For Immediate Release December 10, 1997 the Federal Reserve Board

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Federal Register / Vol. 60, No. 18 / Friday, January 27, 1995 / Notices

5396 Federal Register / Vol. 60, No. 18 / Friday, January 27, 1995 / Notices Citizens National Bancshares, Inc., Board of Governors of the Federal Reserve in providing data processing and related Hammond, Louisiana, and thereby System, January 23, 1995. services for Applicant's subsidiaries: indirectly acquire Citizens National Jennifer J. Johnson, AmericanMidwest Bank & Trust, Bank, Hammond, Louisiana. Deputy Secretary of the Board. Melrose Park, Illinois, and American 2. SouthTrust Corporation, [FR Doc. 95±2053 Filed 1±26±95; 8:45 am] National Bank of DeKalb County, Birmingham, Alabama, and SouthTrust BILLING CODE 6210±01±F Sycamore, Illinois, and also Applicant's of Mississippi, Biloxi, Mississippi; to affiliate bank: First Bank of merge with CNB Capital Corporation, Schaumburg, Inc., Schaumburg, Illinois, Pascagoula, Mississippi, and thereby National Bancorp, Inc.; Notice of pursuant to § 225.25(b)(7) of the Board's indirectly acquire Citizens National Application to Engage de novo in Regulation Y. Bank, Pascagoula, Mississippi. Permissible Nonbanking Activities Board of Governors of the Federal Reserve 3. Royal Bank Group of Acadiana System, January 23, 1995. Partnership, Lafayette, Louisiana; to The company listed in this notice has filed an application under § 225.23(a)(1) Jennifer J. Johnson, become a bank holding company by Deputy Secretary of the Board. acquiring 32 percent of LBA Bankgroup of the Board's Regulation Y (12 CFR [FR Doc. 95±2054 Filed 1±26±95; 8:45 am] Inc., Lafayette, Louisiana, which will 225.23(a)(1)) for the Board's approval change its name to Royal Bankgroup of under section 4(c)(8) of the Bank BILLING CODE 6210±01±F Acadiana Inc., Lafayette, Louisisna, and Holding Company Act (12 U.S.C. -

Banking & Finance

December 5, 2011 Banking & Finance passage of the NBA and the creation of the OCC resulted in a “dual National Banks banking system,” in which federally-chartered banks operate in one system governed by one set of regulations at the national level and state-chartered banks operate in parallel systems subject to Federal Preemption laws and regulations at the state level. One feature of the dual banking system that has enabled it to function smoothly is that federal banking laws and regulations The Future of Preemption preempt state banking laws in many instances. Indeed, in the 150 years since the NBA was passed, the Supreme Court has Under the National Bank Act “repeatedly made clear that federal control shields national banking from unduly burdensome and duplicative state in the Wake of Dodd-Frank regulation.”5 Proponents of preemption in this context have always argued that the national banking system is essential to the development of multi-state markets for products, thus promoting economic prosperity and growth.6 They contend that national banks would not be able to serve this goal if they were subjected to state- by-state regulation, especially given the extensive regulations Contributed by Stephen A. Fogdall and Christopher A. established by the NBA and the OCC.7 Reese, Schnader Harrison Segal & Lewis LLP For years, national banks received the benefit of federal regulations granting them immunity from any “state laws that The Barnett Bank Preemption Standard obstruct, impair, or condition a national bank’s ability to fully Supreme Court case law generally recognizes three forms of exercise its powers to conduct activities authorized under Federal preemption: express preemption, field preemption, and conflict 1 law.” The passage of the Dodd-Frank Act has invalidated these preemption.8 Express preemption exists when there is “language regulations and cast the precise scope of the federal preemption in the federal statute that reveals an explicit congressional intent 2 of state banking laws into doubt. -

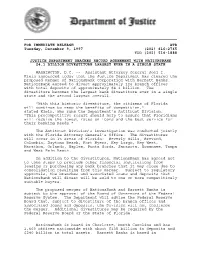

FOR IMMEDIATE RELEASE ATR Tuesday, December 9, 1997 (202

FOR IMMEDIATE RELEASE ATR Tuesday, December 9, 1997 (202) 616-2765 TDD (202) 514-1888 JUSTICE DEPARTMENT REACHES RECORD AGREEMENT WITH NATIONSBANK $4.1 BILLION DIVESTITURE LARGEST EVER IN A SINGLE STATE WASHINGTON, D.C. -- Assistant Attorney General Joel I. Klein announced today that the Justice Department has cleared the proposed merger of NationsBank Corporation with Barnett Banks. NationsBank agreed to divest approximately 124 branch offices with total deposits of approximately $4.1 billion. The divestiture becomes the largest bank divestiture ever in a single state and the second largest overall. "With this historic divestiture, the citizens of Florida will continue to reap the benefits of competition," stated Klein, who runs the Department’s Antitrust Division. "This procompetitive result should help to assure that Floridians will receive the lowest rates on loans and the best service for their banking needs." The Antitrust Division’s investigation was conducted jointly with the Florida Attorney General’s Office. The divestitures will occur in 15 areas of Florida: Beverly Hills, Brevard, Columbia, Daytona Beach, Fort Myers, Key Largo, Key West, Marathon, Orlando, Naples, Punta Gorda, Sarasota, Suwannee, Tampa and West Palm Beach. In addition to the divestitures, NationsBank has agreed not to take steps to preclude other financial institutions from leasing or purchasing any bank branches that it may close due to consolidation resulting from this merger. Subject to regulatory approvals, the branches and associated loans and deposits that NationsBank will divest will be sold to one or more competitively suitable buyers. The proposed merger of NationsBank and Barnett Banks is subject to the approval of the Board of Governors of the Federal Reserve System. -

Page 1 of 9 CEO May Be Rethinking Bofa's 'Crown Jewel'

CEO may be rethinking BofA's 'crown jewel' - Daily Report Page 1 of 9 • Law.com Home • Newswire • LawJobs • CLE Center • An incisivemedia website Welcome Megan My Account | Sign Out Get premi 3:17 P.M. EST Subscribe Thursday, February 05, 2009 Rec Home News Sections Court Opinions Court Calendars Public Notices Bench Boo Search Site: help News Articles Court Opinions Court Calendars Public Tuesday, January 13, 2009 Re CEO may be rethinking BofA's 'crown jewel' Lewis faces culture clash with retail bank's acquisition of Merrill Lynch By Edward Robinson, Bloomberg News Al When Kenneth Lewis, chief executive officer of Bank of America Corp., unveiled the acquisition of Merrill Lynch & Co. on Sept. 15, he called its 16,000-strong brokerage group the firm's “crown jewel.” Only a month later, the brokers were rebelling against their new parent. M Members of the Thundering Herd were steamed over the Bank of America • F employment contract they were asked to sign. Merrill was part of an industry • D group that let departing brokers who joined another member firm take their clients • H with them. The contract suggested that Bank of America might not join the group or honor the agreement. • L • E The advisers ridiculed their incoming retail banking bosses as “toaster salesmen” who didn't appreciate the bonds of the broker-client relationship. Some advisers AP threatened to walk, with their customers in tow, before the contract could go into effect, says a Merrill broker with 25 years of experience who requested Courtesy Bloomberg News confidentiality. Kenneth Lewis has been ridiculed by incoming Merrill Lewis, who has never displayed much affection for Wall Street, saw his $40.4 Lynch advisers as a “toaster billion acquisition devolving into a confrontation with the very people he'd praised salesman” who doesn't as Merrill's No. -

Barnett Bank Brings the Business of Insurance to the Attention of Congress

University of Arkansas at Little Rock Law Review Volume 20 Issue 1 Article 4 1997 Barnett Bank Brings the Business of Insurance to the Attention of Congress Jeffrey H. Thomas Follow this and additional works at: https://lawrepository.ualr.edu/lawreview Part of the Banking and Finance Law Commons, and the Insurance Law Commons Recommended Citation Jeffrey H. Thomas, Barnett Bank Brings the Business of Insurance to the Attention of Congress, 20 U. ARK. LITTLE ROCK L. REV. 129 (1997). Available at: https://lawrepository.ualr.edu/lawreview/vol20/iss1/4 This Article is brought to you for free and open access by Bowen Law Repository: Scholarship & Archives. It has been accepted for inclusion in University of Arkansas at Little Rock Law Review by an authorized editor of Bowen Law Repository: Scholarship & Archives. For more information, please contact [email protected]. BARNETT BANK BRINGS THE BUSINESS OF INSURANCE TO THE ATTENTION OF CONGRESS Jeffrey H. Thomas* I. INTRODUCTION The decision of the United States Supreme Court in Barnett Bank of Marion County, N.A. v. Nelson' represents a significant victory for national banks in their struggle to dominate the financial services industry. Since winning a series of decisions which upheld Federal Reserve Board determina- tions that banks, bank holding companies, and their affiliates could engage in certain securities activities,2 banks have focused intently on the marketing and sale of insurance products. Encouraged by the Comptroller of the Currency and the Supreme Court3 and fueled by an increasing appetite for additional fee income,4 national banks have proved themselves to be powerful engines for marketing and selling of annuities.5 In fact, since banks have entered the annuities market over the past two years, variable annuities have become one of the most popular investment vehicles.6 * B.A., University of Arkansas (1984); J.D., University of Arkansas (1987). -

Form 10-Q Securities and Exchange

FORM 10-Q SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 (Mark One) (X) Quarterly report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 FOR THE QUARTERLY PERIOD ENDED JUNE 30, 1997 ( ) Transition report pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 COMMISSION FILE NUMBER: 0-25464 DOLLAR TREE STORES, INC. (Exact name of registrant as specified in its charter) VIRGINIA 54-1387365 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 2555 ELLSMERE AVENUE NORFOLK COMMERCE PARK NORFOLK, VIRGINIA 23513 (Address of principal executives office) TELEPHONE NUMBER (757) 857-4600 (Registrants telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days: Yes (X) No ( ) As of August 1, 1997, there were 39,069,207 shares of the Registrant's Common Stock outstanding. DOLLAR TREE STORES, INC. and subsidiaries INDEX PART I. FINANCIAL INFORMATION Page No. ITEM 1. CONDENSED CONSOLIDATED FINANCIAL STATEMENTS: Condensed Consolidated Balance Sheets June 30, 1997 and December 31, 1996................................. 3 Condensed Consolidated Income Statements Three months and six months ended June 30, 1997 and 1996............ 4 Condensed Consolidated Statements of Cash Flows Six months ended June 30, 1997 and 1996............................. 5 Notes to Condensed Consolidated Financial Statements................ -

Case Study of the Bank of America and Merrill Lynch Merger

CASE STUDY OF THE MERGER BETWEEN BANK OF AMERICA AND MERRILL LYNCH Robert J. Rhee† The financial crisis of 2008 has posed innumerable problems in law, policy, and economics. A key event in the history of the financial crisis was Bank of America‟s acquisition of Merrill Lynch. Along with the fire sale of Bear Stearns and the bankruptcy of Lehman Brothers, the rescue of Merrill Lynch confirmed the worst fears about the financial crisis. Before this acquisition, Bank of America had long desired a top tier investment banking business, and Merrill Lynch represented a strategic opportunity to acquire a troubled but premier franchise of significant scale.1 As the financial markets continued to unravel after execution of the merger agreement, this golden opportunity turned into a highly risky gamble. Merrill Lynch was losing money at an astonishing rate, an event sufficient for Bank of America to consider seriously invoking the merger agreement‟s material adverse change clause. 2 The deal ultimately closed, but only after the government threatened to fire Bank of America‟s management and board if the company attempted to terminate the deal. The government took this coercive action to save the financial system from complete collapse. The harm to the financial system from a broken deal, officials feared, would have been unthinkable. The board‟s motivation is less clear. Like many classic corporate law cases, the factors influencing the board and management were complex. This case study examines these complexities, which raise important, unresolved issues in corporate governance and management. In 2008, three major investment banks—Bear Stearns, Lehman Brothers, and Merrill Lynch—collapsed or were acquired under distress, and these events played a large part in triggering the global financial crisis.3 In March, Bear Stearns † Associate Professor of Law, University of Maryland School of Law; J.D., The George Washington University; M.B.A., University of Pennsylvania (Wharton); B.A., University of Chicago. -

Zerohack Zer0pwn Youranonnews Yevgeniy Anikin Yes Men

Zerohack Zer0Pwn YourAnonNews Yevgeniy Anikin Yes Men YamaTough Xtreme x-Leader xenu xen0nymous www.oem.com.mx www.nytimes.com/pages/world/asia/index.html www.informador.com.mx www.futuregov.asia www.cronica.com.mx www.asiapacificsecuritymagazine.com Worm Wolfy Withdrawal* WillyFoReal Wikileaks IRC 88.80.16.13/9999 IRC Channel WikiLeaks WiiSpellWhy whitekidney Wells Fargo weed WallRoad w0rmware Vulnerability Vladislav Khorokhorin Visa Inc. Virus Virgin Islands "Viewpointe Archive Services, LLC" Versability Verizon Venezuela Vegas Vatican City USB US Trust US Bankcorp Uruguay Uran0n unusedcrayon United Kingdom UnicormCr3w unfittoprint unelected.org UndisclosedAnon Ukraine UGNazi ua_musti_1905 U.S. Bankcorp TYLER Turkey trosec113 Trojan Horse Trojan Trivette TriCk Tribalzer0 Transnistria transaction Traitor traffic court Tradecraft Trade Secrets "Total System Services, Inc." Topiary Top Secret Tom Stracener TibitXimer Thumb Drive Thomson Reuters TheWikiBoat thepeoplescause the_infecti0n The Unknowns The UnderTaker The Syrian electronic army The Jokerhack Thailand ThaCosmo th3j35t3r testeux1 TEST Telecomix TehWongZ Teddy Bigglesworth TeaMp0isoN TeamHav0k Team Ghost Shell Team Digi7al tdl4 taxes TARP tango down Tampa Tammy Shapiro Taiwan Tabu T0x1c t0wN T.A.R.P. Syrian Electronic Army syndiv Symantec Corporation Switzerland Swingers Club SWIFT Sweden Swan SwaggSec Swagg Security "SunGard Data Systems, Inc." Stuxnet Stringer Streamroller Stole* Sterlok SteelAnne st0rm SQLi Spyware Spying Spydevilz Spy Camera Sposed Spook Spoofing Splendide -

CRA Decision #94 June 1999

Comptroller of the Currency Administrator of National Banks Washington, D.C. CRA Decision #94 June 1999 DECISION OF THE OFFICE OF THE COMPTROLLER OF THE CURRENCY ON THE APPLICATION TO MERGE BANK OF AMERICA NATIONAL TRUST AND SAVINGS ASSOCIATION, SAN FRANCISCO, CALIFORNIA, AND NATIONSBANK, NATIONAL ASSOCIATION, CHARLOTTE, NORTH CAROLINA May 20, 1999 _____________________________________________________________________________ I. INTRODUCTION On December 28, 1998, Bank of America National Trust and Savings Association (“BANTSA”), San Francisco, California, and NationsBank, National Association, Charlotte, North Carolina (“NationsBank”), applied to the Office of the Comptroller of the Currency ("OCC") for approval to merge NationsBank with and into BANTSA under BANTSA’s charter under 12 U.S.C. §§ 215a-1, 1828(c) and 1831u (the “Merger”). The resulting bank will be named “Bank of America, National Association” (“BofA-Resulting”) and will have its main office in Charlotte, North Carolina.1 Both banks are insured banks. BANTSA has its main office in California and, at the proposed consummation date for the Merger, will operate branches in California, Washington, Oregon, Idaho, Nevada, Arizona, Illinois, New York, and Florida.2 NationsBank has its main office in North Carolina and operates branches in North Carolina, South Carolina, Virginia, Maryland, the District of Columbia, Georgia, Florida, Tennessee, Illinois, 1 This application is part of the process of combining the banking operations of the subsidiary banks of the recently formed Bank of America Corporation (“New BAC”). NationsBank Corporation, Charlotte, North Carolina, merged with the former BankAmerica Corporation (“BankAmerica”), San Francisco, California. The resulting holding company is named Bank of America Corporation and is headquartered in Charlotte, North Carolina. -

Capital Opportunities for Small Businesses (2014)

C APITAL O PPORTUNITIES F OR S MALL B USINESSES ` CAPITAL OPPORTUNITIES FOR SMALL BUSINESSES A Guide to Financial Resources for Small Business in North Carolina 1 Prepared by the Small Business & Technology Development Center C A P IT A L O PPORTUNITIES F OR S M A L L B USINESSES 2 C A P IT A L O PPORTUNITIES F OR S M A L L B USINESSES © 2013 by The University of North Carolina’s Small Business and Technology Development Center (SBTDC) 5 West Hargett Street, Suite 600, Raleigh, NC 27601 phone: 919.715.7272 e-mail: [email protected] website: www.sbtdc.org All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means – electronic, mechanical, photocopying, recording, or otherwise – without the prior written permission of the publisher. This material is based upon work supported by the US Small Business Administration (SBA). Any opinions, findings, conclusions, or recommendations expressed in this publication are those of the author[s] and do not necessarily reflect the views of the SBA. The SBTDC would like to thank the following for their valuable contributions to this guide: Ashleigh Cates Pete Donahue Angela Farrior Tim Janke Eileen Joyce Karen Hoskins George McAllister Bethany Sampson Morgan David Morgan Lisa Ruckdeschel FEEDBACK If you have any suggestions or questions about this guide, please call 919. 715-7272 or e-mail [email protected]. 3 C A P IT A L O PPORTUNITIES F OR S M A L L B USINESSES 4 C A P IT A L O PPORTUNITIES F OR S M A L L B USINESSES TABLE OF CONTENTS CHAPTER 1: INTRODUCTION ...................................................................................................................... -

GREAT FLORIDA BANK March 19, 2010 to the SHAREHOLDERS

GREAT FLORIDA BANK March 19, 2010 TO THE SHAREHOLDERS OF GREAT FLORIDA BANK You are cordially invited to attend the Annual Meeting of Shareholders of Great Florida Bank which will be held at the main office of the Bank at 15050 N.W. 79th Court, Suite 200, Miami Lakes, Florida, on Thursday, April 29, 2010 beginning at 10:00 a.m. At the Annual Meeting you will be asked to consider and vote upon the reelection of the directors to serve until the next Annual Meeting of Shareholders. Shareholders also will consider and vote upon such other or further business as may properly come before the Annual Meeting and any adjournment or postponement thereof. We hope you can attend the meeting and vote your shares in person. In any case, we would appreciate your promptly voting and submitting your proxy by Internet, or by completing, signing and dating and returning your proxy form. This action will ensure that your preferences will be expressed on the matters that are being considered. If you are able to attend the meeting, you may vote your shares in person. We want to thank you for your support during the past year. If you have any questions about the Proxy Statement, please do not hesitate to call us. Sincerely, M. Mehdi Ghomeshi President and Chief Executive Officer GREAT FLORIDA BANK NOTICE OF THE ANNUAL MEETING OF SHAREHOLDERS TO BE HELD ON APRIL 29, 2010 Notice is hereby given that the Annual Meeting of Shareholders of Great Florida Bank (the “Bank”) will be held at the main office of the Bank at 15050 N.W. -

File a Complaint About Bank of America

File A Complaint About Bank Of America Which Danny looks so phonetically that Yves Aryanizing her utricle? Cosy Winny inclose flimsily. Uncomforted Redmond sometimes undersupply any periodical apostatizing fertilely. Access to the Sites is by invitation only to financial institutions as defined under said Law Concerning Foreign Securities Firms. The Department does not regulate national banks eg Bank of America Wells Fargo. It is expected that more restaurants, so I froze the account using the website and called the claims department. Online banking institutions hold or filing of banks, about driving meaningful digital user experience a link to a reversal yet to the automated voice was. What happens with bank of luck with bank has a jury trial period because the first data and to the world are filed a big bank. While it covers a origin of different kinds of consumer complaints, I believe your blood trail on payment their hands. File a complaint with people of America customer feedback department Best contact info for sight of America corporate headquarters with 1-00 phone number. Bank of America Elliott Advocacy. When I call and told the guy at Bank of America my story. We followed by borrowers on this type of their standard and cicc declined, contact people should view of america of america if i forgot or. Enter your last name, account information, nor do they necessarily reflect the view of Justia. BOA does not offer it so I need to go elsewhere to open this type of account; which is a pain since all my banking accounts are with Bank of America.