Issues in Designing a Bitcoin-Like Community Currency

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Advantages and Disadvantages of Bitcoin Payments in the New Economy Carina-Elena Stegăroiu, Lecturer Phd, „Constantin Br

Annals of the „Constantin Brâncuşi” University of Târgu Jiu, Economy Series, Issue 1/2018 THE ADVANTAGES AND DISADVANTAGES OF BITCOIN PAYMENTS IN THE NEW ECONOMY CARINA-ELENA STEGĂROIU, LECTURER PHD, „CONSTANTIN BRÂNCUŞI” UNIVERSITY, TÂRGU JIU, ROMANIA [email protected] Abstract In the Internet economy, with the help of cryptography, a branch of mathematics dealing with the security of information, as well as authentication and restriction of access to a computer system, a new digital coin as an alternative to national currencies appeared. In accomplishing this, using both mathematical methods (taking advantage of, for example, the difficulty of factorizing very large numbers), and quantum encryption methods. Throughout the world, information technology companies are focusing on information protection, inventing day-to-day methods with greater durability. In the horizon of Information Security, Quantum Cryptography has emerged, generating new possibilities in that field, hoping that data will be better protected and that the digital currency will resist over time and eventually evolve in the future, although Kurzweil, Bitcoin's pioneering technology is unlikely to be used in this respect. The idea of virtual alternatives to national currencies is not new, with advantages and disadvantages. The advantages of this coin are high payment freedom, transparency of information, high security, reduced risks for traders. Among the disadvantages we highlight the risk and volatility, the lack of notification and understanding, with incomplete functions, but which are developing, so Bitcoin is not perfect. Keywords: bitcoin, criptografie, methodology, economic growth, economic agent, branch production, virtual economy, monedă digitală Classification JEL: F60, F61. F62, F63 1. Introduction The idea of virtual alternatives to national currencies is not a new one, Iceland being a country that in April issued its own virtual modular Auroracoin, distributing it to the population. -

Complementary Currencies: Mutual Credit Currency Systems and the Challenge of Globalization

Complementary Currencies: Mutual Credit Currency Systems and the Challenge of Globalization Clare Lascelles1 Abstract Complementary currencies—currencies operating alongside the official currency—have taken many forms throughout the last century or so. While their existence has a rich history, complementary currencies are increasingly viewed as anachronistic in a world where the forces of globalization promote further integration between economies and societies. Even so, towns across the globe have recently witnessed the introduction of complementary currencies in their region, which connotes a renewed emphasis on local identity. This paper explores the rationale behind the modern-day adoption of complementary currencies in a globalized system. I. Introduction Coined money has two sides: heads and tails. ‘Heads’ represents the state authority that issued the coin, while ‘tails’ displays the value of the coin as a medium of exchange. This duality—the “product of social organization both from the top down (‘states’) and from the bottom up (‘markets’)”—reveals the coin as “both a token of authority and a commodity with a price” (Hart, 1986). Yet, even as side ‘heads’ reminds us of the central authority that underwrote the coin, currency can exist outside state control. Indeed, as globalization exerts pressure toward financial integration, complementary currencies—currencies existing alongside the official currency—have become common in small towns and regions. This paper examines the rationale behind complementary currencies, with a focus on mutual credit currency, and concludes that the modern-day adoption of complementary currencies can be attributed to the depersonalizing force of globalization. II. Literature Review Money is certainly not a topic unstudied. -

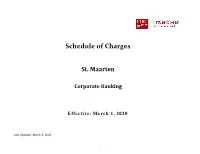

St. Maarten Corporate

Schedule of Charges St. Maarten Corporate Banking Effective: March 1, 2020 Last Updated: March 1, 2020 1 Schedule of Charges CONTENTS 1 CORPORATE DEPOSIT AND TRANSACTION ACCOUNTS - LOCAL CURRENCY 2 CORPORATE DEPOSIT AND TRANSACTION ACCOUNTS - FOREIGN CURRENCY 3 SUNDRY SERVICES 4 LENDING AND CARD SERVICES 5 CORPORATE SERVICES 6 TRADE SERVICES 2 Schedule of Charges CORPORATE DEPOSIT AND TRANSACTION ACCOUNTS - LOCAL CURRENCY Business Current Accounts Call Accounts Minimum monthly service fee $12.50 Minimum monthly service fee $12.50 Withdrawals / Cheques per entry $1.75 Withdrawals / Debits per entry 1 free, thereafter $1.00 Deposits / Credits per entry $1.25 Deposits / Credits per entry 1 free, thereafter $1.00 Business Premium Accounts Fixed Deposit Accounts Minimum monthly service fee $12.50 Transfer to another internal account on maturity No Charge Withdrawals / Cheques per entry 1 free, thereafter $2.00 Transfer to another institution on maturity Draft or Wire Fee Deposits / Credits per entry 1 free, thereafter $2.00 Notes: 1. * - Product/Service Not offered to new clients 2. All figures are quoted in Netherlands Antillean Guilder unless otherwise stated. 3 Schedule of Charges CORPORATE DEPOSIT AND TRANSACTION ACCOUNTS - FOREIGN CURRENCY UNITED STATES DOLLARS (USD) EURO DOLLARS (EUR$) USD Chequing Accounts EUR Business Current Accounts Minimum monthly service fee USD $10.00 Minimum monthly service fee € 10.00 Withdrawals / Cheques per entry 2 free, thereafter USD $0.75 Withdrawals / Cheques per entry 2 free, thereafter €1.00 Deposits / Credits per entry 2 free, thereafter USD $0.75 Deposits / Credits per entry 2 free, thereafter €1.00 USD Business Premium Accounts EUR Business Call Accounts Minimum monthly service fee USD $5.00 Minimum monthly service fee € 10.00 Withdrawals / Cheques per entry 2 free, thereafter USD $1.00 Withdrawals / Cheques per entry 4 free, thereafter €0.40 Deposits / Credits per entry 2 free, thereafter USD $1.00 Deposits / Credits per entry No Charge EUR deposit charge 0.7% p.a. -

Our Monthly View on Asset Allocation

ASSET ALLOCATION INSIGHTS April 2019 OUR MONTHLY VIEW ON ASSET ALLOCATION FINANCIAL REPRESSION, SEASON 2 Artificial business cycle Thanks to a new dose of monetary policy accommodation, central banks in developed markets should extension brings be able to extend the business cycle – although somewhat artificially, as they refuse to normalise rates goldilocks back in order to properly flush out the system. There is still too much debt, following a decade of financial repression, and not enough nominal growth, despite a decade of ultra-loose monetary policy. Economic growth in developed economies is now expected to bottom out around the end of the first quarter, before nearing potential economic growth further down the line. While this is not ideal, it will not be But it’s too late enough to trigger inflation concerns. So we are back in a kind of goldilocks scenario with no recession, to chase momentum low inflation and no interest rate hikes. The extra liquidity has annihilated volatility, reflated asset valuations and triggered a new run-to-carry. However, as the influence of monetary stimulus will soon fade, and valuations are not overly appealing, it is now too late to blindly chase the rally. Minor allocation changes As a result, we did not alter our allocation very much this month. We continue to look for carry, growth this month stories, relatively cheap valuations and diversification. In this context, we favour hard currency emerging market (EM) debt and subordinated debt for their carry and relatively cheap valuations. Meanwhile, we Dovish Fed should benefit are warming up to EM local currency debt because of the Federal Reserve’s very patient dovish attitude, which should cap both US rates and dollar strength. -

Evmpatch: Timely and Automated Patching of Ethereum Smart Contracts

EVMPatch: Timely and Automated Patching of Ethereum Smart Contracts Michael Rodler Wenting Li Ghassan O. Karame University of Duisburg-Essen NEC Laboratories Europe NEC Laboratories Europe Lucas Davi University of Duisburg-Essen Abstract some of these contracts hold, smart contracts have become an appealing target for attacks. Programming errors in smart Recent attacks exploiting errors in smart contract code had contract code can have devastating consequences as an attacker devastating consequences thereby questioning the benefits of can exploit these bugs to steal cryptocurrency or tokens. this technology. It is currently highly challenging to fix er- rors and deploy a patched contract in time. Instant patching is Recently, the blockchain community has witnessed several especially important since smart contracts are always online incidents due smart contract errors [7, 39]. One especially due to the distributed nature of blockchain systems. They also infamous incident is the “TheDAO” reentrancy attack, which manage considerable amounts of assets, which are at risk and resulted in a loss of over 50 million US Dollars worth of often beyond recovery after an attack. Existing solutions to Ether [31]. This led to a highly debated hard-fork of the upgrade smart contracts depend on manual and error-prone pro- Ethereum blockchain. Several proposals demonstrated how to defend against reentrancy vulnerabilities either by means of cesses. This paper presents a framework, called EVMPATCH, to instantly and automatically patch faulty smart contracts. offline analysis at development time or by performing run-time validation [16, 23, 32, 42]. Another infamous incident is the EVMPATCH features a bytecode rewriting engine for the pop- ular Ethereum blockchain, and transparently/automatically parity wallet attack [39]. -

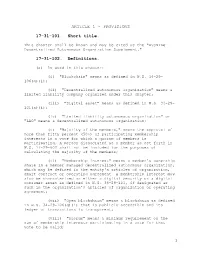

Decentralized Autonomous Organization Supplement."

ARTICLE 1 - PROVISIONS 17-31-101. Short title. This chapter shall be known and may be cited as the "Wyoming Decentralized Autonomous Organization Supplement." 17-31-102. Definitions. (a) As used in this chapter: (i) "Blockchain" means as defined in W.S. 34-29- 106(g)(i); (ii) "Decentralized autonomous organization" means a limited liability company organized under this chapter; (iii) "Digital asset" means as defined in W.S. 34-29- 101(a)(i); (iv) "Limited liability autonomous organization" or "LAO" means a decentralized autonomous organization; (v) "Majority of the members," means the approval of more than fifty percent (50%) of participating membership interests in a vote for which a quorum of members is participating. A person dissociated as a member as set forth in W.S. 17-29-602 shall not be included for the purposes of calculating the majority of the members; (vi) "Membership interest" means a member's ownership share in a member managed decentralized autonomous organization, which may be defined in the entity's articles of organization, smart contract or operating agreement. A membership interest may also be characterized as either a digital security or a digital consumer asset as defined in W.S. 34-29-101, if designated as such in the organization's articles of organization or operating agreement; (vii) "Open blockchain" means a blockchain as defined in W.S. 34-29-106(g)(i) that is publicly accessible and its ledger of transactions is transparent; (viii) "Quorum" means a minimum requirement on the sum of membership interests participating in a vote for that vote to be valid; 1 (ix) "Smart contract" means an automated transaction, as defined in W.S. -

Blockchain & Cryptocurrency Regulation

Blockchain & Cryptocurrency Regulation Third Edition Contributing Editor: Josias N. Dewey Global Legal Insights Blockchain & Cryptocurrency Regulation 2021, Third Edition Contributing Editor: Josias N. Dewey Published by Global Legal Group GLOBAL LEGAL INSIGHTS – BLOCKCHAIN & CRYPTOCURRENCY REGULATION 2021, THIRD EDITION Contributing Editor Josias N. Dewey, Holland & Knight LLP Head of Production Suzie Levy Senior Editor Sam Friend Sub Editor Megan Hylton Consulting Group Publisher Rory Smith Chief Media Officer Fraser Allan We are extremely grateful for all contributions to this edition. Special thanks are reserved for Josias N. Dewey of Holland & Knight LLP for all of his assistance. Published by Global Legal Group Ltd. 59 Tanner Street, London SE1 3PL, United Kingdom Tel: +44 207 367 0720 / URL: www.glgroup.co.uk Copyright © 2020 Global Legal Group Ltd. All rights reserved No photocopying ISBN 978-1-83918-077-4 ISSN 2631-2999 This publication is for general information purposes only. It does not purport to provide comprehensive full legal or other advice. Global Legal Group Ltd. and the contributors accept no responsibility for losses that may arise from reliance upon information contained in this publication. This publication is intended to give an indication of legal issues upon which you may need advice. Full legal advice should be taken from a qualified professional when dealing with specific situations. The information contained herein is accurate as of the date of publication. Printed and bound by TJ International, Trecerus Industrial Estate, Padstow, Cornwall, PL28 8RW October 2020 PREFACE nother year has passed and virtual currency and other blockchain-based digital assets continue to attract the attention of policymakers across the globe. -

World Watch Report

CONFIDENTIAL WORLD WATCH® REPORT ON France Date: 05/07/2019 13:57:02 GMT / UTC UnitedHealthcare Global Risk | 14141 Southwest Freeway, Suite 500 | Sugar Land, Texas 77478 ph: (713) 4307300 | email: [email protected] | url: www.uhcglobal.com World Watch® is confidential and is intended solely for the information and use of UnitedHealthcare Global's clients. Given the nature of the information, UnitedHealthcare Global does not guarantee the accuracy or completeness of the information because agencies outside the control of UnitedHealthcare Global contribute information to World Watch®. While UnitedHealthcare Global vets and verifies all information with the utmost care and consideration for the end user, UnitedHealthcare Global does not guarantee the accuracy or completeness of the information and specifically disclaims all responsibility for any liability, loss or risk, personal or otherwise, which is incurred as a consequence, directly or indirectly, of the use and application of, or reliance upon, any of the information on this site, including customized reports created by clients. Any alteration or modification of the content of World Watch®, either from the website or via printed reports, is strictly prohibited. For more information, please contact us at [email protected] or visit www.uhcglobal.com. Copyright © 2019 UnitedHealthcare Global. All rights reserved. For Terms and Conditions go to Terms Of Use World Watch® Report from UnitedHealthcare Global France Executive Summary for France France is a stable democracy located in Western Europe. To the southwest, the country borders Spain, and to the east, it borders Belgium, Germany, Italy, Luxembourg, Monaco and Switzerland. The semipresidential government is comprised of 96 mainland départements, and also has five overseas départements: French Guiana, Guadeloupe, Martinique, Mayotte and Réunion. -

Article Friis Glaser

International Journal of Community Currency Research 2018 VOLUME 22 (SUMMER) EXTENDING BLOCKCHAIN TECHNOLOGY TO HOST CUSTOMIZA- BLE AND INTEROPERABLE COMMUNITY CURRENCIES Gustav R.B. Friis* and Florian Glaser** * Brainbot Technologies AG, Mainz ** Karlsruhe Institute of Technology (KIT), Karlsruhe ABSTRACT The goal of this paper is to propose an open platform for secure and interoperable virtual community currencies. We follow the established information systems design-science approach to develop a prototype that aims to combine best practices for building mutual-credit community currencies with the unique features of blockchain technology. The result is a specification of an open Internet platform that enables users to join and to host customized community currencies. The hosted currencies can be classified as credit-based future type of money with decentralized issuance. Furthermore, we describe how the transparency, security and interoperability properties of blockchain technology offer a solution to the inherent problems of existing, centrally operated community currency software. The characteristics of the prototype and its ability to fulfil the design-objectives are examined by a relative evaluation against existing payment and currency systems like Bitcoin, LETS and M-Pesa. KEYWORDS Virtual community currencies; blockchain technology; mutual-credit; LETS; Trustlines Network To cite this article: Friis, Gustav R.B. and Glaser, Florian (2018) ‘Extending Blockchain Technology to host Customizable and Interoperable Community Currencies’ International Journal of Community Currency Research 2018 Volume 22 (Summer) 71-84 <www.ijccr.net> ISSN 1325-9547. DOI http://dx.doi.org/10.15133/j.ijccr.2018.017 INTERNATIONAL JOURNAL OF COMMUNITY CURRENCY RESEARCH 2018 VOLUME 22 (SUMMER) 71-84 FRIIS & GLASER 1. -

Offshore Markets for the Domestic Currency: Monetary and Financial Stability Issues

BIS Working Papers No 320 Offshore markets for the domestic currency: monetary and financial stability issues by Dong He and Robert N McCauley Monetary and Economic Department September 2010 JEL classification: E51; E58; F33 Keywords: offshore markets; currency internationalisation; monetary stability; financial stability BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS. Copies of publications are available from: Bank for International Settlements Communications CH-4002 Basel, Switzerland E-mail: [email protected] Fax: +41 61 280 9100 and +41 61 280 8100 This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2010. All rights reserved. Brief excerpts may be reproduced or translated provided the source is stated. ISSN 1020-0959 (print) ISBN 1682-7678 (online) Abstract We show in this paper that offshore markets intermediate a large chunk of financial transactions in major reserve currencies such as the US dollar. We argue that, for emerging market economies that are interested in seeing some international use of their currencies, offshore markets can help to increase the recognition and acceptance of the currency while still allowing the authorities to retain a measure of control over the pace of capital account liberalisation. The development of offshore markets could pose risks to monetary and financial stability in the home economy which need to be prudently managed. -

More Legal Aspects of Smart Contract Applications

More Legal Aspects of Smart Contract Applications Token Sales, Capital Markets, Supply Chain Management, Government and Smart Cities, Real Estate Registries, and Enabling Self-Sovereign Identity J. DAX HANSEN | PARTNER LAURIE ROSINI | ASSOCIATE CARLA L. REYES | ASSISTANT PROFESSOR OF LAW +1.206.359.6324 +1.206.359.3052 Director of Legal RnD - Michigan State University College of Law [email protected] [email protected] Faculty Associate - Berkman Klein Center for Internet & Society at Harvard University [email protected] PerkinsCoie.com/Blockchain Perkins Coie LLP | October 2018 Table of Contents INTRODUCTION .............................................................................................................................................................................. 3 I. A (VERY) BRIEF INTRODUCTION TO SMART CONTRACTS ............................................................................................... 3 THE ORIGINS OF SMART CONTRACTS ........................................................................................................................................................................... 3 SMART CONTRACTS IN A DISTRIBUTED LEDGER TECHNOLOGY WORLD ....................................................................................................... 4 II. CURRENT ACADEMIC LITERATURE AND INDUSTRY INITIATIVES RELATING TO SMART CONTRACTS .................... 6 SMART CONTRACTS AND CONTRACT LAW ................................................................................................................................................................ -

JTL|RELIT Vol

B T P S Journal of Transport Literature JTL|RELIT Vol. 7, n. 4, pp. 50-74, Oct. 2013 Brazilian Transportation www.transport-literature.org Planning Society Research Directory ISSN 2238-1031 The effect of social stigma on fare evasion in Stockholm's public transport [O efeito do estigma social sobre evasão de tarifa no transporte público de Estocolmo] Adeline Sterner, Shu Sheng* Stockholm School of Economics - Sweden Submitted 29 Dec 2012; received in revised form 14 Jan 2013; accepted 21 Jan 2013 Abstract This study examines if there is any social stigma associated with ticket-controls in Stockholm’s subway. We used a survey- based model that measures the willingness to pay for a subway card given different types and number of ticket-controls. By comparing the willingness to pay between the different scenarios we obtained the perceived social stigma in local currency (SEK). Our main result is an increase in the willingness to pay for a subway card of SEK 612 per year when controls are associated with social stigma. However, already fare evading respondents do not react as heavily to social stigma as non-fare evaders. These finding suggest that investing in more stigmatizing ticket controls is not preferable since fare evaders will not be affected by it. Key words: social stigma, fare evasion, free-rider problem, public transport, social norms. Resumo Este estudo examina se há algum problema de estigma social associado aos controles de bilhete no metrô de Estocolmo. Usamos um modelo baseado em pesquisas que mede a disposição a pagar por um cartão de metrô dados diferentes tipos e números de controles de bilhetes.