Phoenix/AXA Full Text Decision

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

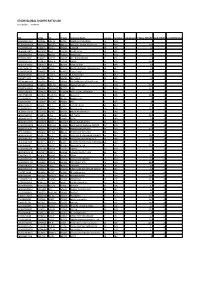

STOXX GLOBAL SHARPE RATIO 100 Selection List

STOXX GLOBAL SHARPE RATIO 100 Last Updated: 20200918 ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) Rank (FINAL)Rank (PREVIOUS) AU000000MIN4 B17ZL56 MIN.AX B17ZL5 MINERAL RESOURCES AU AUD Y 3 1 AU000000FMG4 6086253 FMG.AX 608625 Fortescue Metals Group Ltd. AU AUD Y 18.7 2 CH0267291224 BVSS671 SRCG.S CH501Z SUNRISE CH CHF Y 3.4 3 GB00B06QFB75 B06QFB7 IGG.L B06QFB IG GRP HLDG GB GBP Y 3.3 4 AU000000JBH7 6702623 JBH.AX 670262 JB Hi-Fi Ltd. AU AUD Y 3.6 5 SE0000862997 7240371 BILL.ST 724037 BILLERUDKORSNAS SE SEK Y 2.6 6 US00287Y1091 B92SR70 ABBV.N US20SG ABBVIE US USD Y 118.2 7 GB00B18V8630 B18V863 PNN.L 082699 PENNON GRP GB GBP Y 4.7 8 LU1072616219 BMTRW10 BMEB.L GB40FA B&M EUROPEAN VALUE RETAIL GB GBP Y 4.5 9 AU0000030678 BYWR0T5 COL.AX AU80Q2 Coles Group AU AUD Y 14.6 10 GB00B02J6398 B02J639 ADML.L 926294 ADMIRAL GRP GB GBP Y 7 11 JE00B5TT1872 B5TT187 CEY.L GB60EB CENTAMIN GB GBP Y 2.7 12 PTEDP0AM0009 4103596 EDP.LS 524918 EDP ENERGIAS DE PORTUGAL PT EUR Y 12 13 AU000000WES1 6948836 WES.AX 694883 Wesfarmers Ltd. AU AUD Y 33.3 14 DE000ENAG999 4942904 EONGn.DE 492752 E.ON DE EUR Y 22.2 15 US5007541064 BYRY499 KHC.OQ US20MA KRAFT HEINZ COMPANY US USD Y 9.5 16 US6937181088 2665861 PCAR.OQ PCAR Paccar Inc. US USD Y 24.8 17 JP3768600003 6414401 1808.T 641440 Haseko Corp. JP JPY Y 3.4 18 IT0003128367 7144569 ENEI.MI 579802 ENEL IT EUR Y 59 19 GB00B1FH8J72 B1FH8J7 SVT.L 079851 SEVERN TRENT GB GBP Y 6.3 20 AU000000RIO1 6220103 RIO.AX 622010 Rio Tinto Ltd. -

Phoenix Group Holdings

PROSPECTUS DATED 25 SEPTEMBER 2020 Phoenix Group Holdings plc (incorporated with limited liability in England and Wales with registered number 11606773) £5,000,000,000 Euro Medium Term Note Programme Under the Euro Medium Term Note Programme described in this Prospectus (the “Programme”) Phoenix Group Holdings plc (“Phoenix” or “PGH” or the “Issuer”), subject to compliance with all relevant laws, regulations and directives, may from time to time issue notes (the “Notes”). The Notes may be issued (i) as dated unsubordinated notes (“Senior Notes”), (ii) as dated subordinated notes with terms capable of qualifying as Tier 3 Capital (as defined in “Terms and Conditions of the Tier 3 Notes”) (“Tier 3 Notes”), (iii) as dated subordinated notes with terms capable of qualifying as Tier 2 Capital (as defined in “Terms and Conditions of the Tier 2 Notes”) (“Dated Tier 2 Notes”) or as undated subordinated notes with terms capable of qualifying as Tier 2 Capital (as defined in “Terms and Conditions of the Tier 2 Notes”) (“Undated Tier 2 Notes” and, together with the Dated Tier 2 Notes, the “Tier 2 Notes”). The Tier 2 Notes and the Tier 3 Notes are referred to collectively in this Prospectus as the “Subordinated Notes”. The aggregate nominal amount of Notes outstanding will not at any time exceed £5,000,000,000 (or the equivalent in other currencies). Payments of interest and principal under the Subordinated Notes may be subject to optional or mandatory deferral in accordance with the terms of the relevant Series (as defined herein) of Subordinated Notes. This Prospectus has been approved by the United Kingdom Financial Conduct Authority (the “FCA”), as competent authority under Regulation (EU) 2017/1129 (the “Prospectus Regulation”) as a base prospectus (the “Prospectus”) for the purposes of the Prospectus Regulation. -

Swiss Re Confirms Interest in Certain Closed-Books of Resolution

News release ab Swiss Re confirms interest in certain closed-books of Resolution Contact: Zurich, 15 October 2007 - Swiss Reinsurance Company (“Swiss Re”) confirms it is in discussions with Standard Life PLC Media Relations, Zurich Telephone +41 43 285 7171 (“Standard Life”) in relation to the possibility of entering into an agreement to purchase certain closed-books of Resolution PLC’s Corporate Communications, London Telephone +44 20 7933 3448 (“Resolution”) life business should Standard Life make an offer to acquire Resolution. These discussions are consistent with Swiss Corporate Communications, Asia Telephone +852 2582 3660 Re’s strategy to seek attractive opportunities to expand its Admin Re® business. No binding commitments have yet been entered Corporate Communications, New York Telephone +1 212 317 5663 into regarding the terms of such a transaction, and consequently there can be no assurance that Swiss Re will participate in any Investor Relations, Zurich Telephone +41 43 285 4444 such transaction or otherwise participate in any offer for Resolution, or as to the terms of any such transaction. Should a transaction take place, Swiss Re will acquire for a fixed price to be agreed certain books of business currently owned by Swiss Reinsurance Company Resolution. A further announcement may be made, if and when, Mythenquai 50/60 appropriate. P.O. Box CH-8022 Zurich Dealing Disclosure Requirements Telephone +41 43 285 2121 Fax +41 43 285 2999 Under the provisions of Rule 8.3 of the Takeover Code (the www.swissre.com “Code”), if any person is, or becomes, “interested” (directly or indirectly) in 1% or more of any class of “relevant securities” of Standard Life or of Resolution all “dealings” in any “relevant securities” of that company (including by means of an option in respect of, or a derivative referenced to, any such “relevant securities”) must be publicly disclosed by no later than 3.30 pm (London time) on the London business day following the date of the relevant transaction. -

Robert W. Stirling

Robert W. Stirling Partner, London Insurance; Financial Institutions Robert Stirling focuses on insurance and asset management matters, as well as the regula- tory issues involved in transactional work and the insurance sector generally. He advises on public and private acquisitions, private equity investments, portfolio and other risk transfers, share offerings and asset disposals. Mr. Stirling also has handled numerous representations for clients such as Phoenix Group, Mitsui Sumitomo Insurance Co., Endurance Specialty Holdings, Prudential plc, Marsh and TDR Capital. Mr. Stirling is recognised as a leading individual in non-contentious insurance in Best Lawyers in the UK, IFLR1000, The Legal 500 UK and Chambers UK, which cites his “sophisticated transactional insurance practice” and quotes clients saying: “He has gravitas, he’s pragmatic and he can think his way out of difficult problems. He’s a standout.” Prior to joining Skadden in 2014, Mr. Stirling was head of the non-contentious insurance T: 44.20.7519.7051 practice at a Magic Circle firm. F: 44.20.7072.7051 [email protected] Mr. Stirling also has advised financial institutions on transactional and regulatory matters, including Barclays Capital, BNP Paribas and Credit Suisse. His recent representations include advising: Education University of Cambridge - Phoenix Group Holdings in its: The College of Law, Guildford • £2.9 billion acquisition of Standard Life Assurance Limited from Standard Life Aber- deen plc; and Bar Admissions • acquisition of Abbey Life from Deutsche Bank AG for £935 million, in respect of the Solicitor of the Supreme Court transaction documentation and the connected rights issue; of England and Wales - The Travelers Companies, Inc. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

Wilmington Funds Holdings Template DRAFT

Wilmington Global Alpha Equities Fund as of 5/31/2021 (Portfolio composition is subject to change) ISSUER NAME % OF ASSETS USD/CAD FWD 20210616 00050 3.16% DREYFUS GOVT CASH MGMT-I 2.91% MORGAN STANLEY FUTURE USD SECURED - TOTAL EQUITY 2.81% USD/EUR FWD 20210616 00050 1.69% MICROSOFT CORP 1.62% USD/GBP FWD 20210616 49 1.40% USD/JPY FWD 20210616 00050 1.34% APPLE INC 1.25% AMAZON.COM INC 1.20% ALPHABET INC 1.03% CANADIAN NATIONAL RAILWAY CO 0.99% AIA GROUP LTD 0.98% NOVARTIS AG 0.98% TENCENT HOLDINGS LTD 0.91% INTACT FINANCIAL CORP 0.91% CHARLES SCHWAB CORP/THE 0.91% FACEBOOK INC 0.84% FORTIVE CORP 0.81% BRENNTAG SE 0.77% COPART INC 0.75% CONSTELLATION SOFTWARE INC/CANADA 0.70% UNITEDHEALTH GROUP INC 0.70% AXA SA 0.63% FIDELITY NATIONAL INFORMATION SERVICES INC 0.63% BERKSHIRE HATHAWAY INC 0.62% PFIZER INC 0.62% TOTAL SE 0.61% MEDICAL PROPERTIES TRUST INC 0.61% VINCI SA 0.60% COMPASS GROUP PLC 0.60% KDDI CORP 0.60% BAE SYSTEMS PLC 0.57% MOTOROLA SOLUTIONS INC 0.57% NATIONAL GRID PLC 0.56% PUBLIC STORAGE 0.56% NVR INC 0.53% AMERICAN TOWER CORP 0.53% MEDTRONIC PLC 0.51% PROGRESSIVE CORP/THE 0.50% DANAHER CORP 0.50% MARKEL CORP 0.49% JOHNSON & JOHNSON 0.48% BUREAU VERITAS SA 0.48% NESTLE SA 0.47% MARSH & MCLENNAN COS INC 0.46% ALIBABA GROUP HOLDING LTD 0.45% LOCKHEED MARTIN CORP 0.45% ALPHABET INC 0.44% MERCK & CO INC 0.43% CINTAS CORP 0.42% EXPEDITORS INTERNATIONAL OF WASHINGTON INC 0.41% MCDONALD'S CORP 0.41% RIO TINTO PLC 0.41% IDEX CORP 0.40% DIAGEO PLC 0.40% LENNOX INTERNATIONAL INC 0.40% PNC FINANCIAL SERVICES GROUP INC/THE 0.40% ACCENTURE -

Part VII Transfers Pursuant to the UK Financial Services and Markets Act 2000

PART VII TRANSFERS EFFECTED PURSUANT TO THE UK FINANCIAL SERVICES AND MARKETS ACT 2000 www.sidley.com/partvii Sidley Austin LLP, London is able to provide legal advice in relation to insurance business transfer schemes under Part VII of the UK Financial Services and Markets Act 2000 (“FSMA”). This service extends to advising upon the applicability of FSMA to particular transfers (including transfers involving insurance business domiciled outside the UK), advising parties to transfers as well as those affected by them including reinsurers, liaising with the FSA and policyholders, and obtaining sanction of the transfer in the English High Court. For more information on Part VII transfers, please contact: Martin Membery at [email protected] or telephone + 44 (0) 20 7360 3614. If you would like details of a Part VII transfer added to this website, please email Martin Membery at the address above. Disclaimer for Part VII Transfers Web Page The information contained in the following tables contained in this webpage (the “Information”) has been collated by Sidley Austin LLP, London (together with Sidley Austin LLP, the “Firm”) using publicly-available sources. The Information is not intended to be, and does not constitute, legal advice. The posting of the Information onto the Firm's website is not intended by the Firm as an offer to provide legal advice or any other services to any person accessing the Firm's website; nor does it constitute an offer by the Firm to enter into any contractual relationship. The accessing of the Information by any person will not give rise to any lawyer-client relationship, or any contractual relationship, between that person and the Firm. -

Axa Press Release

AXA PRESS RELEASE PARIS, FEBRUARY 23, 2017 Full Year 2016 Earnings On track towards Ambition 2020 targets Underlying earnings per share up 4% to Euro 2.24 Dividend of Euro 1.16 per share, up 5% from FY15, to be proposed by the Board of Directors Solvency II ratio of 197%, up 6 pts from 9M16 “With the commitment and the engagement of our teams, we have delivered a strong performance in the first year of our new Ambition 2020 plan”, said Thomas Buberl, Chief Executive Officer of AXA. “We recorded Euro 5.7 billion in underlying earnings, a growth of 4% on a per share basis, despite continued low interest rates and market volatility. We generated over Euro 6.2 billion of operating free cash flows and our Solvency II ratio of 197% remained well within our target range. In this context, the Board of Directors is proposing a dividend of Euro 1.16 per share, an increase of 5% versus last year, which corresponds to a payout ratio of 48%.” “AXA’s revenues crossed the Euro 100 billion mark for the first time in the company’s history. In Life & Savings, we continued to grow our profitable Protection & Health and capital light Savings businesses, in line with our strategy. In Property & Casualty, we grew in both personal and commercial lines. We also experienced significant positive net inflows in Asset Management.” “We are on track on the headline targets of our Ambition 2020 plan, focusing on the execution of clear management levers, and pursuing the transformation of the Group towards becoming the innovation leader in insurance and empowering people -

I AXA Group Solvency Ratio

REGISTRATION DOCUMENT ANNUAL FINANCIAL REPORT 2016 CERTAIN PRELIMINARY INFORMATION ABOUT THIS ANNUAL REPORT 1 Group profi le 4 Chairman and Chief Executive Offi cer’s messages 6 THE AXA GROUP 9 1.1 Key fi gures 11 1.2 History 15 1 1.3 Business overview 17 CONTENTS ACTIVITY REPORT AND CAPITAL MANAGEMENT 27 2.1 Market environment 28 2.2 Operating Highlights 33 2 2.3 Activity Report 38 2.4 Liquidity and capital resources 93 2.5 Events subsequent to December 31, 2016 100 2.6 Outlook 101 CORPORATE GOVERNANCE 103 3.1 Corporate governance structure – A balanced and effi cient governance 104 3.2 Executive compensation and share ownership 136 3 3.3 Related-party transactions 171 RISK FACTORS AND RISK MANAGEMENT 177 4.1 Risk factors 178 4.2 Internal control and risk management 190 4 4.3 Market risks 204 4.4 Credit risk 211 4.5 Liquidity risk 214 4.6 Insurance risks 215 4.7 Operational risk 219 4.8 Other material risks 220 CONSOLIDATED FINANCIAL STATEMENTS 223 5.1 Consolidated statement of fi nancial position 224 5.2 Consolidated statement of income 226 5 5.3 Consolidated statement of comprehensive income 227 5.4 Consolidated statement of changes in equity 228 5.5 Consolidated statement of cash fl ows 232 5.6 Notes to the Consolidated Financial Statements 234 5.7 Report of the Statutory Auditors on the consolidated fi nancial statements 370 SHARES, SHARE CAPITAL AND GENERAL INFORMATION 373 6.1 AXA shares 374 6.2 Share capital 375 6 6.3 General information 381 CORPORATE RESPONSIBILITY 391 7.1 General information 392 7.2 Social information 393 7 7.3 Environmental -

Fund Factsheet Indexed UK Equity 01 Oct 2021

| Retirement | Investments | Insurance | Fund Factsheet Indexed UK Equity 01 Oct 2021 FUND FACTS FUND INTRODUCTION Fund Launch Date Apr 2013 Fund Objective Fund Size €2.4m The objective of this fund is to provide broad exposure to UK Equity markets. It does so by aiming Base Currency EUR to track the performance of underlying indices rather than by active management Number of Holdings 86 Fund Strategy Tax Gross The fund is currently aiming to track the MSCI UK Index through an SSgA managed fund but MoneyMate ID 25003820 may elect to track other appropriate indices. The fund is expected to achieve strong returns in the longer term based on the performance CIV Charge 0.10% of equity markets. AMC 0% This fund is also expected to be more volatile than a mixed asset fund given the higher equity content and is suited to a longer term investment horizon. Source: Performance data quoted on a bid to bid basis i.e. the price investors sell units. FUND PERFORMANCE FUND MANAGER INFORMATION Growth of €10,000 to 01 Oct 2021 €20,000 €15,000 €10,000 Fund Manager(s) State Street Global Advisors €5,000 Fund Manager Profile State Street Global Advisors helps investors €0 around the world ranging from governments and 2014 2015 2016 2017 2018 2019 2020 2021 institutions to financial advisors find better ways to achieve their investment goals. They have a Annualised Return to 01 Oct 2021 – Indexed UK Equity long history of developing innovative investment 1m 3m YTD 1y 3y 5y 10y strategies to help their clients, and those who rely on them, achieve their investment goals. -

Notice of Annual General Meeting to Be Held on 22 May 2009

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to any aspect of the proposals referred to in this document or as to the action you should take, you should consult a stockbroker, solicitor, accountant or other appropriate independent professional adviser. If you have sold or transferred all your shares in HSBC Holdings plc (the “Company”), you should at once forward this document and the accompanying Form of Proxy to the stockbroker, bank or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. This document should be read in conjunction with the Annual Report and Accounts and/or Annual Review in respect of the year ended 31 December 2008. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. The ordinary shares of HSBC Holdings plc trade under stock code 5 on The Stock Exchange of Hong Kong Limited. Shareholders may at any time choose to receive corporate communications in printed form or to receive notifications of their availability on HSBC’s website. To receive future notifications of the availability of corporate communications on HSBC’s website by email, or revoke or amend an instruction to receive such notifications by email, go to www.hsbc.com/ecomms. -

Evolving Our BPA Franchise

Evolving our BPA Franchise Justin Grainger Head of BPA, Phoenix Group RBC 2020 Bulk Annuities Seminar 13 May 2020 1 Phoenix’s growth journey continues 2010 2013 2015 2018 Premium Listing on Debt re-terming Investment grade Acquisition of Standard Life London Stock and £250m credit rating from Assurance Limited (“SLAL”) Exchange equity raising Fitch Ratings 2011 2014 2016 2019 £5bn annuity liability Divestment of Ignis Asset Acquisition of AXA Wealth’s Announced acquisition transfer to Guardian Management pension and protection of ReAssure Group plc Assurance businesses and Abbey Life Market capitalisation (£bn) Diversified inforce business 6.0 at 31 Dec 2019 5.0 4.0 3.0 £248bn 2.0 1.0 UK Heritage – 51% UK Open – 38% 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Europe – 10% 2 Our Heritage business will grow through new annuity business Our annuity book will continue to grow(1) Phoenix’s approach to BPA is: Focus on value accretion not Selective £20bn volume Allocation of c. £100 million Proportionate of surplus capital in 2019 £10bn Funded from Capital strain funded by own resources surplus capital 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 BPA Vestings Backbook Over 90% of longevity risk Reinsured risk reinsured Provides long-term Incremental to our Annuity business is cash flows to cash generation value accretive support future Appropriate allocation to targets Asset allocation dividends illiquid assets See Appendix VII for footnotes 3 We are at the beginning of our BPA journey Market share Market segmentation Scottish Canada