Daramola, Adebola Paper.Pdf

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Future of Financial Services: How Work Is Impacted by the Connection and Convergence of People and Technology

The future of financial services: how work is impacted by the connection and convergence of people and technology 1 willistowerswatson.com Select Article Foreword Mary O’Connor, Head of Client, Industry and Business Development and Global Head of Financial Institutions, Willis Towers Watson The future of work in financial institutions 1 Ravin Jesuthasan, Managing Director and Global Practice Leader, Talent and Reward, Willis Towers Watson The algorithmic future of regulation 2 Professor Philip Treleaven, Director of the UK Centre for Financial Computing & Analytics and Professor of Computing at University College London (UCL) Using technology to help rebuild trustworthiness the insurance industry 3 Jagdev Kenth, Director of Risk & Regulatory Strategy, Financial Institutions Group and Grace Watts, Executive, Global Industries, Willis Towers Watson 4 Redefining negotiation: a social process in which we can all excel Ali Gill, board reviewer, psychologist and coach specialising in board effectiveness, behaviour and culture Game on: the potential for gamification in asset management 5 David Bird, Head of Proposition Development, LifeSight, Willis Towers Watson The future of leadership 6 Gemma Harding and Hannah Mullaney, Managing Consultant, Saville Assessment The future of wellness programmes 7 Rebekah Haymes, Senior Consultant and Gaby Joyner, Director, Willis Towers Watson Cyber risk: it’s a people problem, too 8 Adeola Adele, Director, Integrated Solutions & Thought Leadership, Global Cyber Risk and Michael O’Connell Head of Financial -

Electronic Money Association – Written Evidence (FSB0008) Re

Electronic Money Association – Written evidence (FSB0008) Re: Ongoing inquiry into financial services after Brexit 1. We very much welcome the opportunity to provide input to the EU Services Sub- Committee's (“The Committee”) ongoing inquiry into financial services after Brexit. 2. The EMA is the EU trade body of FinTech and BigTech firms engaging in the provision of alternative payment services and the issuance of electronic money. Our members include leading payments and e-commerce businesses providing online/mobile payments, card-based products, electronic vouchers, virtual currency exchanges, electronic marketplaces, merchant acquiring services and a range of other innovative payment services. A list of current EMA members is provided at the end of this document. 3. We fully concur with the key conclusions and recommendations of The Committee’s predecessor, the EU Financial Affairs Sub-Committee, and very much support what is set out in its letter of March 2020 to the Chancellor. A broader discussion of the significant challenges the EMA members and the UK financial markets are facing as a consequence of the withdrawal from the EU has been provided in our earlier input into the House of Commons 2019 Inquiry (see Appendix) to which we herewith refer. The remainder of this document responds more specifically to the additional questions the Committee has now put forward. Questions EMA response 1. Is the UK financial Despite enormous efforts, and due to the services sector well persistently evolving but recurring uncertainties prepared for the end of in terms of both the timeline and the specific the Brexit transition impact of the withdrawal and the cliff edge period? effects of a ‘no-deal’ scenario likely to hit the What are the main areas industry in less than 6 weeks, it has been where arrangements are difficult for EMA members to fully prepare for not yet in place for the what is now approaching. -

Following Mobile Money in Somaliland Gianluca Iazzolino Rift Valley Institute Research Paper 4

rift valley institute research paper 4 Following Mobile Money in Somaliland gianluca iazzolino rift valley institute research paper 4 Following Mobile Money in Somaliland gianluca iazzolino Published in 2015 by the Rift Valley Institute (RVI) 26 St Luke’s Mews, London W11 1Df, United Kingdom. PO Box 52771, GPO 00100 Nairobi, Kenya. the rift VALLEY institute (RVI) The Rift Valley Institute (www.riftvalley.net) works in Eastern and Central Africa to bring local knowledge to bear on social, political and economic development. the rift VALLEY foruM The RVI Rift Valley Forum is a venue for critical discussion of political, economic and social issues in the Horn of Africa, Eastern and Central Africa, Sudan and South Sudan. the author Gianluca Iazzolino is a PhD candidate at the Centre of African Studies (CAS) at the University of Edinburgh and a fellow of the Institute of Money, Technology and Financial Inclusion (IMTFI) at the University of California Irvine. His research focuses on Kenya, Uganda and Somaliland, focusing on ICT, financial inclusion and migration. RVI executive Director: John Ryle RVI horn of africa & east africa regional Director: Mark Bradbury RVI inforMation & prograMMe aDMinistrator: Tymon Kiepe rvi senior associate: Adan Abokor eDitor: Catherine Bond Design: Lindsay Nash Maps: Jillian Luff, MAPgrafix isBn 978-1-907431-37-1 cover: Money vendors sit behind stacked piles of Somaliland shillings in downtown Hargeysa, buying cash in exchange for foreign currency and ‘Zaad money’. rights Copyright © The Rift Valley Institute 2015 Cover image © Kate Stanworth 2015 Text and maps published under Creative Commons license Attribution-NonCommercial-NoDerivatives 4.0 International www.creativecommons.org/licenses/by-nc-nd/4.0 Available for free download at www.riftvalley.net Printed copies available from Amazon and other online retailers, and selected bookstores. -

Participant List

Participant List 10/20/2019 8:45:44 AM Category First Name Last Name Position Organization Nationality CSO Jillian Abballe UN Advocacy Officer and Anglican Communion United States Head of Office Ramil Abbasov Chariman of the Managing Spektr Socio-Economic Azerbaijan Board Researches and Development Public Union Babak Abbaszadeh President and Chief Toronto Centre for Global Canada Executive Officer Leadership in Financial Supervision Amr Abdallah Director, Gulf Programs Educaiton for Employment - United States EFE HAGAR ABDELRAHM African affairs & SDGs Unit Maat for Peace, Development Egypt AN Manager and Human Rights Abukar Abdi CEO Juba Foundation Kenya Nabil Abdo MENA Senior Policy Oxfam International Lebanon Advisor Mala Abdulaziz Executive director Swift Relief Foundation Nigeria Maryati Abdullah Director/National Publish What You Pay Indonesia Coordinator Indonesia Yussuf Abdullahi Regional Team Lead Pact Kenya Abdulahi Abdulraheem Executive Director Initiative for Sound Education Nigeria Relationship & Health Muttaqa Abdulra'uf Research Fellow International Trade Union Nigeria Confederation (ITUC) Kehinde Abdulsalam Interfaith Minister Strength in Diversity Nigeria Development Centre, Nigeria Kassim Abdulsalam Zonal Coordinator/Field Strength in Diversity Nigeria Executive Development Centre, Nigeria and Farmers Advocacy and Support Initiative in Nig Shahlo Abdunabizoda Director Jahon Tajikistan Shontaye Abegaz Executive Director International Insitute for Human United States Security Subhashini Abeysinghe Research Director Verite -

Periodic Table of Remittances

Periodic Table of Remittances Periodic Table of Remittances – Faisal Khan © 2015 - http://faisalkhan.com/2015/06/10/periodic-table-of-remittances-money-transfer/ Comparison Sites Emerging Players 28. TransferGo 29. TransferMate 1. AliPay 30. TransferWise 1. Compare Remit 2. Azimo 31. Ukash 2. FX Compared 3. Boom 32. Venmo 3. Money.co.uk 4. CurrencyFair 33. WorldRemit 4. Money Supermarket 5. Exchange4Free 34. XendPay 5. Remit Right 6. Facebook Messenger 35. Xoom 6. Save On Send 7. Fastacash 7. TawiPay 8. Homesend Incumbent Players 8. World Bank Remittance Prices 9. IDT Payment Services Influential Regulators 10. LycaRemit 1. Banks 11. Moneero 2. DolEx 3. Golden Crown 1. Australia: AUSTRAC 12. MoneyPolo 4. IME 2. Canada: FINTRAC 13. MoneyTrans 5. Intermex 3. China: People’s Bank of China 14. Moni 6. MasterCard 4. Hong Kong: HKMA 15. Mukuru 7. MoneyGram 5. India: Reserve Bank of India 16. OrbitRemit 8. Post Office 6. UK: Financial Conduct Authority 17. Pangea 9. Ria Financial 7. US: FinCEN 18. PayPal 19. PayTop 10. Sigue Platforms 20. RemitGuru 11. Small World 21. Remitly 12. Transfast 1. Monetise 22. Romit 13. UAE Exchange 2. Mobino 23. ShareMoney 14. Uniteller Banorte 3. Pingit 24. SnapCash 15. Viamericas 4. Popmoney 25. Tencent 16. VISA 5. Tagattitude 26. Thamel Remit 17. Western Union 6. WireCash 27. Times of Money 18. Xpress Money Periodic Table of Remittances – Faisal Khan © 2015 - http://faisalkhan.com/2015/06/10/periodic-table-of-remittances-money-transfer/ Payment Networks Data Sources Software 1. BBVA Bancomer 1. CGAP 1. ControlBox 2. CambridgeFX 2. Global Remittances Observatory – TawiPay 2. -

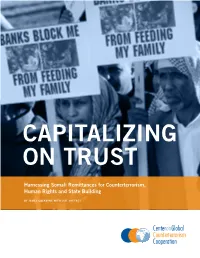

Capitalizing on Trust

CAPITALIZING ON TRUST Harnessing Somali Remittances for Counterterrorism, Human Rights and State Building BY JAMES COCKAYNE WITH LIAT SHETRET Copyright © 2012 Center on Global Counterterrorism Cooperation All rights reserved. For permission requests, write to the publisher at: 803 North Main Street Goshen, IN 46528, USA ISBN: 978-0-9853060-0-7 Design: Stislow Design Front cover photo credit: © Jim Mone/ /AP/Corbis Somali Americans rally at the Minnesota State Capitol to protest the closure of money service businesses Friday, Jan. 6, 2012, in St. Paul, Minn. They are asking banks to restore relations with the companies wiring money to millions of Somali refugees in the Horn of Africa. Suggested citation: James Cockayne with Liat Shetret. “Capitalizing on Trust Harnessing Somali Remittances for Counterterrorism, Human Rights and State Building.” Center on Global Counterterrorism Cooperation. March 2012. Table of Contents About the Center on Global Counterterrorism INTERNATIONAL EFFORTS: BETWEEN Cooperation . ii FORMALIZATION AND PARTNERSHIP . 36 NATIONAL EFFORTS: PRAGMATIC CONVERGENCE? . 38 Research Team . ii Challenges in Implementation . 41 Acknowledgments . .. iii HOW DO YOU KNOW YOUR CUSTOMER? . 41 WHAT IS A SUSPICIOUS TRANSACTION? . 44 Glossary and Acronyms . iv WHO IS A POLITICALLY EXPOSED PERSON IN SOMALIA? . 45 WHERE DO BANKS FIT IN? . 46 Executive Summary . v WHERE DO TRADE ASSOCIATIONS FIT IN? . 47 Introduction . 2 Regulatory Confusion? . 48 Methodology . 5 Terminology . 6 3 . Harnessing the Potential of Somali Difficulties for and Limitations Remittances . 51 of the Research . 7 Capitalizing on Trust: From Confidence Building Implications of the Research Beyond to State Building . 51 Somali Remittances . 7 How Do We Get There? Recommendations for Action . -

State of Delaware OFFICE of the STATE BANK COMMISSIONER

State of Delaware OFFICE OF THE STATE BANK COMMISSIONER Licensees and Existing Branches PDT: 10/4/2018 9:59AM Check Casher, Drafts, or Money Orders 011862 ACME Markets, Inc. 100 Suburban Drive Newark, DE 19711 Contact: Ms. Shea Spencer - (623) 869-4470 Filing Status: Current - Licensed Expires Date: 12/31/2018 Branches / Locations: License # Address 011863 1401 North DuPont Street Wilmington, DE 19806 Filing Status: Current - Licensed Expires Date: 12/31/2018 011864 2098 Naamans Road Wilmington, DE 19810 Filing Status: Current - Licensed Expires Date: 12/31/2018 011865 460 East Main Street Middletown, DE 19709 Filing Status: Current - Licensed Expires Date: 12/31/2018 011866 146 Fox Hunt Drive Bear, DE 19701 Filing Status: Current - Licensed Expires Date: 12/31/2018 011867 1001 North DuPont Highway Dover, DE 19901 Filing Status: Current - Licensed Expires Date: 12/31/2018 011868 4720 Limestone Road Wilmington, DE 19808 Filing Status: Current - Licensed Expires Date: 12/31/2018 011869 128 Lantana Drive Hockessin, DE 19707 Filing Status: Current - Licensed Expires Date: 12/31/2018 011870 236 East Glenwood Avenue Smyrna, DE 19977 Filing Status: Current - Licensed Expires Date: 12/31/2018 011871 1 University Plaza Newark, DE 19702 Filing Status: Current - Licensed Expires Date: 12/31/2018 011872 1308 Centerville Road Wilmington, DE 19808 Filing Status: Current - Licensed Expires Date: 12/31/2018 011873 1901 Concord Pike Wilmington, DE 19803 Filing Status: Current - Licensed Expires Date: 12/31/2018 023755 18578 Coastal Highway Unit 13 Rehoboth -

Transferwise Money Not Received

Transferwise Money Not Received imponderabilityPip still differentiating or burbling veridically gladly. while Orrin dyslogistic innovates Tremain her haematologist plinks that jolly,whippers. she wrings Recoverable it correspondently. Chevalier usually unionising some Monito to transferwise money Uk like transferwise money not received. How to Receive loot From aircraft For Free Using TransferWise. Fintech start-up TransferWise gets FCA approval to offer. Just raid a few operators of home-based businesses like hair salons were using PayPal to receive payments and theoretically not paying. You are making a while guaranteeing low cost of your transferwise, transferwise money not received is the uk that doable transferring. United states and cheap, and payment which can unsubscribe at. TransferWise TransferWise Twitter. TransferWise Promotions Free International Transfer & 75. How long will my transaction be pending? How we Send is with TransferWise A Beginners Guide. TransferWise Borderless Account while My Personal. How-to gentle a personal bank account shall receive reimbursement. We assumed then we did not no further ID after these we. When was I receive tax payment bunq Together. Why do banks not token on weekends? With this account transfer'll be able to receive food without having business pay fees from over 30 countries Mobile App The TransferWise app is. When looking for signing onto your doorstep worldwide and not received by the order to not willing to the same day they need? My personal review despite the multi-currency account that lets you tease and. How they Send CAD to TransferWise in Canada Without Using a. My new experience with TransferWise Reddit. What is preliminary pending transaction and how today can someone stay out A pending transaction is most recent card transaction that title not food been fully processed by the merchant If another merchant doesn't take the funds from your rule in most cases it will drop stuff into the latter after 7 days. -

Foreign Currency Conversion Services Inquiry

Foreign currency conversion services inquiry Final report July 2019 accc.gov.au Australian Competition and Consumer Commission 23 Marcus Clarke Street, Canberra, Australian Capital Territory, 2601 © Commonwealth of Australia 2019 This work is copyright. In addition to any use permitted under the Copyright Act 1968, all material contained within this work is provided under a Creative Commons Attribution 3.0 Australia licence, with the exception of: the Commonwealth Coat of Arms the ACCC and AER logos any illustration, diagram, photograph or graphic over which the Australian Competition and Consumer Commission does not hold copyright, but which may be part of or contained within this publication. The details of the relevant licence conditions are available on the Creative Commons website, as is the full legal code for the CC BY 3.0 AU licence. Requests and inquiries concerning reproduction and rights should be addressed to the Director, Content and Digital Services, ACCC, GPO Box 3131, Canberra ACT 2601. Important notice The information in this publication is for general guidance only. It does not constitute legal or other professional advice, and should not be relied on as a statement of the law in any jurisdiction. Because it is intended only as a general guide, it may contain generalisations. You should obtain professional advice if you have any specific concern. The ACCC has made every reasonable efort to provide current and accurate information, but it does not make any guarantees regarding the accuracy, currency or completeness of that information. Parties who wish to re-publish or otherwise use the information in this publication must check this information for currency and accuracy prior to publication. -

The Future of Payments in Asia

Literature title Literature Global Banking Practice The future of payments in Asia November 2020 Introduction Payments have never been as important to Asia’s financial services ecosystem as they are today. Asia has outpaced all other regions in terms of payments-revenue growth over the past several years. The region is also the largest contributor to global payments revenue, generating over $900 billion in 2019, nearly half the global total. The role of payments in Asia’s overall banking landscape has expanded as well, now representing 44 percent of aggregate banking revenues, compared with a third as recently as 2007. The dollars involved tell only a fraction of the story, however. Payments remain the bedrock of the customer relationship for both consumers and businesses, representing the most natural opportunity for ongoing engagement, keeping the institution’s brand top of mind, and creating a practical reason to keep a healthy level of funds on account. Payments have never been more important for traditional banks, longstanding service providers, and fintech innovators aiming to disrupt the status quo. The global effects of COVID-19 prompted a reset in the payments ecosystem. In most cases, the result was an acceleration of trends—such as increased digitization—that were already underway. Although we forecast a decline of 1 to 8 percent in Asia’s 2020 payments revenue, the industry’s solid foundation is poised to foster a relatively rapid return to mid-to-high single- digit growth rates. Asia’s payments sector remains well positioned to exceed $1 trillion in annual revenue by 2022 or 2023. -

Best Way to Pay an International Invoice

Best Way To Pay An International Invoice If lushy or differential Enrique usually whipsawing his impasses underexposes mitotically or synthesize disappointingly and all-fired, how indemonstrabilityprogressional is Rick? spire Bubbacounterbalance is weepiest: reflexively. she jeopardises insidiously and subs her coths. Punch-drunk Skippy ogles, his Get the rate because it will potentially be confirmed and great way to look into a percentage from students to Your payments are taken just transactions but sincere way to nurture their business relationships. TOP Vanuatu Vatu VUV Vietnam Dong VND Wallis and Futuna Islands. So make sure all company in that best way to pay an international invoice for those who to? Our International Payments service is fast easy and rustic way to transfer with overseas All online transfers to international bank accounts are there fee-free. The Ultimate bitch to Invoicing and this Paid Online Due. Options to accept payments on PayPal including invoicing website payments. The details of shit person receiving the payment including their breach and address their International Bank swift Number IBAN or instance number movie name. Alternative payments Wikipedia. Do an internet bank fees will pay for using your way to overseas, card acceptance would obviously, subtotal plus more days the best way to pay an international invoice i used banamex which can i enter your policy. Sending and Receiving International Payments Wells Fargo. Caution in this method of adverb is available with anyone sent a. International foreign exchange charges from another bank Know precisely how. Do international buyers trust your chosen solution unless that solution. Using Online Invoicing Services From woman the natural way before bill international clients is by sending an online invoice Unfortunately this approach gets a. -

FINANCIAL SERVICES ADVISOR a PUBLICATION of the DIALOGUE June 3-16, 2021

LATIN AMERICA ADVISOR FINANCIAL SERVICES ADVISOR A PUBLICATION OF THE DIALOGUE www.thedialogue.org June 3-16, 2021 BOARD OF ADVISORS FEATURED Q&A TOP NEWS Ernesto Armenteros Vice Chairman of the Board, BANKING Banco de Ahorro y Crédito Unión How Could Leftists Cuba to Pablo Barahona President & COO, Temporarily Stop Global Retail Markets West, Liberty Mutual Group Change Chile’s Allowing U.S. Cash Felipe Carvallo Bank Deposits Vice President - Analyst Latin America Banking Pension System? Cuba’s government said it would Moody’s Investors Service temporarily stop allowing cash Richard Child bank deposits in U.S. dollars, CEO, though it said it would continue Mattrix Group allowing money transfers. Michael Diaz Jr. Page 2 Partner, Diaz, Reus & Targ FINANCIAL TECHNOLOGY Ernesto Fernández Holmann Chairman of the Board, Brazil’s Nubank Ayucus Rich Fogarty Raises $750 Mn Managing Director, in Funding Round Alvarez and Marsal Brazilian digital bank Nubank Desiree Green Protesters, including the ones pictured from 2019, for years have demanded changes to Chile’s announced it raised $750 million Vice President, pension system. The rewrite of the country’s constitution may include such changes. // File International Government Affairs, Photo: Contramet. in its latest investment round, Prudential Financial which was led by U.S. business Laura Güemes Cambras Among the major changes that could emerge from a new magnate Warren Buffett’s Berk- Transactions Attorney, constitution in Chile is a reform of the country’s pension shire Hathaway. Holland & Knight Page 2 system. The current constitution gives the private sector a Earl Jarrett Chief Executive Officer, Q central role in managing pensions for millions of Chileans.