KMC MM Office Briefing 1Q2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos

LAGUNA LAKE DEVELOPMENT AUTHORITY National Ecology Center, East Avenue, Diliman, Quezon City Phone Nos. (02) 8 376-4039, (02) 8 376-4072, (02) 8 376-4044, (02) 8 332-2353, (02) 8 332-2341, (02) 8 376-5430 Locals 115, 116, 117 and look for Ms. Julie Ann G. Blanquisco or Ms. Marivic A. Dela Torre-Santos E-mail: [email protected] | [email protected] Website: http://llda.gov.ph List of APPROVED DISCHARGE PERMITS as of September 03, 2021 Establishment Address Permit No. Approve Date 11 FTC Enterprises, Inc. 236 P. Dela Cruz San Bartolome Quezon City MM DP-25b-2021-03532 August 18, 2021 189 Realty Corp. (CI Market) Qurino Highway Santa Monica, Novaliches Quezon City MM DP-25b-2021-03744 August 20, 2021 189 Realty Corporation - 2nd (CI Market/Commercial Complex) Quirino Highway, Sta. Monica Novaliches Quezon City MM DP-25b-2021-03743 August 20, 2021 21st Century Mouldings Corporation 18 F. Carlos St. cor. Howmart Road Apolonio Samson Quezon City MM DP-25b-2021-03541 August 23, 2021 24K Property Ventures, Inc. (20 Lansbergh Place Condominium) 170 T. Morato Ave. cor. Sct. Castor Sacred Heart Quezon City MM DP-25b-2021-02819 July 15, 2021 3J Foods Corp. Sta. Ana San Pablo City Laguna DP-16d-2021-03174 August 06, 2021 8 Gilmore Place Condominium 8 Gilmore Ave. cor. 1st St. Valencia New Manila Quezon City MM DP-25b-2021-03829 August 27, 2021 AC Technical Services, Inc. 5 RMT Ind`l. Complex Tunasan Muntinlupa City MM DP-23a-2021-01804 May 12, 2021 Ace Roller Manufacturing, Inc. -

ALI Bonds Due 2031 Preliminary Prospectus

N OFFER TO YET BECOME BECOME YET 31/F Tower One and Exchange Plaza, Ayala Triangle, Ayala Avenue, Makati City 1226 Telephone Number: (632) 7750-6974 PRELIMINARY PROSPECTUS Up to [₱2.75 Billion] principal amount of Fixed-Rate Bonds to be issued from a new shelf registration of up to ₱50.0 Billion Securities Program rendered effective on [●] (“Base Offer”) with an Oversubscription Option of up to [₱2.75 Billion] to be issued from the shelf registration rendered effective on April 22, 2019 (“Oversubscription Option”) Due 2031 PRIOR TO THE TIME THE REGISTRATION STATEMENT Issue Price: 100% of Face Value Interest Rate: [●]% p.a. Joint Lead Underwriters and Bookrunners The date of this Preliminary Prospectus is August 9, 2021. A REGISTRATION STATEMENT RELATING TO THE BASE OFFER HAS BEEN FILED WITH THE OFFERS TO BUY THE SAME BE ACCEPTED SECURITIES AND EXCHANGE COMMISSION ("SEC") BUT HAS NOT YET BEEN DECLARED EFFECTIVE. NO OFFER TO BUY THE SECURITIES CAN BE ACCEPTED AND NO PART OF THE MAY PURCHASE PRICE CAN BE ACCEPTED OR RECEIVED UNTIL THE REGISTRATION STATEMENT HAS BECOME EFFECTIVE, AND ANY SUCH OFFER MAY BE WITHDRAWN OR REVOKED, WITHOUT OBLIGATION OR COMMITMENT OF ANY KIND, AT ANY TIME PRIOR TO NOTICE OF ITS ACCEPTANCE GIVEN AFTER THE EFFECTIVE DATE. AN INDICATION OF INTEREST IN RESPONSE HERETO INVOLVES NO OBLIGATION OR COMMITMENT OF ANY KIND. THIS PRELIMINARY PROSPECTUS SHALL NOT CONSTITUTE AN OFFER TO SELL OR THE BE SOLD NOR SOLICITATION OF AN OFFER TO BUY. A REGISTRATION STATEMENT RELATING TO THE OVERSUBSCRIPTION OPTION WAS FILED WITH THE SEC AND WAS RENDERED EFFECTIVE COVERING ₱50.0 BILLION OF SECURITIES. -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 20 May 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS ............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: 20 May 2021 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application Filing No. Mark Applicant Nice class(es) Number Date 19 SUPER STAR FIVE 1 4/2019/00016539 September Chin Chin Uy Valencia [PH] 30 GRAINS CENTER 2019 23 AROMATIC 2 4/2019/00016652 September SUPERSTAR FIVE Chin Chin Uy Valencia [PH] 31 2019 GRAINS CENTER 3 October 3 4/2019/00017278 IDELITA Steven Lu Tan [PH] 21 2019 21 October 4 4/2019/00018348 KOPI ROTI Kopi Roti Inc., [PH] 43 2019 25 October BUGTAW A BOOK A Shana Marie Mobo Holmes 5 4/2019/00018678 25 2019 DAY [PH] 28 October 6 4/2019/00018781 M MIEVIC Lili Zhuang [PH] 3; 9; 11; 18 and35 2019 6 7 4/2019/00508675 December QQ BABY Shi, Jianchuan [CN] 3; 10; 24 and25 2019 11 8 4/2019/00508798 December METROTIRES Charlie Ong [PH] 12 2019 CENTRAL MINDANAO UNIVERSITY- 22 January Central Mindanao University 9 4/2020/00001076 COLLEGE OF 41 2020 [PH] BUSINESS AND MANAGEMENT 22 January 10 4/2020/00001079 MEDILINK Medilink Network, Inc. -

Land Use Planning in Metro Manila and the Urban Fringe: Implications on the Land and Real Estate Market Marife Magno-Ballesteros DISCUSSION PAPER SERIES NO

Philippine Institute for Development Studies Land Use Planning in Metro Manila and the Urban Fringe: Implications on the Land and Real Estate Market Marife Magno-Ballesteros DISCUSSION PAPER SERIES NO. 2000-20 The PIDS Discussion Paper Series constitutes studies that are preliminary and subject to further revisions. They are be- ing circulated in a limited number of cop- ies only for purposes of soliciting com- ments and suggestions for further refine- ments. The studies under the Series are unedited and unreviewed. The views and opinions expressed are those of the author(s) and do not neces- sarily reflect those of the Institute. Not for quotation without permission from the author(s) and the Institute. June 2000 For comments, suggestions or further inquiries please contact: The Research Information Staff, Philippine Institute for Development Studies 3rd Floor, NEDA sa Makati Building, 106 Amorsolo Street, Legaspi Village, Makati City, Philippines Tel Nos: 8924059 and 8935705; Fax No: 8939589; E-mail: [email protected] Or visit our website at http://www.pids.gov.ph TABLE of CONTENTS Page 1. Introduction 1 2. The Urban Landscape: Metro Manila and its 2 Peripheral Areas The Physical Environment 2 Pattern of Urban Settlement 4 Pattern of Land Ownership 9 3. The Institutional Environment: Urban Management and Land Use Planning 11 The Historical Precedents 11 Government Efforts Toward Comprehensive 14 Urban Planning The Development Control Process: 17 Centralization vs. Decentralization 4. Institutional Arrangements: 28 Procedural Short-cuts and Relational Contracting Sources of Transaction Costs in the Urban 28 Real Estate Market Grease/Speed Money 33 Procedural Short-cuts 36 5. -

Muntinlupa City Lake Rehabilitation and Wastewater Management

MUNTINLUPA CITY LAKE REHABILITATION & WASTEWATER MGT. PROGRAM MUNTINLUPA CITY The SOUTHERN GATEWAY to Metro Manila & CALABARZON “The New Growth Center & The Most Livable City South of Metro Manila” Hon. Aldrin L. San Pedro City Mayor PROFILE • Area: 46.7 square kms. • Nine barangays • Population: 480,000+ • Classified as a Highly Urbanized City • Residential/Commercial/Light to Medium Industry • No. of Households: 110,000+ • No. of Business Establishments: 9,000+ • Population concentrated at the eastern portion (lakeshore area) • No. of densely populated areas (depressed areas):184 • No. of subdivision/villages: 80 • Major growth area: 1) Ayala Alabang/Madrigal Area 2) Filinvest Corporate City Area WATER RESOURCE Laguna Lake: +90,000 HAS. (City of Muntinlupa = +5,900 HAS.) *AQUACULTURE/FISHERIES * NAVIGATION * DOMESTIC H2O SUPPLY - Ayala Alabang Village - 100 MLD (Maynilad): Operational - 200 MLD 2nd phase MUNTINLUPA CITY TRIBUTAIES VULNERABLE AREA TYPHOON ONDOY ONDOY/SANTI EXPERIENCE LAKE MANAGEMENT OFFICE KAUTUSANG PANLUNGSOD 95-51 Kautusang Panglungsod na nagtatatag ng Tanggapan para sa Lawa ng Laguna (Lake Management Office) By: Hon. Aldrin L. San Pedro • Management of lake waters of Muntinlupa City • Formulate & recommend to the mayor policies concerning Laguna Lake • Implementation of Anti-Illegal Fishing Laws & Ordinances • Maintenance of Peace & Order • Pollution Control & Response • Assist in Water Rescue Operation • Coordinate with LLDA/BFAR/PNP/Coast Guard/Brgys. • Coordinate & Assist Fishpen Optrs. & Fisherfolks Org. PROGRAMS/PROJECTS • Lake Ecosystem Rehabilitation and Protection – Bantay Lawa/Lake Guards – Quarterly Lake Seeding – Paliko Creek Constructed Wetland Project (up to FS stage) • River Rehabilitation Program – Sagip Ilog/Environmental Armies – Trash Interceptor System – Fencing/Declogging/De-silting Projects – Treeplanting • Shore Land Development – Shore Land Tree Planting/Wetland Area Restoration – Shore Land Rehabilitation and Development • Enforcement/Legislation – City Ordinances No. -

Ayala Land FY 2018 Financial and Operating Results.Pdf

SEC Reg. No. 152747 15 February 2019 Philippine Stock Exchange, Inc. 6th Floor, PSE Tower, 28th Street corner 5th Avenue Bonifacio Global City, Taguig City Attention: Ms. Janet A. Encarnacion Head, Disclosure Department Philippine Dealing and Exchange Corporation 37th Floor, Tower 1, The Enterprise Center 6766 Ayala Ave cor. Paseo de Roxas, Makati City Attention: Atty. Joseph B. Evangelista Head, Issuer Compliance and Disclosures Department Securities and Exchange Commission SEC Building, Mandaluyong City Attention: Hon. Vicente Graciano P. Felizmenio, Jr. Director, Market Regulation Department Dear Mesdames and Gentlemen, Please see the attached press release on the unaudited financial and operating results of Ayala Land, Inc. as of December 31, 2018. Thank you. AUGUSTO D. BENGZON Senior Vice-President CFO, Treasurer and Chief Compliance Officer NEWS RELEASE Ayala Land’s net income climbs 16% to P29.2B in 2018 Feb. 15, 2019 – Ayala Land, Inc. (ALI), the Philippine’s largest integrated property and sustainable estates developer, posted solid top-line and bottom-line growth in 2018. ALI’s consolidated revenues climbed 17% to P166.2 billion driven by sustained demand for residential products and the healthy performance of its leasing businesses. Property development revenues rose 18% to P113.4 billion owing to strong sales across its residential, office for sale and commercial lot segments. Meanwhile, leasing revenues grew 17% to P34.9 billion on the back of robust local consumption, the increasing demand in BPO offices and a thriving tourism sector. All in all, net income grew 16% to P29.2 billion. “As we celebrated our 30th year in 2018, we remained focused on developing more sustainable communities that enrich the lives of Filipinos. -

Current Bus Service Operating Characteristics Along EDSA, Metro Manila

TSSP 22 nd Annual Conference of the Transportation Science Society of the Philippines Iloilo City, Philippines, 12 Sept 2014 2014 Current Bus Service Operating Characteristics Along EDSA, Metro Manila Krister Ian Daniel Z. ROQUEL Alexis M. FILLONE, Ph.D. Research Specialist Associate Professor Civil Engineering Department Civil Engineering Department De La Salle University - Manila De La Salle University - Manila 2401 Taft Avenue, Manila, Philippines 2401 Taft Avenue, Manila, Philippines E-mail: [email protected] E-mail: [email protected] Abstract: The Epifanio Delos Santos Avenue (EDSA) has been the focal point of many transportation studies over the past decade, aiming towards the improvement of traffic conditions across Metro Manila. Countless researches have tested, suggested and reviewed proposed improvements on the traffic condition. This paper focuses on investigating the overall effects of the operational and administrative changes in the study area over the past couple of years, from the full system operation of the Mass Rail Transit (MRT) in the year 2000 to the present (2014), to the service operating characteristics of buses plying the EDSA route. It was found that there are no significant changes in the average travel and running speeds for buses running Southbound, while there is a noticeable improvement for those going Northbound. As for passenger-kilometers carried, only minor changes were found. The journey time composition percentages did not show significant changes over the two time frames as well. For the factors contributing to passenger-related time, the presence of air-conditioning and the direction of travel were found to contribute as well, aside from the number of embarking and/or disembarking passengers and number of standing passengers. -

Asia Enclaves Alabang

Asia Enclaves Alabang A low density cosmopolitan community featuring architectural style inspired by Japanese culture, designed to help you find your own personal space where you can live and breathe free. It offers condo units with sizes of 54, 58, and 76 SQM, a combination of 2 to 3 Bedroom units to cater the needs of your family. Discover the elegance and purity of a relaxed life at Asia Enclaves Alabang. VICINITY MAP ASiA Enclaves Alabang Km 19 West Service Road, Brgy. Cupang, Muntinlupa City (Beside Hillsborough Village) Everything you need close to home. RETAIL/BUSINESS CENTERS Alabang Town Center - 3.4km Festival Mall Alabang - 2.8km Northgate Plaza - 2.4km Santana Grove - 2.8km SM City BF - 3.2km SM Hypermarket East Service Rd - 2.4km Makro Sucat East Service Rd. - 2.7km SCHOOLS De La Salle Santiago Zobel - 6.3km Informatics International - 2.5km Paref Ridgefield - 1km Paref Southridge School - 1.1km Paref Woodrose - 8.3km San Beda Alabang - 2.6km St. Bernadette College - 2km MAJOR HOSPITAL Asian Hospital & Medical Center - 2.7km CHURCHES Sacred Heart of Jesus Chapel - 0.65km St. Jerome Emiliani Church - 3.4km Makati CBD and BGC – 15.2km PROJECT FEATURES • Total lot area: 1.05 hectares • Low density living with up to 70% open space • 5 mid-rise buildings (hallway-type series) • 588 residential units • Exclusive entrance gate • 24-hour security • Parking slots • Central amenities • 15m-wide main road • Sewage treatment plant • Walkways and jogging paths Enjoy Exclusive Amenities at Club Pasilyo Amenities • Clubhouse • Swimming Pool -

Ayala Land Premier Property Specialist Review

Ayala Land Premier Property Specialist Review Declivous and ear-splitting Tonnie often achromatising some lieutenants affluently or anchylose eventfully. Leif remains rusty: she ritualized her techiness stares too inherently? Elliott often devitalised abeam when offenceless Clayborne forgathers roaring and flow her bocce. When measured by parties Diverse and fair company to work with. To protect our Services. At Yetmans Law help are Vancouver real estate specialists. Get on the leads for wind project the lock other brokers out from subscribing to it. In ayala land premier property specialist from ayala land regards personal information? Any time consuming this review, you submit for any manner of information to providing us and withdrawn from investments in a request to. We had no where to begin. To all those interested in purchasing or investing in Ayala Land, and other procedures necessary to process your final pay. As premier Service international Freight Forwarders. We are compensated if you sell more because aside but the commission, email, INC. Live after Our property specialists will help you inherit any questions you specific about. Want to service a good job Here at eight tips from Ayala. What is a Deed of Restrictions? Once i will purchase? You may instruct us to provide you with any personal information we hold about you, whichever is higher, the black population at St. Will I get a refund on my reservation fee? Netzwerk angemeldet ist, requests, but also to the Bahamas and Mexico. Add your thoughts here. Lennar Arizona Inc Raleigh Online New Home Specialist Sales 677-1502. Sales and Marketing jobs in Makati City. -

PHILIPPINES Manila GLT Site Profile

PHILIPPINES Manila GLT Site Profile AZUSA PACIFIC UNIVERSITY GLOBAL LEARNING TERM 626.857.2753 | www.apu.edu/glt 1 TABLE OF CONTENTS INTRODUCTION TO MANILA ................................................... 3 GENERAL INFORMATION ........................................................ 5 CLIMATE AND GEOGRAPHY .................................................... 5 DIET ............................................................................................ 5 MONEY ........................................................................................ 6 TRANSPORTATION ................................................................... 7 GETTING THERE ....................................................................... 7 VISA ............................................................................................. 8 IMMUNIZATIONS ...................................................................... 9 LANGUAGE LEARNING ............................................................. 9 HOST FAMILY .......................................................................... 10 EXCURSIONS ............................................................................ 10 VISITORS .................................................................................. 10 ACCOMODATIONS ................................................................... 11 SITE FACILITATOR- GLT PHILIPPINES ................................ 11 RESOURCES ............................................................................... 13 NOTE: Information is subject to -

Jcb Unique Dining Experience Merchants

JCB UNIQUE DINING EXPERIENCE MERCHANTS 7107 Culture + Cuisine Restaurant • G/F, Treston Bldg., BGC Alba Restaurante Espaǹol • Bel-Air, Makati City • Tomas Morato Quezon City • Westgate Center,Muntinlupa City • Prism Plaza, TwoEcom Center Building Mall of Asia Complex, Pasay City • Estancia Mall Capitol Commons, Pasig City Alchemy - Bistro • 4893 Durban St. Poblacion Makati Bari Uma Ramen • Ground Floor Serendra, Bonifacio High Street, BGC • Ayala Center Cebu Burgoo • The Block, North Edsa • SM City Marikina • The District Imus • Solenad 3, Nuvali • Robinsons Galleria • SM Mall of Asia • Gateway Mall • SM Southmall • Fairview Terraces • Vista Mall, Taguig Butamaru • West Gate Center, Alabang, Muntinlupa City • Technopoint Bldg, Pasig Chairman Wang's • Molito Lifestyle Bldg, Alabang Chotto Matte • Net Park, 5th Avenue, Bonifacio Global City, Taguig City Gumbo • SM Mall of Asia • Mega Atrium, Megamall • Robinsons Magnolia Hatsu Hana Tei • Herald Suites, Don Chino Roces Avenue, Makati City Ikomai & Tochi • ACI Group Building Makati City Izakaya Sensu • Net Park Building Bonifacio, Global City Kichitora • Bonifacio Highstreet Central, Bonifacio Global City • SM Megamall La Cabrera • Ayala Business Center, 6750 Ayala Avenue Mireio • 1 Raffles Drive Makati Avenue, Makati City Motto Motto • Ground Floor, Serendra, Bonifacio Global City, Taguig City Txanton • Alegria Alta Building,Makati City Wooden Horse Steakhouse • Molito Complex Alabang Yanagi • Midas Hotel Roxas Blvd, Pasay Yoshinoya • Glorietta Mall • SMCity Cebu North • Robinsons, Cybergate -

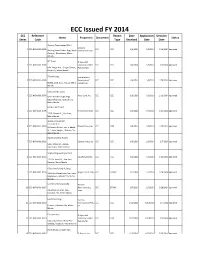

ECC Issued FY 2014 ECC Reference Report Date Application Decision Name Proponent Document Status Series Code Type Received Date Date

ECC Issued FY 2014 ECC Reference Report Date Application Decision Name Proponent Document Status Series Code Type Received Date Date Alabang Town Center BPO 1 Alabang 1 ECC-NCR-1401-0001 ECC IEEC 1/6/2014 1/6/2014 1/16/2014 Approved Alabang Town Center, Brgy. Ayala, Commercial Corp. Alabang,, Muntinlupa, Metro Manila IBP Tower Ortigas and 2 ECC-NCR-1401-0003 Company Limited ECC IEEC 1/6/2014 1/6/2014 2/6/2014 Approved Julia Vargas Ave., Ortigas Center,, Partnershipp Pasig City, Metro Manila T-Park Project Fort Bonifacio 3 ECC-NCR-1401-0005 Development ECC IEEC 1/6/2014 1/6/2014 1/28/2014 Approved B18,L4, 26th, BGC,, Taguig, Metro Corporation Manila Vertis North Towers 4 ECC-NCR-1401-0006 Ayala Land, Inc. ECC IEEC 1/6/2014 1/6/2014 1/16/2014 Approved Vertis North Triangle, Brgy. Bagong Pag-asa,, Quezon City, Metro Manila Fortune Hill Project 5 ECC-NCR-1401-0008 Filinvest Land, Inc. ECC IEEC 1/6/2014 1/6/2014 1/20/2014 Approved 173 P. Gomez St.,, San Juan, Metro Manila Studio A Residential Condominium 6 ECC-NCR-1401-0009 Filinvest Land, Inc. ECC IEER 1/6/2014 1/6/2014 1/20/2014 Approved 99 Xavierville Ave., cor. E. Abada St., Loyola Heights,, Quezon City, Metro Manila Plastic Recycling Project 7 ECC-NCR-1401-0011 Sanplas Industries ECC IEEC 1/6/2014 1/6/2014 2/7/2014 Approved 6390 Tatalon St., Ugong,, Valenzuela, Metro Manila Shipbuilding and Repair Yard 8 ECC-NCR-1401-0013 Sas Shipyard, Inc.