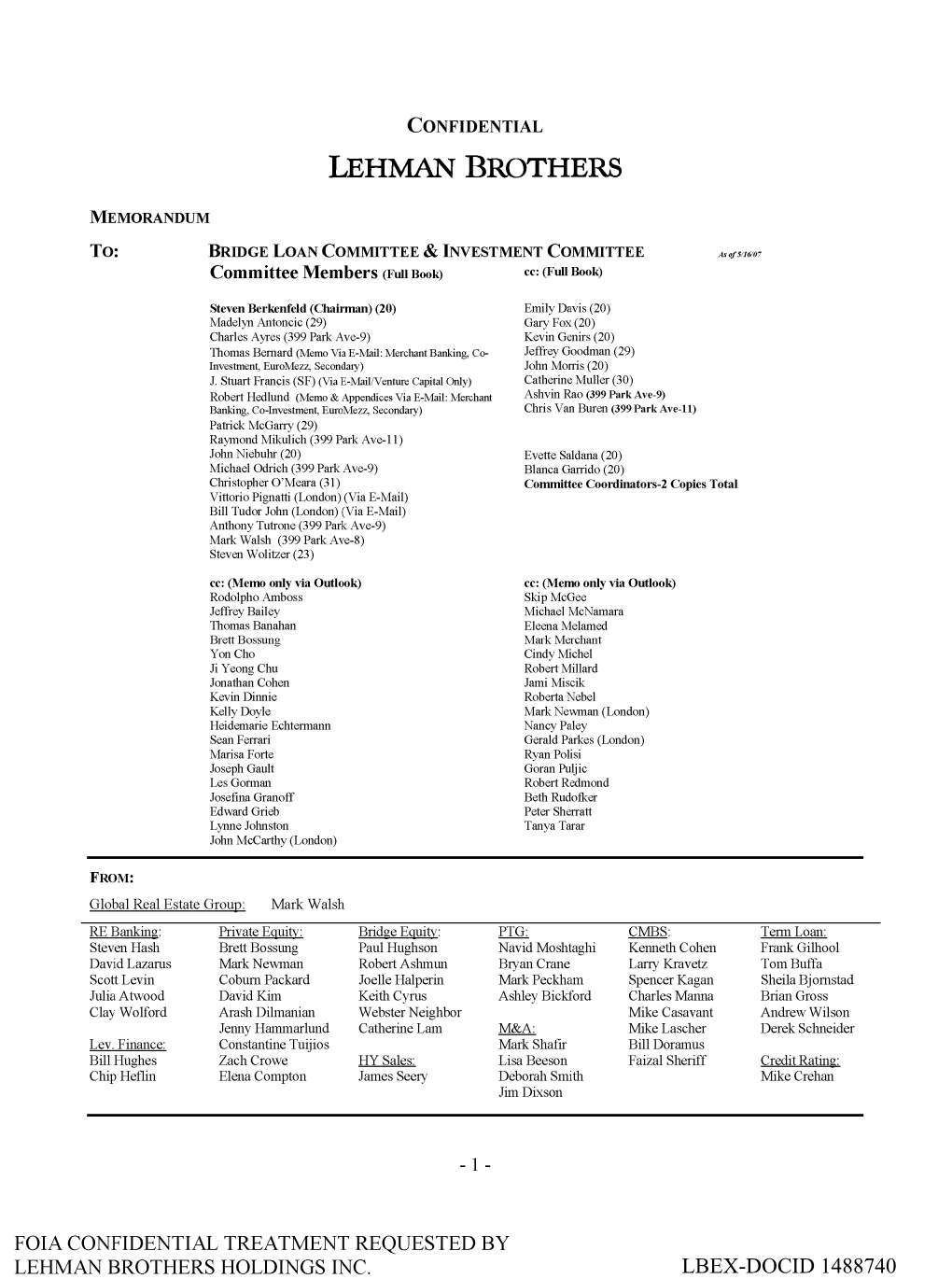

Lehman Brothers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Corporate Governance Lessons from the Financial Crisis

ISSN 1995-2864 Financial Market Trends © OECD 2009 Pre-publication version for Vol. 2009/1 The Corporate Governance Lessons from the Financial Crisis Grant Kirkpatrick * This report analyses the impact of failures and weaknesses in corporate governance on the financial crisis, including risk management systems and executive salaries. It concludes that the financial crisis can be to an important extent attributed to failures and weaknesses in corporate governance arrangements which did not serve their purpose to safeguard against excessive risk taking in a number of financial services companies. Accounting standards and regulatory requirements have also proved insufficient in some areas. Last but not least, remuneration systems have in a number of cases not been closely related to the strategy and risk appetite of the company and its longer term interests. The article also suggests that the importance of qualified board oversight and robust risk management is not limited to financial institutions. The remuneration of boards and senior management also remains a highly controversial issue in many OECD countries. The current turmoil suggests a need for the OECD to re-examine the adequacy of its corporate governance principles in these key areas. * This report is published on the responsibility of the OECD Steering Group on Corporate Governance which agreed the report on 11 February 2009. The Secretariat’s draft report was prepared for the Steering Group by Grant Kirkpatrick under the supervision of Mats Isaksson. FINANCIAL MARKET TRENDS – ISSN 1995-2864 - © OECD 2008 1 THE CORPORATE GOVERNANCE LESSONS FROM THE FINANCIAL CRISIS Main conclusions The financial crisis can This article concludes that the financial crisis can be to an be to an important important extent attributed to failures and weaknesses in corporate extent attributed to governance arrangements. -

Lehman Brothers Inc. and Barclays Agree to End Litigation and Resolve Claims Wind-Down of Estate Continues

Lehman Brothers Inc. and Barclays Agree to End Litigation and Resolve Claims Wind-Down of Estate Continues New York, June 5, 2015 – James W. Giddens, Trustee for the liquidation of Lehman Brothers Inc. (LBI) under the Securities Investor Protection Act (SIPA), and Barclays Capital Inc. and Barclays Bank PLC today agreed to resolve certain claims and end all ongoing and potential litigation between them. The agreement is consistent with past orders and judgments entered in the litigation and is subject to approval by U.S. Bankruptcy Judge, the Honorable Shelley C. Chapman. “It has always been our duty to prudently and diligently pursue every avenue of recovery for assets we believe belong to the estate, and we did so on behalf of creditors by taking the Barclays litigation all the way to the Supreme Court,” Giddens said. “This agreement ends years of litigation and achieves the best result under the circumstances as winding-down and closing out the estate continues in earnest.” Barclays purchased Lehman’s brokerage business following a hearing in Bankruptcy Court that began on September 19, 2008. Immediately after the purchase, the Trustee set in motion the transfer to Barclays of more than 110,000 customer accounts representing more than $92 billion in customer property. At the same time, the Trustee and Barclays engaged in complex and lengthy litigation over certain disputed assets. The Trustee was successful in Bankruptcy Court after 34 days of trial in a case that presented complex and novel legal issues. Subsequently, various appeals court rulings sided with Barclays. The litigation is now concluded as part of this agreement. -

The Immediate and Lasting Impacts of the 2008 Economic Collapse—Lehman Brothers, General Motors, and the Secured Credit Markets

DO NOT DELETE 4/22/2011 11:28 AM THE IMMEDIATE AND LASTING IMPACTS OF THE 2008 ECONOMIC COLLAPSE—LEHMAN BROTHERS, GENERAL MOTORS, AND THE SECURED CREDIT MARKETS Edward J. Estrada * I. INTRODUCTION Following the economic meltdown that began in the spring of 2008, immediate and longer term ramifications began to ripple through all aspects of the economy. Clearly, these tremors have not yet subsided, and continued fallout will be felt in the coming years. Importantly, even those companies and industries that have seemingly passed through the most immediate wave of im- pacts will be susceptible to the ongoing struggle to achieve sus- tainable growth. Many such companies may experience future de- faults, largely dependent upon the strength and vitality of economic growth in the coming year and their industry perfor- mance in that timeframe. In 2008, as the financial giants of the world began to struggle and collapse, some in the course of a few days, it was widely be- lieved that the credit markets, and in turn the global economy, would completely seize up, causing an economic catastrophe un- paralleled in modern history.1 While tumultuous, what did in fact happen was something far less dramatic, but it had a lasting negative impact, nevertheless. As often happens in crises, some impacts were to be expected and other events were complete surprises. For example, the re- sulting flight from risk by investors (both corporate and individu- * Partner in the Commercial Restructuring and Bankruptcy Group of the New York office of Reed Smith LLP. The author would like to thank Aaron Bourke, an associate in the Commercial Restructuring and Bankruptcy Group of the New York office of Reed Smith LLP, for his contributions to the article. -

Annual Report 2018

2018Annual Report Annual Report July 1, 2017–June 30, 2018 Council on Foreign Relations 58 East 68th Street, New York, NY 10065 tel 212.434.9400 1777 F Street, NW, Washington, DC 20006 tel 202.509.8400 www.cfr.org [email protected] OFFICERS DIRECTORS David M. Rubenstein Term Expiring 2019 Term Expiring 2022 Chairman David G. Bradley Sylvia Mathews Burwell Blair Effron Blair Effron Ash Carter Vice Chairman Susan Hockfield James P. Gorman Jami Miscik Donna J. Hrinak Laurene Powell Jobs Vice Chairman James G. Stavridis David M. Rubenstein Richard N. Haass Vin Weber Margaret G. Warner President Daniel H. Yergin Fareed Zakaria Keith Olson Term Expiring 2020 Term Expiring 2023 Executive Vice President, John P. Abizaid Kenneth I. Chenault Chief Financial Officer, and Treasurer Mary McInnis Boies Laurence D. Fink James M. Lindsay Timothy F. Geithner Stephen C. Freidheim Senior Vice President, Director of Studies, Stephen J. Hadley Margaret (Peggy) Hamburg and Maurice R. Greenberg Chair James Manyika Charles Phillips Jami Miscik Cecilia Elena Rouse Nancy D. Bodurtha Richard L. Plepler Frances Fragos Townsend Vice President, Meetings and Membership Term Expiring 2021 Irina A. Faskianos Vice President, National Program Tony Coles Richard N. Haass, ex officio and Outreach David M. Cote Steven A. Denning Suzanne E. Helm William H. McRaven Vice President, Philanthropy and Janet A. Napolitano Corporate Relations Eduardo J. Padrón Jan Mowder Hughes John Paulson Vice President, Human Resources and Administration Caroline Netchvolodoff OFFICERS AND DIRECTORS, Vice President, Education EMERITUS & HONORARY Shannon K. O’Neil Madeleine K. Albright Maurice R. Greenberg Vice President and Deputy Director of Studies Director Emerita Honorary Vice Chairman Lisa Shields Martin S. -

Donors 2015-2016 the Museum of Modern Art Moma PS1

Donors 2015-2016 The Museum of Modern Art MoMA PS1 1 Trustees of The Museum of Modern Art Jerry I. Speyer Glenn Dubin Joan Tisch Chairman John Elkann Edgar Wachenheim III Laurence Fink Leon D. Black Glenn Fuhrman Honorary Trustees Co-Chairman Kathleen Fuld Lin Arison Howard Gardner Mrs. Jan Cowles Marie-Josée Kravis Anne Dias Griffin Lewis B. Cullman President Mimi Haas H.R.H. Duke Franz of Bavaria Alexandra A. Herzan Maurice R. Greenberg Sid R. Bass Marlene Hess Wynton Marsalis Mimi Haas Ronnie Heyman Richard E. Oldenburg* Marlene Hess AC Hudgins Lord Rogers of Riverside Richard E. Salomon Jill Kraus Ted Sann Vice Chairmen Marie-Josée Kravis Gilbert Silverman Ronald S. Lauder Yoshio Taniguchi Glenn D. Lowry Thomas H. Lee Eugene V. Thaw Director Michael Lynne Khalil Gibran Muhammad *Director Emeritus Richard E. Salomon Philip S. Niarchos Treasurer James G. Niven Ex-Officio Peter Norton Glenn D. Lowry James Gara Daniel S. Och Director Assistant Treasurer Maja Oeri Michael S. Ovitz Agnes Gund Patty Lipshutz Ronald O. Perelman Chairman of the Board of MoMA PS1 Secretary David Rockefeller, Jr. Sharon Percy Rockefeller Sharon Percy Rockefeller David Rockefeller Richard E. Salomon President of the International Council Honorary Chairman Marcus Samuelsson Anna Deavere Smith Thomas R. Osborne Ronald S. Lauder Jerry I. Speyer Ann Schaffer Honorary Chairman Ricardo Steinbruch Co-Chairmen of The Contemporary Daniel Sundheim Arts Council Robert B. Menschel Alice M. Tisch Chairman Emeritus Gary Winnick Bill de Blasio Mayor of the City of New York Agnes Gund Life Trustees President Emerita Eli Broad Gabrielle Fialkoff Douglas S. -

As Parex Banka

AS PAREX BANKA ANNUAL REPORT FOR THE YEAR ENDED 31 DECEMBER 2008 TOGETHER WITH INDEPENDENT AUDITORS’ REPORT Table of Contents Management Report 3 Management of the Bank 7 Statement of Responsibility of the Management 8 Financial Statements: Statements of Income 9 Balance Sheets 10 Statements of Changes in Equity 11 Statements of Cash Flows 13 Notes 14 Auditors’ Report 80 AS Parex banka Smilšu 3, Riga, LV-1522, Latvia Phone: (371) 67010 000 Facsimile: (371) 67010 001 Registration number: 40003074590 2 AS Parex banka Management Report The year 2008 brought major change to Parex banka , including substantial changes in shareholders structure and the management of the bank in the last months of 2008. This report has been prepared by the new Management Board and Supervisory Council of the Bank and they are committed to leading the Bank into a new phase of development. Financial crisis and its implications on Parex banka The year of 2008 brought unprecedented challenges for the financial sector both in Latvia and worldwide. The global credit crunch, starting in the United States of America, caused a chain reaction all over the world and intensified the economic difficulties in Latvia. The financial sector in Latvia has been affected in a number of ways, mostly through reduced availability of funding and liquidity from international financial markets, a weakening economy and the resulting decline of asset quality. The crisis has necessitated the adoption of new approaches to the financial sector and has led to a thorough reconsideration of its practices. Parex banka itself experienced a severe impact from the crisis of 2008. -

Public Housing in the 21St Century

Public Housing in the 21st Century Acknowledgements When the New York City Housing Authority turned to Citizens Housing and Planning Council to organize a conversation about the future of public housing and report on the findings, we turned to our supporters for help. Thanks to their long standing commitment to affordable housing, we received generous support and assistance from The Fannie Mae Foundation Citi Community Capital Goldman Sachs, Public Sector Investment Group We gratefully acknowledge their role in carrying out this work. We also thank the New York City Housing Authority for its invaluable collaboration in this effort. Sincerely, The Board and Staff of Citizens Housing and Planning Council 1 2 Contents Acknowledgments 1 Contents 3 PH21 Roundtable Participants 4 A Note from the Co-Chairs 5 Introduction 6 Presentations PHAs and Capital Markets 9 Housing Supply, Housing Need, and the Role of Public Housing in NYC 9 Public Housing Reforms in the United Kingdom 11 Three Public Housing Case Studies 12 Survey Respondents 14 Survey Findings 15 Roundtable Findings 18 Recommendations 21 CHPC Board of Directors 22 3 PH21 Roundtable Participants Roundtable Co-Chairs Doug Apple, General Manager New York City Housing Authority Alicia Glen, Managing Director Goldman Sachs & Co. Tino Hernandez, Chairman New York City Housing Authority Jerilyn Perine, Executive Director Citizens Housing and Planning Council Panelists Ray Adkins, Senior Business Developer Fannie Mae Richard D. Baron, Chairman and CEO McCormack Baron Salazar Rafael Cestero, Senior Vice President Enterprise Community Partners, Inc. Kurt Creager, Principal Urbanist Housing Solutions Shaun Donovan, Commissioner NYC Dept. of Housing Preservation and Development Mary Brennan, Senior Vice President Community Preservation Corporation Paul Graziano, Housing Commissioner Baltimore Housing Carl Greene, Executive Director Philadelphia Housing Authority Jon Gutzmann, Executive Director St. -

1. the Composition, Membership, Vacancies On, And/Or Appointments to Be Made to the Intelligence Oversight Board ('IOB') 2

OFFICE OF THE DIRECTOR OF NATIONAL INTELLIGENCE WASHINGTON, DC 20511 Mr. Mark Rumold Electronic Frontier Foundation 454 Shotwell Street San Francisco, CA 94110 OCT 6 m Reference: DF-2011-00046 Dear Mr. Rumold: This responds to your 15 February 2011 facsimile to the Office of the Director of National Intelligence, wherein you requested, under the Freedom of Information Act (FOIA), the following information: 1. The composition, membership, vacancies on, and/or appointments to be made to the Intelligence Oversight Board ('IOB') 2. Any discussions or communications between officials or employees of ODNI and any White House officials or employees regarding the composition, membership, vacancies on, and/or appointments to be made to the IOB. 3. Any discussions or communications between officials or employees of ODNI and officials or employees of other intelligence agencies regarding the composition, membership, vacancies on, and/or appointments to be made to the IOB. 4. Any discussions or communications between officials or employees of ODNI and any member of Congress or congressional staffer regarding the composition, membership, vacancies on, and/or appointments to be made to the IOB. 5. Any discussions or communications regarding the reasons, explanations, or rationales provided for President Obama's appointment of, or the failure to appoint, members to the IOB. As this response completes our processing of your request, we have administratively closed your 28 February 2011 appeal of our denial of expedited processing. Your request was processed in accordance with the FOIA, 5 U.S.C. § 552, as amended. ODNI searches resulted in the location of three documents responsive to your request. -

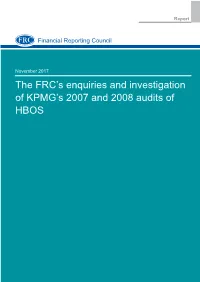

The FRC's Enquiries and Investigation of KPMG's 2007 and 2008 Audits Of

Report Professional discipline Financial Reporting Council November 2017 The FRC’s enquiries and investigation of KPMG’s 2007 and 2008 audits of HBOS The FRC’s mission is to promote transparency and integrity in business. The FRC sets the UK Corporate Governance and Stewardship Codes and UK standards for accounting and actuarial work; monitors and takes action to promote the quality of corporate reporting; and operates independent enforcement arrangements for accountants and actuaries. As the Competent Authority for audit in the UK the FRC sets auditing and ethical standards and monitors and enforces audit quality. The FRC does not accept any liability to any party for any loss, damage or costs howsoever arising, whether directly or indirectly, whether in contract, tort or otherwise from any action or decision taken (or not taken) as a result of any person relying on or otherwise using this document or arising from any omission from it. © The Financial Reporting Council Limited 2017 The Financial Reporting Council Limited is a company limited by guarantee. Registered in England number 2486368. Registered Offi ce: 8th Floor, 125 London Wall, London EC2Y 5AS Contents Page 1 Executive Summary ........................................................................................................ 3 2 Summary Background: HBOS and the contemporaneous banking and financial conditions ........................................................................................................................ 6 3 Accounting Requirements and Auditing -

Sonny Bazbaz (MBA ’04) Enjoys the Views at Real Estate Giant Fisher Brothers

FALL/WINTER 2005 the Alumni Magazine of NYU Stern STERNbusiness HIGH RISE Sonny Bazbaz (MBA ’04) enjoys the views at real estate giant Fisher Brothers Jack Welch Headlines Stellar CEO Lineup ■ Stern Entrepreneurs Make Business Plans Pay ■ Is Your 401(k) OK? ■ Why Soap Costs $1.99 Digital Rights and Wrongs ■ Hollywood’s Boffo Foreign Box Office a letter fro m the dean Welcome to the new and companies to manage digital rights? Why does a six- improved STERNbusiness. pack of cola priced at $3.99 strike consumers as being For many years, the maga- a lot cheaper than a $4.00 six-pack? zine has functioned as a As you read through the magazine, it will be clear highly effective – and visu- that Stern regards New York City as not just its home, ally appealing – showcase but as a classroom and laboratory. Because of our for the prodigious and var- location, our students and faculty have the rare abili- ied research of our faculty. ty to see and experience things first-hand, to learn With this issue, the maga- directly from practitioners at the highest levels in cru- zine has been redesigned and re-imagined. Its vision, cial fields. In an “only in New York” story (p. 10), scope, and circulation have all been expanded. Sonny Bazbaz (MBA ’04), within two years of arriving Why change a good thing? in the city, became a teaching assistant and then a col- NYU Stern may be a group of buildings in league to Richard Fisher of the real estate firm Fisher Greenwich Village. -

Physical Education and Athletics at Horace Mann, Where the Life of the Mind Is Strengthened by the Significance of Sports

magazine Athletics AT HORACE MANN SCHOOL Where the Life of the Mind is strengthened by the significance of sports Volume 4 Number 2 FALL 2008 HORACE MANN HORACE Horace Mann alumni have opportunities to become active with their School and its students in many ways. Last year alumni took part in life on campus as speakers and participants in such dynamic programs as HM’s annual Book Day and Women’s Issues Dinner, as volunteers at the School’s Service Learning Day, as exhibitors in an alumni photography show, and in alumni athletic events and Theater For information about these and other events Department productions. at Horace Mann, or about how to assist and support your School, and participate in Alumni also support Horace Mann as participants in HM’s Annual Fund planning events, please contact: campaign, and through the Alumni Council Annual Spring Benefit. This year alumni are invited to participate in the Women’s Issues Dinner Kristen Worrell, on April 1, 2009 and Book Day, on April 2, 2009. Book Day is a day that Assistant Director of Development, engages the entire Upper Division in reading and discussing one literary Alumni Relations and Special Events work. This year’s selection is Ragtime. The author, E.L. Doctorow, will be the (718) 432-4106 or keynote speaker. [email protected] Upcoming Events November December January February March April May June 5 1 3 Upper Division Women’s HM Alumni Band Concert Issues Dinner Council Annual Spring Benefit 6-7 10 6 2 6 5-7 Middle Robert Buzzell Upper Division Book Day, Bellet HM Theater Division Memorial Orchestra featuring Teaching Alumni Theater Games Concert E.L. -

Lonelier Heart Surgery Centers

20101213-NEWS--0001-NAT-CCI-CN_-- 12/10/2010 8:23 PM Page 1 INSIDE TOP STORIES Inside AOL’s Why our airports struggle to reinvent need an upgrade itself after a Yahoo ® —William Rudin and Jonathan Tisch tie-up dead-ends on improving NY’s air travel network P. 11 PAGE 3 Restaurants stay VOL. XXVI, NO. 50 WWW.CRAINSNEWYORK.COM DECEMBER 13-19, 2010 PRICE: $3.00 open later, filling nightlife void PAGE 2 Lonelier Boom heart in all things surgery B’klyn, from salsa to wine centers PAGE 3 Good: Operations Under fire, the decline. Bad: So do Bents beat a retreat hospitals’ revenues PAGE 4 Alair Townsend bids BY GALE SCOTT farewell to some WHEN 70-YEAR-OLD Francis Benner vis- ited his Mount Sinai Hospital cardiol- great New Yorkers ogist recently, he knew he might need PAGE 12 angioplasty and stent placement—pro- cedures in which doctors use a catheter to clear a blocked artery and insert a de- vice to keep it open. Instead, he had a pleasant surprise. Dr. Samin Sharma, director of Mount Sinai’s interventional cardiology clinic, told Mr.Benner that the procedure was- n’t necessary, and that he would do fine with medication and some weight loss. “I was definitely relieved,” says Mr. Benner, a retired financial services ex- ecutive who lives in Merrick, L.I. “You don’t want to have an operation if you USINESS IVES don’t have to.” B L His experience signals a shift in how doctors treat heart problems. With na- GOTHAM GIGS See CARDIOLOGY on Page 20 Life is sweet for this enrico varrasso Sugar Plum Fairy P.