Pricing Interest Rate Derivatives: an Application to the Uruguayan Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

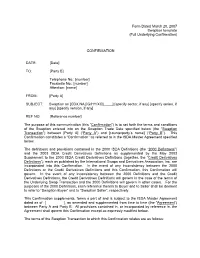

Form Dated March 20, 2007 Swaption Template (Full Underlying Confirmation)

Form Dated March 20, 2007 Swaption template (Full Underlying Confirmation) CONFIRMATION DATE: [Date] TO: [Party B] Telephone No.: [number] Facsimile No.: [number] Attention: [name] FROM: [Party A] SUBJECT: Swaption on [CDX.NA.[IG/HY/XO].____] [specify sector, if any] [specify series, if any] [specify version, if any] REF NO: [Reference number] The purpose of this communication (this “Confirmation”) is to set forth the terms and conditions of the Swaption entered into on the Swaption Trade Date specified below (the “Swaption Transaction”) between [Party A] (“Party A”) and [counterparty’s name] (“Party B”). This Confirmation constitutes a “Confirmation” as referred to in the ISDA Master Agreement specified below. The definitions and provisions contained in the 2000 ISDA Definitions (the “2000 Definitions”) and the 2003 ISDA Credit Derivatives Definitions as supplemented by the May 2003 Supplement to the 2003 ISDA Credit Derivatives Definitions (together, the “Credit Derivatives Definitions”), each as published by the International Swaps and Derivatives Association, Inc. are incorporated into this Confirmation. In the event of any inconsistency between the 2000 Definitions or the Credit Derivatives Definitions and this Confirmation, this Confirmation will govern. In the event of any inconsistency between the 2000 Definitions and the Credit Derivatives Definitions, the Credit Derivatives Definitions will govern in the case of the terms of the Underlying Swap Transaction and the 2000 Definitions will govern in other cases. For the purposes of the 2000 Definitions, each reference therein to Buyer and to Seller shall be deemed to refer to “Swaption Buyer” and to “Swaption Seller”, respectively. This Confirmation supplements, forms a part of and is subject to the ISDA Master Agreement dated as of [ ], as amended and supplemented from time to time (the “Agreement”) between Party A and Party B. -

Interest Rate Options

Interest Rate Options Saurav Sen April 2001 Contents 1. Caps and Floors 2 1.1. Defintions . 2 1.2. Plain Vanilla Caps . 2 1.2.1. Caplets . 3 1.2.2. Caps . 4 1.2.3. Bootstrapping the Forward Volatility Curve . 4 1.2.4. Caplet as a Put Option on a Zero-Coupon Bond . 5 1.2.5. Hedging Caps . 6 1.3. Floors . 7 1.3.1. Pricing and Hedging . 7 1.3.2. Put-Call Parity . 7 1.3.3. At-the-money (ATM) Caps and Floors . 7 1.4. Digital Caps . 8 1.4.1. Pricing . 8 1.4.2. Hedging . 8 1.5. Other Exotic Caps and Floors . 9 1.5.1. Knock-In Caps . 9 1.5.2. LIBOR Reset Caps . 9 1.5.3. Auto Caps . 9 1.5.4. Chooser Caps . 9 1.5.5. CMS Caps and Floors . 9 2. Swap Options 10 2.1. Swaps: A Brief Review of Essentials . 10 2.2. Swaptions . 11 2.2.1. Definitions . 11 2.2.2. Payoff Structure . 11 2.2.3. Pricing . 12 2.2.4. Put-Call Parity and Moneyness for Swaptions . 13 2.2.5. Hedging . 13 2.3. Constant Maturity Swaps . 13 2.3.1. Definition . 13 2.3.2. Pricing . 14 1 2.3.3. Approximate CMS Convexity Correction . 14 2.3.4. Pricing (continued) . 15 2.3.5. CMS Summary . 15 2.4. Other Swap Options . 16 2.4.1. LIBOR in Arrears Swaps . 16 2.4.2. Bermudan Swaptions . 16 2.4.3. Hybrid Structures . 17 Appendix: The Black Model 17 A.1. -

Master Thesis the Use of Interest Rate Derivatives and Firm Market Value an Empirical Study on European and Russian Non-Financial Firms

Master Thesis The use of Interest Rate Derivatives and Firm Market Value An empirical study on European and Russian non-financial firms Tilburg, October 5, 2014 Mark van Dijck, 937367 Tilburg University, Finance department Supervisor: Drs. J.H. Gieskens AC CCM QT Master Thesis The use of Interest Rate Derivatives and Firm Market Value An empirical study on European and Russian non-financial firms Tilburg, October 5, 2014 Mark van Dijck, 937367 Supervisor: Drs. J.H. Gieskens AC CCM QT 2 Preface In the winter of 2010 I found myself in the heart of a company where the credit crisis took place at that moment. During a treasury internship for Heijmans NV in Rosmalen, I experienced why it is sometimes unescapable to use interest rate derivatives. Due to difficult financial times, banks strengthen their requirements and the treasury department had to use different mechanism including derivatives to restructure their loans to the appropriate level. It was a fascinating time. One year later I wrote a bachelor thesis about risk management within energy trading for consultancy firm Tensor. Interested in treasury and risk management I have always wanted to finish my finance study period in this field. During the master thesis period I started to work as junior commodity trader at Kühne & Heitz. I want to thank Kühne & Heitz for the opportunity to work in the trading environment and to learn what the use of derivatives is all about. A word of gratitude to my supervisor Drs. J.H. Gieskens for his quick reply, well experienced feedback that kept me sharp to different levels of the subject, and his availability even in the late hours after I finished work. -

5. Caps, Floors, and Swaptions

Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Interest Rate and Credit Models 5. Caps, Floors, and Swaptions Andrew Lesniewski Baruch College New York Spring 2019 A. Lesniewski Interest Rate and Credit Models Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Outline 1 Options on LIBOR based instruments 2 Valuation of LIBOR options 3 Local volatility models 4 The SABR model 5 Volatility cube A. Lesniewski Interest Rate and Credit Models Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Options on LIBOR based instruments Interest rates fluctuate as a consequence of macroeconomic conditions, central bank actions, and supply and demand. The existence of the term structure of rates, i.e. the fact that the level of a rate depends on the maturity of the underlying loan, makes the dynamics of rates is highly complex. While a good analogy to the price dynamics of an equity is a particle moving in a medium exerting random shocks to it, a natural way of thinking about the evolution of rates is that of a string moving in a random environment where the shocks can hit any location along its length. A. Lesniewski Interest Rate and Credit Models Options on LIBOR based instruments Valuation of LIBOR options Local volatility models The SABR model Volatility cube Options on LIBOR based instruments Additional complications arise from the presence of various spreads between rates, as discussed in Lecture Notes #1, which reflect credit quality of the borrowing entity, liquidity of the instrument, or other market conditions. -

Interest Rate Modelling and Derivative Pricing

Interest Rate Modelling and Derivative Pricing Sebastian Schlenkrich HU Berlin, Department of Mathematics WS, 2019/20 Part III Vanilla Option Models p. 140 Outline Vanilla Interest Rate Options SABR Model for Vanilla Options Summary Swaption Pricing p. 141 Outline Vanilla Interest Rate Options SABR Model for Vanilla Options Summary Swaption Pricing p. 142 Outline Vanilla Interest Rate Options Call Rights, Options and Forward Starting Swaps European Swaptions Basic Swaption Pricing Models Implied Volatilities and Market Quotations p. 143 Now we have a first look at the cancellation option Interbank swap deal example Bank A may decide to early terminate deal in 10, 11, 12,.. years. p. 144 We represent cancellation as entering an opposite deal L1 Lm ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ ✻ T˜0 T˜k 1 T˜m − ✲ T0 TE Tl 1 Tn − ❄ ❄ ❄ ❄ ❄ ❄ K K [cancelled swap] = [full swap] + [opposite forward starting swap] K ✻ ✻ Tl 1 Tn − ✲ TE T˜k 1 T˜m − ❄ ❄ ❄ ❄ Lm p. 145 Option to cancel is equivalent to option to enter opposite forward starting swap K ✻ ✻ Tl 1 Tn − ✲ TE T˜k 1 T˜m − ❄ ❄ ❄ ❄ Lm ◮ At option exercise time TE present value of remaining (opposite) swap is n m Swap δ V (TE ) = K · τi · P(TE , Ti ) − L (TE , T˜j 1, T˜j 1 + δ) · τ˜j · P(TE , T˜j ) . − − i=l j=k X X future fixed leg future float leg | {z } | {z } ◮ Option to enter represents the right but not the obligation to enter swap. ◮ Rational market participant will exercise if swap present value is positive, i.e. Option Swap V (TE ) = max V (TE ), 0 . -

Introduction to Black's Model for Interest Rate

INTRODUCTION TO BLACK'S MODEL FOR INTEREST RATE DERIVATIVES GRAEME WEST AND LYDIA WEST, FINANCIAL MODELLING AGENCY© Contents 1. Introduction 2 2. European Bond Options2 2.1. Different volatility measures3 3. Caplets and Floorlets3 4. Caps and Floors4 4.1. A call/put on rates is a put/call on a bond4 4.2. Greeks 5 5. Stripping Black caps into caplets7 6. Swaptions 10 6.1. Valuation 11 6.2. Greeks 12 7. Why Black is useless for exotics 13 8. Exercises 13 Date: July 11, 2011. 1 2 GRAEME WEST AND LYDIA WEST, FINANCIAL MODELLING AGENCY© Bibliography 15 1. Introduction We consider the Black Model for futures/forwards which is the market standard for quoting prices (via implied volatilities). Black[1976] considered the problem of writing options on commodity futures and this was the first \natural" extension of the Black-Scholes model. This model also is used to price options on interest rates and interest rate sensitive instruments such as bonds. Since the Black-Scholes analysis assumes constant (or deterministic) interest rates, and so forward interest rates are realised, it is difficult initially to see how this model applies to interest rate dependent derivatives. However, if f is a forward interest rate, it can be shown that it is consistent to assume that • The discounting process can be taken to be the existing yield curve. • The forward rates are stochastic and log-normally distributed. The forward rates will be log-normally distributed in what is called the T -forward measure, where T is the pay date of the option. -

Tax Treatment of Derivatives

United States Viva Hammer* Tax Treatment of Derivatives 1. Introduction instruments, as well as principles of general applicability. Often, the nature of the derivative instrument will dictate The US federal income taxation of derivative instruments whether it is taxed as a capital asset or an ordinary asset is determined under numerous tax rules set forth in the US (see discussion of section 1256 contracts, below). In other tax code, the regulations thereunder (and supplemented instances, the nature of the taxpayer will dictate whether it by various forms of published and unpublished guidance is taxed as a capital asset or an ordinary asset (see discus- from the US tax authorities and by the case law).1 These tax sion of dealers versus traders, below). rules dictate the US federal income taxation of derivative instruments without regard to applicable accounting rules. Generally, the starting point will be to determine whether the instrument is a “capital asset” or an “ordinary asset” The tax rules applicable to derivative instruments have in the hands of the taxpayer. Section 1221 defines “capital developed over time in piecemeal fashion. There are no assets” by exclusion – unless an asset falls within one of general principles governing the taxation of derivatives eight enumerated exceptions, it is viewed as a capital asset. in the United States. Every transaction must be examined Exceptions to capital asset treatment relevant to taxpayers in light of these piecemeal rules. Key considerations for transacting in derivative instruments include the excep- issuers and holders of derivative instruments under US tions for (1) hedging transactions3 and (2) “commodities tax principles will include the character of income, gain, derivative financial instruments” held by a “commodities loss and deduction related to the instrument (ordinary derivatives dealer”.4 vs. -

Forward Contracts and Futures a Forward Is an Agreement Between Two Parties to Buy Or Sell an Asset at a Pre-Determined Future Time for a Certain Price

Forward contracts and futures A forward is an agreement between two parties to buy or sell an asset at a pre-determined future time for a certain price. Goal To hedge against the price fluctuation of commodity. • Intension of purchase decided earlier, actual transaction done later. • The forward contract needs to specify the delivery price, amount, quality, delivery date, means of delivery, etc. Potential default of either party: writer or holder. Terminal payoff from forward contract payoff payoff K − ST ST − K K ST ST K long position short position K = delivery price, ST = asset price at maturity Zero-sum game between the writer (short position) and owner (long position). Since it costs nothing to enter into a forward contract, the terminal payoff is the investor’s total gain or loss from the contract. Forward price for a forward contract is defined as the delivery price which make the value of the contract at initiation be zero. Question Does it relate to the expected value of the commodity on the delivery date? Forward price = spot price + cost of fund + storage cost cost of carry Example • Spot price of one ton of wood is $10,000 • 6-month interest income from $10,000 is $400 • storage cost of one ton of wood is $300 6-month forward price of one ton of wood = $10,000 + 400 + $300 = $10,700. Explanation Suppose the forward price deviates too much from $10,700, the construction firm would prefer to buy the wood now and store that for 6 months (though the cost of storage may be higher). -

An Analysis of OTC Interest Rate Derivatives Transactions: Implications for Public Reporting

Federal Reserve Bank of New York Staff Reports An Analysis of OTC Interest Rate Derivatives Transactions: Implications for Public Reporting Michael Fleming John Jackson Ada Li Asani Sarkar Patricia Zobel Staff Report No. 557 March 2012 Revised October 2012 FRBNY Staff REPORTS This paper presents preliminary fi ndings and is being distributed to economists and other interested readers solely to stimulate discussion and elicit comments. The views expressed in this paper are those of the authors and are not necessarily refl ective of views at the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the authors. An Analysis of OTC Interest Rate Derivatives Transactions: Implications for Public Reporting Michael Fleming, John Jackson, Ada Li, Asani Sarkar, and Patricia Zobel Federal Reserve Bank of New York Staff Reports, no. 557 March 2012; revised October 2012 JEL classifi cation: G12, G13, G18 Abstract This paper examines the over-the-counter (OTC) interest rate derivatives (IRD) market in order to inform the design of post-trade price reporting. Our analysis uses a novel transaction-level data set to examine trading activity, the composition of market participants, levels of product standardization, and market-making behavior. We fi nd that trading activity in the IRD market is dispersed across a broad array of product types, currency denominations, and maturities, leading to more than 10,500 observed unique product combinations. While a select group of standard instruments trade with relative frequency and may provide timely and pertinent price information for market partici- pants, many other IRD instruments trade infrequently and with diverse contract terms, limiting the impact on price formation from the reporting of those transactions. -

Pricing of Index Options Using Black's Model

Global Journal of Management and Business Research Volume 12 Issue 3 Version 1.0 March 2012 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA) Online ISSN: 2249-4588 & Print ISSN: 0975-5853 Pricing of Index Options Using Black’s Model By Dr. S. K. Mitra Institute of Management Technology Nagpur Abstract - Stock index futures sometimes suffer from ‘a negative cost-of-carry’ bias, as future prices of stock index frequently trade less than their theoretical value that include carrying costs. Since commencement of Nifty future trading in India, Nifty future always traded below the theoretical prices. This distortion of future prices also spills over to option pricing and increase difference between actual price of Nifty options and the prices calculated using the famous Black-Scholes formula. Fisher Black tried to address the negative cost of carry effect by using forward prices in the option pricing model instead of spot prices. Black’s model is found useful for valuing options on physical commodities where discounted value of future price was found to be a better substitute of spot prices as an input to value options. In this study the theoretical prices of Nifty options using both Black Formula and Black-Scholes Formula were compared with actual prices in the market. It was observed that for valuing Nifty Options, Black Formula had given better result compared to Black-Scholes. Keywords : Options Pricing, Cost of carry, Black-Scholes model, Black’s model. GJMBR - B Classification : FOR Code:150507, 150504, JEL Code: G12 , G13, M31 PricingofIndexOptionsUsingBlacksModel Strictly as per the compliance and regulations of: © 2012. -

Modeling VXX

Modeling VXX Sebastian A. Gehricke Department of Accountancy and Finance Otago Business School, University of Otago Dunedin 9054, New Zealand Email: [email protected] Jin E. Zhang Department of Accountancy and Finance Otago Business School, University of Otago Dunedin 9054, New Zealand Email: [email protected] First Version: June 2014 This Version: 13 September 2014 Keywords: VXX; VIX Futures; Roll Yield; Market Price of Variance Risk; Variance Risk Premium JEL Classification Code: G13 Modeling VXX Abstract We study the VXX Exchange Traded Note (ETN), that has been actively traded in the New York Stock Exchange in recent years. We propose a simple model for the VXX and derive an analytical expression for the VXX roll yield. The roll yield of any futures position is the return not due to movements of the underlying, in commodity futures it is often called the cost of carry. Using our model we confirm that the phenomena of the large negative returns of the VXX, as first documented by Whaley (2013), which we call the VXX return puzzle, is due to the predominantly negative roll yield as proposed but never quantified in the literature. We provide a simple and robust estimation of the market price of variance risk which uses historical VXX returns. Our VXX price model can be used to study the price of options written on the VXX. Modeling VXX 1 1 Introduction There are three major risk factors which are traded in financial markets: market risk which is traded in the stock market, interest rate risk which is traded in the bond markets and interest rate derivative markets, and volatility risk which up until recently was only traded indirectly in the options market. -

Panagora Global Diversified Risk Portfolio General Information Portfolio Allocation

March 31, 2021 PanAgora Global Diversified Risk Portfolio General Information Portfolio Allocation Inception Date April 15, 2014 Total Assets $254 Million (as of 3/31/2021) Adviser Brighthouse Investment Advisers, LLC SubAdviser PanAgora Asset Management, Inc. Portfolio Managers Bryan Belton, CFA, Director, Multi Asset Edward Qian, Ph.D., CFA, Chief Investment Officer and Head of Multi Asset Research Jonathon Beaulieu, CFA Investment Strategy The PanAgora Global Diversified Risk Portfolio investment philosophy is centered on the belief that risk diversification is the key to generating better risk-adjusted returns and avoiding risk concentration within a portfolio is the best way to achieve true diversification. They look to accomplish this by evaluating risk across and within asset classes using proprietary risk assessment and management techniques, including an approach to active risk management called Dynamic Risk Allocation. The portfolio targets a risk allocation of 40% equities, 40% fixed income and 20% inflation protection. Portfolio Statistics Portfolio Composition 1 Yr 3 Yr Inception 1.88 0.62 Sharpe Ratio 0.6 Positioning as of Positioning as of 0.83 0.75 Beta* 0.78 December 31, 2020 March 31, 2021 Correlation* 0.87 0.86 0.79 42.4% 10.04 10.6 Global Equity 43.4% Std. Deviation 9.15 24.9% U.S. Stocks 23.6% Weighted Portfolio Duration (Month End) 9.0% 8.03 Developed non-U.S. Stocks 9.8% 8.5% *Statistic is measured against the Dow Jones Moderate Index Emerging Markets Equity 10.0% 106.8% Portfolio Benchmark: Nominal Fixed Income 142.6% 42.0% The Dow Jones Moderate Index is a composite index with U.S.