State Strategies to Detect Local Fiscal Distress How States Assess and Monitor the Financial Health of Local Governments

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Press Release: National Organization Names

STATE OF MINNESOTA OFFICE OF THE STATE AUDITOR SUITE 500 525 PARK STREET (651) 296-2551 (Voice) (651) 296-4755 (Fax) REBECCA OTTO SAINT PAUL, MN 55103-2139 [email protected] (E-mail) STATE AUDITOR 1-800-627-3529 (Relay Service) ***PRESS RELEASE*** National Organization Names State Auditor Otto to Program Committee Contact: Jim Levi, Office of the State Auditor, (651) 297-3683, [email protected] ST. PAUL (1/4/2010) – Minnesota State Auditor Rebecca Otto has been invited by the President of the National Association of State Auditors, Comptrollers and Treasurers (NASACT) to serve on the Annual Conference Program Committee. The Committee, which develops the educational program for the NASACT annual conference, is chaired by NASACT President Glen B. Gainer III, the State Auditor of West Virginia. "I am honored to be invited to serve on this committee with other State Auditors, Comptrollers and Treasurers from around the country," said State Auditor Otto. Founded in 1915, NASACT is an organization for state officials who deal with the financial management of state government. The group's mission is to assist state leaders in enhancing and promoting effective and efficient management of government resources. The 2010 NASACT Annual Conference will be held August 7-11 in Charleston, West Virginia. -- 30 -- The Office of the State Auditor is a constitutional office that is charged with overseeing more than $20 billion spent annually by local governments in Minnesota. The Office of the State Auditor does this by performing audits of local government financial statements, and by reviewing documents, data, reports, and complaints reported to the Office. -

AVAILABLE from DOCUMENT RESUME SP 038 711 Minnesota State High School League. a Program Evaluation Minnesota State Office Of

DOCUMENT RESUME ED 433 308 SP 038 711 TITLE Minnesota State High School League. A Program Evaluation Report. Report #98-07. INSTITUTION Minnesota State Office of the Legislative Auditor, St. Paul. Program Evaluation Div. PUB DATE 1998-06-00 NOTE 65p. AVAILABLE FROM Legislative Auditor's Office, Program Evaluation Division, Centennial Office Bldg., First Floor South, St. Paul, MN 55155; Tel: 612-296-4708; Fax: 612-296-4712; Web site: http://www.auditor.leg.state.mn.us/ped2.htm; alternative formats such as large print, Braille, or audio tape: Tel: 612-296-8976, or Minnesota Relay Service: Tel: 612-297-5353; Tel: 800-627-3529 (Toll Free). PUB TYPE Reports - Evaluative (142) EDRS PRICE MF01/PC03 Plus Postage. DESCRIPTORS *Accountability; Athletics; Costs; *Extracurricular Activities; High School Students; High Schools; Private Schools; Program Evaluation; Public Schools; State Government; State Legislation IDENTIFIERS *Minnesota ABSTRACT This document presents a program evaluation report of the Minnesota State High School League, a nonprofit corporation that is a voluntary association of public and private high schools. Member schools delegate control of certain extracurricular activities to the League and, in turn, the League administers athletic and fine arts programs and competitions and establishes student eligibility rules. It is not a state agency, though in the last decade, the state legislature has shown continuing interest in its activities. This study focused on changes that have occurred since the 1987 evaluation of the League, state laws that govern the League's operation and how they compare with those governing state agencies, and changes needed to make the League more accountable to the legislature, students, parents, member schools, and the public. -

Capitol Region Watershed District Management Letter

State of Minnesota Julie Blaha State Auditor ______________________________________________________________________________ Capitol Region Watershed District Saint Paul, Minnesota Management and Compliance Report Year Ended December 31, 2020 Description of the Office of the State Auditor The mission of the Office of the State Auditor is to oversee local government finances for Minnesota taxpayers by helping to ensure financial integrity and accountability in local governmental financial activities. Through financial, compliance, and special audits, the State Auditor oversees and ensures that local government funds are used for the purposes intended by law and that local governments hold themselves to the highest standards of financial accountability. The State Auditor performs approximately 100 financial and compliance audits per year and has oversight responsibilities for over 3,300 local units of government throughout the state. The office currently maintains five divisions: Audit Practice – conducts financial and legal compliance audits of local governments; Government Information – collects and analyzes financial information for cities, towns, counties, and special districts; Legal/Special Investigations – provides legal analysis and counsel to the Office and responds to outside inquiries about Minnesota local government law; as well as investigates allegations of misfeasance, malfeasance, and nonfeasance in local government; Pension – monitors investment, financial, and actuarial reporting for Minnesota’s local public pension funds; -

Pension Fund Leaders Term Corporate Board Diversification ‘Unacceptably Slow,’ Call for Increased Attention from Investors, Corporate Boards

FOR IMMEDIATE RELEASE PR16:21 Contact: Marc Lifsher June 1, 2016 [email protected] 916-653-2995 Pension Fund Leaders Term Corporate Board Diversification ‘Unacceptably Slow,’ Call for Increased Attention From Investors, Corporate Boards California State Treasurer John Chiang joins group of fiduciaries from funds with more than $1 trillion under management SACRAMENTO – California State Treasurer John Chiang today joined a group of state and local officials who contend that corporate boards have been too slow to diversify their ranks and that institutional investors should increase their focus on board diversity as a corporate governance priority. The joint statement emphasizes that racial and LGBT diversity as well as gender diversity are critical dimensions of effective board composition and performance. “There is broad agreement that a diverse corporate board is good for business,” Treasurer Chiang said. “Boards with directors, who possess a wide range of skills and experiences, are better positioned to oversee company strategy, risk mitigation and management performance.” Statistics show that board diversification has been slow—or has even regressed. White directors hold 85 percent of the board seats at the largest 200 S&P 500 companies, and the percentage of those boards with exclusively white directors has increased over the last decade. Men occupy 80 percent of all S&P 500 board seats. It is also estimated that there are fewer than 10 openly lesbian, gay, bisexual, or transgender directors among Fortune 500 companies. The 14 co-signers, many of them longtime leaders on the issue of board diversity, are fiduciaries for pension funds responsible for the retirement security of six million participants and with more than $1 trillion in assets under management. -

Graduate Affairs Committee January 27, 2004 3:30 P.M

Graduate Affairs Committee January 27, 2004 3:30 p.m. - 5:00 p.m. UL 1126 AGENDA 1. Approval of the minutes for November 25, 2003 .................................................... Queener 2. Associate Dean’s Report .......................................................................................... Queener 3. Purdue Dean’s Report ................................................................................................... Story 4. Graduate Office Report ............................................................................................ Queener 5. Committee Business a. Curriculum Subcommittee ........................................................................... O’Palka 6. International Affairs a. IELTS vs. TOEFL ............................................................................................ Allaei 7. Program Approval .................................................................................................... Queener a. M.S. Health Sciences Education – Name Change b. M.A. in Political Science c. M.S. in Music Therapy 8. Discussion ................................................................................................................ Queener a. MSD Thesis Optional b. Joint Ph.D. in Electrical and Computer Engineering 9. New Business…………………………………… 10. Next Meeting (February 24) and adjournment Graduate Affairs Committee January 27, 2004 Minutes Present: William Bosron, Mark Brenner (co-chair), Ain Haas, Dolores Hoyt, Andrew Hsu, Jane Lambert, Joyce MacKinnon, Jackie O’Palka, Douglas -

Two Women Deny Terrorism Endangered Jamaica Jihadists Plead Not Guilty to Plotting Terror Attack in U.S

• JAMAICA TIMES • ASTORIA TIMES • FOREST HILLS LEDGER • LAURELTON TIMES LARGEST AUDITED • QUEENS VILLAGE TIMES COMMUNITY • RIDGEWOOD LEDGER NEWSPAPER • HOWARD BEACH TIMES IN QUEENS • RICHMOND HILL TIMES May 15–21, 2015 Your Neighborhood — Your News® FREE ALSO COVERING ELMHURST, JACKSON HEIGHTS, LONG ISLAND CITY, MASPETH, MIDDLE VILLAGE, REGO PARK, SUNNYSIDE Steinway site Two women deny terrorism endangered Jamaica jihadists plead not guilty to plotting terror attack in U.S. by buildings BY SADEF ALI KULLY BY BILL PARRY GIVING IT HER BEST SHOT Two women from Jamaica who were accused of plotting Passions are running high a terror attack in the United among Astoria preservation- States pleaded not guilty to ists since the city Department conspiracy to use a weapon of Buildings made public the of mass destruction and addi- owners’ plans for construc- tonal counts related to their tion at the Steinway Mansion. alleged terror plot after a While the historic 27-room grand jury indictment May 8 home, built by the legendary in Brooklyn federal court. piano-making Steinway fam- After evidence was pre- ily in 1858, is landmarked and sented to a grand jury, Asia cannot be touched, the acre of Siddiqui, 31, and Noelle Velent- land it sits on is not. zas, 28, were also charged with Philip Loria, an attorney teaching and distributing in- at the Astoria-based law firm formation pertaining to the Loria and Associates, and his making and use of an explo- partner, who purchased the sive, destructive device and Steinway Mansion for $2.65 weapon of mass destruction. million last year, plan to exca- Siddiqui was also charged vate the sloping hill that domi- with making material false nates the property to within statements in a federal grand feet of the home and level the jury indictment, according to land for development. -

IN the UNITED.Tif

Exhibit A Exhibit A Rule 2002 Service List Description of Party Notice Party Address1 Address2 Address3 City State Zip Office of the United States Trustee Office of the United States Trustee Frank J. Perch III 844 King Street Suite 2207 Wilmington DE 19801 Federal Energy Regulatory Commission Federal Energy Regulatory Commission Attn: Cynthia A. Marlette 888 First Street NE Washington DC 20246 Montana Public Service Commission Montana Public Service Commission Rob Rowe, Chairman 1701 Prospect Avenue Helena MT 59620-2601 South Dakota Public Service Commission South Dakota Public Utilities Commission Pam Bonrud, Executive Director Capitol Building, 1st Floor 500 East Capitol Avenue Pierre SD 57501-5070 Nebraska Public Service Commission Nebraska Public Service Commission Anne C. Boyle, Chairwoman 1200 N. Street, Suite 300 Lincoln NE 68508 Securities and Exchange Commission Securities and Exchange Commission Attn: David Lynn, Chief Counsel 450 Fifth Street Washington DC 20549 Timothy R. Pohl, Esq. Attorney for DIP Lenders Skadden Arps Samuel Ory, Esq. 333 West Wacker Drive Chicago IL 60606 Jesse Austin, Esq. Attorney for Debtor Paul, Hastings, Janofsky & Walker, LLP Karol Denniston, Esq. 600 Peachtree Road NE Atlanta GA 30308 Scott D. Cousins, Esq. Victoria W. Counihan, Esq. Local Counsel Greenberg Traurig LLP William E. Chipman, Jr., Esq. The Brandywine Building 1000 West Street Suite 1540 Wilmington DE 19801 Cayman Islands Branch/Syndicated Primary Lender and Agent for Finance Group Pre-petition Lenders Credit Suisse First Boston Secured Term Loan Credit Facility Attn: Rob Loh 11 Madison Avenue 21st Floor New York NY 10010 DIP Lender Bank One, NA DIP Lender Attn: Andrew D. -

American Legislative Exchange Council (ALEC) in Support of Proposed Regulation

July 30, 2020 Mr. James A. DeWitt Office of Regulations and Interpretations Employee Benefits Security Administration Room N-5655 U.S. Department of Labor 200 Constitution Ave., NW Washington, DC 20210 Re: RIN 1210-AB95, Financial Factors in Selecting Plan Investments; Comments of the American Legislative Exchange Council (ALEC) in support of proposed regulation Dear Mr. DeWitt, The American Legislative Exchange Council (ALEC) submits these comments in support of a regulation proposed under Title I of the Employee Retirement Income Security Act of 1974 (ERISA). The proposed regulation would confirm that EIRSA requires plan fiduciaries to select investments and investment courses of actions based solely on pecuniary considerations relevant to the risk-adjusted economic value of a particular investment or investment course of action. The proposal would clarify that “investment behaviors, such as socially responsible investing, sustainable and responsible investing, environmental, social, and corporate governance (ESG) investing, and economically targeted investing”1 fall outside of the pecuniary requirements mandated by ERISA. ALEC supports the proposed regulation and recommends that the Department of Labor, through the Employee Benefits Security Administration, adopt it. This recommendation follows ALEC research and analysis on public pension investments, which offer counterfactuals of what happens when divestments occur due to environmental or social reasons rather than pecuniary concerns. Individual investors can assume higher financial -

2008 Verizon Political Contributions Report

VERIZON POLITICAL CONTRIBUTIONS JANUARY – DECEMBER 2008 Verizon Political Contributions January – December 2008 1 A Message from Tom Tauke Verizon is affected by a wide variety of government policies — from telecommunications regulation to taxation to health care and more — that have an enormous impact on the business climate in which we operate. We owe it to our shareowners, employees and customers to advocate public policies that will enable us to compete fairly and freely in the marketplace. Political contributions are one way we support the democratic electoral process and participate in the policy dialogue. Our employees have established political action committees at the federal level and in 25 states. These political action committees (PACs) allow employees to pool their resources to support candidates for office who generally support the public policies our employees advocate. This report lists all PAC contributions and corporate political contributions made by Verizon in 2008. The contribution process is overseen by the Corporate Governance and Policy Committee of our Board of Directors, which receives a comprehensive report and briefing on these activities at least annually. We intend to update this voluntary disclosure twice a year and publish it on our corporate website. We believe this transparency with respect to our political spending is in keeping with our commitment to good corporate governance and a further sign of our responsiveness to the interests of our shareowners. Thomas J. Tauke Executive Vice President Public -

How Are Digital Trends Reshaping Government Financial Organizations? Findings from Deloitte NASACT 2015 Digital Government Transformation Survey

How are digital trends reshaping government financial organizations? Findings from Deloitte NASACT 2015 Digital Government Transformation Survey A publication of Deloitte and the National Association of State Auditors, Comptrollers and Treasurers (NASACT) Message from NASACT Findings from the Deloitte NASACT 2015 Digital Government Transformation Survey of US state and local financial government executives help shed light on the state of digital transformation in government. A total of 33 NASACT members, with diverse functional and organizational backgrounds, participated in the survey. This is a subset of Deloitte’s Global Digital Government Transformation Survey that covered 1,205 public sector executives across 70+ countries during January and February 2015. The survey explores how digital transformation is reshaping state and local governments. It seeks to understand what strategies government organizations are using to navigate the digital roadmap and to identify the areas of greatest opportunity in adapting a digital-first strategy. The organizations have to recognize that digital transformation is not just about implementing digital technologies. They have to create a strategic plan to best implement a digital transformation by taking into consideration a number of issues, such as: • How does the culture of an organization impact digital transformation? • Do leaders and workforces have sufficient skills and resources to successfully achieve digital transformation? • What procurement processes are in place to provide much-needed flexibility to design and develop digital services? Not surprisingly, many organizations recognize hurdles to manage the digital transition in all of these areas. At least two-thirds of the organizations find it challenging to manage digital transition in each — culture, leadership, workforce, and procurement. -

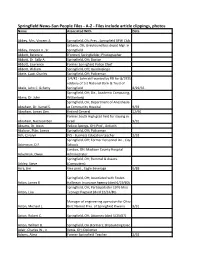

Springfield News-Sun People Files - A-Z - Files Include Article Clippings, Photos Name Associated with Date

Springfield News-Sun People Files - A-Z - Files include article clippings, photos Name Associated With Date Abbey, Mrs. Vincent A. Springfield, Oh; Pres., Springfield BPW Club Urbana, OH; Greyhound bus depot Mgr. in Abbey, Vincent A., Sr. Springfield Abbott, Berenice (Former) Springfielder; Photographer Abbott, Dr. Sally A. Springfield, OH; Doctor Abbott, Lawrence Former Springfield Police Chief Abbott, William Springfield, OH; Quadraplegic Abele, Capt. Charles Springfield, OH; Policeman 1/4/42 - John still wanted by FBI for 8/1935 robbery of 1st National Bank & Trust of Abele, John C. & Betty Springfield 8/29/35 Springfield, OH; Dir., Academic Computing, Abma, Dr. John Wittenberg Springfield, OH; Department of Anesthesia Abraham, Dr. Kamel S. at Community Hospital 9/93 Abraham, James Gen. Retired General 12/90 Former South High grad held for slaying in Abraham, Nachson Ben Israel 9/91 Abrams, Dr. Irwin Yellow Springs, OH; Prof., Antioch Abshear, Ptlm. James Springfield, OH; Policeman Ach, Carolyn JVS - Business Education teacher 2/93 Springfield, OH; Former Personnel Dir., City Ackerman, D.F. Schools London, OH; Madison County Hospital Ackerman, Owen Administrator Springfield, OH; Rummel & Assocs. Ackley, Steve (Computers) Acra, Jim Vice presi., Eagle Beverage 6/88 Springfield, OH; Associated with Foster- Acton, James R. Hallinean Insurance Agency (died 6/19/80) Springfield, OH; Participated in 1976 Miss Acton, Lisa Teenage Pageant (died 12/24/80) Manager of engineering operation for Ohio Acton, Michael L. Bell; Named Pres. of Springfield Kiwanis 9/91 Acton, Robert C. Springfield, OH; Attorney (died 5/25/87) Acton, William B. Springfield, OH (Former); Shipbuilding Exec. Adair, Charles W., Jr. -

County of Greene, Ohio

County of Greene, Ohio 2019 Annual Information Statement in connection with Bonds, Notes and Certificates of Indebtedness of the County This Annual Informational Statement pertains to the operations of Greene County for the calendar year 2018 (where possible, 2019 data has been provided). In addition to providing information on an annual basis, the County of Greene intends that this Statement will be used, together with information to be specifically provided by the County for that purpose, in connection with the original offering and issuance by the County of its bonds, notes and certificates of indebtedness. Questions regarding information contained in this Annual Information Statement should be directed to David A. Graham, Greene County Auditor, Greene County Office Building, 69 Greene Street, Xenia, Ohio 45385. The date of this Annual Information Statement is September 1, 2019. TABLE OF CONTENTS Page INTRODUCTORY STATEMENT ................................................................................................ 1 GREENE COUNTY, OHIO ........................................................................................................... 2 County Government .................................................................................................................. 2 General Government ........................................................................................................... 3 Administration of Justice System ....................................................................................... 4 County-owned