Annual Report 2018 ST BARBARA LIMITED 2018 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Mineral Facilities of Asia and the Pacific," 2007 (Open-File Report 2010-1254)

Table1.—Attribute data for the map "Mineral Facilities of Asia and the Pacific," 2007 (Open-File Report 2010-1254). [The United States Geological Survey (USGS) surveys international mineral industries to generate statistics on the global production, distribution, and resources of industrial minerals. This directory highlights the economically significant mineral facilities of Asia and the Pacific. Distribution of these facilities is shown on the accompanying map. Each record represents one commodity and one facility type for a single location. Facility types include mines, oil and gas fields, and processing plants such as refineries, smelters, and mills. Facility identification numbers (“Position”) are ordered alphabetically by country, followed by commodity, and then by capacity (descending). The “Year” field establishes the year for which the data were reported in Minerals Yearbook, Volume III – Area Reports: Mineral Industries of Asia and the Pacific. In the “DMS Latitiude” and “DMS Longitude” fields, coordinates are provided in degree-minute-second (DMS) format; “DD Latitude” and “DD Longitude” provide coordinates in decimal degrees (DD). Data were converted from DMS to DD. Coordinates reflect the most precise data available. Where necessary, coordinates are estimated using the nearest city or other administrative district.“Status” indicates the most recent operating status of the facility. Closed facilities are excluded from this report. In the “Notes” field, combined annual capacity represents the total of more facilities, plus additional -

Our Minerals and Mining Capabilities

KAURNA ACKNOWLEDGEMENT We acknowledge and pay our respects to the Kaurna Just as the minerals sector is central to our nation’s identity people, the original custodians of the Adelaide Plains and prosperity, so it is to the University of Adelaide. and the land on which the University of Adelaide’s Through our world-class research and development campuses at North Terrace, Waite, and Roseworthy expertise, we’ve supported and strengthened Australian are built. We acknowledge the deep feelings of WELCOME attachment and relationship of the Kaurna people mining since 1889; and we will continue to act as a catalyst to country and we respect and value their past, for its success well into the future. present and ongoing connection to the land and As you’ll see in these pages, our relevant expertise and cultural beliefs. The University continues to develop experience—coordinated and focused through our Institute respectful and reciprocal relationships with all for Mineral and Energy Resources—encompasses every Indigenous peoples in Australia, and with other Indigenous peoples throughout the world. aspect of the minerals value chain. You will also see evidenced here the high value we place on industry collaboration. We believe strong, productive partnerships are essential, both to address the sector’s biggest challenges and maximise its greatest opportunities. An exciting tomorrow is there for the making—more efficient, more productive and environmentally sustainable. We would welcome the chance to shape it with you. Regards, Professor Peter Høj -

ESG Reporting by the ASX200

Australian Council of Superannuation Investors ESG Reporting by the ASX200 August 2019 ABOUT ACSI Established in 2001, the Australian Council of Superannuation Investors (ACSI) provides a strong, collective voice on environmental, social and governance (ESG) issues on behalf of our members. Our members include 38 Australian and international We undertake a year-round program of research, asset owners and institutional investors. Collectively, they engagement, advocacy and voting advice. These activities manage over $2.2 trillion in assets and own on average 10 provide a solid basis for our members to exercise their per cent of every ASX200 company. ownership rights. Our members believe that ESG risks and opportunities have We also offer additional consulting services a material impact on investment outcomes. As fiduciary including: ESG and related policy development; analysis investors, they have a responsibility to act to enhance the of service providers, fund managers and ESG data; and long-term value of the savings entrusted to them. disclosure advice. Through ACSI, our members collaborate to achieve genuine, measurable and permanent improvements in the ESG practices and performance of the companies they invest in. 6 INTERNATIONAL MEMBERS 32 AUSTRALIAN MEMBERS MANAGING $2.2 TRILLION IN ASSETS 2 ESG REPORTING BY THE ASX200: AUGUST 2019 FOREWORD We are currently operating in a low-trust environment Yet, safety data is material to our members. In 2018, 22 – for organisations generally but especially businesses. people from 13 ASX200 companies died in their workplaces. Transparency and accountability are crucial to rebuilding A majority of these involved contractors, suggesting that this trust deficit. workplace health and safety standards are not uniformly applied. -

Aussie Mine 2016 the Next Act

Aussie Mine 2016 The next act www.pwc.com.au/aussiemine2016 Foreword Welcome to the 10th edition of Aussie Mine: The next act. We’ve chosen this theme because, despite gruelling market conditions and industry-wide poor performance in 2016, confidence is on the rise. We believe an exciting ‘next act’ is about to begin for our mid-tier miners. Aussie Mine provides industry and financial analysis on the Australian mid-tier mining sector as represented by the Mid-Tier 50 (“MT50”, the 50 largest mining companies listed on the Australian Securities Exchange with a market capitalisation of less than $5bn at 30 June 2016). 2 Aussie Mine 2016 Contents Plot summary 04 The three performances of the last 10 years 06 The cast: 2016 MT50 08 Gold steals the show 10 Movers and shakers 12 The next act 16 Deals analysis and outlook 18 Financial analysis 22 a. Income statement b. Cash flow statement c. Balance sheet Where are they now? 32 Key contributors & explanatory notes 36 Contacting PwC 39 Aussie Mine 2016 3 Plot summary The curtain comes up Movers and shakers The mining industry has been in decline over the last While the MT50 overall has shown a steadying level few years and this has continued with another weak of market performance in 2016, the actions and performance in 2016, with the MT50 recording an performances of 11 companies have stood out amongst aggregated net loss after tax of $1bn. the crowd. We put the spotlight on who these movers and shakers are, and how their main critic, their investors, have But as gold continues to develop a strong and dominant rewarded them. -

2013 Global Gold Price Report Annually, Pwc Surveys Gold Mining Companies from Around the World

www.pwc.com/ca/mining 2013 Global Gold Price Report Annually, PwC surveys gold mining companies from around the world. This year, we contacted executives from a cross-section of senior, mid-tier and junior gold mining companies representing 35 million ounces of gold mined in 2012 and 35 million ounces expected to be mined in 2013. Inside 1 Survey participants 14 Interview with Randy Smallwood, President and CEO, Silver Wheaton Corporation 2 PwC’s point of view 17 Global silver price survey responses 4 Gold price performance 18 Deals activity in 2012 6 Interview with Jamie Sokalsky, President and CEO, Barrick Gold Corporation 20 Gold deal activity 8 Gold miners’ cash allocation and capital 22 Mining in South Africa — 2013 outlook investment strategies Back Contact information 10 Mine planning data ii Global gold price Global silver price survey participants survey participants We would like to thank the senior executives from the companies We would like to thank the senior executives listed below for participating in our Global Gold Price Survey. from the companies listed below for participating in our Global Silver Price Survey. Agnico-Eagle Mines Ltd McEwen Mining Inc Coeur d’Alene Mines Corp Amara Mining plc Midway Gold Corp Endeavour Silver Corp B2Gold Corp New Gold Inc First Majestic Silver Corp Barrick Gold Corp Newmont Mining Corp Fortuna Silver Mines Inc Caledonia Mining Corp Northern Star Mining Corp Great Panther Silver Ltd Cerro Grande Mining Corp OceanaGold Corp Impact Silver Corp Centerra Gold Inc Orvana Minerals Corp Pan American -

The Mineral Industry of Australia in 2008

2008 Minerals Yearbook AUSTRALIA U.S. Department of the Interior August 2010 U.S. Geological Survey THE MINERAL INDUS T RY OF AUS T RALIA By Pui-Kwan Tse Australia was one of the world’s leading mineral producing and the Brockman iron project in the Pilbara region of Western countries and ranked among the top 10 countries in the world Australia (Australian Bureau of Agricultural and Resource in the production of bauxite, coal, cobalt, copper, gem and Economics, 2009a). near-gem diamond, gold, iron ore, lithium, manganese ore, tantalum, and uranium. Since mid-2008, the global financial Minerals in the National Economy crisis had sharply weakened world economic activities, and the slowdown had been particularly pronounced in the developed Australia’s mining sector contributed more than $105 billion countries in the West. Emerging Asian economies were also to the country’s gross domestic product (GDP), or 7.7% of the adversely affected by the sharply weaker demand for exports GDP during fiscal year 2007-08. In 2008, the mining sector and tighter credit conditions. After a period of strong expansion, employed 173,900 people who worked directly in mining and an Australia’s economic growth decreased by 0.5% in the final additional 200,000 who were involved in supporting the mining quarter of 2008. Overall, Australia’s economy grew at a rate activities. Expectations of sustained levels of global demand for of 2.4% during 2008. During the past several years, owing to minerals led to increased production of minerals and metals in anticipated higher prices of mineral commodities in the world Australia, and the mineral industry was expected to continue markets, Australia’s mineral commodity output capacities to be a major contributor to the Australian economy in the next expanded rapidly. -

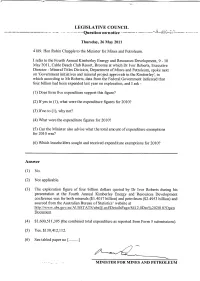

2011-08-09 Qon Exploration Expenditure

LEGISLATIVE COUNCIL C 'lff"\ 1"'.( "''1 ---------~~-~Question- on"notice ----------- ..'-?ibt;-:s::'.;"--- --_.- Thursday, 26 May 2011 4189. Hon Robin Chapple to the Minister for Mines and Petroleum. I refer to the Fourth Annual Kimberley Energy and Resources Development, 9 - 10 May 2011, Cable Beach Club Resort, Broome at which Dr Ivor Roberts, Executive Director - Mineral Titles Division, Department of Mines and Petroleum, spoke next on 'Government initiatives and mineral project approvals in the Kimberley', in which according to Mr Roberts, data from the Federal Government indicated that four billion had been expended last year on exploration, and 1 ask - (1) Does form five expenditure support this figure? (2) If yes to (1), what were the expenditure figures for 201O? (3) Ifno to (1), why not? (4) What were the expenditure figures for 2010? (5) Can the Minister also advise what the total amount of expenditure exemptions for 2010 was? (6) Which leaseholders sought and received expenditure exemptions for 2010? Answer (1) No. (2) Not applicable. (3) The exploration figure of four billion dollars quoted by Dr Ivor Roberts during his presentation at the Fourth Annual Kimberley Energy and Resources Development conference was for both minerals ($1.4017 billion) and petroleum ($2.4953 billion) and sourced from the Australian Bureau of Statistics' website at http://www.abs.gov.au/AUSST ATS/[email protected]/DetailsPage/8412.0Dec%20201 O?Open Document (4) $1,600,511,395 (the combined total expenditure as reported from Form 5 submissions). (5) Yes, $130,412,112. -

Stoxx® Australia 150 Index

STOXX® AUSTRALIA 150 INDEX Components1 Company Supersector Country Weight (%) Commonwealth Bank of Australia Banks Australia 8.37 CSL Ltd. Health Care Australia 7.46 BHP GROUP LTD. Basic Resources Australia 7.23 National Australia Bank Ltd. Banks Australia 4.37 Westpac Banking Corp. Banks Australia 4.09 Australia & New Zealand Bankin Banks Australia 3.75 Wesfarmers Ltd. Retail Australia 3.30 WOOLWORTHS GROUP Personal Care, Drug & Grocery Australia 2.87 Macquarie Group Ltd. Financial Services Australia 2.84 Rio Tinto Ltd. Basic Resources Australia 2.48 Fortescue Metals Group Ltd. Basic Resources Australia 2.27 Transurban Group Industrial Goods & Services Australia 2.20 Telstra Corp. Ltd. Telecommunications Australia 2.05 Goodman Group Real Estate Australia 1.77 AFTERPAY Industrial Goods & Services Australia 1.54 Coles Group Personal Care, Drug & Grocery Australia 1.39 Woodside Petroleum Ltd. Energy Australia 1.28 Newcrest Mining Ltd. Basic Resources Australia 1.27 Aristocrat Leisure Ltd. Travel & Leisure Australia 1.11 XERO Technology Australia 1.00 SYDNEY AIRPORT Industrial Goods & Services Australia 0.93 Brambles Ltd. Industrial Goods & Services Australia 0.91 Sonic Healthcare Ltd. Health Care Australia 0.90 ASX Ltd. Financial Services Australia 0.82 SCENTRE GROUP Real Estate Australia 0.80 Cochlear Ltd. Health Care Australia 0.74 QBE Insurance Group Ltd. Insurance Australia 0.73 SUNCORP GROUP LTD. Insurance Australia 0.71 South32 Australia Basic Resources Australia 0.71 Santos Ltd. Energy Australia 0.68 Ramsay Health Care Ltd. Health Care Australia 0.66 Insurance Australia Group Ltd. Insurance Australia 0.65 Mirvac Group Real Estate Australia 0.60 DEXUS Real Estate Australia 0.59 SEEK Ltd. -

IATA Codes for Papua New Guinea

IATA Codes for Papua New Guinea N.B. To check the official, current database of IATA Codes see: http://www.iata.org/publications/Pages/code-search.aspx City State IATA Code Airport Name Web Address Afore AFR Afore Airstrip Agaun AUP Aiambak AIH Aiambak Aiome AIE Aiome Aitape ATP Aitape Aitape TAJ Tadji Aiyura Valley AYU Aiyura Alotau GUR Ama AMF Ama Amanab AMU Amanab Amazon Bay AZB Amboin AMG Amboin Amboin KRJ Karawari Airstrip Ambunti AUJ Ambunti Andekombe ADC Andakombe Angoram AGG Angoram Anguganak AKG Anguganak Annanberg AOB Annanberg April River APR April River Aragip ARP Arawa RAW Arawa City State IATA Code Airport Name Web Address Arona AON Arona Asapa APP Asapa Aseki AEK Aseki Asirim ASZ Asirim Atkamba Mission ABP Atkamba Aua Island AUI Aua Island Aumo AUV Aumo Babase Island MKN Malekolon Baimuru VMU Baindoung BDZ Baindoung Bainyik HYF Hayfields Balimo OPU Bambu BCP Bambu Bamu BMZ Bamu Bapi BPD Bapi Airstrip Bawan BWJ Bawan Bensbach BSP Bensbach Bewani BWP Bewani Bialla, Matalilu, Ewase BAA Bialla Biangabip BPK Biangabip Biaru BRP Biaru Biniguni XBN Biniguni Boang BOV Bodinumu BNM Bodinumu Bomai BMH Bomai Boridi BPB Boridi Bosset BOT Bosset Brahman BRH Brahman 2 City State IATA Code Airport Name Web Address Buin UBI Buin Buka BUA Buki FIN Finschhafen Bulolo BUL Bulolo Bundi BNT Bundi Bunsil BXZ Cape Gloucester CGC Cape Gloucester Cape Orford CPI Cape Rodney CPN Cape Rodney Cape Vogel CVL Castori Islets DOI Doini Chungribu CVB Chungribu Dabo DAO Dabo Dalbertis DLB Dalbertis Daru DAU Daup DAF Daup Debepare DBP Debepare Denglagu Mission -

St Barbara Limited

St Barbara Limited ACN 009 165 066 Level 10, 432 St Kilda Road, Melbourne VIC 3004 Locked Bag 9, Collins Street East, Melbourne VIC 8003 Tel +61 3 8660 1900 Fax +61 3 8660 1999 www.stbarbara.com.au Notice of 2012 Annual General Meeting The Annual General Meeting of the Company will be held at 11.00 am (Melbourne time) on Thursday 22 November 2012, in the State Library of Victoria Conference Centre, Entry 3 in La Trobe Street between Russell and Swanston Streets, Melbourne. The 2012 Annual Report, Notice of Annual General Meeting and Proxy Form are attached, as distributed to shareholders today. Ross Kennedy Executive General Manager Corporate Services Company Secretary 22 October 2012 For personal use only 1 Annual Report 2012 For personal use only Contents 01 Introduction 04 Chairman and Managing Director & CEO’s Joint Report 06 Operations Report 08 Discovery and Growth 09 Chief Financial Offi cer’s Review 10 People, Environment, Safety & Social Responsibility 11 Board of Directors 12 Executives 13 Ore Reserves and Mineral Resources Statements 18 Corporate Governance 21 Financial Statements Highlights Gold Production Revenue 338,879 ounces – 31% $541 million – 50% 2012 2012 2011 2011 2010 2010 2009 2009 2008 2008 0 50,000 100,000 150,000 200,000 250,000 300,000 350,000 0 150,000 300,000 450,000 600,000 NPAT EPS $130 million – 90% 40 cents per share (1) – 90% For personal use only 2012 2012 2011 2011 2010 2010 2009 2009 2008 2008 -90 -60 -30 0 30 60 90 120 150 -40 -20 0 20 40 (1) Shares adjusted for 6:1 consolidation in November 2010 Introduction 2012 was an historic year for St Barbara. -

Simberi – Oxide and Sulphide

ST BARBARA LIMITED SHORT FORM RESOURCE REPORT Simberi – Oxide and Sulphide TENEMENT: ML136 OWNER: St Barbara Ltd 100% OPERATOR: Simberi Gold Company Limited Simberi Island, New Ireland Province, Papua New Guinea COMMODITIES: Gold MODELED BY: Chris De-Vitry REPORT BY: Chris De-Vitry MODEL DATE: 31 December 2019 JORC CODE STATEMENT The information in this report that relates to Mineral Resources is based on information compiled by Chris De- Vitry, who is a member of the Australasian Institute of Mining and Metallurgy. Chris De-Vitry is an employee of Manna Hill Geoconsulting and has sufficient experience relevant to the style of mineralisation and type of deposit under consideration and to the activity which he is undertaking to qualify as a Competent Person as defined in the 2012 Edition of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”. Chris De-Vitry consents to the inclusion in the report of the matters based on his information in the form and context in which it appears. Project Summary The Simberi Gold Project is located on Simberi Island in the Tabar Islands Group situated in the New Ireland Province of Papua New Guinea (PNG), approximately 80 km north-west of Lihir Island. Simberi is the oldest and northernmost island of the Tabar Group. It measures approximately 10 km east-west, 8 km north-south and rises to over 300 m above sea level. The currently known gold prospects (Sorowar, Pigiput, Pigibo, Botlu, Pigicow, Samat, Bekou and Monun Creek) on Simberi Island are located in the eastern half of the island within the central volcanic core.