China Is Investing Heavily in European Wind

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report Annual Report 2020

2020 Annual Report Annual Report 2020 For further details about information disclosure, please visit the website of Yanzhou Coal Mining Company Limited at Important Notice The Board, Supervisory Committee and the Directors, Supervisors and senior management of the Company warrant the authenticity, accuracy and completeness of the information contained in the annual report and there are no misrepresentations, misleading statements contained in or material omissions from the annual report for which they shall assume joint and several responsibilities. The 2020 Annual Report of Yanzhou Coal Mining Company Limited has been approved by the eleventh meeting of the eighth session of the Board. All ten Directors of quorum attended the meeting. SHINEWING (HK) CPA Limited issued the standard independent auditor report with clean opinion for the Company. Mr. Li Xiyong, Chairman of the Board, Mr. Zhao Qingchun, Chief Financial Officer, and Mr. Xu Jian, head of Finance Management Department, hereby warrant the authenticity, accuracy and completeness of the financial statements contained in this annual report. The Board of the Company proposed to distribute a cash dividend of RMB10.00 per ten shares (tax inclusive) for the year of 2020 based on the number of shares on the record date of the dividend and equity distribution. The forward-looking statements contained in this annual report regarding the Company’s future plans do not constitute any substantive commitment to investors and investors are reminded of the investment risks. There was no appropriation of funds of the Company by the Controlling Shareholder or its related parties for non-operational activities. There were no guarantees granted to external parties by the Company without complying with the prescribed decision-making procedures. -

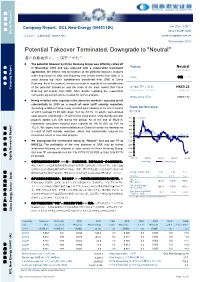

Potential Takeover Terminated, Downgrade to "Neutral" 潜在收购被终止,下调至“中性”

股 票 研 [Table_Title] Company Report: GCL New Energy (00451 HK) Jun Zhu 朱俊杰 究 (852) 2509 7592 Equity Research 公司报告: 协鑫新能源 (00451 HK) [email protected] 19 December 2019 [Table_Summary] Potential Takeover Terminated, Downgrade to "Neutral" 潜在收购被终止,下调至“中性” The potential takeover by China Huaneng Group was officially called off [Table_Rank] 公 in November 2019 and was replaced with a cooperation framework Rating: Neutral Downgraded agreement. We believe that termination of the potential takeover (majority 司 stake acquisition) of GNE and acquiring only certain assets from GNE is to 报 评级: 中性 (下调) avoid having too much indebtedness transferred from GNE to China 告 Huaneng. As of the moment, we are uncertain in regards to the consideration of the potential transaction and the scale of the solar assets that China 6[Table_Price-18m TP 目标价] : HK$0.22 Company Report Huaneng will acquire from GNE. More details regarding the cooperation Revised from 原目标价: HK$0.45 framework agreement will be needed for further analysis. Share price 股价: HK$0.172 Newly installed solar capacity in the domestic market is expected to fall substantially in 2019 as a result of solar tariff subsidy reduction. According to NEA of China, newly installed solar capacity in the first 9 months Stock performance of 2019 reached 15.99 GW, down YoY by 53.7%. In which, concentrated 股价表现 solar projects contributed 7.73 GW of new installations, while distributed solar [Table_QuotePic] 50.0 % of return projects added 8.26 GW during the period. As at the end of 9M2019, 40.0 nationwide cumulative installed solar capacity hit 190.19 GW, up YoY by 30.0 证 15.2%. -

Roadmap for the Demonstration of Carbon Capture and Storage (CCS) in China

Final Report/June 2011 ADB TA‐7286 (PRC) People’s Republic of China Carbon Dioxide Capture and Storage Demonstration – Strategic Analysis and Capacity Strengthening Roadmap for the Demonstration of Carbon Capture and Storage (CCS) in China Final Report June 2011 Final Report /June 2011 ADB TA‐7286 (PRC) People’s Republic of China Carbon Dioxide Capture and Storage Demonstration – Strategic Analysis and Capacity Strengthening Roadmap for the Demonstration of Carbon Capture and Storage (CCS) in China Final Report June 2011 Report submitted by Project Team Prof. J. YAN – Team Leader & CCS Experts Prof. H. JIN – National Co‐leader Prof. Li Z., Dr. J. Hetland, Dr. Teng F., Prof. Jiang K.J., Ms. C. J. Vincent, Dr. A. Minchener, Prof. Zeng RS, Prof. Shen PP, Dr. X. D. Pei, Dr. Wang C., Prof. Hu J, Dr. Zhang JT The views expressed are those of the Consultants and do not necessarily reflect those of the Ministry or the Asian Development Bank (ADB). i Final Report /June 2011 TABLE OF CONTENTS Tables .............................................................................................................................. iv Figures ............................................................................................................................. v Key findings: .................................................................................................................... ix Main Recommendations: ................................................................................................. xi 1. Background and Objectives ....................................................................................... -

Announcement on Replies to the Letter of Enquiry from The

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. (a Sino-foreign joint stock limited company incorporated in the People’s Republic of China) (Stock Code: 902) ANNOUNCEMENT ON REPLIES TO THE LETTER OF ENQUIRY FROM THE SHANGHAI STOCK EXCHANGE Huaneng Power International, Inc. (“the Company”), on 14 April 2020, received a Letter of Enquiry regarding Information Disclosure of 2019 Annual Report of Huaneng Power International, Inc. (Shang Zheng Gong Han [2020] No. 0350) (the “Letter of Enquiry”) from the Shanghai Stock Exchange. Upon receiving the Letter of Enquiry, the Company proactively arranged with relevant parties to carry out diligent research as well as discussion and analysis on the issues raised in the Letter of Enquiry. In accordance with the requirements of the Letter of Enquiry, replies to relevant issues are as follows: I. In relation to Assets Impairment with Significant Amount According to the annual report, the Company accrued significant asset impairment of RMB5.886 billion at the end of the reporting period. To this, please supplement and explain each of the following items: 1. In relation to aggregate impairment amount of RMB3.818 billion for the 10 asset groups, including Huaneng Yushe Power Generation Co., -

Advancing Clean Energy & Sustainable Energy Infrastructure

Advancing Clean Energy & Sustainable Energy Infrastructure through PEER A BRIEF ON CHINA’S ENERGY INITIATIVES MAY 2020 BACKGROUND China’s power sector services 1.1 billion consumers, supplying 6,994 TWh from more than 1.91 TW of installed capacity. Coal is the primary source of electricity generation in China. The total installed capacity of renewable energy (including hydropower) in China is more than 728 GW. At the end of 2018, China’s power sector continued to be dominated by large state-owned companies. Source: China Energy Portal The country’s grid is owned and operated primarily by the state-owned State Grid Corporation of China (which supplies power to 88 percent of the country), while China Southern Grid, also state-owned, accounts for most of the remainder. A handful of large state-owned power generation companies are responsible for generating most electricity, including the so-called “big five” – China Datang Corporation, China Guodian Corporation, China Huadian Group, China Huaneng Group, and China Power Investment Corporation – that account for 47 percent of power capacity. In 2016, the 13th Five-Year Plan targeted 2,000 GW of capacity to be installed by The world’s biggest energy 2020 – a nearly 20 percent increase from consumer is aiming for renewables the current capacity – and a 15 percent to account for at least 35 percent increase in the share of non-fossil fuel of electricity consumption by 2030, energy. Based on this five-year plan, according to a revised draft plan China aims to achieve 6.5 percent annual from the National Development & average growth in their GDP from 2016- Reform Commission (NDRC). -

About CR Power

Electric power generation is our business. "We do everything at our best efforts" is the cornerstone of our business philosophy. Our company mission is to become one of the leading independent power producers ("IPP"s) in the world and the best IPP in China. We are committed to accomplishing this mission. About CR Power China Resources Power Holdings Company Limited (the “Company” or “CR Power”) is a fast-growing independent power producer which invests, develops, operates and manages power plants and coal mine projects in the more affluent regions and regions with abundant coal resources in China. As at 31 December 2009, CR Power has 41 power plants in commercial operation. The total attributable operational generation capacity of the power plants held by the Company is 17,753 MW, with 37% located in Eastern China, 22% located in Southern China, 20% located in Central China, 12% located in Northern China, and 9% located in Northeastern China. Corporate Structure China Resources (Holdings) Company Limited 64.59% China Resources Power Holdings Company Limited Coal-fired Coal-fired Coal-fired Clean Energy (≥600MW) (300MW) (≤200MW) • Changshu • Huaxin • Yixing • Danan Wind • Fuyang • Liyujiang A • Xingning • Shantou Wind • Liyujiang B • Cangzhou • Tangshan • Penglai Wind • Shouyangshan • Dengfeng • Jiaozuo • Chaonan Wind • Changzhou • Gucheng • Luoyang • Dahao Wind • Shazhou • Hubei • Jinzhou • Huilaixian’an Wind • Zhenjiang • Lianyuan • Shenhai Thermal • Honghe Hydro • Yangzhou No. 2 • Caofeidian • Banqiao • Beijing Thermal • Shaojiao C • -

Solar Is Driving a Global Shift in Electricity Markets

SOLAR IS DRIVING A GLOBAL SHIFT IN ELECTRICITY MARKETS Rapid Cost Deflation and Broad Gains in Scale May 2018 Tim Buckley, Director of Energy Finance Studies, Australasia ([email protected]) and Kashish Shah, Research Associate ([email protected]) Table of Contents Executive Summary ......................................................................................................... 2 1. World’s Largest Operational Utility-Scale Solar Projects ........................................... 4 1.1 World’s Largest Utility-Scale Solar Projects Under Construction ............................ 8 1.2 India’s Largest Utility-Scale Solar Projects Under Development .......................... 13 2. World’s Largest Concentrated Solar Power Projects ............................................... 18 3. Floating Solar Projects ................................................................................................ 23 4. Rooftop Solar Projects ................................................................................................ 27 5. Solar PV With Storage ................................................................................................. 31 6. Corporate PPAs .......................................................................................................... 39 7. Top Renewable Energy Utilities ................................................................................. 44 8. Top Solar Module Manufacturers .............................................................................. 49 Conclusion ..................................................................................................................... -

China's Belt and Road Initiative in the Global Trade, Investment and Finance Landscape

China's Belt and Road Initiative in the Global Trade, Investment and Finance Landscape │ 3 China’s Belt and Road Initiative in the global trade, investment and finance landscape China's Belt and Road Initiative (BRI) development strategy aims to build connectivity and co-operation across six main economic corridors encompassing China and: Mongolia and Russia; Eurasian countries; Central and West Asia; Pakistan; other countries of the Indian sub-continent; and Indochina. Asia needs USD 26 trillion in infrastructure investment to 2030 (Asian Development Bank, 2017), and China can certainly help to provide some of this. Its investments, by building infrastructure, have positive impacts on countries involved. Mutual benefit is a feature of the BRI which will also help to develop markets for China’s products in the long term and to alleviate industrial excess capacity in the short term. The BRI prioritises hardware (infrastructure) and funding first. This report explores and quantifies parts of the BRI strategy, the impact on other BRI-participating economies and some of the implications for OECD countries. It reproduces Chapter 2 from the 2018 edition of the OECD Business and Financial Outlook. 1. Introduction The world has a large infrastructure gap constraining trade, openness and future prosperity. Multilateral development banks (MDBs) are working hard to help close this gap. Most recently China has commenced a major global effort to bolster this trend, a plan known as the Belt and Road Initiative (BRI). China and economies that have signed co-operation agreements with China on the BRI (henceforth BRI-participating economies1) have been rising as a share of the world economy. -

Roshan Power (Private) Limited

..t ROSHAN POWER (PRIVATE) LIMITED The Registrar, Date: February 10, 2014 National Electric Power Regulatory Authority, Ref: RPL/14/I/003 2nd Floor, OPF Building, SeCtor G-5/2, Reg. 50/2010 Islamabad. Dear Sir, APPLICATION FOR A GENERATION LICENSE OF 10 MW SOLAR POWER PROJECT ROSHAN POWER (PRIVATE) LIMITED 1, Rao Mahmud Ilahi, Director Energy projects being the duly Authorized representative of Roshan Power Pvt. Ltd. by virtue of board resolution dated January 28, 2014, hereby apply to the National Electric Power Regulatory Authority (NEPRA) and for the Grant of a Generation License of 10 MW Solar Power Project to Roshan Power (Pvt.) Ltd pursuant to the section 15 of the Regulation of Generation, Transmission and Distribution of Electric Power Act, 1997. I certify that the documents-in-support attached with this application are prepared and submitted in conformity with the provision of National Electric Power Regulatory Authority Licensing (Application and Modification Procedure) Regulations, 1999, and undertake to abide by the terms and provisions of above-said regulations. I further undertake and confirm that the information provided in the attached documents-in-support is true and correct to the best of my knowledge and belief. Two Bank drafts (DD3050621 & DD3050671) in the sum of Rupees 131,632 (One Hundred Thirty One Thousand, Six Hundred & Thirty Two only) being the non-refundable License application fee calculated in accordance with Schedule-II to National Electric Power Regulatory Authority Licensing (Application and Modification Procedure) Regulations, 1999, is • also attached herewith. Best Regards, - R o M. Ilahi Director Energy Projects u-11 Gurumangat Road, Gulberg-III, Lahore, Pakistan. -

Green Energy Powering Life with China Resources Power Holdings Company Limited Holdings Company Power China Resources Sustainable Development Report 2020

Green Energy Green Powering Life with with Life Powering China Resources Power Holdings Company Limited Holdings Company Power China Resources Sustainable Development Report 2020 China Resources Power Holdings Company Limited SUSTAINABLE DEVELOPMENT REPORT 2020 润电力���限�司 This is the 11th annual Sustainable Development Report published by China Resources Power About Holdings Company Limited (“CR Power”) for the year from January 1 to December 31, 2020. the Report Basis of Preparation Scope This Report is prepared with reference to the This Report relates to China Resources Power following important standards: Holdings Company Limited and its affiliates • Environmental, Social and Governance (see Organizational Structure at page 13), Reporting Guide as set forth in Appendix referred to herein as “We,” “the Company,” 27 of the Rules Governing the Listing of or “CR Power.” Securities on the Stock Exchange of Hong Kong Limited issued by the Stock Exchange We have engaged an independent of Hong Kong Limited (“HKEx” ) third party to provide assurance of 16 • Sustainability Reporting Guidelines of the performance indicators in this Report. Global Reporting Initiative (GRI Standards) See pages 4-5 for the Assurance Report. • Guidelines on Corporate Social Responsibility Reporting for Chinese Enterprises (CASS-CSR4.0) – Basic Framework of the Chinese Academy of Social Sciences • Guidelines on Corporate Social Responsibility Reporting for Chinese Enterprises - Power Production Industry (CASS-CSR3.0) • Guidelines to the State-Owned Enterprises Directly -

An Overview of China's Energy Sector

BOFIT Policy Brief 2021 No. 4 Juuso Kaaresvirta, Eeva Kerola, Riikka Nuutilainen, Seija Parviainen and Laura Solanko How far is China from hitting its climate targets? – An overview of China’s energy sector Bank of Finland Bank of Finland Institute for Emerging Economies (BOFIT) BOFIT Policy Brief Editor-in-Chief Mikko Mäkinen BOFIT Policy Brief 4/2021 16.2.2021 Juuso Kaaresvirta, Eeva Kerola, Riikka Nuutilainen, Seija Parviainen and Laura Solanko How far is China from hitting its climate targets? – An overview of China’s energy sector ISSN 2342-205X (online) Bank of Finland Bank of Finland Institute for Emerging Economies (BOFIT) PO Box 160 FIN-00101 Helsinki Phone: +358 9 183 2268 Email: [email protected] Website: www.bofit.fi/en The opinions expressed in this paper are those of the authors and do not necessarily reflect the views of the Bank of Finland. Kaaresvirta, Kerola, Nuutilainen, Parviainen and Solanko An overview of China’s energy sector Contents Abstract ................................................................................................................................................ 3 1. Introduction ...................................................................................................................................... 4 2. Coal’s persisting dominance in China’s energy mix ....................................................................... 5 3. The world’s largest importer and second largest consumer of crude oil ......................................... 7 4. Despite massive investment, the small -

SINOSING SERVICES PTE. LTD. (A Company Incorporated Under the Laws of Singapore)

NOT FOR DISTRIBUTION IN THE UNITED STATES Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement is for information purposes only and does not constitute an invitation or a solicitation of an offer to acquire, purchase or subscribe for securities or an invitation to enter into an agreement to do any such things, nor is it calculated to invite any offer to acquire, purchase or subscribe for any securities. This announcement is not an offer of securities for sale in the PRC, Hong Kong and the United States or elsewhere. The Bonds are not available for general subscription in Hong Kong or elsewhere. This announcement is not for distribution, directly or indirectly, in or into the United States (including its territories and possessions, any state of the United States and the District of Columbia). This announcement does not constitute or form a part of an offer to sell or the solicitation of an offer to buy any securities in the United States or any other jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The securities referred to herein have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”) and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the Securities Act.