Measuring the Impact of Microfinance: Taking Stock of What We Know

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

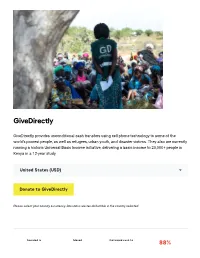

Givedirectly

GiveDirectly GiveDirectly provides unconditional cash transfers using cell phone technology to some of the world’s poorest people, as well as refugees, urban youth, and disaster victims. They also are currently running a historic Universal Basic Income initiative, delivering a basic income to 20,000+ people in Kenya in a 12-year study. United States (USD) Donate to GiveDirectly Please select your country & currency. Donations are tax-deductible in the country selected. Founded in Moved Delivered cash to 88% of donations sent to families 2009 US$140M 130K in poverty families Other ways to donate We recommend that gifts up to $1,000 be made online by credit card. If you are giving more than $1,000, please consider one of these alternatives. Check Bank Transfer Donor Advised Fund Cryptocurrencies Stocks or Shares Bequests Corporate Matching Program The problem: traditional methods of international giving are complex — and often inefficient Often, donors give money to a charity, which then passes along the funds to partners at the local level. This makes it difficult for donors to determine how their money will be used and whether it will reach its intended recipients. Additionally, charities often provide interventions that may not be what the recipients actually need to improve their lives. Such an approach can treat recipients as passive beneficiaries rather than knowledgeable and empowered shapers of their own lives. The solution: unconditional cash transfers Most poverty relief initiatives require complicated infrastructure, and alleviate the symptoms of poverty rather than striking at the source. By contrast, unconditional cash transfers are straightforward, providing funds to some of the poorest people in the world so that they can buy the essentials they need to set themselves up for future success. -

Nber Working Paper Series What Drives Media Slant?

NBER WORKING PAPER SERIES WHAT DRIVES MEDIA SLANT? EVIDENCE FROM U.S. DAILY NEWSPAPERS Matthew Gentzkow Jesse M. Shapiro Working Paper 12707 http://www.nber.org/papers/w12707 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 November 2006 We are grateful to Gary Becker, Gary Chamberlain, Raj Chetty, Tim Conley, Edward Glaeser, Tim Groseclose, Christian Hansen, Larry Katz, Kevin M. Murphy, Andrea Prat, Sam Schulhofer-Wohl, Andrei Shleifer, Wing Suen, Abe Wickelgren, and seminar participants at the University of Chicago, the University of Illinois at Chicago, Clemson University, the University of Toronto, the University of Houston, Rice University, Texas A&M University, Harvard University, and Northwestern University for helpful comments. We especially wish to thank Renata Voccia, Paul Wilt, Todd Fegan, and the rest of the staff at ProQuest for their support and assistance at all stages of this project. Steve Cicala, Hays Golden, Jennifer Paniza, and Mike Sinkinson provided outstanding research assistance and showed tireless dedication to this project. We also thank Yujing Chen, Alex Fogel, and Lisa Furchtgott for excellent research assistance. This research was supported by National Science Foundation Grant SES-0617658. The views expressed herein are those of the author(s) and do not necessarily reflect the views of the National Bureau of Economic Research. © 2006 by Matthew Gentzkow and Jesse M. Shapiro. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source. What Drives Media Slant? Evidence from U.S. Daily Newspapers Matthew Gentzkow and Jesse M. -

October 26, 2014

Animal Charity Evaluators Board of Directors Meeting Type of Meeting: Standard Monthly Meeting Date: October 26, 2014 In attendance: Chairperson: Simon Knutsson Treasurer: Brian Tomasik Secretary: Rob Wiblin Board Member: Sam BankmanFried Board Member: Peter Singer Board Member: S. Greenberg Executive Director: Jon Bockman Absent: Quorum established: Yes 1. Call to order: SK called the meeting to order at 9:05 am PST 2. Important questions document 1. In the philosophy document (and in the important questions document and the strategy plan, which refer to it): a. Edit the part about veganism, which can be seen as a method for benefiting animals rather than a vision or a philosophical position. b. Edit the part about wild animal suffering. The challenge is to balance bringing up an important idea with making a good impression on those who are not already aware of it or interested in it. Some board members think that we have been giving it too much space in these documents and others think it warrants that level of space because of the importance of the issue. i. Could interview others about wild animal suffering or invite them to guest blog about it. c. Improve general writing quality based on the comments from the board. 2. Consider writing a report that is as objective as possible on the important questions. 3. PS can help getting academics interested in effective animal activism. a. Has a contact at the Animal Studies Initiative at NYU – maybe this person could organize a conference b. Researchers studying persuasion might be interested (ACE or PS can encourage them) 4. -

Understanding Development and Poverty Alleviation

14 OCTOBER 2019 Scientific Background on the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2019 UNDERSTANDING DEVELOPMENT AND POVERTY ALLEVIATION The Committee for the Prize in Economic Sciences in Memory of Alfred Nobel THE ROYAL SWEDISH ACADEMY OF SCIENCES, founded in 1739, is an independent organisation whose overall objective is to promote the sciences and strengthen their influence in society. The Academy takes special responsibility for the natural sciences and mathematics, but endeavours to promote the exchange of ideas between various disciplines. BOX 50005 (LILLA FRESCATIVÄGEN 4 A), SE-104 05 STOCKHOLM, SWEDEN TEL +46 8 673 95 00, [email protected] WWW.KVA.SE Scientific Background on the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel 2019 Understanding Development and Poverty Alleviation The Committee for the Prize in Economic Sciences in Memory of Alfred Nobel October 14, 2019 Despite massive progress in the past few decades, global poverty — in all its different dimensions — remains a broad and entrenched problem. For example, today, more than 700 million people subsist on extremely low incomes. Every year, five million children under five die of diseases that often could have been prevented or treated by a handful of proven interventions. Today, a large majority of children in low- and middle-income countries attend primary school, but many of them leave school lacking proficiency in reading, writing and mathematics. How to effectively reduce global poverty remains one of humankind’s most pressing questions. It is also one of the biggest questions facing the discipline of economics since its very inception. -

The Impacts of Microcredit: Evidence from Bosnia and Herzegovina †

American Economic Journal: Applied Economics 2015, 7 1 : 183–203 http://dx.doi.org/10.1257/app.20130272 ( ) The Impacts of Microcredit: Evidence from Bosnia and Herzegovina † By Britta Augsburg, Ralph De Haas, Heike Harmgart, and Costas Meghir * We use an RCT to analyze the impacts of microcredit. The study pop- ulation consists of loan applicants who were marginally rejected by an MFI in Bosnia. A random subset of these were offered a loan. We provide evidence of higher self-employment, increases in inventory, a reduction in the incidence of wage work and an increase in the labor supply of 16–19-year-olds in the household’s business. We also pres- ent some evidence of increases in profits and a reduction in consump- tion and savings. There is no evidence that the program increased overall household income. JEL C93, G21, I38, J23, L25, P34, P36 ( ) substantial part of the world’s poor has limited, if any, access to formal sources A of credit. Instead, they depend on informal credit from expensive moneylenders or have to borrow from family and friends Collins et al. 2010 . Such credit rationing ( ) may constrain entrepreneurship and keep people trapped in poverty. Microfinance, pioneered by the Bangladeshi Grameen Bank, aimed to deal with this issue in a sustainable fashion. A key research and policy question is whether the availability of credit for the more disadvantaged can reduce poverty. We address this question by analyzing the results of an experiment where we ran- domly allocated loans at the individual level to a subset of applicants considered too ( ) risky and “unreliable” to be offered credit as regular borrowers of a well-established microfinance institution MFI in Bosnia and Herzegovina. -

Against 'Effective Altruism'

Against ‘Effective Altruism’ Alice Crary Effective Altruism (EA) is a programme for rationalising for the most part adopt the attitude that they have no charitable giving, positioning individuals to do the ‘most serious critics and that sceptics ought to be content with good’ per expenditure of money or time. It was first for- their ongoing attempts to fine-tune their practice. mulated – by two Oxford philosophers just over a decade It is a posture belied by the existence of formidable ago–as an application of the moral theory consequential- critical resources both inside and outside the philosoph- ism, and from the outset one of its distinctions within ical tradition in which EA originates. In light of the undis- the philanthropic world was expansion of the class of puted impact of EA, and its success in attracting idealistic charity-recipients to include non-human animals. EA young people, it is important to forcefully make the case has been the target of a fair bit of grumbling, and even that it owes its success primarily not to the – question- some mockery, from activists and critics on the left, who able – value of its moral theory but to its compatibility associate consequentialism with depoliticising tenden- with political and economic institutions responsible for cies of welfarism. But EA has mostly gotten a pass, with some of the very harms it addresses. The sincere ded- many detractors concluding that, however misguided, its ication of many individual adherents notwithstanding, efforts to get bankers, tech entrepreneurs and the like to reflection on EA reveals a straightforward example of give away their money cost-effectively does no serious moral corruption. -

EA Course: Overview and Future Plans

EA Course: Overview and Future Plans Note: I encourage you to first read the One Page Summary at the bottom and then skip to the sections you’re interested in. ❖ Background ❖ Goals ➢ For the class ➢ For the club ➢ Ideal student ❖ Class Structure ➢ Basics ➢ Giving games ➢ Final project ➢ Potential changes ❖ Course Content ❖ Advertising and Recruiting ❖ Speakers ❖ Financial Management ➢ Banking ➢ Sources of Money ➢ Financial management issues ■ Communication Issues ■ Payment Issues ■ Reimbursement Issues ➢ Potential changes ❖ Website ❖ Final Project ➢ Goals ➢ Winning project ➢ Potential changes ❖ Evidence of Impact ➢ Collection ➢ Outcomes ➢ Potential changes ❖ Future Plans ❖ Funding Goals ❖ One Page Summary Background ● Oliver Habryka and I taught a studentled class (“DeCal”) during the Spring 2015 semester at UC Berkeley called The Greater Good, on effective altruism ● The class was taught under the banner of Effective Altruists of Berkeley, a student organization we founded the previous semester ● Overall, I think it was a success and satisfied most of our initial goals (details below) Goals ● Goals for the class: ○ Primarily, we wanted to recruit people for our newly created Effective Altruists of Berkeley club ■ Having to engage with/debate EA for a semester beforehand would allow people to really understand if they wanted to become involved in it ■ It would also allow them to contribute to the club’s projects without having to be given a whole lot of background first ■ We also felt that going through a class together first would -

Givewell NYC Research Event, December 14, 2015 – Top Charities

GiveWell NYC Research Event, December 14, 2015 – Top Charities GiveWell NYC Research Event, December 14, 2015 – Top Charities GiveWell NYC Research Event, December 14, 2015 – Top Charities This transcript was compiled by an outside contractor, and GiveWell did not review it in full before publishing, so it is possible that parts of the audio were inaccurately transcribed. If you have questions about any part of this transcript, please review the original audio recording that was posted along with these notes. Elie: All right. Well, thanks everyone for coming. I'm Elie Hassenfeld. I'm one of Givewell's co- founders. This is Natalie Crispin. Natalie: Hi. I'm a senior research analyst at Givewell. Elie: We're really happy that you joined us tonight. I just want to quickly go through some of the logistics and the basic plan for the evening. Then I'll turn it over to Natalie to talk a little bit. Just first, like we do with pretty much everything that Givewell does, we're going to try to share as much of this evening as we can with our audience. That means that we're going to record the audio of the session and publish a transcript on our website. If you say anything that you would prefer not be included in the audio or transcript, just email me, [email protected] or [email protected] or just come find me at the end of the night, and we can make sure to cut that from the event. You should feel free to speak totally freely this evening. -

Savings by and for the Poor: a Research Review and Agenda

Savings by and for the Poor: A Research Review and Agenda Dean Karlan, Aishwarya Lakshmi Ratan, and Jonathan Zinman Abstract The poor can and do save, but often use formal or informal instruments that have high risk, high cost, and limited functionality. This could lead to undersaving compared to a world without market or behavioral frictions. Undersaving can have important welfare consequences: variable consumption, low resilience to shocks, and foregone profitable investments. We lay out five sets of constraints that may hinder the adoption and effective usage of savings products and services by the poor: transaction costs, lack of trust and regulatory barriers, information and knowledge gaps, social constraints, and behavioral biases. We discuss each in theory, and then summarize related empirical evidence, with a focus on recent field experiments. We then put forward key open areas for research and practice. JEL Codes: D12, D91, G21, O16 Keywords: Savings, Randomized Evaluation, Poverty Working Paper 346 www.cgdev.org November 2013 Savings by and for the poor: A research review and agenda Dean Karlan Yale University, IPA, J-PAL, and NBER Aishwarya Lakshmi Ratan Yale University, IPA Jonathan Zinman Dartmouth College, IPA, J-PAL, and NBER This paper was developed as a guiding white paper for the Yale Savings and Payments Research Fund, supported by the Bill and Melinda Gates Foundation, and with support from UNU-WIDER, based on a lecture at the 2011 Poverty and Behavioral Economics Conference. Contact and affiliations are as follows. Karlan, [email protected]; Yale University, Innovations for Poverty Action, Abdul Latif Jameel Poverty Action Lab at M.I.T, and NBER. -

Field Experiments in Development Economics1 Esther Duflo Massachusetts Institute of Technology

Field Experiments in Development Economics1 Esther Duflo Massachusetts Institute of Technology (Department of Economics and Abdul Latif Jameel Poverty Action Lab) BREAD, CEPR, NBER January 2006 Prepared for the World Congress of the Econometric Society Abstract There is a long tradition in development economics of collecting original data to test specific hypotheses. Over the last 10 years, this tradition has merged with an expertise in setting up randomized field experiments, resulting in an increasingly large number of studies where an original experiment has been set up to test economic theories and hypotheses. This paper extracts some substantive and methodological lessons from such studies in three domains: incentives, social learning, and time-inconsistent preferences. The paper argues that we need both to continue testing existing theories and to start thinking of how the theories may be adapted to make sense of the field experiment results, many of which are starting to challenge them. This new framework could then guide a new round of experiments. 1 I would like to thank Richard Blundell, Joshua Angrist, Orazio Attanasio, Abhijit Banerjee, Tim Besley, Michael Kremer, Sendhil Mullainathan and Rohini Pande for comments on this paper and/or having been instrumental in shaping my views on these issues. I thank Neel Mukherjee and Kudzai Takavarasha for carefully reading and editing a previous draft. 1 There is a long tradition in development economics of collecting original data in order to test a specific economic hypothesis or to study a particular setting or institution. This is perhaps due to a conjunction of the lack of readily available high-quality, large-scale data sets commonly available in industrialized countries and the low cost of data collection in developing countries, though development economists also like to think that it has something to do with the mindset of many of them. -

The Impacts of Microcredit: Evidence from Ethiopia†

American Economic Journal: Applied Economics 2015, 7(1): 54–89 http://dx.doi.org/10.1257/app.20130475 The Impacts of Microcredit: Evidence from Ethiopia† By Alessandro Tarozzi, Jaikishan Desai, and Kristin Johnson* We use data from a randomized controlled trial conducted in 2003–2006 in rural Amhara and Oromiya Ethiopia to study the impacts of increasing access to microfinance( on a) number of socioeconomic outcomes, including income from agriculture, animal husbandry, nonfarm self-employment, labor supply, schooling and indicators of women’s empowerment. We document that despite sub- stantial increases in borrowing in areas assigned to treatment the null of no impact cannot be rejected for a large majority of outcomes. JEL G21, I20, J13, J16, O13, O16, O18 ( ) eginning in the 1970s, with the birth of the Grameen Bank in Bangladesh, Bmicrocredit has played a prominent role among development initiatives. Many proponents claim that microfinance has had enormously positive effects among borrowers. However, the rigorous evaluation of such claims of success has been complicated by the endogeneity of program placement and client selection, both common obstacles in program evaluations. Microfinance institutions MFIs typi- ( ) cally choose to locate in areas predicted to be profitable, and or where large impacts / are expected. In addition, individuals who seek out loans in areas served by MFIs and that are willing and able to form joint-liability borrowing groups a model often ( preferred by MFIs are likely different from others who do not along a number of ) observable and unobservable factors. Until recently, the results of most evaluations could not be interpreted as conclusively causal because of the lack of an appropriate control group see Brau and Woller 2004 and Armendáriz de Aghion and Morduch ( 2005 for comprehensive early surveys . -

Beyond Feel-Good Philanthropy by Dr Michael Liffman, Director of the Asia-Pacific Centre for Social Investment and Philanthropy at Swinburne University

Beyond feel-good Philanthropy By Dr Michael Liffman, Director of the Asia-Pacific Centre for Social Investment and Philanthropy at Swinburne University. am sure we have all experienced social investment is effective, and can be shown to be so. This is, that strange feeling when driving, in my view, a very good place for the debate to have moved to. of arriving at the other side of a difficult intersection with no recollection Encouragingly, a similar focus is emerging in Australia too. of how we crossed it. The current debate The Centre for Social Impact is offering useful resources for overseas about the importance of impact the measurement of social return through the December in giving reminds me a little of that feeling. issue of its publication Knowledge Connect, and its Suddenly, instead of talking about the forthcoming short course: http://csi.edu.au/latest-csi-news/ virtue of giving, the commentators csi-march-newsletter/#Social are talking about ‘social return’. “ I contend that a mature philanthropic Typical is the December 2009 issue of that especially useful UK-based journal, Alliance which draws attention sector is one which recognises that to commentators who urge that outcomes are more generosity does not exonerate virtuous important than donor intentions. people from the responsibility to A discussion at the European Foundation Centre Conference consider the effectiveness of their in Rome last year led to leading British consultant (and one of APCSIP’s early Waislitz Visiting Fellows) David Carrington actions, by ensuring that their gift, being commissioned to produce a report asking whether better if not maximising the good it can do, research into philanthropy and social investment could improve is at least is doing some real good.” the practice of philanthropy.