TA Securities FBMKLCI: 1 ,806.09 a Member of the TA Group

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Table of Contents

TABLE OF CONTENTS PAGE Introduction ANANDA KRISHNAN PROFILE AND BACKGROUND 3 - 8 MAXIS COMMUNICATION COMPANY PROFILE 9 - 12 ASTRO COMPANY PROFILE 13 - 20 STYLE OF LEADERSHIP 21 - 24 LEADERSHIP THEORY ADAPTATION 25 Conclusion 26 References 27 1 (a) Background of the leader: the aim of this section is to know and understand the leader as a person and the bases for his/her success. The data and information should be taken from any published sources such as newspapers, company reports, magazines, journals, books etc. INTRODUCTION ANANDA KRISHNAN Who is Ananda Krishnan? According to a report then by Bernama News Agency, the grandfathers of Tan Sri T. Ananda Krishnan and Tan Sri G. Gnanalingam had been brought to Malaysia from Jaffna by British colonial rulers to work in Malaysia¶s Public Works Department, a common practice then as Jaffna produced some of the most educated people in the whole country. Tan Sri Gnanalingam himself told one of our ministers that he wants to put something back into this country because his grandfather was Sri Lankan," Deputy Director-General of Sri Lanka's Board of Investment (BOI) Santhusht Jayasuriya had told a a group of visiting Malaysian journalists then, 2 according to the Bernama 2003 story. Gnanalingam, executive chairman of Malaysia's Westport, held talks with Prime Minister Ranil Wickremesinghe during a visit to Malaysia in 2003 and the former followed up with a visit to Colombo. In the same year a Memorandum of Understanding was formalized in March this year between 'Westport' and the Sri Lanka Ports Authority (SLPA). Westport is keen to invest in Sri Lanka but no formal process has begun. -

M.V. Solita's Passage Notes

M.V. SOLITA’S PASSAGE NOTES SABAH BORNEO, MALAYSIA Updated August 2014 1 CONTENTS General comments Visas 4 Access to overseas funds 4 Phone and Internet 4 Weather 5 Navigation 5 Geographical Observations 6 Flags 10 Town information Kota Kinabalu 11 Sandakan 22 Tawau 25 Kudat 27 Labuan 31 Sabah Rivers Kinabatangan 34 Klias 37 Tadian 39 Pura Pura 40 Maraup 41 Anchorages 42 2 Sabah is one of the 13 Malaysian states and with Sarawak, lies on the northern side of the island of Borneo, between the Sulu and South China Seas. Sabah and Sarawak cover the northern coast of the island. The lower two‐thirds of Borneo is Kalimantan, which belongs to Indonesia. The area has a fascinating history, and probably because it is on one of the main trade routes through South East Asia, Borneo has had many masters. Sabah and Sarawak were incorporated into the Federation of Malaysia in 1963 and Malaysia is now regarded a safe and orderly Islamic country. Sabah has a diverse ethnic population of just over 3 million people with 32 recognised ethnic groups. The largest of these is the Malays (these include the many different cultural groups that originally existed in their own homeland within Sabah), Chinese and “non‐official immigrants” (mainly Filipino and Indonesian). In recent centuries piracy was common here, but it is now generally considered relatively safe for cruising. However, the nearby islands of Southern Philippines have had some problems with militant fundamentalist Muslim groups – there have been riots and violence on Mindanao and the Tawi Tawi Islands and isolated episodes of kidnapping of people from Sabah in the past 10 years or so. -

Property Market 2013

Property Market 2013 www.wtw.com.my C H Williams Talhar and Wong 30.01, 30th Floor, Menara Multi-Purpose@CapSquare, 8 Jalan Munshi Abdullah, 51000 Kuala Lumpur Tel: 03-2616 8888 Fax: 03-2616 8899 KDN No. PP013/07/2012 (030726) Property Market 2013 www.wtw.com.my C H Williams Talhar and Wong 30.01, 30th Floor, Menara Multi-Purpose@CapSquare, 8 Jalan Munshi Abdullah, 51000 Kuala Lumpur Tel: 03-2616 8888 Fax: 03-2616 8899 KDN No. PP013/07/2012 (030726) CH Williams Talhar & Wong established in 1960, is a leading real estate services company in Malaysia & Brunei (headquartered in Kuala Lumpur) operating with 25 branches and associated offices. HISTORY Colin Harold Williams established C H Williams & Co, Chartered Surveyor, Valuer and Estate Agent in 1960 in Kuala Lumpur. In 1974, the company merged with Talhar & Co, a Johor-base Chartered Surveying and Valuation company under the sole-proprietorship of Mohd Talhar Abdul Rahman. With the inclusion of Wong Choon Kee, in a 3-way equal partnership arrangement, C H Williams Talhar and Wong was founded. PRESENT MANAGEMENT The Group is headed by Chairman, Mohd Talhar Abdul Rahman who guides the group on policy de- velopments and identifies key marketing strategies which have been instrumental in maintaining the strong competitive edge of WTW. The current Managing Directors of the WTW Group operations are: C H Williams Talhar & Wong Sdn Bhd Foo Gee Jen C H Williams Talhar & Wong (Sabah) Sdn Bhd Robin Chung York Bin C H Williams Talhar Wong & Yeo Sdn Bhd (operating in Sarawak) Robert Ting Kang Sung -

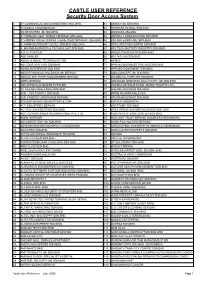

CASTLE USER REFERENCE Security Door Access System

CASTLE USER REFERENCE Security Door Access System 1 2Y COMMUNICATION ENGINEERING SND. BHD. 61 AMWAY (M) SDN.BHD. 2 38 BIDARA CONDOMINIUM 62 ANGKASA GLOBAL SDN.BHD. 3 3D NETWORKS (M) SDN.BHD. 63 ANGSANA ANJUNG 4 A ‘FARMOSA GOLF RESORT BERHAD (MELAKA) 64 ANTARA CONSOLIDATION SDN BHD 5 A ’FAMOSA WATER WORLD THEME PARK SDN.BHD. (MELAKA) 65 ANTARA EKSKLUSIF SDN.BHD. 6 A ’FARMOSA RESORT HOTEL SDN BHD (MELAKA) 66 APAC AUCTION CENTRE SDN BHD 7 A. MAXIMA BUSINESS & TECHNOLOGY SDN BHD 67 APL TECH BATTERY INDUSTRY SDN BHD 8 A.G.V.I.S GROUP 68 APLEX CORPORATION SDN BHD 9 ABB DAIMLER 69 APL-NOL (M) SDN BHD 10 ABDUL & ABDUL TECHNOLOGY S/B 70 APMCE 11 ABI CONSTRUCTION SDN.BHD. 71 APPLIED BUSINESS SYSTEMS SDN BHD. 12 ABIMA ENTERPRISE SDN BHD 72 APPLIED EQUIPMENT (PENANG) 13 ABRAR FINANCIAL HOLDINGS (M) BERHAD 73 AQM CONCEPT (M) SDN.BHD. 14 ABRAR UNIT TRUST MANAGEMENT BERHAD 74 AR DENTAL SUPPLIES SDN.BHD. 15 ABRIC BERHAD 75 ARCADIAN WIRELESS ASIA PACIFIC (M) SDN.BHD. 16 ABS APPLIED BUSINESS SYSTEMS 76 AREMAC INTERNATIONAL MARKETING PTE LTD 17 AC NEILSEN (MALAYSIA) SDN BHD 77 ARENSI HOLDINGS SDN BHD 18 ACE – TEX PLASTIC SND.BHD. 78 ARKIB NEGARA MALAYSIA 19 ACE SYNERGY INSURANCE BERHAD 79 AROSA BUILDINGS SDN BHD 20 ACM NETWORKS ADVERTISING & COM 80 ARTHUR ANDERSON 21 ACP INDUSTRIES BERHAD 81 ARTSTAMP SDN BHD 22 AC-TECH ENGINEERING SDN BHD 82 ASEA BROWN BOVORI HOLDINGS SDN. BHD. 23 ADC TECHNOLOGIES INTERNATIONAL PTE. LTD. 83 ASIA PACIFIC ZONE SYSTEM SDN.BHD. 24 ADEM INTERIOR 84 ASIA UNIT TRUST BERHAD.(KOMPLEKS KEWANGAN) 25 ADVANTEST-ENG (M) SDN BHD 85 ASIAN PAC HOLDING BERHAD 26 ADVERTISING DESIGN IMPACT CHALENGGER 86 ASSOCIATED LOCKSMITH OF AMERICA (SEREMBAN) 27 ADWORKS SDN BHD 87 ASSOCIATED PROPERTY SDN.BHD. -

Malaysia Real Estate Highlights

RESEARCH REAL ESTATE HIGHLIGHTS 1ST HALF 2016 KUALA LUMPUR PENANG JOHOR BAHRU KOTA KINABALU HIGHLIGHTS KUALA LUMPUR HIGH END CONDOMINIUM MARKET The residential market continues to remain lacklustre with lower volume and value of transactions recorded. ECONOMIC AND MARKET INDICATORS Limited project completions and new Malaysia’s economy expanded at a launches of high end condominiums / slower pace in 2015 with Gross Domestic residences during the review period. Product (GDP) growing at an annual rate of 5.0% (2014: 6.0%). For 2016, the Government has trimmed the country’s Growing pressure on rentals amid GDP growth forecast to 4 - 4.5% due to strong supply pipeline (existing and the volatility in crude oil prices and other new completions) and a challenging economic challenges. GDP continued rental market while prices in to moderate in the first quarter of 2016, the secondary market generally posting 4.2% growth, its slowest since continue to remain resilient. 3Q2009 (4Q2015: 4.5%), driven by domestic demand. Private consumption expanded by 5.3% while private Developers adopt innovative ‘push investment moderated to 2.2%. marketing’ strategies to boost Headline inflation for April 2016 registered at sales of selected projects and 2.1%. It is expected to be lower at 2% to 3% improve revenue. this year, compared to an earlier projection Aria of 2.5% to 3.5% and will continue to remain stable in 2017. (432 units) and The Residences at The Meanwhile, labour market conditions St. Regis Kuala Lumpur (160 units). continued to weaken with more retrenchment of workers, particularly in By the second half of 2016, the scheduled the manufacturing, mining and services completions of another five projects will sectors. -

Annual Report 2017 Group Highlights 2017

ANNUAL REPORT 2017 GROUP HIGHLIGHTS 2017 1. SALES 4. SHAREHOLDERS FUND 7. PROFIT ATTRIBUTABLE TO RM4.92 billion RM11.94 BILLION OWNERS OF THE COMPANY RM933 million 2. REVENUE 5. EARNINGS PER SHARE 8. ENLARGED LAND BANKS RM4.52 billion 26.77 Sen 9,606 acres 3. PROFIT BEFORE TAX 6. DIVIDEND PER SHARE 9. STRONG GDV IN THE PIPELINE RM1.27 billion 15.5 sen RM128.37 billion 10. ON-GOING PROJECTS 44 projects TOTAL SALES 11. UNBILLED SALES ACHIEVED RM7.72 billion FOR FY2017 IS 12. TOTAL STRONG DYNAMIC & DIVERSIFIED EMPLOYEES RM4.92 BILLION 2,300 people COVER RATIONALE At S P Setia, the sky is not the limit. In fact, we believe that the future is limitless. Opened to the possibilities of tomorrow, we embarked on a journey of strengthening growth, anchored by the dynamic and highly-talented Team Setia and our wide range of products. Guided by our ethos, we worked together, embraced change and demonstrated our resilience in the face of challenges while at the same time, boosting our capabilities today to fortify tomorrow’s opportunities. We will continue to reinforce our strong foundations, define our path forward to build a meaningful, sustainable future, for us and for our stakeholders. CONTENT OUR BUSINESS OUR LEADERSHIP AND PEOPLE Vision, Mission & Values 3 Board of Directors 36 Corporate Profile 4 Directors’ Profiles 38 Global Presence 6 Senior Management Team Profiles 48 Corporate Structure 8 Corporate Information 11 OUR ACHIEVEMENTS AND ACCOLADES Achievements 54 OUR PERFORMANCE REVIEW Accolades 60 Chairman’s Message 12 Management Discussion -

Kuala Lumpur Office

Asian Cities Report – 2H 2019 REPORT Savills Research Kuala Lumpur Offi ce Kuala Lumpur Offi ce Strong interest in quality offi ce space is being led by the expansion of fl exible space operators NEW SUPPLY GRAPH 1: Greater KL Offi ce Stock, 2010 to 1H/2019 Stock of offi ce space in Greater KL, the single largest offi ce market in ASEAN, stands at approximately 126 million sq ft, with the completion of four new offi ce buildings KL City The Rest of Greater KL Greater KL contributing 1.08 million sq ft in 1H/2019. 140 125.3 126.4 The fi rst offi ce tower within the Tun Razak Exchange, namely Menara Prudential, 120.4 115.4 was completed this year and serves as the headquarters for Prudential Assurance 120 111.5 105.4 Malaysia Bhd. The KYM Tower in Mutiara Damansara and Symphony Square in 102.2 97.9 Petaling Jaya were also completed in early 2019. With the exception of the EkoCheras 100 91.5 86.7 Offi ce Suites, the other three new buildings are single-owned en-bloc buildings, built with quality features and modern specifi cations. 80 By the end of 2019, the stock of offi ce space is expected to expand by 3.8 million sq 60 ft, touching approximately 130 million sq ft – with the completion of Southeast Asia’s tallest building, The Exchange 106, which will replace the Petronas Twin Towers as MILLION SQ FT 40 the tallest building in the country. This landmark offi ce tower, located within the Tun Razak Exchange (TRX), stands at 492m tall, off ering 2.4 million sq ft of column- 20 free offi ce space with spacious fl oor plates ranging from 22,000 to 34,000 sq ft. -

Malaysia Real Estate Highlights

RESEARCH REAL ESTATE HIGHLIGHTS 1ST HALF 2015 KUALA LUMPUR PENANG JOHOR BAHRU KOTA KINABALU KUALA LUMPUR HIGH END CONDOMINIUM MARKET (MPC) meeting in May in an effort to support economic growth and domestic HIGHLIGHTS consumption. • Softening demand in the SUPPLY & DEMAND high-end condominium With the completion of seven notable segment amid a cautious projects contributing an additional market. 1,296 units [includes projects that are physically completed but pending Madge Mansions issuance of Certificate of Completion • Lower volume of transactions and Compliance (CCC)], the cumulative expected to come on-stream. The KL in 1Q2015. supply of high end condominiums in City locality will account for circa 35% Kuala Lumpur stands at 39,610 units. (1,310 units) of the new supply; followed • Developers with niche high by Mont’ Kiara / Sri Hartamas with Approximately 45% (582 units) of the new 34% (1,256 units); KL Sentral / Pantai / end residential projects in KL completions are located in the Ampang Damansara Heights with 20% (734 units); City review products, pricing Hilir / U-Thant area, followed by some and the remaining 11% (425 units) from and marketing strategies in 26% (335 units) in the locality of KL City; the locality of Ampang Hilir / U-Thant. a challenging market with 16% (204 units) from the locality of KL lacklustre demand, impacted Sentral / Pantai / Damansara Heights Notable projects slated for completion by a general slowdown in the area; and 14% (175 units) from the Mont’ in KL City include Face Platinum Suites, economy, tight lending Kiara / Sri Hartamas locality. Le Nouvel, Mirage Residences as well as guidelines, weaker job market the delayed project of Crest Jalan Sultan The three completions in Ampang Hilir amongst other reasons. -

The Financial Year 2012 Was, Without Doubt, Another Challenging Period for Tenaga Nasional Berhad (Tnb)

KEEPING THE LIGHTS ON YOU SEE Tenaga Nasional Berhad www.tnb.com.my No. 129, Jalan Bangsar, 59200 Kuala Lumpur Tel: 603 2180 4582 Fax: 603 2180 4589 Email: [email protected] Annual Report Annual 2012 Tenaga Nasional Berhad Tenaga 200866-W annual report 2012 WE SEE... OUR COMMITMENT TO THE NATION >OH[ `V\ ZLL PZ Q\Z[ VUL ZTHSS WPLJL VM [OL IPN WPJ[\YL 6\Y YVSL PZ [V WYV]PKL TPSSPVUZ VM 4HSH`ZPHUZ ^P[O HMMVYKHISL YLSPHISL LMMPJPLU[ HUK \UPU[LYY\W[LK HJJLZZ [V LSLJ[YPJP[` -YVT WV^LYPUN [OL UH[PVU»Z HKTPUPZ[YH[P]L JHWP[HS [V SPNO[PUN \W OV\ZLOVSKZ HUK LTWV^LYPUN HSS ZLJ[VYZ VM [OL LJVUVT` ^L OH]L OLSWLK YHPZL [OL X\HSP[` VM SPML PU [OL JV\U[Y` HUK ZW\Y [OL UH[PVU»Z WYVNYLZZ V]LY [OL `LHYZ 4VYL [OHU Q\Z[ SPNO[PUN \W OVTLZ HUK Z[YLL[Z ;5) PZ JVTTP[[LK [V LUZ\YPUN [OH[ L]LY` 4HSH`ZPHU PZ HISL [V LUQV` [OL ILULMP[Z VM LSLJ[YPJP[` LHJO HUK L]LY` KH` VM [OL `LHY I` RLLWPUN [OL SPNO[Z VU KEEPING THE LIGHTS ON INSIDEwhat’s TO BE AMONG THE LEADING VISION CORPORATIONS IN ENERGY AND RELATED BUSINESSES 4 Notice of the 22nd Annual General Meeting 7 Appendix I 9 Statement Accompanying Notice GLOBALLY of the 22nd Annual General Meeting 10 Financial Calendar 11 Investor Relations 14 Share Performance WE ARE 15 Facts at a Glance 16 Chairman’s Letter to Shareholders COMMITTED TO 22 President/CEO’s Review 33 Key Highlights 34 Key Financial Highlights EXCELLENCE 35 Five-Year Group Financial Summary MISSION IN OUR 36 Five-Year Group Growth Summary PRODUCTS AND SERVICES KEEPING THE LIGHTS ON Corporate Framework Operations Review 40 About Us 135 Core Businesses 42 Corporate Information 136 Generation 1 44 Group Corporate Structure 142 Transmission 5 46 Organisational Structure 146 Distribution 47 Awards & Recognition 153 Non-Core Businesses 51 Key Past Awards 154 New Business & Major Projects 54 Media Highlights 160 Group Finance 56 Calendar of Events 163 Planning 62 Milestones Over 60 Years 168 Corporate Affairs & Services 175 Procurement Performance Review Other Services 179 Sabah Electricity Sdn. -

Webinars Launched Newsletter Of

Webinars Launched Newsletter of “The Mapping Guru” Unearth A Masterpiece. EDITION Number 13 V16.7sp2 RELEASED THIS ARTICLE HIGHLIGHTS SOME OF THE KEY FEATURES OF THE RECENTLY RELEASED V16.7SP2. Petrosys has introduced webinars to the range of events available to new and existing users. pg 2 The webinars are a free and easy way to get insight, information and demonstrations of Petrosys products and workflows. PETROSYS ASIA EXPANSION READ ABOUT THE EXCITING CHANGES TAKING Learn from Petrosys Mapping Gurus at your PLACE IN OUR KUALA LUMPUR OFFICE, AND desk, listen to software tips and tricks, learn CATCH UP ON GENERAL EVENTS IN THE REGION. about new features, get started with our products and more. Upcoming webinars are: pg 3 The Petrosys plug-in for Petrel - Integrated Workflows CHECKSHOT NOW IN WDF Presenter: Nathan Balls WE EXPLAIN WHAT A CHECKSHOT Date/time: June 28 2010, 3pm (UTC +1) SURVEY IS, HOW TO IMPORT A SURVEY INTO A WDF AND HOW TO USE THE Geoscientists and engineers using Petrel can SURVEY DATA IN PETROSYS. learn how to present their insight, integrated from several data sources, with the benefits of the Petrosys plug-in. pg 4 What's New in Petrosys v16.8 Presenter: Andrew Weller PPDM 3.8 CULTURE COMPLIANCY Date/time: July 8 2010, 1pm (UTC +8) CLIENTS WITH THE PETROSYS DBMAP SPATIAL OPTION WILL BENEFIT FROM Discover ways in which the features and SPATIALISATION OF THE PETROSYS enhancements of v16.8 can streamline your DBMAP CULTURE MODULE. DISCOVER workflows. HOW. Jump Start to Using Petrosys pg 6 Presenter: Andrew Weller Date/time: July 22 2010, 10am (UTC -5) DEAR STEVE.. -

Malaysia Real Estate Highlights

RESEARCH REAL ESTATE HIGHLIGHTS 2ND HALF 2016 KUALA LUMPUR PENANG JOHOR BAHRU KOTA KINABALU HIGHLIGHTS KUALA LUMPUR HIGH END CONDOMINIUM MARKET Despite the subdued market, there were noticeably more ECONOMIC INDICATORS launches and previews in the TABLE 1 second half of 2016. Malaysia’s Gross Domestic Product Completion of High End (GDP) grew 4.3% in 3Q2016 from 4.0% Condominiums / Residences in in 2Q2016, underpinned by private 2H2016 The secondary market, however, expenditure and private consumption. continues to see lower volume Exports, however, fell 1.3% in 3Q2016 of transactions due to the weak compared to a 1.0% growth in 2Q2016. economy and stringent bank KL Trillion lending guidelines. Amid growing uncertainties in the Jalan Tun Razak external environment, a weak domestic KL City market and continued volatility in the 368 Units The rental market in locations Ringgit, the central bank has maintained with high supply pipeline and a the country’s growth forecast for 2016 at weak leasing market undergoes 4.0% - 4.5% (2015: 5.0%). correction as owners and Le Nouvel investors compete for the same Headline inflation moderated to 1.3% in Jalan Ampang 3Q2016 (2Q2016: 1.9%). pool of tenants. KL City 195 Units Unemployment rate continues to hold steady at 3.5% since July 2016 (2015: The review period continues to 3.1%) despite weak labour market see more developers introducing conditions. Setia Sky creative marketing strategies and Residences - innovative financing packages Bank Negara Malaysia (BNM) lowered the Divina Tower as they look to meet their sales Overnight Policy Rate (OPR) by 25 basis Jalan Raja Muda KL City target and clear unsold stock. -

Malaysian Gamer Spends Four Days Creating Scale Replica of Petronas Twin Towers in 'Minecraft

Thursday, 28 May 2020 Malaysian gamer spends four days creating scale replica of Petronas Twin Towers in ‘Minecraft PETALING JAYA, May 28 — University student Yusri Haneef has created a stunning replica of the iconic Petronas Twin Towers in the world of Minecraft. The youth from Kuching, Sarawak told Malay Mail that he spent four days constructing the landmark in the sandbox video game, in which players can mine raw materials and build custom structures or earthworks. He did so with the help of fellow Minecraft gamer Yu Yi Hao and another player known by the username Ivine123. Yusri explained that the virtual version of the Petronas Twin Towers is part of their contribution towards the Build The Earth (BTE) project, a worldwide effort by players to recreate a scale replica of our planet in Minecraft. The most challenging part of the building process was ensuring that the replica was true to scale and resembled the landmark in terms of visuals, decorations, lighting, and more. “The BTE project focuses on a perfect recreation of the Earth in Minecraft on a one-to-one scale (one metre equals one block in-game) so we needed to take into account every measurement including height, length, decoration, number of floors, and lighting. “Google Maps alone was not enough to be a reference when recreating the buildings, so we would look for aerial pictures on Google, drone footage, and even vlogs that were uploaded on YouTube,” said Yusri. The 21-year-old and his fellow gamers are still working on building the Suria KLCC shopping mall at the base of the towers after completing the nearby KLCC Tower 3 and the Maxis Tower.