India- Ahmedabad- Residential Q4 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

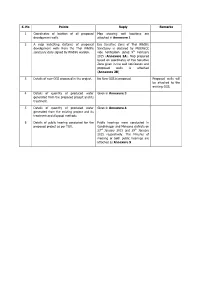

S. No Points Reply Remarks 1 Coordinates of Location of All Proposed Development Wells Map Showing Well Locations Are Attached I

S. No Points Reply Remarks 1 Coordinates of location of all proposed Map showing well locations are development wells attached in Annexure 1 2 A map indicating distance of proposed Eco Sensitive Zone of Thol Wildlife development wells from the Thol Wildlife Sanctuary is declared by MOEF&CC sanctuary dully signed by Wildlife warden. vide notification dated 9th February 2015 (Annexure 2A). Map prepared based on coordinates of Eco Sensitive Zone given in the said notification and proposed wells is attached (Annexure 2B) 3 Details of new GGS proposed in the project. No New GGS is proposed Proposed wells will be attached to the existing GGS. 4 Details of quantity of produced water Given in Annexure 3 generated from the proposed project and its treatment. 5 Details of quantity of produced water Given in Annexure 4 generated from the existing project and its treatment and disposal methods 6 Details of public hearing conducted for the Public hearings were conducted in proposed project as per TOR. Gandhinagar and Mehsana districts on 23rd January 2015 and 29th January 2015 respectively. The Minutes of meeting of both public hearings are attached as Annexure 5 Co ordinates of mining lease Name of Latitude (N) Longitude (E) Field PEL/ML Point (Sq. km.) Deg. Min. Sec. Deg. Min. Sec. Kalol Main H 72 35 57.01 23 11 58.99 ML I 72 31 19.99 23 9 31.00 J 72 30 7.02 23 11 21.01 K 72 34 52.00 23 13 54.01 H 72 35 57.01 23 11 58.99 Kalol EXT – 1 N' 72 35 10.00 23 11 33.00 ML T' 72 35 35.99 23 8 30.98 T 72 34 40.01 23 7 59.99 S' 72 33 37.01 23 10 0.98 S 72 -

205 Bus Time Schedule & Line Route

205 bus time schedule & line map 205 Vasna Terminus View In Website Mode The 205 bus line Vasna Terminus has one route. For regular weekdays, their operation hours are: (1) Vasna Terminus: 6:45 AM - 9:25 PM Use the Moovit App to ƒnd the closest 205 bus station near you and ƒnd out when is the next 205 bus arriving. Direction: Vasna Terminus 205 bus Time Schedule 37 stops Vasna Terminus Route Timetable: VIEW LINE SCHEDULE Sunday 6:45 AM - 9:25 PM Monday 6:45 AM - 9:25 PM Vasna Terminus Ashram Road, Ahmadābād Tuesday 6:45 AM - 9:25 PM Jawahar Nagar Wednesday 6:45 AM - 9:25 PM Anand Nagar Thursday 6:45 AM - 9:25 PM Friday 6:45 AM - 9:25 PM Jain Merchant Society Saturday 6:45 AM - 9:25 PM Parimal Garden Chimanlal Girdharlal Road, Ahmadābād Panchvati 205 bus Info Telephone Exchange (C. G. Road) Direction: Vasna Terminus Stops: 37 Swastik Society Trip Duration: 69 min Commerce College Road, Ahmadābād Line Summary: Vasna Terminus, Jawahar Nagar, Anand Nagar, Jain Merchant Society, Parimal Sardar Patel Square Garden, Panchvati, Telephone Exchange (C. G. Road), Swastik Society, Sardar Patel Square, Usmanpura Usmanpura, Vadaj Bus Terminuss, Subhash Bridge, Radhaswami Satsang, Ranip, Gayatri Vidyalay, Vimal Tenament, Ramwadi(Madhav Bagh), Deshwali Vadaj Bus Terminuss Society, Shankar Da Hall, Chhaya Flats, R. C. Technical Institute, Gujarat High Court Brts, Sola Subhash Bridge Police Chowki, Thaltej Gam, Sahajanand Bungalows, Sindhu Bhavan, Iskon Mandir, Ramdev Nagar, Radhaswami Satsang Satellite Gate, Abhishree Complex, Kirti Sagar Apartment, Butbhavani Mata Mandir, Shanti Niketan Ranip Vidyalaya, Vejalpur Road, Juhapura, Pravin Nagar, Vasna Terminus Gayatri Vidyalay Vimal Tenament Ramwadi(Madhav Bagh) Deshwali Society Shankar Da Hall Chhaya Flats R. -

MATHEMATICS Textbook for Class VIII

https://ncertpdf.in MATHEMATICS Textbook for Class VIII 2019-20 https://ncertpdf.in ISBN 978-81-7450-814-0 First Edition January 2008 Magha 1929 ALL RIGHTS RESERVED Reprinted January 2009 Pausa 1930 q No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, January 2010 Magha 1931 photocopying, recording or otherwise without the prior permission of the November 2010 Kartika 1932 publisher. January 2012 Magha 1933 q This book is sold subject to the condition that it shall not, by way of trade, be November 2012 Kartika 1934 lent, re-sold, hired out or otherwise disposed of without the publisher’s November 2013 Kartika 1935 consent, in any form of binding or cover other than that in which it is published. November 2014 Kartika 1936 q The correct price of this publication is the price printed on this page, Any revised price indicated by a rubber stamp or by a sticker or by any other December 2015 Agrahayna 1937 means is incorrect and should be unacceptable. December 2016 Pausa 1938 December 2017 Pausa 1939 January 2019 Pausa 1940 PD 900T RPS OFFICES OF THE PUBLICATION DIVISION, NCERT © National Council of Educational NCERT Campus Research and Training, 2008 Sri Aurobindo Marg New Delhi 110 016 Phone : 011-26562708 108, 100 Feet Road Hosdakere Halli Extension Banashankari III Stage Bengaluru 560 085 Phone : 080-26725740 Navjivan Trust Building P.O. Navjivan Ahmedabad 380 014 Phone : 079-27541446 CWC Campus Opp. Dhankal Bus Stop Panihati Kolkata 700 114 Phone : 033-25530454 CWC Complex Maligaon Guwahati 781 021 Phone : 0361-2674869 ` 60.00 Publication Team Head, Publication : M. -

87 Bus Time Schedule & Line Route

87 bus time schedule & line map 87 Kalupur Terminus - Chandkheda View In Website Mode The 87 bus line (Kalupur Terminus - Chandkheda) has 2 routes. For regular weekdays, their operation hours are: (1) Chandkheda: 6:40 AM - 9:30 PM (2) Kalupur Terminus: 7:50 AM - 10:40 PM Use the Moovit App to ƒnd the closest 87 bus station near you and ƒnd out when is the next 87 bus arriving. Direction: Chandkheda 87 bus Time Schedule 26 stops Chandkheda Route Timetable: VIEW LINE SCHEDULE Sunday 6:40 AM - 9:30 PM Monday 6:40 AM - 9:30 PM Maninagar Maninagar Railway Station, Ahmadābād Tuesday 6:40 AM - 9:30 PM Jawahar Chowk Wednesday 6:40 AM - 9:30 PM Bhairavnath Thursday 6:40 AM - 9:30 PM Friday 6:40 AM - 9:30 PM Sah Alam Darwaja Saturday 6:40 AM - 9:30 PM S. T. Stand Kamnath Mahadev / Raipur Darwaja Sarangpur 87 bus Info Direction: Chandkheda Kalupur Stops: 26 Trip Duration: 47 min Naroda Road, Ahmadābād Line Summary: Maninagar, Jawahar Chowk, Prem Darwaja Bhairavnath, Sah Alam Darwaja, S. T. Stand, Kamnath Mahadev / Raipur Darwaja, Sarangpur, Kalupur, Prem Darwaja, Dariyapur Darwaja, Delhi Dariyapur Darwaja Darwaja, Income Tax O∆ce, Usmanpura, Vadaj Bus Terminuss, Subhash Bridge, Keshav Nagar, Delhi Darwaja Dharmanagar, Ram Nagar, Chintamani Society, Abu Koba Cross Road, Gujarat Stadium, Motera Gam, Income Tax O∆ce Government Engineering College, Santokba Hospital, Shivshakti Nagar, Chandkheda Usmanpura Vadaj Bus Terminuss Subhash Bridge Keshav Nagar Dharmanagar Ram Nagar Chintamani Society Abu Koba Cross Road Ram Bag Road, Ahmadābād Gujarat Stadium -

Asset Recovery Department STAR MEGA E-AUCTION Relationship Beyond Banking 6Th Floor, Bank of India Building, Bhadra, Ahmedabad

Asset Recovery Department STAR MEGA E-AUCTION Relationship beyond banking 6th Floor, Bank of India Building, Bhadra, Ahmedabad. Phone : 079 - 25380162 FOR SALE OF PROPERTIES SALE NOTICE FOR SALE OF IMMOVABLE & MOVABLE PROPERTIES DATE AND TIME OF E-AUCTION : 30.09.2019, 12:00 NOON TO 02.00 PM WITH AUTO EXTENSION CLAUSE INCASE OF BID IN LAST 5 MINUTES BEFORE CLOSING E-AUCTION SALE NOTICE FOR SALE OF IMMOVABLE AND MOVABLE ASSETS UNDER THE SECURITISATION AND RECONSTRUCTION OF FINANCIAL ASSETS AND ENFORCEMENT OF SECURITY INTEREST ACT, 2002 READ WITH PROVISO TO RULE 8 (6) AND 6(2) OF THE SECURITY INTEREST (ENFORCEMENT) RULES, 2002. Notice is hereby given to the public in general and in particular to the Borrower(s) and Guarantor(s) that the below described immovable & movable property mortgaged / hypothecated / charged to the Secured Creditor. The physical possession of which has been taken by the respective Authorised Officer of Bank of India ‘the Secured Creditor’, will be sold on “As is where is”, As is what is”, and Whatever there is” basis on 30.09.2019 for recovery of Rs. (as mentioned below respectively) due to the said Secured Creditor from the Borrower(s) and Guarantor(s) as mentioned below respectively. The Reserve Price and the Earnest Money Deposit will be as mentioned below. The Auction will be “Online E-Auctioning” through website https://boi.auctiontiger.net DESCRIPTION OF THE IMMOVABLE AND MOVABLE PROPERTIES WITH KNOWN ENCUMBRANCES IF ANY Name of Borrower / Guarantor & Address & Name of the Branch Reserve EMD Sr. Description of Properties No. & Outstanding Dues Price Price 1 M/s. -

Developer Details

Developer Details Reg. No. Name Type Resident Address Office Address Mobile No. Reg. Date Validity Date Email ID DEV/00898 Zarna Developers Developer as above 5, Shiv Darshan 9825190196 28-Sep-2015 27-Sep-2020 [email protected] Sandipbhai B Kakadiya Bunglows, Opp. Shreeram DEV/00899 LAXMINARAYAN Developer 11, GIRIRAJ COLONY, 11, GIRIRAJ 9825034144 28-Sep-2015 27-Sep-2020 [email protected] INFRASRTUCUTRE PANCHVATI, COLONY, MANOJKUMAR AAMBAWADI, PANCHVATI, DEV/00900 Shrinand Buildcon Developer as above 1, S.F, Shreedhar 9825061073 16-Oct-2015 15-Oct-2020 [email protected] Jayantilal Nagjibhai Bunglows, Opp. Patel Grand Bhagwati, DEV/00901 SHREE SARJU Developer 9, Swagat Mahal, Near 9, Swagat Mahal, 9727442416 27-Oct-2015 26-Oct-2020 [email protected] BUILDERS Matrushree Party Plot, Near Matrushree CHANDRESHKUMAR Chandkheda , Party Plot, DEV/00902 PATEL DHIREN Developer B-6, MILAP B-6, MILAP 7096638633 03-Nov-2015 02-Nov-2020 [email protected] PRAHLADBHAI APPARTMENT, OPP. APPARTMENT, RANAKPUR SOC, OPP. RANAKPUR DEV/00903 SATASIYA Developer 14, SUROHI PARK 14, SUROHI PARK 9898088520 05-Nov-2015 04-Nov-2020 [email protected] PRAKASHBHAI PART-2,OPP.SUKAN PART-2, KARSHANBHAI BUNGLOWS AUDA T.P OPP.SUKAN DEV/00904 KARNAVATI Developer 17/A, KAMLA SOC, 17/A, KAMLA SOC, 9824015660 24-Nov-2015 23-Nov-2020 [email protected] BUILDERS RAMANI STADIUM ROAD, STADIUM ROAD, BHISHAM J NAVRANGPURA, NAVRANGPURA, DEV/00905 PATEL Developer F/101, SANGATH F/101, SANGATH 9925018327 01-Dec-2015 30-Nov-2020 [email protected] MALAYKUMAR SILVER, B/H D MART SILVER, B/H D BHARATBHAI MALL MOTERA, MART MALL DEV/00906 Harikrupa Developers Developer As Above 6, Ishan Park 7874377897 11-Dec-2015 10-Dec-2020 [email protected] Prajapati Jaymesh Society, Nr. -

Behrouz Biryani

Online Offer – Behrouz Biryani: • G 42, Shree Mahalaxmi Shops, Rudra Square, Bodakdev, Ahmedabad • 25, Rivera Arcade, Near Prahlad Nagar Garden, Prahlad Nagar, Ahmedabad • 2, IM Complex, Vastrapur Lake, Vastrapur, Ahmedabad • G/F 1, Animesh Complex, Panchavati Ellis Bridge, Near Chandra Colony, C G Road, Ahmedabad • 14, Ground Floor, Vitthal the Mall, Near Swagat Status, Chandkheda • C-19-20 Swagat Rainforest 2, Village Kudasan, Ta and District, Airport Gandhinagar Highway, Gandhinagar, Ahmedabad • 7th Cross Road, 8th Main, BTM Layout, Bangalore • Near Sony World Signal, Koramangala 6th Block, Bangalore • Kodichikkanahalli Main Road, Begur Hobli, Bommanahalli, Bangalore • Ground Floor, Actove Hotel, Kadubisanahalli, Marathahalli, Bangalore • Food Court, Sjr I-Park, Built In, Whitefield, Bangalore • Old Airport Road, Old Airport Road, Bangalore • Devatha Plaza, Residency Road, Bangalore • 123, Kamala Complex, AECS Layout, ITPL Main Road, Whitefield, Bangalore • 2318, Sector 1, Near NIFT College, HSR Layout, Bangalore • Kaggadaspura, CV Raman Nagar, Bangalore • Shop A-94 6/2, Opposite State Bank of India, 2nd Phase, J P Nagar, Bangalore • 101, Ground Floor, Manjunatha Complec, 22nd Main Road, 2nd Stage, Banashankari, Bangalore • Site No 8, New No 1, Channasandra, Property No 121, 2nd Main Road, Kr Puram Hobli, Kasturi Nagar, Bangalore • Shop 10-11, Electronic City Phase-1, 2nd Cross Road, Near Infosys Gate 1, Bangalore • 2283, 1st Main Road, Sahakar Nagar D Block, Bangalore • 3, 1st Floor, Apple City, Kadugodi Hoskote, Main Road, Seegehalli, Bangalore • Shop No. 837, BEML 3rd Stage, Halagevaderahalli, Rajarajeshwari Nagar, Bangalore • Dodaballapur Main Road, Puttenahalli, Yelahanka, Bangalore • Colony Skylineapartment, Canara Bank, Chandra Layout, Bangalore • Shop No. 90, First Floor, Sanjay Nagar Main Road, Geddalahalli, Bangalore • 6, First Floor, 9 Cross, 2nd Main, Binnamangala, 1st Stage, Indiranagar, Bangalore • Shop No. -

Sr. No Age Sex Address 1 64 M Sundarlal Ni Chali, Near

COVID ‐ 19 POSITIVE CASE LIST 05.05.2020, 08:00 PM SR. NO AGE SEX ADDRESS SUNDARLAL NI CHALI, NEAR SANGEETHA FURNITURE, 164M SAIJPUR, AHMEDABAD. 46, PATANI, SANJOGNAGAR, MEGHANINAGAR, 28F AHMEDABAD. 46, PATANI, SANJOGNAGAR, MEGHANINAGAR, 314F AHMEDABAD. 45, BHAVSAR NI CHALI, OPP. SHARDABEN HOSPITAL, 448M SARASPUR, AHMEDABAD. 5 57 M 753/3, AMBAVDI, SARDARNAGAR, AHMEDABAD. 6 25 F 753/2, AMBAVDI, SARDARNAGAR, AHMEDABAD. 7 28 F 753/2, AMBAVDI, SARDARNAGAR, AHMEDABAD. 8 26 M 753/3, AMBAVDI, SARDARNAGAR, AHMEDABAD. 9 8 M 753/3, AMBAVDI, SARDARNAGAR, AHMEDABAD. C‐2, SURDHARA SOCIETY, OPP. RAMINI CHALI, RAKHIAL, 10 35 F AHMEDABAD. C‐2, SURDHARA SOCIETY, OPP. RAMINI CHALI, RAKHIAL, 11 32 F AHMEDABAD. 54, BHOIWALA NI POLE, DILLI CHAKLA, SHAHPUR, 12 33 M AHMEDABAD. 52/1233, GUJRAT HOUSING BOARD, MEGHANINAGAR, 13 45 M AHMEDABAD. 6, HIREN APARTMENT, RAMNAGAR, SABARMATI, 14 53 M AHMEDABAD. 3603, MOTI VHORWAD, ASTODIYA KAJI NA DHABA, 15 56 F JAMALPUR, AHMEDABAD. A‐10, GUIMOHAR SOCIETY, NEAR THE NEW AGE SCHOOL, 16 55 M OPP. MEMON HALL, JUHAPURA‐SARKHEJ ROAD, AHMEDABAD. 206, 2/F, MADNI APARTMENT, KAZI NA DHABA, 17 54 F ASTODIA, AHMEDABAD. SR. NO AGE SEX ADDRESS 22, SHREEMAT SOCIETY, NR DUDHWALI CHALI, MELDI 18 62 F MATA NU MANDIR, BEHRAMPURA, AHMEDABAD. 181, SARVODAY NAGAR SOCIETY, OUTSIDE SHAHPUR 19 30 F GATE, SHAHPUR, AHMEDABAD. 20 75 F 1, MANMANDIR ROW HOUSE, VEJALPUR, AHMEDABAD. VASUDEV DHANJEE NICHALI, GITA MANDIR, 21 32 F AHMEDABAD. 45/K, RATAN POL, SHETH NI POL, MANEK CHOWK, 22 35 F AHMEDABAD. MAHAJAN NO VANDDO, VASANT NAGAR POLICE 23 50 M STATION SAME, JAMALPUR, AHMEDABAD. -

JP Iscon Riverside

https://www.propertywala.com/jp-iscon-riverside-ahmedabad JP Iscon Riverside - Shahibag, Ahmedabad 3 & 4 BHK apartments for sale in JP Iscon Riverside JP Iscon Riverside presented by JP Iscon Group with 3 & 4 BHK apartments for sale in Shahibaug, Ahmedabad Project ID : J811899297 Builder: JP Iscon Group Location: JP River Side, Shahibag, Ahmedabad - 440034 (Gujarat) Completion Date: May, 2016 Status: Started Description JP River Side Woods is a new launch by JP Iscon Group. The project is located in Shahibaug, Ahmedabad. The project offers spacious 3 & 4 BHK apartments in best price. The project is well equipped with all the amenities to facilitate the needs of the residents. Project Details Number of Floors: 1 Number of Units: 7 Amenities Garden 24Hr Backup Security Club House Library Community Hall Swimming Pool Gymnasium Indoor Games JP Iscon Group is today among Gujarat’s pre-eminent real estate developers, with a widespread corporate reputation founded on benchmark performance. The group is famous today for its diverse repertoire of architectural expertise, its inherent streak of innovation, time-conscious planning & execution of projects, and highly evolved skill in property management. Features Luxury Features Security Features Power Back-up Centrally Air Conditioned Lifts Electronic Security Intercom Facility RO System High Speed Internet Wi-Fi Interior Features Recreation Woodwork Modular Kitchen Swimming Pool Fitness Centre / GYM Feng Shui / Vaastu Compliant Club / Community Center Maintenance Land Features Maintenance Staff -

Sr No. RTO Name Dealer Name Dealer Address 1 Ahmedabad Kataria Automobile Kataria Automobiles Makarba Ahmedabad 2 Ahmedabad TORQUE AUTOMOTIVE PVT.LTD

Sr No. RTO_Name Dealer_Name Dealer_Address 1 Ahmedabad Kataria Automobile Kataria Automobiles Makarba Ahmedabad 2 Ahmedabad TORQUE AUTOMOTIVE PVT.LTD. OPP. LJ CAMPUS, NR. SARKHEJ-SANAND CIRCLE, S.G. ROAD, AHMEDABAD 3 Ahmedabad KATARIA MOTORS PVT LTD OPP. GIDC APPAREL PARK, NR.ANUPAM CINEMA, KHOKHARA MANINAGAR AHMEDABAD 4 Ahmedabad KAVERI MOTORS G-22, SATYMEV COMPLEX, OPP. GUJARAT HIGH COURT, S.G. ROAD, AHMEDABAD-380060 5 Ahmedabad KATARIA MOTORS PVT LTD 103 B S G HIGHWAY SANAND AHMEDABAD 6 Ahmedabad KATARIA CARS PVT LTD VEDANT BEHIND YMCA CLUB S G HIGHWAY MAKARBA AHMEDABAD 7 Ahmedabad PUNJAB HONDA PUNJAB HONDA 5 MARUTI CENTER, NEAR HIMALAYA MALL DRIVE IN ROAD, AHMEDABAD 8 Ahmedabad WEST SIDE CARS PVT LTD FORD: G/F BLOCK A, SOLITAIRE BUSINESS PARK, S.G. ROAD, MAKARBA, AHMEDABAD 9 Ahmedabad AMIN AUTOMOBILES LALDARWAJA AHMEDABAD 10 Ahmedabad UNIVERSAL AUTO PRODUCTS NEHRU BRIDGE LAL DARWAJA AHMEDABAD 11 Ahmedabad GLOBAL MOTORS Polaris, Opp. Vipul Dudhiya, Stadium Road, Swastik Society, Navrangpura, Ahmedabad 12 Ahmedabad KATARIA AUTOMOBILES MANINAGAR KATARIA AUTOMOBILES PVT. LTD. OPP. GIDC APPAREL PARK NEAR KHOKRA BRIDGE KHOKHARA MANINAGAR 13 Ahmedabad KATARIA AUTOMOBILES DARIYAPUR NR. K.S. LOKHANDWALA COMPOUND OUT SIDE DARIYAPUR DARWAJA AHMEDABAD 380016. 14 Ahmedabad APEX AUTOMOTIVE APEX AUTOMOTIVE, KANKARIYA SHAHEALAM MANINAGAR AHMEDABAD 15 Ahmedabad INNOVATIVE HONDA INNOVATIVE HONDA, 4, GANESH PLAZA, OFF. C.G.ROAD, NAVRANGPURA, AHMEDABAD 16 Ahmedabad SHIVALIK IB AUTOGEM PVT LTD Shivalik Hyundai Vedant, Ground Floor, Near YMCA International -

Thaltej Village: an Incremental Approach to Urban Encroachment

Thaltej Village: An Incremental Approach to Urban Encroachment Thaltej Village: An Incremental Approach to Urban Encroachment Emily Brown Allison Buchwach Ryan Hagerty Mary Richardson Laura Schultz Bin Yan Under the advisement of Professor Michael Dobbins Georgia Institute of Technology April 27, 2012 Acknowlegements This report was produced with help from faculty and students at CEPT University in Ahmdebad, as well as many other generous folks both here and abroad that have helped us immeasurably with their advice, insight and feedback along the way. To all, we extend our heartfelt gratitude. Contents 1 INTRODUCTION ............................................................................................................................................. 1 2 INDIAN NATIONAL CONTEXT ......................................................................................................................... 3 2.1 INDIA’S URBANIZATION AND ITS IMPACT ON SLUMS AND THE ENVIRONMENT ................................................................ 3 2.2 IMPACT OF URBANIZATION: ENVIRONMENTAL DEGRADATION .................................................................................... 5 2.3 POLICY RESPONSES ............................................................................................................................................ 6 2.4 POLICY RESPONSES ............................................................................................................................................ 8 2.4.1 Slum Clearance (1956) ............................................................................................................................ -

Ahmedabad Municipal Corporation Councillor List (Term 2021-2026)

Ahmedabad Municipal Corporation Councillor List (term 2021-2026) Ward No. Sr. Mu. Councillor Address Mobile No. Name No. 1 1-Gota ARATIBEN KAMLESHBHAI CHAVDA 266, SHIVNAGAR (SHIV PARK) , 7990933048 VASANTNAGAR TOWNSHIP, GOTA, AHMEDABAD‐380060 2 PARULBEN ARVINDBHAI PATEL 291/1, PATEL VAS, GOTA VILLAGE, 7819870501 AHMEDABAD‐382481 3 KETANKUMAR BABULAL PATEL B‐14, DEV BHUMI APPARTMENT, 9924136339 SATTADHAR CROSS ROAD, SOLA ROAD, GHATLODIA, AHMEDABAD‐380061 4 AJAY SHAMBHUBHAI DESAI 15, SARASVATINAGAR, OPP. JANTA 9825020193 NAGAR, GHATLODIA, AHMEDABAD‐ 380061 5 2-Chandlodia RAJESHRIBEN BHAVESHBHAI PATEL H/14, SHAYONA CITY PART‐4, NR. R.C. 9687250254, 8487832057 TECHNICAL ROAD, CHANDLODIA‐ GHATLODIA, AHMDABAD‐380061 6 RAJESHWARIBEN RAMESHKUMAR 54, VINAYAK PARK, NR. TIRUPATI 7819870503, PANCHAL SCHOOL, CHANDLODIA, AHMEDABAD‐ 9327909986 382481 7 HIRABHAI VALABHAI PARMAR 2, PICKERS KARKHANA ,NR. 9106598270, CHAMUDNAGAR,CHANDLODIYA,AHME 9913424915 DABAD‐382481 8 BHARATBHAI KESHAVLAL PATEL A‐46, UMABHAVANI SOCIETY, TRAGAD 7819870505 ROAD, TRAGAD GAM, AHMEDABAD‐ 382470 9 3- PRATIMA BHANUPRASAD SAXENA BUNGLOW NO. 320/1900, Vacant due to Chandkheda SUBHASNAGAR, GUJ. HO.BOARD, resignation of Muni. CHANDKHEDA, AHMEDABAD‐382424 Councillor 10 RAJSHRI VIJAYKUMAR KESARI 2,SHYAM BANGLOWS‐1,I.O.C. ROAD, 7567300538 CHANDKHEDA, AHEMDABAD‐382424 11 RAKESHKUMAR ARVINDLAL 20, AUTAMNAGAR SOC., NR. D CABIN 9898142523 BRAHMBHATT FATAK, D CABIN SABARMATI, AHMEDABAD‐380019 12 ARUNSINGH RAMNYANSINGH A‐27,GOPAL NAGAR , CHANDKHEDA, 9328784511 RAJPUT AHEMDABAD‐382424 E:\BOARDDATA\2021‐2026\WEBSITE UPDATE INFORMATION\MUNICIPAL COUNCILLOR LIST IN ENGLISH 2021‐2026 TERM.DOC [ 1 ] Ahmedabad Municipal Corporation Councillor List (term 2021-2026) Ward No. Sr. Mu. Councillor Address Mobile No. Name No. 13 4-Sabarmati ANJUBEN ALPESHKUMAR SHAH C/O. BABULAL JAVANMAL SHAH , 88/A 079- 27500176, SHASHVAT MAHALAXMI SOCIETY, RAMNAGAR, SABARMATI, 9023481708 AHMEDABAD‐380005 14 HIRAL BHARATBHAI BHAVSAR C‐202, SANGATH‐2, NR.