Table of Contents.2008.Docx

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

THE POLAND SCHOOLS December 4, 2017 - Update

THE POLAND SCHOOLS December 4, 2017 - update To: All Personnel Re: Snow Delays/Closings From: David Janofa, Superintendent 1. With winter weather approaching, it is appropriate to review the districts’ policies and procedures in the event it is necessary to delay or close schools due to hazardous weather/road conditions. 2. Should the school district exceed the maximum numbers of calamity days per negotiated agreement, makeup days would be added at the end of the school year. The first makeup day would be Thursday, June 6 and additional days would be consecutively scheduled week days. Teacher report day would be the weekday following the last makeup day. 3. Decisions to delay or close schools will be made in most instances between 6:00 and 6:30 a.m. Any change in the normal school schedule will be announced to staff, students, and the public through these methods: . TV Channels: 21, 27, 33, and 62 . Radio Stations: 570 AM-WKBN, 1390 AM-WNIO, 93.3 WNCD, 95.9 FM-WAKZ (KISS), 98.9 FM-WMXY, 106.1 FM-WBBG, 101 FM-HOT, and Y103 FM. http://www.poland.k12.oh.us/ or WKBN.com or WYFX.com or Polandbulldogs.com . “All Call” computerized phone notification to parents/employees 4. Should a delay be implemented, here are some important procedures to remember: A two hour delay means all schools simply start two hours later. Students’ hours for example would be: High School would start at 9:45 a.m. instead of 7:45 a.m. Middle School and McKinley Elem. would start at 10:35 a.m. -

2021 Q1 Cash Sweepstakes Appendix a - Participating Stations

2021 Q1 Cash Sweepstakes Appendix A - Participating Stations Station iHM Market Station Website Office Phone Mailing Address WHLO-AM Akron, OH 640whlo.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WHOF-FM Akron, OH sunny1017.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WHOF-HD2 Akron, OH cantonsnewcountry.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WKDD-FM Akron, OH wkdd.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WRQK-FM Akron, OH wrqk.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WGY-AM Albany, NY wgy.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 WGY-FM Albany, NY wgy.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 WKKF-FM Albany, NY kiss1023.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 WOFX-AM Albany, NY foxsports980.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 WPYX-FM Albany, NY pyx106.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 WRVE-FM Albany, NY 995theriver.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 WRVE-HD2 Albany, NY wildcountry999.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 WTRY-FM Albany, NY 983try.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 KABQ-AM Albuquerque, NM abqtalk.iheart.com 505-830-6400 5411 Jefferson NE, Ste 100, Albuquerque, NM 87109 KABQ-FM Albuquerque, NM 1047kabq.iheart.com 505-830-6400 5411 Jefferson NE, Ste 100, Albuquerque, NM -

Regular Meeting Poland Board of Education Held November 23, 2020

11/23/2020 2702 Regular Meeting Poland Board of Education held November 23, 2020 The Regular meeting of the Poland Board of Education was held on Monday, November 23, 2020, at 6:00 p.m. President, Mr. Riddle called the meeting to order at 6:00 p.m. Pledge of Allegiance Members present for roll call and answering their names were Ms. Colucci, Dr. Dinopoulos, Mr. Polis, Mr. Riddle and Mr. Warren PUBLIC PARTICIPATION - Jessica Cene – 4465 Arrel Road – Concerned about Poland’s recent decision to go to remote learning. Approval to Commend Staff and Student Achievements – Resolution #2020-170 Mr. Polis moved and Ms. Colucci seconded with all members present voting aye to congratulate the following members of the 2020 Fall Homecoming Court. Motion passed 5-0. Morgan Decore Madison Wess Ella Harrell (Queen) Chloe Kosco Camryn Lattanzio Alex Giaros Karter Kelgren Anthony Koulianos (King) Elias Lopuchovsky Brody Todd Approval of Consent Agenda – Resolution #2020-171 Moved by Mr. Warren, seconded by Dr. Dinopoulos to approve the following consent agenda items: Treasurer/CFO Requests of Consent: Janet Muntean 1. The Board approve the Minutes of October 26, 2020, October 28, 2020 and November 16, 2020. 2. The Board approve the Financial Report of October 2020 as submitted. 3. The Board approve the FY21 appropriation modifications and submit for certification to the Mahoning County Budget Commission for all funds. Superintendent’s Requests of Consent: Dr. Edwin Holland 1. The Board approve the following non-teaching personnel be placed on the approved substitute list for the 2020-2021 school year, substitute basis only, according to wage rate for the assignment designated; all required reports are on file: Joseph Colella - Substitute Bus Driver/Sub Bus Aide; effective November 12, 2020 11/23/2020 2703 2. -

This Is Onlya Test

PreparednessEmergency is located in your local Information This is telephone directory a test. only Siren Test Thursday, Siren Notification System September 1, Each large, pole-mounted emergency siren is equipped with different signals. Two of these are the Alert Signal and Fire Signal. 6:15 p.m. Alert Signal: A steady tone for three minutes. If the Alert Signal sounds, immediately tune your Emergency sirens in Beaver, radio or TV to your Emergency Alert System Columbiana and Hancock station for information and instructions. counties will be tested on Fire Signal: A 20 second steady alert tone, Thursday, September 1, at repeated as necessary. The Fire Signal is used to alert firefighters. No response is necessary approximately 6:15 p.m. from the general public. The test – a steady, three-minute siren tone – will Need special help during an emergency? include 120 large pole-mounted sirens. This test is Tell us NOW! performed as a federal requirement to ensure the If you need special help, transportation or sirens in the ten-mile radius around Beaver Valley other assistance during an emergency, please Power Station are working properly. contact your county’s emergency management If you hear the siren on September 1, at agency (EMA) or office of emergency manage- 6:15 p.m., you do not need to respond. ment (OEM) at the following number to make sure you receive the assistance you need. This The alert signal being tested would be sounded by information will be kept confidential and will only your county emergency management agency in case be used to ensure you are provided with help of an emergency at Beaver Valley Power Station – or during an emergency. -

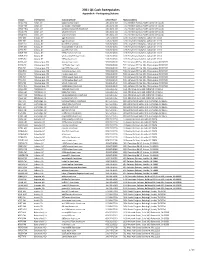

Stations Monitored

Stations Monitored 10/01/2019 Format Call Letters Market Station Name Adult Contemporary WHBC-FM AKRON, OH MIX 94.1 Adult Contemporary WKDD-FM AKRON, OH 98.1 WKDD Adult Contemporary WRVE-FM ALBANY-SCHENECTADY-TROY, NY 99.5 THE RIVER Adult Contemporary WYJB-FM ALBANY-SCHENECTADY-TROY, NY B95.5 Adult Contemporary KDRF-FM ALBUQUERQUE, NM 103.3 eD FM Adult Contemporary KMGA-FM ALBUQUERQUE, NM 99.5 MAGIC FM Adult Contemporary KPEK-FM ALBUQUERQUE, NM 100.3 THE PEAK Adult Contemporary WLEV-FM ALLENTOWN-BETHLEHEM, PA 100.7 WLEV Adult Contemporary KMVN-FM ANCHORAGE, AK MOViN 105.7 Adult Contemporary KMXS-FM ANCHORAGE, AK MIX 103.1 Adult Contemporary WOXL-FS ASHEVILLE, NC MIX 96.5 Adult Contemporary WSB-FM ATLANTA, GA B98.5 Adult Contemporary WSTR-FM ATLANTA, GA STAR 94.1 Adult Contemporary WFPG-FM ATLANTIC CITY-CAPE MAY, NJ LITE ROCK 96.9 Adult Contemporary WSJO-FM ATLANTIC CITY-CAPE MAY, NJ SOJO 104.9 Adult Contemporary KAMX-FM AUSTIN, TX MIX 94.7 Adult Contemporary KBPA-FM AUSTIN, TX 103.5 BOB FM Adult Contemporary KKMJ-FM AUSTIN, TX MAJIC 95.5 Adult Contemporary WLIF-FM BALTIMORE, MD TODAY'S 101.9 Adult Contemporary WQSR-FM BALTIMORE, MD 102.7 JACK FM Adult Contemporary WWMX-FM BALTIMORE, MD MIX 106.5 Adult Contemporary KRVE-FM BATON ROUGE, LA 96.1 THE RIVER Adult Contemporary WMJY-FS BILOXI-GULFPORT-PASCAGOULA, MS MAGIC 93.7 Adult Contemporary WMJJ-FM BIRMINGHAM, AL MAGIC 96 Adult Contemporary KCIX-FM BOISE, ID MIX 106 Adult Contemporary KXLT-FM BOISE, ID LITE 107.9 Adult Contemporary WMJX-FM BOSTON, MA MAGIC 106.7 Adult Contemporary WWBX-FM -

2020-Siren-Test.Pdf

PreparednessEmergency is locatedInformation on the County websites onlyThis is a test. Siren Notification System Each large, pole-mounted emergency siren is equipped with different signals. Two of these are the Alert Signal and Siren Test Fire Signal. Alert Signal: A steady tone for three minutes. If the Alert Signal sounds, Thursday, immediately tune your radio or TV to your Emergency Alert System station for information and instructions. September 10, Fire Signal: A 20 second steady alert tone, repeated as necessary. The Fire Signal is 11:00 a.m. used to alert firefighters.No response is necessary from the general public. Emergency sirens in Beaver, Need special help during an emergency? Tell us NOW! Columbiana and Hancock If you need special help, transportation or counties will be tested on other assistance during an emergency, please contact your county’s emergency Thursday, September 10, at management agency (EMA) or office of approximately 11:00 a.m. emergency management (OEM) at the following number to make sure you receive The test – a steady, three-minute siren the assistance you need. This information tone – will include 118 large pole-mounted will be kept confidential and will only be sirens. This test is performed as a federal used to ensure you are provided with help requirement to ensure the sirens in the ten- during an emergency. mile radius around Beaver Valley Power Eric Brewer, Beaver County Station are working properly. EMA Director (724) 775-1700 If you hear the siren on September 10, at Jeremy Ober, Hancock County 11:00 a.m., you do not need to respond. -

Appendix a - Participating Stations

Appendix A - Participating Stations Station City Website Phone Address WHLO-AM Akron, OH 640whlo.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WHOF-FM Akron, OH sunny1017.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WHOF-HD2 Akron, OH cantonsnewcountry.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WKDD-FM Akron, OH wkdd.iheart.com 330-492-4700 7755 Freedom Avenue, North Canton OH 44720 WTRY-FM Albany, NY 983try.iheart.com 518-452-4800 1203 Troy Schenectady Rd., Latham NY 12110 KZRR-HD2 Albuquerque, NM 1009thebeat.iheart.com 505-830-6400 5411 Jefferson NE, Ste 100, Albuquerque, NM 87109 WAEB-AM Allentown, PA 790waeb.iheart.com 610-434-1742 1541 Alta Drive, Suite 400, Whitehall PA 18052 KYMG-FM Anchorage, AK magic989fm.iheart.com 907-522-1515 800 East Dimond, Suite 3-370, Anchorage, AK 99515 WUBL-FM Atlanta, GA 949thebull.iheart.com 404-875-8080 1819 Peachtree Rd NE, Atlanta, GA 30309 WMXA-FM Auburn, AL mix967online.iheart.com 334-745-4656 915 Veterans Parkway, Opelika, AL 36801 WBBQ-FM Augusta, GA wbbq.iheart.com 706-396-6000 2743 Perimeter Parkway, Building 100, Suite 300, Augusta, GA 30909 KBFP-FM Bakersfield, CA sunny1053.com 661-322-9929 1100 Mohawk Street, Suite 280, Bakersfield, CA 93309 WCAO-AM Baltimore, MD heaven600.iheart.com 240-747-2700 711 West 40th Street Baltimore, MD 21211 KRVE-FM Baton Rouge, LA 961theriver.iheart.com 225-231-1860 5555 Hilton Ave, Ste 500, Baton Rouge, LA 70808 WYNK-FM Baton Rouge, LA wynkcountry.iheart.com 225-231-1860 5555 Hilton Ave, Ste -

Appendix 2-1 Summary of Plan Reviews Butler Township Comprehensive Recreation, Parks and Open Space Plan - 1995

9th Inning: Appendices Appendix 2-1 Summary of Plan Reviews Butler Township Comprehensive Recreation, Parks and Open Space Plan - 1995 A thorough regional analysis is provided, including lists of: * National Recreation Areas * Pennsylvania State Parks * State Forest Natural Areas * State Game Lands * Regional Bicycle/Pedestrian Trails * Municipal, County and other Public Parks and Facilities * Historical Sites and Commercial Facilities History o Butler Township formal organization was in 1804. Original four townships were divided into 13 townships. Incorporated in 1817. It was then divided into North and South Butler. In 1854, the Township acquired its present boundaries. o Before European settlement, the Shawnee and Delaware Indians were its inhabitants. o Sawmills and whiskey distilleries were among the first industries in the area.Tanneries and brickyards soon followed to quickly become the importance of local economy. Small scale mining started taking place around 1811. Once the railroads made large-scale transportation possible, the natural resource became seriously exploited by 1871. o Butler Township is still home to ARMCO Steel and American Glass Research. o Butler Township has the largest population of any municipality in Butler County. o In 1937, a large portion of Butler Township Park was purchased. Another portion was purchased from the Catholic Diocese in 1990. o Deshon Woods Park was purchased from the federal government in mid-1950s. o A part-time recreation director was employed by the township for about 10 years, but retired in early 1990s. No replacement has been hired. Cultural Resources Inventory o Large-scale commercial development has taken place mostly in the northern portion of the Township. -

Market, Financial Analysis, and Economic Impact for Idaho Falls, Idaho Multipurpose Events Center

Final Report Market, Financial Analysis, and Economic Impact for Idaho Falls, Idaho Multipurpose Events Center Idaho Falls, Idaho Prepared for City of Idaho Falls Submitted by Economics Research Associates Spring 2008 Reprinted January 4, 2010 ERA Project No. 17704 10990 Wilshire Boulevard Suite 1500 Los Angeles, CA 90024 310.477.9585 FAX 310.478.1950 www.econres.com Los Angeles San Francisco San Diego Chicago Washington DC New York London Completed Spring 2008 - Reprinted Jan 4, 2010 Table of Contents Section 1. Executive Summary.............................................. 1 Section 2. Introduction and Scope of Services .................... 7 Section 3. Idaho Falls, Idaho Overview ................................ 11 Section 4. Potential Anchor Tenants / Sports Leagues / Other Events ......................................................... 22 Section 5. Comparable Events Centers ................................ 43 Section 6. Events Center – Potential Sizing and Attendance .................................................... 54 Section 7. Financial Analysis – Base Case, High and Low Scenarios ....................................................... 56 Section 8. Economic Impact Analysis ................................... 83 Appendix. Site Analysis Proposed Idaho Falls Multipurpose Events Center ERA Project No. 17704 Page i Completed Spring 2008 - Reprinted Jan 4, 2010 General Limiting Conditions Every reasonable effort has been made to ensure that the data contained in this study reflect the most accurate and timely information possible, and they are believed to be reliable. This study is based on estimates, assumptions and other information reviewed and evaluated by Economics Research Associates from its consultations with the client and the client's representatives and within its general knowledge of the industry. No responsibility is assumed for inaccuracies in reporting by the client, the client's agent and representatives or any other data source used in preparing or presenting this study. -

Other Football Leagues

Sports Facility Reports, Volume 7, Appendix 3.1 Other Football Leagues League: Arena Football League (AFL) Team: Arizona Rattlers Principal Owner: Bobby Hernreich Team Website Stadium: U.S. Airways Center Date Built: 1992 Facility Cost (millions): $90 M Facility Financing: The City of Phoenix contributed $35 M with $28 M going to construct the arena and $7 M for the land. The Phoenix Suns contributed $55 M. The city has a 30-year commitment from the Suns to repay a portion of the contribution at $500,000 per year, with an annual 3% increase. The city will also receive 40% of revenue from luxury boxes and advertising. Facility Website UPDATE: Bobby Hernreich, co-owner of the Sacramento Kings, is the new owner of the Arizona Rattlers. Hernreich will be the majority owner, while Robert Sarver will retain minority ownership. Terms of the deal were not disclosed. NAMING RIGHTS: US Airways is paying $26 M over 30 years for the naming rights that expire in 2019. In January 2006, the name of the arena was changed from America West Arena to the US Airways Center after America West and US Airways merged in 2005. Team: Austin Wranglers Principal Owner: Tony Boselli, Mark Brunell, Jeff Clarke, Perry Coughlin, John Craparo, Leonard Davis, Bob Davis, Tom Hogan, Flynn Kile, Doug MacGregor, Tim McClure, Charlie McMurtry, Glyn Milburn, Bret Plymire, Jim Schneider, Leigh Steinberg, Andre Wadsworth, and Mike Williams Team Website © Copyright 2006, National Sports Law Institute of Marquette University Law School Page 1 Stadium: Frank Erwin Center Date Built: 1977 Facility Cost (millions): $34 Facility Website Team: Chicago Rush Principal Owner: Mike Ditka, Arthur Price, Peter Levin, and Alan M. -

This Is a Test

Emergency is locatedPreparedness in your local telephoneInformation directory This is only a test. Siren Notification System Each large, pole-mounted emergency siren is equipped with different signals. Two of these are the Alert Signal and Siren Test Fire Signal. Alert Signal: A steady tone for three minutes. If the Alert Signal sounds, Thursday, immediately tune your radio or TV to your Emergency Alert System station for information and instructions. September 6, Fire Signal: A 20 second steady alert tone, repeated as necessary. The Fire Signal is 11:00 a.m. used to alert firefighters. No response is necessary from the general public. Emergency sirens in Beaver, Need special help during an emergency? Tell us NOW! Columbiana and Hancock If you need special help, transportation or counties will be tested on other assistance during an emergency, please contact your county’s emergency Thursday, September 6, at management agency (EMA) or office of approximately 11:00 a.m. emergency management (OEM) at the following number to make sure you receive The test – a steady, three-minute siren the assistance you need. This information tone – will include 118 large pole-mounted will be kept confidential and will only be sirens. This test is performed as a federal used to ensure you are provided with help requirement to ensure the sirens in the ten- during an emergency. mile radius around Beaver Valley Power Eric Brewer, Beaver County Station are working properly. EMA Director (724) 775-1700 If you hear the siren on September 6, at Jeremy Ober, Hancock County 11:00 a.m., you do not need to respond. -

“The Good News Newspaper” Vol

“The Good News Newspaper” VOL. 13 NO. 12 JUNE 10, 2017 SERVING THE LAKESHORE COMMUNITIES SUMMER VACATION AIR SHOW FLIES IN JUNE 17-18 By Sally Lane ummer vacation has to be the fun means to you - dance through our The 70th anniversary of the U.S. Air Force will be celebrated with the most anticipated time of the year. heads, just waiting to become memories. Thunder Over the Valley air show June 17 and 18 at the Youngstown Air Who doesn’t remember bursting It just feels good to be outside and feel the Reserve Station in Vienna. S through the school doors on that warm air. According to Col. Jeffrey Shaffer, the U.S. Air Force reserve command last day, free at last! Visions of sunny The kids will love the Splash Pad on has designated this air show to be the showcase event celebrating the U.S. beaches and waves, music, picnics Pearl Street. A pavilion, picnic tables and Air Force’s 70th birthday this year. Shaffer is show planner for the event. and fair food – or whatever summer new landscaping recently finished off the The 2017 air show features the world-famous United States Air Force project. It is ready for prime splashing! Thunderbirds and some of the best civilian and military aviators in the With Mosquito Lake in our backyard, world. Base officials are planning for 25,000 people to visit the base for more fun is always nearby. There is each day of the free show. The show will run both days from 11 a.m.