliances 10 2.6 Conditions to successfully create an alliance 13 2.7 Types of alliances 14 2.8 Levels of cooperation 15 2.9 Expected benefits 16 2.10 Realized benefits 18 2.11 Drawbacks and risks 20 2.12 Tentative answers to the research questions 20 3 Methodology 23 4 Research findings 25 4.1 Air France – KLM Cargo 25 4.2 Lufthansa Cargo 28 4.3 Malaysia Airlines Cargo (MASkargo) 30 4.4 Cargolux 33 4.5 Key cargo figures 37 5 Conclusions, discussion and recommendations 39 5.1 Conclusions 39 5.2 Discussion 41 5.2.1 What are the reasons for airlines to join or create an 41 air cargo alliance? 5.2.2 How do these reasons differ from the foundations of 43 other alliances, especially compared to air passenger airlines? 5.2.3 How could these differences be explained and what 46 are the consequences? 5.2.4 What is the impact of air cargo alliances on carriers? 47 5.2.5 Limitations 51 5.3 Recommendations 51 Literature 53 Appendix A Interview guide 57 Appendix B List of respondents 60 Appendix C Other cooperation forms alliance members 61 Appendix D Additional information from case studies 64 Air cargo alliances; Walking on a Thin Line.