Legend Ove Chart Line Ad

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

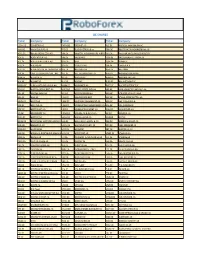

R Trader Instruments Cfds and Stocks

DE SHARES Ticker Company Ticker Company Ticker Company 1COV.DE COVESTRO AG FNTN.DE FREENET AG P1Z.DE PATRIZIA IMMOBILIEN AG AAD.DE AMADEUS FIRE AG FPE.DE FUCHS PETROLUB vz PBB.DE DEUTSCHE PFANDBRIEFBANK AG ACX1.DE BET-AT-HOME.COM AG FRA.DE FRAPORT AG FRANKFURT AIRPORTPFV.DE PFEIFFER VACUUM TECHNOLOGY ADJ.DE ADO PROPERTIES FRE.DE FRESENIUS PSM.DE PROSIEBENSAT.1 MEDIA SE ADL.DE ADLER REAL ESTATE AG G1A.DE GEA PUM.DE PUMA SE ADS.DE ADIDAS AG G24.DE SCOUT24 AG QIA.DE QIAGEN N.V. ADV.DE ADVA OPTICAL NETWORKING SE GBF.DE BILFINGER SE RAA.DE RATIONAL AFX.DE CARL ZEISS MEDITEC AG - BR GFT.DE GFT TECHNOLOGIES SE RHK.DE RHOEN-KLINIKUM AG AIXA.DE AIXTRON SE GIL.DE DMG MORI RHM.DE RHEINMETALL AG ALV.DE ALLIANZ SE GLJ.DE GRENKE RIB1.DE RIB SOFTWARE SE AM3D.DE SLM SOLUTIONS GROUP AG GMM.DE GRAMMER AG RKET.DE ROCKET INTERNET SE AOX.DE ALSTRIA OFFICE REIT-AG GWI1.DE GERRY WEBER INTL AG S92.DE SMA SOLAR TECHNOLOGY AG ARL.DE AAREAL BANK AG GXI.DE GERRESHEIMER AG SAX.DE STROEER SE & CO KGAA BAS.DE BASF SE HAB.DE HAMBORNER REIT SAZ.DE STADA ARZNEIMITTEL AG BAYN.DE BAYER AG HBM.DE HORNBACH BAUMARKT AG SFQ.DE SAF HOLLAND S.A. BC8.DE BECHTLE AG HDD.DE HEIDELBERGER DRUCKMASCHINENSGL.DE SGL CARBON SE BDT.DE BERTRANDT AG HEI.DE HEIDELBERGCEMENT AG SHA.DE SCHAEFFLER AG BEI.DE BEIERSDORF AG HEN3.DE HENKEL AG & CO KGAA SIE.DE SIEMENS AG BIO4.DE BIOTEST AG HLAG.DE HAPAG-LLOYD AG SIX2.DE SIXT SE BMW.DE BAYERISCHE MOTOREN WERKE AGHLE.DE HELLA KGAA HUECK & CO SKB.DE KOENIG & BAUER AG BNR.DE BRENNTAG AG HNR1.DE HANNOVER RUECK SE SPR.DE AXEL SPRINGER SE BOSS.DE HUGO BOSS -

Market Cap Close ADV 1598 67Th Pctl 745,214,477.91 $ 23.96

Market Cap Close ADV 1598 67th Pctl $ 745,214,477.91 $ 23.96 225,966.94 801 33rd Pctl $ 199,581,478.89 $ 10.09 53,054.83 2399 Ticker_ Listing_ Effective_ Revised Symbol Security_Name Exchange Date Mkt Cap Close ADV Stratum Stratum AAC AAC Holdings, Inc. N 20160906 M M M M-M-M M-M-M AAMC Altisource Asset Management Corp A 20160906 L M L L-M-L L-M-L AAN Aarons Inc N 20160906 H H H H-H-H H-H-H AAV Advantage Oil & Gas Ltd N 20160906 H L M H-L-M H-M-M AB Alliance Bernstein Holding L P N 20160906 H M M H-M-M H-M-M ABG Asbury Automotive Group Inc N 20160906 H H H H-H-H H-H-H ABM ABM Industries Inc. N 20160906 H H H H-H-H H-H-H AC Associated Capital Group, Inc. N 20160906 H H L H-H-L H-H-L ACCO ACCO Brand Corp. N 20160906 H L H H-L-H H-L-H ACU Acme United A 20160906 L M L L-M-L L-M-L ACY AeroCentury Corp A 20160906 L L L L-L-L L-L-L ADK Adcare Health System A 20160906 L L L L-L-L L-L-L ADPT Adeptus Health Inc. N 20160906 M H H M-H-H M-H-H AE Adams Res Energy Inc A 20160906 L H L L-H-L L-H-L AEL American Equity Inv Life Hldg Co N 20160906 H M H H-M-H H-M-H AF Astoria Financial Corporation N 20160906 H M H H-M-H H-M-H AGM Fed Agricul Mtg Clc Non Voting N 20160906 M H M M-H-M M-H-M AGM A Fed Agricultural Mtg Cla Voting N 20160906 L H L L-H-L L-H-L AGRO Adecoagro S A N 20160906 H L H H-L-H H-L-H AGX Argan Inc N 20160906 M H M M-H-M M-H-M AHC A H Belo Corp N 20160906 L L L L-L-L L-L-L AHL ASPEN Insurance Holding Limited N 20160906 H H H H-H-H H-H-H AHS AMN Healthcare Services Inc. -

2019 Was a Fantastic Year for Our Company, Thanks to the Hard Work of Our Talented Teams, Who Achieved Incredible Accomplishments and Milestones

YEAR IN REVIEW 2019 was a fantastic year for our company, thanks to the hard work of our talented teams, who achieved incredible accomplishments and milestones. We are proud of all of our successes in 2019, and thrilled to share some of the highlights with you here. January Xfinity Internet: Comcast launches Xfinity xFi Advanced Security to protect WiFi-connected devices in the home Sky: Sky Ocean Rescue and World Wildlife Fund launch a renewed campaign to encourage people to reduce their plastic usage Xfinity Internet: Comcast announces partnership with Xfinity xFi Advanced Security monitors, blocks Intel to deliver faster speeds, more capacity and responsive and informs customers of online threats and networks for broadband customers provides seamless protection in the home. Fusion Arena, a first-of-its-kind venue, will serve as a premier destination for competitive gaming events, as well as a variety of live entertainment programming and experiences. February Corporate: Comcast NBCUniversal is named #3 on Fortune’s ‘Best Big Companies to Work For’ list Comcast Ventures: Comcast Ventures invests in Dandelion Energy, which offers modern, cost-effective geothermal heating and cooling systems to homeowners March Film: Universal’s Green Book wins Academy Award for Best Picture Xfinity: Comcast launches Xfinity Flex streaming platform for Xfinity Internet-only Sports: NBC Sports Group partners customers with Rory McIlroy to create GolfPass Digital Membership Experience Corporate: Comcast acquires BluVector, a developer of AI-powered cybersecurity -

Corporate Venturing Report 2019

Tilburg University 2019 Corporate Venturing Report Eckblad, Joshua; Gutmann, Tobias; Lindener, Christian Publication date: 2019 Document Version Publisher's PDF, also known as Version of record Link to publication in Tilburg University Research Portal Citation for published version (APA): Eckblad, J., Gutmann, T., & Lindener, C. (2019). 2019 Corporate Venturing Report. Corporate Venturing Research Group, TiSEM, Tilburg University. General rights Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of accessing publications that users recognise and abide by the legal requirements associated with these rights. • Users may download and print one copy of any publication from the public portal for the purpose of private study or research. • You may not further distribute the material or use it for any profit-making activity or commercial gain • You may freely distribute the URL identifying the publication in the public portal Take down policy If you believe that this document breaches copyright please contact us providing details, and we will remove access to the work immediately and investigate your claim. Download date: 24. sep. 2021 Corporate Venturing 2019 Report SUMMIT@RSM All Rights Reserved. Copyright © 2019. Created by Joshua Eckblad, Academic Researcher at TiSEM in The Netherlands. 2 TABLE OF CONTENTS LEAD AUTHORS 03 Forewords Joshua G. Eckblad 06 All Investors In External Startups [email protected] 21 Corporate VC Investors https://www.corporateventuringresearch.org/ 38 Accelerator Investors CentER PhD Candidate, Department of Management 43 2018 Global Startup Fundraising Survey (Our Results) Tilburg School of Economics and Management (TiSEM) Tilburg University, The Netherlands 56 2019 Global Startup Fundraising Survey (Please Distribute) Dr. -

Market Cap Close ADV

Market Cap Close ADV 1598 67th Pctl $745,214,477.91 $23.96 225,966.94 801 33rd Pctl $199,581,478.89 $10.09 53,054.83 2399 Listing_ Revised Ticker_Symbol Security_Name Exchange Effective_Date Mkt Cap Close ADV Stratum Stratum AAC AAC Holdings, Inc. N 20160906 M M M M-M-M M-M-M Altisource Asset Management AAMC Corp A 20160906 L M L L-M-L L-M-L AAN Aarons Inc N 20160906 H H H H-H-H H-H-H AAV Advantage Oil & Gas Ltd N 20160906 H L M H-L-M H-M-M AB Alliance Bernstein Holding L P N 20160906 H M M H-M-M H-M-M ABG Asbury Automotive Group Inc N 20160906 H H H H-H-H H-H-H ABM ABM Industries Inc. N 20160906 H H H H-H-H H-H-H AC Associated Capital Group, Inc. N 20160906 H H L H-H-L H-H-L ACCO ACCO Brand Corp. N 20160906 H L H H-L-H H-L-H ACU Acme United A 20160906 L M L L-M-L L-M-L ACY AeroCentury Corp A 20160906 L L L L-L-L L-L-L ADK Adcare Health System A 20160906 L L L L-L-L L-L-L ADPT Adeptus Health Inc. N 20160906 M H H M-H-H M-H-H AE Adams Res Energy Inc A 20160906 L H L L-H-L L-H-L American Equity Inv Life Hldg AEL Co N 20160906 H M H H-M-H H-M-H AF Astoria Financial Corporation N 20160906 H M H H-M-H H-M-H AGM Fed Agricul Mtg Clc Non Voting N 20160906 M H M M-H-M M-H-M AGM A Fed Agricultural Mtg Cla Voting N 20160906 L H L L-H-L L-H-L AGRO Adecoagro S A N 20160906 H L H H-L-H H-L-H AGX Argan Inc N 20160906 M H M M-H-M M-H-M AHC A H Belo Corp N 20160906 L L L L-L-L L-L-L ASPEN Insurance Holding AHL Limited N 20160906 H H H H-H-H H-H-H AHS AMN Healthcare Services Inc. -

Downloading of Movies, Television Shows and Other Video Programming, Some of Which Charge a Nominal Or No Fee for Access

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2011 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO Commission file number 001-32871 COMCAST CORPORATION (Exact name of registrant as specified in its charter) PENNSYLVANIA 27-0000798 (State or other jurisdiction of (I.R.S. Employer Identification No.) incorporation or organization) One Comcast Center, Philadelphia, PA 19103-2838 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code: (215) 286-1700 SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: Title of Each Class Name of Each Exchange on which Registered Class A Common Stock, $0.01 par value NASDAQ Global Select Market Class A Special Common Stock, $0.01 par value NASDAQ Global Select Market 2.0% Exchangeable Subordinated Debentures due 2029 New York Stock Exchange 5.50% Notes due 2029 New York Stock Exchange 6.625% Notes due 2056 New York Stock Exchange 7.00% Notes due 2055 New York Stock Exchange 8.375% Guaranteed Notes due 2013 New York Stock Exchange 9.455% Guaranteed Notes due 2022 New York Stock Exchange SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. -

September 2014 M&A and Investment Summary

September 2014 M&A and Investment Summary Expertise. Commitment. Results. Table of Contents 1 Overview of Monthly M&A and Investment Activity 3 2 Monthly M&A and Investment Activity by Industry Segment 9 3 Additional Monthly M&A and Investment Activity Data 42 4 About Petsky Prunier 57 Securities offered through Petsky Prunier Securities, LLC, member of FINRA. This M&A and Investment Summary has been prepared by and is being distributed in the United States by Petsky Prunier, a broker dealer register with the U.S. SEC and a member of FINRA. Petsky Prunier is not affiliated with Altium Capital Ltd, but has partnered with Altium to expand its international presence. Altium has not prepared or verified the information in this Summary. Persons in the United States should contact Petsky Prunier for further information or services. This M&A and Investment Summary is not being distributed by Altium Capital Ltd in the United States and Altium Capital Ltd is not offering any services to persons in the United States. 2| M&A and Investment Summary September 2014 M&A and Investment Summary for All Segments Transaction Distribution . A total of 428 deals were announced in September 2014, of which 236 were worth $37.5 billion in aggregate reported value . Software was the most active and highest reported value segment with 92 deals announced, of which 46 were reported at $13.5 billion in aggregate value . Digital Media/Commerce was another active segment with 85 transactions that were worth $4.5 billion . Strategic buyers announced 197 deals (46 percent of total volume), of which 40 were worth $24.9 billion in aggregate value . -

Hamilton Lane Incorporated Nps 2021 V3

110 Washington Street Suite 1300 Conshohocken, PA 19428 Telephone: (610) 934-2222 July 22, 2021 Fellow Stockholders: You are cordially invited to attend our 2021 Annual Meeting of Stockholders, which will be held via live audio webcast on Thursday, September 2, 2021 at 9:30 a.m. (Eastern Time). All Hamilton Lane Incorporated stockholders of record at the close of business on July 7, 2021 are welcome to attend the Annual Meeting, but it is important that your shares are represented at the Annual Meeting whether or not you plan to attend. To ensure that you will be represented, we ask you to vote by telephone, mail or over the Internet. Hamilton Lane continues to monitor public health and safety concerns related to the coronavirus (“COVID-19”) pandemic and the various measures being implemented to reduce its impact, including recommendations and protocols issued by public health authorities and federal, state, and local governments. In light of these concerns and to support the health and well-being of our employees and stockholders, the Annual Meeting will be a virtual meeting of stockholders conducted via live audio webcast. You will be able to attend and participate in the Annual Meeting online by visiting www.virtualshareholdermeeting.com/ HLNE2021 at the meeting date and time described above and in the accompanying proxy statement and by entering the 16-digit control number that appears on your Notice of Internet Availability of Proxy Materials or, if you received a paper copy of the proxy materials, your proxy card (printed in the box and marked by the arrow) or the instructions that accompanied your proxy materials. -

Payments / Banking

Financial Technology Sector Summary June 24, 2015 Financial Technology Sector Summary Table of Contents I. GCA Savvian Overview II. Market Summary III. Payments / Banking IV. Securities / Capital Markets / Data & Analytics V. Healthcare / Insurance I. GCA Savvian Overview GCA Savvian Overview Highlights Firm Statistics GCA Savvian Focus . Over 225 professionals today Mergers & Acquisitions Private Capital Markets . Full spectrum of buy-side, sell- Agented private capital raiser Headquarters in San Francisco and Tokyo; offices in New side and strategic advisory York, London, Shanghai, Mumbai, Singapore, and Osaka . Equity and debt capital markets . Public and private company advisory services experience . Provides mergers and acquisitions advisory services, private . Core competency, with important capital & capital markets advisory services, and principal . Strategic early-stage growth relationships among the venture investing companies through industry capital and private equity defining, multi-billion dollar community transactions . Over 550 transactions completed . Publicly traded on the Tokyo Stock Exchange (2174) Senior level attention and focus, Relationships and market extensive transaction intelligence; a highly experienced team in experience and deep domain insight the industry Global Advisory Firm Market Positioning Bulge Bracket Growth Sector Focus Transaction Expertise . Senior Team with . Growth Company Focus Unparalleled Transaction . Sector Expertise / Domain Experience Knowledge . Highest Quality Client . Private Capital -

Deloitte's Technology Fast

Deloitte’s 2015 Technology Fast 500™ Powerful connections @DeloitteTMT #Fast500 ANNUAL RANKING OF THE FASTEST GROWING TECHNOLOGY COMPANIES IN NORTH AMERICA About Deloitte’s Technology Fast 500 About Deloitte’s Technology Fast 500 The Technology Fast 500 is the leading technology awards program in North America (U.S. and Canada) with 2015 being its twenty-first year. Combining technological innovation, entrepreneurship and rapid growth, Fast 500 companies — large, small, public, and private — span a variety of industry sectors. These companies are on the cutting edge and are transforming the way we do business today. Selection and qualifying criteria The Technology Fast 500 provides a ranking of the fastest growing technology, media, telecommunications, life sciences and energy tech companies — both public and private — in North America (U.S. and Canada). Technology Fast 500 award winners for 2015 are selected based on percentage fiscal year revenue growth during the period from 2011 to 2014. In order to be eligible for Technology Fast 500 recognition, companies must own proprietary intellectual property or technology that is sold to customers in products that contribute to a majority of the company’s operating revenues. Companies must have base-year (2011) operating revenues of at least $50,000 USD or CD, and current-year (2014) operating revenues of at least $5 million USD or CD. Additionally, companies must be in business for a minimum of four years, and be headquartered within North America. This ranking is compiled from applications submitted directly to the Technology Fast 500 Web site, and public company database research conducted by Deloitte LLP. -

Weekly Internet / Digital Media / Saas Sector Summary

Weekly Internet / Digital Media / SaaS Sector Summary Week of July 14th, 2014 Industry Stock Market Valuation Internet / Digital Media / SaaS Last 12 Months Last 3 Months 180 120 14.6% 160 11.9% 60.8% 10.4% 10.4% 110 7.9% 140 22.3% 7.7% 21.0% 6.6% 20.4% 5.9% 120 20.0% 5.1% 16.3% 100 13.9% 100 13.0% 10.8% 80 90 7/12/13 9/23/13 12/5/13 2/16/14 4/30/14 7/12/14 4/11/14 5/4/14 5/27/14 6/19/14 7/12/14 (1) (2) (3) (4) Search / Online Advertising Internet Commerce Internet Content Publishers (5) (6) (7) (8) NASDAQ Diversified Marketing Media Conglomerates Gaming SaaS Notes: 1) Search/Online Advertising Composite includes: BCOR, BLNX-GB, CNVR, CRTO, GOOG, FUEL, MCHX, MM, MRIN, MSFT, QNST, RLOC, RUBI, TRMR, TWTR, YHOO, YNDX, YUME. 2) Internet Commerce Composite includes: AMZN, AWAY, COUP, CPRT, DRIV, EBAY, EXPE, FLWS, LINTA, NFLX, NILE, OPEN, OSTK, PCLN, PRSS, SSTK, STMP, TZOO, VPRT, ZU. 3) Internet Content Composite includes: AOL, CRCM, DHX, DMD, EHTH, IACI, MOVE, MWW, RATE, RENN, RNWK, SCOR, SFLY, TRLA, TST, TTGT, UNTD, WBMD, WWWW, XOXO, Z. 4) Publishers Composite includes: GCI, MMB-FR, NWSA, NYT, PSON-GB, SSP, TRI, UBM-GB, WPO. 5) Diversified Marketing Composite includes: ACXM, EFX, EXPN-GB, HAV-FR, HHS, IPG, MDCA, NLSN, VCI, WPP-GB. 6) Media Conglomerates Composite includes: CBS, CMCSA, DIS, DISCA, LGF, SNE, TWX, VIA.B. 7) Gaming Composite includes: 2432-JP, 3632-JP, 3765-JP, 700-HK, ATVI, CYOU, EA, GA, GAME, GLUU, NTES, PWRD, UBI-FR, ZNGA. -

FT PARTNERS RESEARCH 2 Fintech Meets Alternative Investments

FT PARTNERS FINTECH INDUSTRY RESEARCH Alternative Investments FinTech Meets Alternative Investments Innovation in a Burgeoning Asset Class March 2020 DRAFT ©2020 FinTech Meets Alternative Investments Alternative Investments FT Partners | Focused Exclusively on FinTech FT Partners’ Advisory Capabilities FT Partners’ FinTech Industry Research Private Capital Debt & Raising Equity Sell-Side / In-Depth Industry Capital Buy-Side Markets M&A Research Reports Advisory Capital Strategic Structuring / Consortium Efficiency Proprietary FinTech Building Advisory FT Services FINTECH Infographics Partners RESEARCH & Board of INSIGHTS Anti-Raid Advisory Directors / Advisory / Monthly FinTech Special Shareholder Committee Rights Plans Market Analysis Advisory Sell-Side Valuations / LBO Fairness FinTech M&A / Financing Advisory Opinion for M&A Restructuring Transaction Profiles and Divestitures Named Silicon Valley’s #1 FinTech Banker Ranked #1 Most Influential Person in all of Numerous Awards for Transaction (2016) and ranked #2 Overall by The FinTech in Institutional Investors “FinTech Excellence including Information Finance 40” “Deal of the Decade” • Financial Technology Partners ("FT Partners") was founded in 2001 and is the only investment banking firm focused exclusively on FinTech • FT Partners regularly publishes research highlighting the most important transactions, trends and insights impacting the global Financial Technology landscape. Our unique insight into FinTech is a direct result of executing hundreds of transactions in the sector combined with over 18 years of exclusive focus on Financial Technology FT PARTNERS RESEARCH 2 FinTech Meets Alternative Investments I. Executive Summary 5 II. Industry Overview and The Rise of Alternative Investments 8 i. An Introduction to Alternative Investments 9 ii. Trends Within the Alternative Investment Industry 23 III. Executive Interviews 53 IV.