The Bermudan Swaptions Pricing Odyssey

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

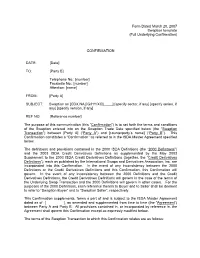

Form Dated March 20, 2007 Swaption Template (Full Underlying Confirmation)

Form Dated March 20, 2007 Swaption template (Full Underlying Confirmation) CONFIRMATION DATE: [Date] TO: [Party B] Telephone No.: [number] Facsimile No.: [number] Attention: [name] FROM: [Party A] SUBJECT: Swaption on [CDX.NA.[IG/HY/XO].____] [specify sector, if any] [specify series, if any] [specify version, if any] REF NO: [Reference number] The purpose of this communication (this “Confirmation”) is to set forth the terms and conditions of the Swaption entered into on the Swaption Trade Date specified below (the “Swaption Transaction”) between [Party A] (“Party A”) and [counterparty’s name] (“Party B”). This Confirmation constitutes a “Confirmation” as referred to in the ISDA Master Agreement specified below. The definitions and provisions contained in the 2000 ISDA Definitions (the “2000 Definitions”) and the 2003 ISDA Credit Derivatives Definitions as supplemented by the May 2003 Supplement to the 2003 ISDA Credit Derivatives Definitions (together, the “Credit Derivatives Definitions”), each as published by the International Swaps and Derivatives Association, Inc. are incorporated into this Confirmation. In the event of any inconsistency between the 2000 Definitions or the Credit Derivatives Definitions and this Confirmation, this Confirmation will govern. In the event of any inconsistency between the 2000 Definitions and the Credit Derivatives Definitions, the Credit Derivatives Definitions will govern in the case of the terms of the Underlying Swap Transaction and the 2000 Definitions will govern in other cases. For the purposes of the 2000 Definitions, each reference therein to Buyer and to Seller shall be deemed to refer to “Swaption Buyer” and to “Swaption Seller”, respectively. This Confirmation supplements, forms a part of and is subject to the ISDA Master Agreement dated as of [ ], as amended and supplemented from time to time (the “Agreement”) between Party A and Party B. -

5. Caps, Floors, and Swaptions

Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Interest Rate and Credit Models 5. Caps, Floors, and Swaptions Andrew Lesniewski Baruch College New York Spring 2019 A. Lesniewski Interest Rate and Credit Models Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Outline 1 Options on LIBOR based instruments 2 Valuation of LIBOR options 3 Local volatility models 4 The SABR model 5 Volatility cube A. Lesniewski Interest Rate and Credit Models Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Options on LIBOR based instruments Interest rates fluctuate as a consequence of macroeconomic conditions, central bank actions, and supply and demand. The existence of the term structure of rates, i.e. the fact that the level of a rate depends on the maturity of the underlying loan, makes the dynamics of rates is highly complex. While a good analogy to the price dynamics of an equity is a particle moving in a medium exerting random shocks to it, a natural way of thinking about the evolution of rates is that of a string moving in a random environment where the shocks can hit any location along its length. A. Lesniewski Interest Rate and Credit Models Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Options on LIBOR based instruments Additional complications arise from the presence of various spreads between rates, as discussed in Lecture Notes #1, which reflect credit quality of the borrowing entity, liquidity of the instrument, or other market conditions. -

Interest Rate Modelling and Derivative Pricing

Interest Rate Modelling and Derivative Pricing Sebastian Schlenkrich HU Berlin, Department of Mathematics WS, 2019/20 Part III Vanilla Option Models p. 140 Outline Vanilla Interest Rate Options SABR Model for Vanilla Options Summary Swaption Pricing p. 141 Outline Vanilla Interest Rate Options SABR Model for Vanilla Options Summary Swaption Pricing p. 142 Outline Vanilla Interest Rate Options Call Rights, Options and Forward Starting Swaps European Swaptions Basic Swaption Pricing Models Implied Volatilities and Market Quotations p. 143 Now we have a first look at the cancellation option Interbank swap deal example Bank A may decide to early terminate deal in 10, 11, 12,.. years. p. 144 We represent cancellation as entering an opposite deal L1 Lm ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ T˜0 T˜k 1 T˜m − ✲ T0 TE Tl 1 Tn − ❄ ❄ ❄ ❄ ❄ ❄ K K [cancelled swap] = [full swap] + [opposite forward starting swap] K ✻ ✻ Tl 1 Tn − ✲ TE T˜k 1 T˜m − ❄ ❄ ❄ ❄ Lm p. 145 Option to cancel is equivalent to option to enter opposite forward starting swap K ✻ ✻ Tl 1 Tn − ✲ TE T˜k 1 T˜m − ❄ ❄ ❄ ❄ Lm ◮ At option exercise time TE present value of remaining (opposite) swap is n m Swap δ V (TE ) = K · τi · P(TE , Ti ) − L (TE , T˜j 1, T˜j 1 + δ) · τ˜j · P(TE , T˜j ) . − − i=l j=k X X future fixed leg future float leg | {z } | {z } ◮ Option to enter represents the right but not the obligation to enter swap. ◮ Rational market participant will exercise if swap present value is positive, i.e. Option Swap V (TE ) = max V (TE ), 0 . -

Introduction to Black's Model for Interest Rate

INTRODUCTION TO BLACK'S MODEL FOR INTEREST RATE DERIVATIVES GRAEME WEST AND LYDIA WEST, FINANCIAL MODELLING AGENCY© Contents 1. Introduction 2 2. European Bond Options2 2.1. Different volatility measures3 3. Caplets and Floorlets3 4. Caps and Floors4 4.1. A call/put on rates is a put/call on a bond4 4.2. Greeks 5 5. Stripping Black caps into caplets7 6. Swaptions 10 6.1. Valuation 11 6.2. Greeks 12 7. Why Black is useless for exotics 13 8. Exercises 13 Date: July 11, 2011. 1 2 GRAEME WEST AND LYDIA WEST, FINANCIAL MODELLING AGENCY© Bibliography 15 1. Introduction We consider the Black Model for futures/forwards which is the market standard for quoting prices (via implied volatilities). Black[1976] considered the problem of writing options on commodity futures and this was the first \natural" extension of the Black-Scholes model. This model also is used to price options on interest rates and interest rate sensitive instruments such as bonds. Since the Black-Scholes analysis assumes constant (or deterministic) interest rates, and so forward interest rates are realised, it is difficult initially to see how this model applies to interest rate dependent derivatives. However, if f is a forward interest rate, it can be shown that it is consistent to assume that • The discounting process can be taken to be the existing yield curve. • The forward rates are stochastic and log-normally distributed. The forward rates will be log-normally distributed in what is called the T -forward measure, where T is the pay date of the option. -

Dixit-Pindyck and Arrow-Fisher-Hanemann-Henry Option Concepts in a Finance Framework

Dixit-Pindyck and Arrow-Fisher-Hanemann-Henry Option Concepts in a Finance Framework January 12, 2015 Abstract We look at the debate on the equivalence of the Dixit-Pindyck (DP) and Arrow-Fisher- Hanemann-Henry (AFHH) option values. Casting the problem into a financial framework allows to disentangle the discussion without unnecessarily introducing new definitions. Instead, the option values can be easily translated to meaningful terms of financial option pricing. We find that the DP option value can easily be described as time-value of an American plain-vanilla option, while the AFHH option value is an exotic chooser option. Although the option values can be numerically equal, they differ for interesting, i.e. non-trivial investment decisions and benefit-cost analyses. We find that for applied work, compared to the Dixit-Pindyck value, the AFHH concept has only limited use. Keywords: Benefit cost analysis, irreversibility, option, quasi-option value, real option, uncertainty. Abbreviations: i.e.: id est; e.g.: exemplum gratia. 1 Introduction In the recent decades, the real options1 concept gained a large foothold in the strat- egy and investment literature, even more so with Dixit & Pindyck (1994)'s (DP) seminal volume on investment under uncertainty. In environmental economics, the importance of irreversibility has already been known since the contributions of Arrow & Fisher (1974), Henry (1974), and Hanemann (1989) (AFHH) on quasi-options. As Fisher (2000) notes, a unification of the two option concepts would have the benefit of applying the vast results of real option pricing in environmental issues. In his 1The term real option has been coined by Myers (1977). -

Finance II (Dirección Financiera II) Apuntes Del Material Docente

Finance II (Dirección Financiera II) Apuntes del Material Docente Szabolcs István Blazsek-Ayala Table of contents Fixed-income securities 1 Derivatives 27 A note on traditional return and log return 78 Financial statements, financial ratios 80 Company valuation 100 Coca-Cola DCF valuation 135 Bond characteristics A bond is a security that is issued in FIXED-INCOME connection with a borrowing arrangement. SECURITIES The borrower issues (i.e. sells) a bond to the lender for some amount of cash. The arrangement obliges the issuer to make specified payments to the bondholder on specified dates. Bond characteristics Bond characteristics A typical bond obliges the issuer to make When the bond matures, the issuer repays semiannual payments of interest to the the debt by paying the bondholder the bondholder for the life of the bond. bond’s par value (or face value ). These are called coupon payments . The coupon rate of the bond serves to Most bonds have coupons that investors determine the interest payment: would clip off and present to claim the The annual payment is the coupon rate interest payment. times the bond’s par value. Bond characteristics Example The contract between the issuer and the A bond with par value EUR1000 and coupon bondholder contains: rate of 8%. 1. Coupon rate The bondholder is then entitled to a payment of 8% of EUR1000, or EUR80 per year, for the 2. Maturity date stated life of the bond, 30 years. 3. Par value The EUR80 payment typically comes in two semiannual installments of EUR40 each. At the end of the 30-year life of the bond, the issuer also pays the EUR1000 value to the bondholder. -

Value at Risk for Linear and Non-Linear Derivatives

Value at Risk for Linear and Non-Linear Derivatives by Clemens U. Frei (Under the direction of John T. Scruggs) Abstract This paper examines the question whether standard parametric Value at Risk approaches, such as the delta-normal and the delta-gamma approach and their assumptions are appropriate for derivative positions such as forward and option contracts. The delta-normal and delta-gamma approaches are both methods based on a first-order or on a second-order Taylor series expansion. We will see that the delta-normal method is reliable for linear derivatives although it can lead to signif- icant approximation errors in the case of non-linearity. The delta-gamma method provides a better approximation because this method includes second order-effects. The main problem with delta-gamma methods is the estimation of the quantile of the profit and loss distribution. Empiric results by other authors suggest the use of a Cornish-Fisher expansion. The delta-gamma method when using a Cornish-Fisher expansion provides an approximation which is close to the results calculated by Monte Carlo Simulation methods but is computationally more efficient. Index words: Value at Risk, Variance-Covariance approach, Delta-Normal approach, Delta-Gamma approach, Market Risk, Derivatives, Taylor series expansion. Value at Risk for Linear and Non-Linear Derivatives by Clemens U. Frei Vordiplom, University of Bielefeld, Germany, 2000 A Thesis Submitted to the Graduate Faculty of The University of Georgia in Partial Fulfillment of the Requirements for the Degree Master of Arts Athens, Georgia 2003 °c 2003 Clemens U. Frei All Rights Reserved Value at Risk for Linear and Non-Linear Derivatives by Clemens U. -

Term Structure Lattice Models

Term Structure Models: IEOR E4710 Spring 2005 °c 2005 by Martin Haugh Term Structure Lattice Models 1 The Term-Structure of Interest Rates If a bank lends you money for one year and lends money to someone else for ten years, it is very likely that the rate of interest charged for the one-year loan will di®er from that charged for the ten-year loan. Term-structure theory has as its basis the idea that loans of di®erent maturities should incur di®erent rates of interest. This basis is grounded in reality and allows for a much richer and more realistic theory than that provided by the yield-to-maturity (YTM) framework1. We ¯rst describe some of the basic concepts and notation that we need for studying term-structure models. In these notes we will often assume that there are m compounding periods per year, but it should be clear what changes need to be made for continuous-time models and di®erent compounding conventions. Time can be measured in periods or years, but it should be clear from the context what convention we are using. Spot Rates: Spot rates are the basic interest rates that de¯ne the term structure. De¯ned on an annual basis, the spot rate, st, is the rate of interest charged for lending money from today (t = 0) until time t. In particular, 2 mt this implies that if you lend A dollars for t years today, you will receive A(1 + st=m) dollars when the t years have elapsed. -

Solution to the Chooser Question

Solution to the Chooser Question The payoff of the chooser option at time 1 is given by max[C(S1,X,1),P(S1,X,1)], where C(S1,X,1) is the value of a call option that matures at time 2, with exercise price X and stock price S1. Put call parity implies that at time 1, C(S1,X,1)- P(S1,X,1)=S1-X/R. Substituting in for the value of the put, the chooser payoff at time 1 is given by max[C(S1,X,1),C(S1,X,1)- S1+X/R]= C(S1,X,1)+max[0,X/R-S1]. But, max[0,X/R-S1] is the payoff of a put option that expires at time 1, with exercise price X/R. So, at time 0, the value of the chooser must be equal to C(S0,X,2)+P(S0,X/R,1). We can then use put call parity again to substitute out the value of the one period put in terms of a one period call, giving us the final result that the 2 chooser payoff equals C(S0,X,2)+ C(S0,X/R,1)-S0+X/R . You would likely purchase the chooser option of you wanted a positive payoff in the tails of the distribution of the underlying return in the future. To solve for the value of the chooser, we work recursively through the tree. The call option payoffs are given by Cuu=Max(15.625-10,0)=5.625 Cu C0 Cud=Max(10-10,0)=0 Cd Cdd=Max(6.4-10,0)=0 Clearly, after the first down move, the call is worthless. -

FX Options and Structured Products

FX Options and Structured Products Uwe Wystup www.mathfinance.com 7 April 2006 www.mathfinance.de To Ansua Contents 0 Preface 9 0.1 Scope of this Book ................................ 9 0.2 The Readership ................................. 9 0.3 About the Author ................................ 10 0.4 Acknowledgments ................................ 11 1 Foreign Exchange Options 13 1.1 A Journey through the History Of Options ................... 13 1.2 Technical Issues for Vanilla Options ....................... 15 1.2.1 Value ................................... 16 1.2.2 A Note on the Forward ......................... 18 1.2.3 Greeks .................................. 18 1.2.4 Identities ................................. 20 1.2.5 Homogeneity based Relationships .................... 21 1.2.6 Quotation ................................ 22 1.2.7 Strike in Terms of Delta ......................... 26 1.2.8 Volatility in Terms of Delta ....................... 26 1.2.9 Volatility and Delta for a Given Strike .................. 26 1.2.10 Greeks in Terms of Deltas ........................ 27 1.3 Volatility ..................................... 30 1.3.1 Historic Volatility ............................ 31 1.3.2 Historic Correlation ........................... 34 1.3.3 Volatility Smile .............................. 35 1.3.4 At-The-Money Volatility Interpolation .................. 41 1.3.5 Volatility Smile Conventions ....................... 44 1.3.6 At-The-Money Definition ........................ 44 1.3.7 Interpolation of the Volatility on Maturity -

Download Download

CBU INTERNATIONAL CONFERENCE ON INNOVATION, TECHNOLOGY TRANSFER AND EDUCATION MARCH 25-27, 2015, PRAGUE, CZECH REPUBLIC WWW.CBUNI.CZ, OJS.JOURNALS.CZ MODIFICATION OF DELTA FOR CHOOSER OPTIONS Marek Ďurica1 Abstract: Correctly used financial derivatives can help investors increase their expected returns and minimize their exposure to risk. To ensure the specific needs of investors, a large number of different types of non- standard exotic options is used. Chooser option is one of them. It is an option that gives its holder the right to choose at some predetermined future time whether the option will be a standard call or put with predetermined strike price and maturity time. Although the chooser options are more expensive than standard European-style options, in many cases they are a more suitable instrument for investors in hedging their portfolio value. For an effective use of the chooser option as a hedging instrument, it is necessary to check the values of the Greek parameters delta and gamma for the options. Especially, if the value of the parameter gamma is too large, hedging of the portfolio value using only parameter delta is insufficient and brings high transaction costs because the portfolio has to be reviewed relatively often. Therefore, in this article, a modification of delta-hedging as well as using the value of parameter gamma is suggested. Error of the delta modification is analyzed and compared with the error of widely used parameter delta. Typical patterns for the modified hedging parameter variation with various time to choose time for chooser options are also presented in this article. -

The Swaption Cube

The Swaption Cube Abstract We use a comprehensive database of inter-dealer quotes to conduct the first empirical analysis of the swaption cube. Using a model independent approach, we establish a set of stylized facts regarding the cross-sectional and time-series variation in conditional volatility and skewness of the swap rate distributions implied by the swaption cube. We then develop and estimate a dynamic term structure model that is consistent with these stylized facts and use it to infer volatility and skewness of the risk-neutral and physical swap rate distributions. Finally, we investigate the fundamental drivers of these distributions. In particular, we find that volatility, volatility risk premia, skewness, and skewness risk premia are significantly related to the characteristics of agents’ belief distributions for the macro-economy, with GDP beliefs being the most important factor in the USD market and inflation beliefs being the most important factor in the EUR market. This is consistent with differences in monetary policy objectives in the two markets. 1 Introduction In this paper, we conduct an extensive empirical analysis of the market for interest rate swaptions – options to enter into interest rate swaps – using a novel data set. Understanding the pricing of swaptions is important for several reasons. By some measures (such as the notional amount of outstanding contracts) the swaption market is the world’s largest options market. Furthermore, many standard fixed income securities, such as fixed rate mortgage- backed securities and callable agency securities, imbed swaption-like options, and swaptions are used to hedge and risk-manage these securities in addition to many exotic interest rate derivatives and structured products.