A Skills Action Plan for the Low Carbon Environmental Goods and Services Sector May 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Turning the Tide, Tidal Power in the UK

Turning the tide The Sustainable Development Commission is the Government’s independent watchdog on sustainable in the UK Tidal Power development, reporting to the Prime Minister, the First Ministers of Scotland and Wales and the First Minister and Deputy First Minister of Northern Ireland. Through advocacy, advice and appraisal, we help put sustainable development at the heart of Government policy. www.sd-commission.org.uk England (Main office) 55 Whitehall London SW1A 2HH 020 7270 8498 [email protected] Scotland 3rd Floor, Osborne House 1-5 Osborne Terrace, Haymarket, Edinburgh EH12 5HG 0131 625 1880 [email protected] www.sd-commission.org.uk/scotland Wales c/o Welsh Assembly Government, Cathays Park, Cardiff CF10 3NQ Turning 029 2082 6382 Commission Development Sustainable [email protected] www.sd-commission.org.uk/wales Northern Ireland Room E5 11, OFMDFM the Tide Castle Buildings, Stormont Estate, Belfast BT4 3SR 028 9052 0196 Tidal Power in the UK [email protected] www.sd-commission.org.uk/northern_ireland Turning the Tide Tidal Power in the UK Contents Executive Summary 5 1 Introduction 15 1.1 Background to this project 16 1.2 Our approach 17 1.3 UK tidal resource 19 1.3.1 Two types of tidal resource 19 1.3.2 Electricity generating potential 22 1.3.3 Resource uncertainties 22 1.3.4 Timing of output from tidal sites 23 1.3.5 Transmission system constraints 25 1.4 Energy policy context 28 1.4.1 Current Government policy 28 1.4.2 The SDC’s advice 28 1.5 Public and stakeholder engagement -

Trade Your Way

BUSINESS WITH PERSONALITY CAM’S LEGACY NOTHING TO WINE ABOUT THE GOOD, THE BAD THE SOMMELIER’S GUIDE TO AND THE EU THE BEST VINO-TECH P23 REFERENDUM P19 WEDNESDAY 18 SEPTEMBER 2019 ISSUE 3,459 CITYAM.COM FREE French bank chief: EU to NOW WEWORK’S grow closer HARRY ROBERTSON @henrygrobertson THE Bank of France governor suggested yesterday that the European Union will move towards closer integration in FLOATJAMES WARRINGTON PUT ON ICE reports that the New York-based com- vealed in a filing last month, despite ongoing commitment,” the company the wake of Brexit. AND SEB MCCARTHY pany was considering dramatically its revenue climbing to $1.54bn. said in a statement. Francois Villeroy de Galhau, slashing the valuation it will seek “The We Company is looking for- Neil Wilson, chief market analyst at who is also a European @j_a_warrington and @sebmccarthy when it sells shares on the stock ward to our upcoming [initial public Markets.com, said: “Wework is said to Central Bank (ECB) board WEWORK has pushed back plans for market. offering], which we expect to be com- be delaying its planned IPO. Investors member, told business its highly-anticipated initial public of- We Company is reportedly looking pleted by the end of the year. We want have given it the cold shoulder. It’s delegates in London that the fering (IPO) amid cooling investor ap- at a valuation of just over $20bn to thank all of our employees, mem- been something of a lemon so far bloc’s collective response to petite. (£16.12bn), less than half the bers and partners for their with valuations drastically cut.” Britain’s departure might FRIDAY 6 SEPTEMBER 2019 SSURE GROWS S TO THE BIG SS ISSUE 3,451 P3, P16 GOING OUT P Following a number of setbacks over $47bn price tag it received in CITYAM.COM He added: “It’s amazing how the become a further shift its ambitions to go public, the fast-ris- private fundraising in January. -

LOW CARBON ENERGY OBSERVATORY ©European Union, 2019 OCEAN ENERGY Technology Market Report

LOW CARBON ENERGY OBSERVATORY ©European Union, 2019 OCEAN ENERGY Technology market report Joint EUR 29924 EN Research Centre This publication is a Technical report by the Joint Research Centre (JRC), the European Commission’s science and knowledge service. It aims to provide evidence-based scientific support to the European policymaking process. The scientific output expressed does not imply a policy position of the European Commission. Neither the European Commission nor any person acting on behalf of the Commission is responsible for the use that might be made of this publication. Contact information Name: Davide MAGAGNA Address: European Commission, Joint Research Centre, Petten, The Netherlands E-mail: [email protected] Name: Matthijs SOEDE Address: European Commission DG Research and Innovation, Brussels, Belgium Email: [email protected] EU Science Hub https://ec.europa.eu/jrc JRC118311 EUR 29924 EN ISSN 2600-0466 PDF ISBN 978-92-76-12573-0 ISSN 1831-9424 (online collection) doi:10.2760/019719 ISSN 2600-0458 Print ISBN 978-92-76-12574-7 doi:10.2760/852200 ISSN 1018-5593 (print collection) Luxembourg: Publications Office of the European Union, 2019 © European Union, 2019 The reuse policy of the European Commission is implemented by Commission Decision 2011/833/EU of 12 December 2011 on the reuse of Commission documents (OJ L 330, 14.12.2011, p. 39). Reuse is authorised, provided the source of the document is acknowledged and its original meaning or message is not distorted. The European Commission shall not be liable for any consequence stemming from the reuse. For any use or reproduction of photos or other material that is not owned by the EU, permission must be sought directly from the copyright holders. -

Digest of United Kingdom Energy Statistics 2012

Digest of United Kingdom Energy Statistics 2012 Production team: Iain MacLeay Kevin Harris Anwar Annut and chapter authors A National Statistics publication London: TSO © Crown Copyright 2012 All rights reserved First published 2012 ISBN 9780115155284 Digest of United Kingdom Energy Statistics Enquiries about statistics in this publication should be made to the contact named at the end of the relevant chapter. Brief extracts from this publication may be reproduced provided that the source is fully acknowledged. General enquiries about the publication, and proposals for reproduction of larger extracts, should be addressed to Kevin Harris, at the address given in paragraph XXIX of the Introduction. The Department of Energy and Climate Change reserves the right to revise or discontinue the text or any table contained in this Digest without prior notice. About TSO's Standing Order Service The Standing Order Service, open to all TSO account holders, allows customers to automatically receive the publications they require in a specified subject area, thereby saving them the time, trouble and expense of placing individual orders, also without handling charges normally incurred when placing ad-hoc orders. Customers may choose from over 4,000 classifications arranged in 250 sub groups under 30 major subject areas. These classifications enable customers to choose from a wide variety of subjects, those publications that are of special interest to them. This is a particularly valuable service for the specialist library or research body. All publications will be dispatched immediately after publication date. Write to TSO, Standing Order Department, PO Box 29, St Crispins, Duke Street, Norwich, NR3 1GN, quoting reference 12.01.013. -

ENERGY PRICES Briefing

SPICe ENERGY PRICES briefing SCHERIE NICOL AND GRAEME COOK 5 December 2008 Energy prices have risen between 10% and 50% over the last year with 08/70 Consumer Focus estimating the current average annual domestic energy bill to be over £1,300. With the percentage of households in fuel poverty having increased from 13% to 25% over the last 5 years and fuel prices predicted to continue to rise, energy prices have been a subject of recent interest. This briefing provides an overview of recent trends in energy prices and highlights the key factors influencing the general price of energy and the price of oil, domestic gas and electricity. It then considers the key impacts that changing energy prices have on consumers, producers and the environment before summarising the key policy levers available to the EU, the UK and Scottish Governments. Scottish Parliament Information Centre (SPICe) Briefings are compiled for the benefit of the Members of the Parliament and their personal staff. Authors are available to discuss the contents of these papers with MSPs and their staff who should contact Scherie Nicol on extension 85380 or email [email protected]. Members of the public or external organisations may comment on this briefing by emailing us at [email protected]. However, researchers are unable to enter into personal discussion in relation to SPICe Briefing Papers. If you have any general questions about the work of the Parliament you can email the Parliament’s Public Information Service at [email protected]. Every effort is made to ensure that the information contained in SPICe briefings is correct at the time of publication. -

Wind Powered Electricity in the UK Wind Powered Electricity in the UK

Special feature – Wind powered electricity in the UK Wind powered electricity in the UK This article looks at wind powered electricity in the UK, examining how its position in the UK energy mix has shifted from 2010 to 20191, and how wind capacity may change in the future. Key points • Total wind generating capacity increased by 19 GW from 5.4 GW in 2010 to 24 GW in 2019. This is the result of sizeable increases in capacity both onshore and offshore, which are up 10 GW and 8.5 GW respectively. • In the last year, UK offshore wind capacity rose 1.6 GW following the opening of Hornsea One, Beatrice extension (partially operational in 2018) and East Anglia One (partially operational). Hornsea One is now the largest offshore wind farm in the world with an operational capacity of over 1.2 GW. • In 2019, wind generators became the UK’s second largest source of electricity, providing 64 TWh; almost one fifth of the UK’s total generation. This was achieved by record onshore and offshore generation despite suboptimal conditions for wind, with 2019 reporting the lowest average wind speeds since 2012. • Onshore generation exceeded offshore for every year 2010 to 2019, however the gap narrowed each year. In 2019 the difference was marginal with each providing 32 TWh of electricity and 9.9 per cent of the UK’s total generation. • Offshore sites are typically able to use more of their available capacity for generation, as wind speed and direction are more consistent offshore. This is measured by the load factor, the proportion of maximum generation achieved. -

Marine Current Energy Conversion

Marine Current Energy Conversion Resource and Technology MÅRTEN GRABBE UURIE 309-09L ISSN 0349-8352 Division of Electricity Department of Engineering Sciences Uppsala, December 2008 Abstract Research in the area of energy conversion from marine currents has been car- ried out at the Division of Electricity for several years. The focus has been to develop a simple and robust system for converting the kinetic energy in freely flowing water to electricity. The concept is based on a vertical axis turbine di- rectly coupled to a permanent magnet synchronous generator that is designed to match the characteristics of the resource. During this thesis work a pro- totype of such a variable speed generator, rated at 5 kW at 10 rpm, has been constructed to validate previous finite element simulations. Experiments show that the generator is well balanced and that there is reasonable agreement be- tween measurements and corresponding simulations, both at the nominal op- erating point and at variable speed and variable load operation from 2–16 rpm. It is shown that the generator can accommodate operation at fixed tip speed ratio with different fixed pitch vertical axis turbines in current velocities of 0.5–2.5 m/s. The generator has also been tested under diode rectifier opera- tion where it has been interconnected with a second generator on a common DC-bus similar to how several units could be connected in offshore operation. The conditions for marine current energy conversion in Norway have been investigated based on available data in pilot books and published literature. During this review work more than 100 sites have been identified as interest- ing with an estimated total theoretical resource—i.e. -

UK Innovation Systems for New and Renewable Energy Technologies

The UK Innovation Systems for New and Renewable Energy Technologies Final Report A report to the DTI Renewable Energy Development & Deployment Team June 2003 Imperial College London Centre for Energy Policy and Technology & E4tech Consulting ii Executive summary Background and approach This report considers how innovation systems in the UK work for a range of new and renewable energy technologies. It uses a broad definition of 'innovation' - to include all the stages and activities required to exploit new ideas, develop new and improved products, and deliver them to end users. The study assesses the diversity of influences that affect innovation, and the extent to which they support or inhibit the development and commercialisation of innovative new technologies in the UK. The innovation process for six new and renewable energy sectors is analysed: • Wind (onshore and offshore) • Marine (wave and tidal stream) • Solar PV • Biomass • Hydrogen from renewables • District and micro-CHP In order to understand innovation better, the report takes a systems approach, and a generic model of the innovation system is developed and used to explore each case. The systems approach has its origins in the international literature on innovation. The organising principles are twofold: • The stages of innovation. Innovation proceeds through a series of stages, from basic R&D to commercialisation – but these are interlinked, and there is no necessity for all innovations to go through each and every stage. The stages are defined as follows: Basic and applied R&D includes both ‘blue skies’ science and engineering/application focused research respectively; Demonstration from prototypes to the point where full scale working devices are installed in small numbers; Pre-commercial captures the move from the first few multiples of units to much larger scale installation for the first time; Supported commercial is the stage where technologies are rolled out in large numbers, given generic support measures; Commercial technologies can compete unsupported within the broad regulatory framework. -

Notice Concerning Copyright Restrictions

NOTICE CONCERNING COPYRIGHT RESTRICTIONS This document may contain copyrighted materials. These materials have been made available for use in research, teaching, and private study, but may not be used for any commercial purpose. Users may not otherwise copy, reproduce, retransmit, distribute, publish, commercially exploit or otherwise transfer any material. The copyright law of the United States (Title 17, United States Code) governs the making of photocopies or other reproductions of copyrighted material. Under certain conditions specified in the law, libraries and archives are authorized to furnish a photocopy or other reproduction. One of these specific conditions is that the photocopy or reproduction is not to be "used for any purpose other than private study, scholarship, or research." If a user makes a request for, or later uses, a photocopy or reproduction for purposes in excess of "fair use," that user may be liable for copyright infringement. This institution reserves the right to refuse to accept a copying order if, in its judgment, fulfillment of the order would involve violation of copyright law. HOT DRY ROCK - A EUROPEAN PERSPECTIVE J.D. Garnish Energy Technology Support Unit AERE Harwell, Oxon, England ABSTRACT permeability but natural hydrothermal circulation in existing fractures. For the purposes of this review HDR Research into hot dry rock technology is being pursued research is defined narrowly as work directed towards the actively in several European countries. All these projects creation of a heat transfer zone in otherwise impermeable employ variations of the basic hydrofracturing approach. rock, and the extraction of useful heat by the circulation of Following proof of the concept at Los Alamos, the UK fluid through that zone. -

Water Power & Severn Barrage Review

SUPPLEMENT TO THE HISTELEC NEWS AUGUST 2007 "WATER POWER & SEVERN BARRAGE REVIEW" Two of our members, Mike Hield and Glyn England have produced articles pertaining to the Severn Barrage as prelude to the talk by David Kerr of Sir Robert MacAlpine on 10th October. ----------------------------------------------------------------------------------------------------------------------- WATER POWER by Mike Hield Introduction Normally a report on a talk is done after the event, but in the case of the talk on "The Severn Barrage" I thought a preliminary briefing would be of interest. My own interest arises from a career in SWEB as an electrical distribution engineer and my leisure activity as a dinghy sailor and yachtsman. History Man used water power as long ago as 200 BC for grain milling and water pumping, around 1100 AD for "Fulling" woollen cloth and later for processing metals. From about 1700 mathematicians and engineers started to analyse the workings of the water wheel and came to realise that the weight of water in the wheel was more significant than the impact from the flow. Isaac Newton (1642-1727) established his Second Law of Motion - i.e. Force is equal to rate of change of Momentum. Leonhard Euler (1707-1783) a Swiss mathematician developed his equation of motion for non-viscous flow. Daniel Bernoulli (1700-1782) defined three forms of energy in a fluid ie. height, velocity and pressure; these being interchangeable and the total constant. These ideas formed the basis for analysing the performance of turbines, fans and pumps. Tidal Mills were very rare as they needed to be away from damaging waves and also the relative small size of the mills made them impracticable for large tidal ranges. -

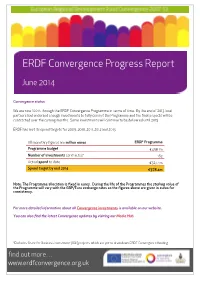

ERDF Convergence Progress Report, Jun 2014 DRAFT.Pub

ERDF Convergence Progress Report June 2014 Convergence status We are now 100% through the ERDF Convergence Programme in terms of time. By the end of 2013 local partners had endorsed enough investments to fully commit the Programme and the final projects will be contracted over the coming months. Some investments will continue to be delivered until 2015. ERDF has met its spend targets for 2009, 2010, 2011, 2012 and 2013. All monetary figures are million euros ERDF Programme Programme budget €458.1m Number of investments contracted* 163 Actual spend to date €327.4m Spend target by end 2014 €378.4m Note: The Programme allocation is fixed in euros. During the life of the Programmes the sterling value of the Programme will vary with the GBP/Euro exchange rates so the figures above are given in euros for consistency. For more detailed information about all Convergence investments is available on our website. You can also find the latest Convergence updates by visiting our Media Hub. *Excludes Grant for Business Investment (GBI) projects which are yet to draw down ERDF Convergence funding. find out more… www.erdfconvergence.org.uk CONVERGENCE INVESTMENTS New Investments Apple Aviation Ltd Apple Aviation, an aircraft maintenance, repair and overhaul company, has established a base at Newquay Airport’s Aerohub. Convergence funding from the Grant for Business Investment programme will contribute to salary costs for thirteen new jobs in the business. ERDF Convergence investment: £211,641 (through the GBI SIF) Green Build Hub Located alongside the Eden Project, the Green Build Hub will be a research facility capable of demonstrating and testing the performance of innovative sustainable construction techniques and materials in a real building setting. -

United Downs Deep Geothermal Power Project, UK. Project Update

PROCEEDINGS, 44th Workshop on Geothermal Reservoir Engineering Stanford University, Stanford, California, February 11-13, 2019 SGP-TR-214 The United Downs Deep Geothermal Power Project Peter Ledingham, Lucy Cotton and Ryan Law Geothermal Engineering Ltd, Falmouth Business Park, Bickland Water Road, Falmouth, Cornwall TR11 4SZ, UK [email protected] Keywords: United Downs, Cornwall, UK, Deep Geothermal, ABSTRACT The United Downs Deep Geothermal Power project is the first geothermal power project in the United Kingdom. It is located near Redruth in west Cornwall, UK and is part-funded by the European Regional Development Fund and Cornwall Council. The project consists of two deviated wells; a production well to a target depth of 4,500m and an injection well to a depth of 2,500m. Both wells target a sub-vertical, inactive fault structure that is thought will provide enhanced permeability relative to the surrounding granitic rock, sufficient to support circulation of between 20 and 60l/s. Geothermal gradients in Cornwall are relatively good and the bottom hole temperature is expected to be in the region of 190OC, allowing anticipated production to surface at greater than 175OC, which should allow electricity generation of between 1 and 3WMe. After funding agreements were signed in June 2017, a period of preparation and procurement followed, and drilling began in November 2018. This paper places the project in the context of previous geothermal research carried out in Cornwall, summarises the concept and describes the site selection work carried out. It also outlines the microseismic and noise monitoring programmes implemented to protect the local community and describes the public outreach, education and research initiatives associated with the project.