Uber Technologies, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Amazon's Antitrust Paradox

LINA M. KHAN Amazon’s Antitrust Paradox abstract. Amazon is the titan of twenty-first century commerce. In addition to being a re- tailer, it is now a marketing platform, a delivery and logistics network, a payment service, a credit lender, an auction house, a major book publisher, a producer of television and films, a fashion designer, a hardware manufacturer, and a leading host of cloud server space. Although Amazon has clocked staggering growth, it generates meager profits, choosing to price below-cost and ex- pand widely instead. Through this strategy, the company has positioned itself at the center of e- commerce and now serves as essential infrastructure for a host of other businesses that depend upon it. Elements of the firm’s structure and conduct pose anticompetitive concerns—yet it has escaped antitrust scrutiny. This Note argues that the current framework in antitrust—specifically its pegging competi- tion to “consumer welfare,” defined as short-term price effects—is unequipped to capture the ar- chitecture of market power in the modern economy. We cannot cognize the potential harms to competition posed by Amazon’s dominance if we measure competition primarily through price and output. Specifically, current doctrine underappreciates the risk of predatory pricing and how integration across distinct business lines may prove anticompetitive. These concerns are height- ened in the context of online platforms for two reasons. First, the economics of platform markets create incentives for a company to pursue growth over profits, a strategy that investors have re- warded. Under these conditions, predatory pricing becomes highly rational—even as existing doctrine treats it as irrational and therefore implausible. -

Move Over Ipos: Unicorn Direct Listings May Be the New Mythical Beasts in Town

Fordham Journal of Corporate & Financial Law Volume 26 Issue 1 Article 5 2021 Move Over IPOs: Unicorn Direct Listings May Be the New Mythical Beasts in Town Tatum Sornborger Fordham University School of Law Follow this and additional works at: https://ir.lawnet.fordham.edu/jcfl Part of the Securities Law Commons Recommended Citation Tatum Sornborger, Move Over IPOs: Unicorn Direct Listings May Be the New Mythical Beasts in Town, 26 Fordham J. Corp. & Fin. L. 215 (2021). This Note is brought to you for free and open access by FLASH: The Fordham Law Archive of Scholarship and History. It has been accepted for inclusion in Fordham Journal of Corporate & Financial Law by an authorized editor of FLASH: The Fordham Law Archive of Scholarship and History. For more information, please contact [email protected]. MOVE OVER IPOS: UNICORN DIRECT LISTINGS MAY BE THE NEW MYTHICAL BEASTS IN TOWN Tatum Sornborger* ABSTRACT Most people think of “going public” as an Initial Public Offering (IPO), but as IPOs have boomed and busted over the past decade, the direct listing has emerged as an unconventional but viable way to raise capital. The direct listing approach was uncovered by one rebellious “unicorn,” a term used to describe privately held companies with valuations exceeding one billion dollars. By circumventing the traditional IPO process, Spotify prompted both the SEC and major stock exchanges to examine direct listings and promulgate rules for future offerings. Though these rules are still developing, companies now have a clear path to follow in Spotify’s footsteps and forgo the traditional IPO. -

Capstone Headwaters Education Technology M&A Coverage Report

Capstone Headwaters EDUCATION TECHNOLOGY 2019 YEAR IN REVIEW TABLE OF CONTENTS MERGER & ACQUISTION OVERVIEW M&A Overview The Education Technology (EdTech) industry has continued to experience rapid consolidation with 195 transactions announced or completed in 2019. Active Buyers Heightened merger and acquisition (M&A) activity has been fueled by Notable Transactions persistent demand for disruptive and scalable technology as industry operators Select Transactions seek to expand product offerings and market share. In addition to robust transaction activity, recent investment patterns have targeted EdTech providers Public Company Data that offer innovative products for classroom teacher support and to streamline Firm Transactions in Market administrative operations in K-12 schools. Funding in the segment has risen Firm Track Record substantially with teacher needs and school operations garnering $95 million and $148 million in 2018, respectively, according to EdSurge.1 Large industry operators have remained acquisitive through year-end, evidenced by Renaissance Learning’s three acquisitions (page three) in 2019. CONTRIBUTORS EdTech providers have also utilized M&A as a means to diversify product offerings and end-markets outside of their core competencies. Notably, Health Jacob Voorhees & Safety Institute, a leader in environmental health and safety software and Managing Director, training services, acquired Martech Media, Inc, a provider of industrial Head of Education Practice, technology e-learning training solutions (December 2019, undisclosed). Head of Global M&A 617-619-3323 Private equity firms have remained active in the industry, accounting for 52% of [email protected] transaction volume. Operators that provide disruptive platforms and institutional business models, selling directly to schools districts, have garnered David Michaels significant investment interest and premium valuations. -

Q2 2016 Venture Capital Deals and Exits Download the Data Pack July 2016

Q2 2016 Venture Capital Deals and Exits Download the Data Pack July 2016 Fig. 1: Global Quarterly Venture Capital Deals*, Q1 2011 - Fig. 3: Number of Venture Capital Deals in Q2 2016 by Q2 2016 Fig. 2: Venture Capital Deals* in Q2 2016 by Region Investment Stage 3,000 50 100% 1.5 187 0.6 Angel/Seed 45 1.0 Aggregate Deal Value ($bn) DealValue Aggregate 90% 53 2,500 237 40 80% 1% 8% Series A/Round 1 1% 3% 35 16.7 Series B/Round 2 2,000 70% 460 2% 30 3% 60% 33% Series C/Round 3 1,500 25 50% 407 7% 20 3.1 Series D/Round 4 and Later No. of Deals 1,000 40% 15 Growth Capital/Expansion Proportion of Total Proportion 30% 10 500 17.5 15% PIPE 5 20% 900 0 0 10% Grant Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 0% 27% Venture Debt 2011 2012 2013 2014 2015 2016 No. of Deals Aggregate Deal Value ($bn) Add-on & Other No. of Deals Aggregate Deal Value ($bn) North America Europe Greater China India Israel Other Source: Preqin Private Equity Online Source: Preqin Private Equity Online Source: Preqin Private Equity Online Fig. 5: Average Value of Venture Capital Deals, 2014 - Fig. 6: Number of US Venture Capital Deals* in Q2 2016 by Fig. 4: Venture Capital Deals* in Q2 2016 by Industry H1 2016 State 35% 120 111 111 31% 30% 96 27% 100 25% 2014 California 80 78 21% 21% 26% 20% 20% 16% 60 2015 New York 15% 13% 13% 44 39 37 Massachusetts 10% 9% 40 30 32 H1 2016 45% 25 Proportion of Total Proportion 5% 23 23 4% 4% Deal Size ($mn) Average 18 18 5% 3% 2% 3% 3% 20 10 12 3% Texas 1% 2% 1% 8 10 1% 1 2 0% 1 4% 0 Washington 8% Other Other Other IT Other Internet Business Services Clean Food & Food Series Series B/ Round 2 Round Round 1 Round Round 3 Round Telecoms Related Series Series A/ Series Series C/ 14% Agriculture Software & Healthcare Consumer Technology Angel/Seed Discretionary Expansion 4 andLater 4 Venture Debt Venture No. -

How to Catch a Unicorn

How to Catch a Unicorn An exploration of the universe of tech companies with high market capitalisation Author: Jean Paul Simon Editor: Marc Bogdanowicz 2016 EUR 27822 EN How to Catch a Unicorn An exploration of the universe of tech companies with high market capitalisation This publication is a Technical report by the Joint Research Centre, the European Commission’s in-house science service. It aims to provide evidence-based scientific support to the European policy-making process. The scientific output expressed does not imply a policy position of the European Commission. Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use which might be made of this publication. JRC Science Hub https://ec.europa.eu/jrc JRC100719 EUR 27822 EN ISBN 978-92-79-57601-0 (PDF) ISSN 1831-9424 (online) doi:10.2791/893975 (online) © European Union, 2016 Reproduction is authorised provided the source is acknowledged. All images © European Union 2016 How to cite: Jean Paul Simon (2016) ‘How to catch a unicorn. An exploration of the universe of tech companies with high market capitalisation’. Institute for Prospective Technological Studies. JRC Technical Report. EUR 27822 EN. doi:10.2791/893975 Table of Contents Preface .............................................................................................................. 2 Abstract ............................................................................................................. 3 Executive Summary .......................................................................................... -

The Social Costs of Uber

Rogers: The Social Costs of Uber The Social Costs of Uber Brishen Rogerst INTRODUCTION The "ride-sharing" company Uber has become remarkably polarizing over the last year. Venture capital firms still love Ub- er's prospects, as reflected in a recent $40 billion valuation.1 Yet the company seems determined to alienate just about everyone else.2 Taxi drivers have cast Uber as an unsafe and rapacious competitor, leading lawmakers to shut it out of various mar- kets.3 Uber's claim that its average New York City driver earns over $90,000 a year was so hard to verify that a Slate writer en- titled her article "In Search of Uber's Unicorn." 4 And in what some have called "Ubergate,"5 a senior executive stated that the company might investigate the personal and family lives of its critics-in particular a female journalist who accused it of disre- garding female passengers' and drivers' safety.6 t Associate Professor of Law, Temple University James E. Beasley School of Law. I'd like to thank the staff of The University of Chicago Law Review for superb edito- rial assistance. Errors are of course mine alone. 1 Mike Isaac and Michael J. De La Merced, Uber Adds a Billion Dollars More to Its Coffers, NY Times Dealbook Blog (NY Times Dec 4, 2014), online at http://dealbook .nytimes.com/2014/12/04/uber-files-to-sell-1-8-billion-in-new-shares (visited Feb 26, 2015). 2 Indeed, one Silicon Valley venture capital chieftain has called the company "ethi- cally challenged." Hailey Lee, Uber Is 'Ethically Challenged'-Peter Thiel (CNBC Sept 17, 2014), online at http://www.enbe.com/id/102008782 (visited Feb 26, 2015). -

Public Investment Memorandum Summit Partners Growth Equity

COMMONWEALTH OF PENNSYLVANIA PUBLIC SCHOOL EMPLOYEES’ RETIREMENT SYSTEM Public Investment Memorandum Summit Partners Growth Equity Fund X, L.P. Private Equity Fund Commitment Darren C. Foreman, CAIA Senior Manager, Private Markets Patrick G. Knapp, CFA Senior Investment Professional, Private Markets December 19, 2018 COMMONWEALTH OF PENNSYLVANIA PUBLIC SCHOOL EMPLOYEES’ RETIREMENT SYSTEM Recommendation: Staff, together with Hamilton Lane Advisors, L.L.C. (“Hamilton Lane”), recommends to the Board a commitment of up to $150 million to Summit Partners Growth Equity Fund X, L.P. (“Summit Growth Equity X” or the “Fund”). Summit Partners, L.P. (“Summit” or the “Firm”) is forming the Fund to continue its long history of investing in U.S. growth equity opportunities which spans nine U.S. growth equity funds with aggregate committed capital of $13.6 billion. Firm Overview: Summit Partners, L.P. is a global alternative investment firm managing investment vehicles focused primarily on growth companies. The Firm was founded in 1984 with a commitment to partner with exceptional entrepreneurs and management teams, providing capital and strategic support to help them achieve their growth objectives. Since inception, Summit has raised and managed more than $22 billion in capital dedicated to growth equity, fixed income, and public equity strategies, including 15 growth equity and venture capital funds with combined committed capital of approximately $17.4 billion and eight fixed income funds with combined committed capital of approximately $4.1 billion. Over the last three decades, Summit has invested in more than 475 companies in technology, healthcare and life sciences, and other growth industries — including more than 430 companies from the U.S. -

GROWTHCAP INSIGHTS 2016 Top 40 Under 40 Growth Investors

GrowthCap 40 Under 40 | November 2016 GROWTHCAP INSIGHTS 2016 Top 40 Under 40 Growth Investors It gives us great pleasure to announce GrowthCap’s 2016 40 Under 40 Growth Investors list. Those appearing in this year’s list were first nominated by their firm, their peers or by GrowthCap. They were then evaluated based on breadth of experience (volume of completed deals, capital invested, number of exits, and realized returns, among other factors) as well as qualitative aspects contributing to their overall effectiveness working with peers, CEOs, LPs and deal professionals. We realized after the publication of our 2014 and 2015 lists, the influence the list can have on LPs evaluating new fund investments or CEOs deciding on prospective capital partners. In particular, the list has been helpful to large family offices in identifying talented investors in the growth equity asset class. The large majority of this year’s nominees provided information on their professional background and investment experience, which played a key role in our selection process and ranking methodology. GrowthCap also conducted interviews with select nominees and in some cases, has had the benefit of direct experience working with nominated individuals and/or represented firms. - RJ Lumba, Managing Partneraaaaa Clockwise from top left: Kapil Venkatachalam (Technology Crossover Ventures), Jason Werlin (TA Associates), Mohamad Makhzoumi (New Enterprise Associates), Chris Adams (Francisco Partners) Page 1 GrowthCap 40 Under 40 | November 2016 Kapil Venkatachalam joined Technology Crossover Ventures in 2006 as an 1 associate and now works as a general partner for the firm. Reflecting on his experience with TCV, Kapil remarks, “Technology is the heart of our business. -

1Q 2019 Relationship Management Purpose-Built for Finance Learn More at Affinity.Co

Co-sponsored by Global League Tables 1Q 2019 Relationship Management Purpose-Built for Finance Learn more at affinity.co IMPROVE ELIMINATE SUPPORT DISCOVER PROPIERTARY CROSSING YOUR NEW EXECUTIVE DEAL FLOW WIRES PORTFOLIO CONNECTIONS Learn why 500+ firms use Affinity's patented technology to leverage their network and increase deal flow “Within weeks of moving “The biggest problems Affinity “Let’s be honest, no one wants to Affinity, we were able to helps me solve are how to to use Salesforce reporting. easily discover and manage track all of my activity and how Affinity isn’t just better for most the 1,000s of entrepreneur to prioritize my time. It makes teams, it’ll make the difference and venture community me a better investor. All of the between managing your relationships already latent things I need to do on a day-to- pipeline to success, versus not within our team." day basis I now do in Affinity.” tracking it at all.” ERIC EMMONS KYLE LUI KEVIN ZHANG Managing Director Partner Principal MassMutual Ventures DCM Ventures Bain Capital Ventures [email protected]@affinity.co AffinityAffinity is a relationship is a relationship intelligence intelligence platform platform built to builtexpand to expandand evolve and theevolve traditional the traditional CRM. AffinityCRM. Affinityinstantly instantly surfaces surfaces all all www.affinity.cowww.affinity.co of yourof team’s your team’sdata to data show to you show who you is bestwho issuited best tosuited make to the make crucial the crucialintroductions introductions you need you to need close to your close next your big next deal. big deal. -

Valuation of Unicorn Companies: the Airbnb Case

DEPARTMENT OF BUSINESS & MANAGEMENT MASTER’S DEGREE IN CORPORATE FINANCE THESIS IN M&A AND INVESTMENT BANKING Valuation of Unicorn Companies: The Airbnb case Supervisor: Co-supervisor: Luigi De Vecchi Leone Pattofatto Author: Luca Inchingolo ID Number: 705781 Academic Year 2019-20 INDEX Figures, charts and tables……………………………………………………………...3 Introduction .................................................................................................................... 5 Chapter 1: The Change .................................................................................................. 7 1.1 IPO’s features and birth of Unicorns .............................................................................. 7 1.2 Who they are? .................................................................................................................. 11 1.3 PIPO ................................................................................................................................. 13 1.3.1 PE’s transaction ........................................................................................................................ 14 1.3.2 PIPO’s role ............................................................................................................................... 16 1.3.3 The Unicorn landscape by country, sector, and valuation ........................................................ 17 1.3.4 Supply and Demand condition underlying the PIPO market and implication of trend ............ 20 Chapter 2: The Unicorn’s overvaluation ................................................................... -

September 29, 2020

Plymouth County Retirement Association September 29, 2020 Meeting Materials BOSTON CHICAGO LONDON MIAMI NEW YORK PORTLAND SAN DIEGO MEKETA.COM Plymouth County Retirement Association Agenda Agenda 1. Estimated Retirement Association Performance As of August 31, 2020 2. Performance Update As of July 31, 2020 3. Current Issues Non-Core Real Estate RFP Respondent Review Non-Core Infrastructure Finalist Presentations 4. Disclaimer, Glossary, and Notes 2 of 129 Estimated Retirement Association Performance As of August 31, 2020 3 of 129 Plymouth County Retirement Association Estimated Retirement Association Performance Estimated Aggregate Performance1 August2 QTD YTD 1 YR 3 YR 5 YR 10 YR (%) (%) (%) (%) (%) (%) (%) Total Retirement Association 2.7 6.3 0.5 7.8 5.0 6.4 7.9 Policy Benchmark 3.1 6.8 3.0 10.1 6.9 7.7 8.5 Benchmark Returns August QTD YTD 1 YR 3 YR 5 YR 10 YR (%) (%) (%) (%) (%) (%) (%) Russell 3000 7.2 13.3 9.4 21.4 14.0 13.9 14.9 MSCI EAFE 5.1 7.6 -4.6 6.4 2.3 4.7 5.9 MSCI Emerging Markets 2.2 11.3 0.5 14.5 2.8 8.7 3.8 Barclays Aggregate -0.8 0.7 6.9 6.5 5.1 4.3 3.7 Barclays TIPS 1.1 3.4 9.6 9.0 5.7 4.6 3.7 Barclays High Yield 1.0 5.7 1.7 4.7 4.9 6.5 6.9 JPM GBI-EM Global Diversified (Local Currency) -0.3 2.7 -4.4 1.7 0.7 4.6 1.3 S&P Global Natural Resources 4.0 7.6 -13.0 -1.9 -0.1 5.6 1.5 Estimated Total Assets Estimate Total Retirement Association $1,106,611,546 1 The August performance estimates are calculated using index returns as of August 31, 2020 for each asset class. -

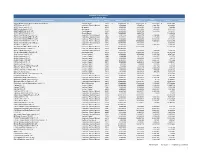

HIERS Performance Report by Investment

Statement of Investments (1) As of June 30, 2017 Total Investment Name Investment Strategy Vintage Committed Paid-In Capital (2) Valuation Net IRR Distributions Abraaj Global Growth Markets Strategic Fund, L.P. Growth Equity 2015 $ 45,000,000 $ 30,442,233 $ 6,226,973 $ 34,191,582 ABRY Partners VII, L.P. Corporate Finance/Buyout 2011 3,500,000 3,569,519 3,861,563 2,239,428 ABRY Senior Equity III, L.P. Mezzanine 2010 5,000,000 4,618,602 7,138,392 322,958 ABRY Senior Equity IV, L.P. Mezzanine 2012 6,503,582 6,227,869 1,900,948 6,205,777 ABS Capital Partners VI, L.P. Growth Equity 2009 4,000,000 3,906,193 1,775,815 1,812,911 ABS Capital Partners VII, L.P. Growth Equity 2012 10,000,000 9,054,134 - 11,860,984 Advent International GPE V-B, L.P. Corporate Finance/Buyout 2012 2,801,236 2,583,570 3,290,856 248,977 Advent International GPE V-D, L.P. Corporate Finance/Buyout 2005 3,179,324 3,038,405 7,175,404 245,538 Advent International GPE VI-A, L.P. Corporate Finance/Buyout 2008 9,500,000 9,500,000 14,172,848 5,876,065 Advent International GPE VII-B, L.P. Corporate Finance/Buyout 2012 30,000,000 27,000,000 11,400,028 32,412,380 Advent International GPE VIII-B, L.P. Corporate Finance/Buyout 2016 36,000,000 8,424,000 - 8,986,703 Alta Partners VIII, L.P.