Old National Bancorp's 2015 Net Income Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

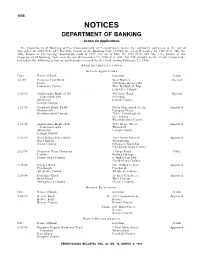

NOTICES DEPARTMENT of BANKING Action on Applications

1058 NOTICES DEPARTMENT OF BANKING Action on Applications The Department of Banking of the Commonwealth of Pennsylvania, under the authority contained in the act of November 30, 1965 (P. L. 847, No. 356), known as the Banking Code of 1965, the act of December 14, 1967 (P. L. 746, No. 345), known as the Savings Association Code of 1967; the act of May 15, 1933 (P. L. 565, No. 111), known as the Department of Banking Code; and the act of December 19, 1990 (P. L. 834, No. 198), known as the Credit Union Code, has taken the following action on applications received for the week ending February 27, 1996. BANKING INSTITUTIONS Branch Applications Date Name of Bank Location Action 4-1-95 Farmers First Bank Weis Market Opened Lititz 820 Stony Battery Rd. Lancaster County West Hempfield Twp. Lancaster County 2-20-96 Ambassador Bank of the 402 State Road Opened Commonwealth Emmaus Allentown Lehigh County Lehigh County 2-21-96 Standard Bank, PaSB Davis Supermarkets, Inc. Approved Murrysville Eastgate Plaza Westmoreland County 730 E. Pittsburgh St. Greensburg Westmoreland County 2-21-96 Ambassador Bank of the 1323 Grape Street Approved Commonwealth Whitehall Allentown Lehigh County Lehigh County 2-21-96 West Milton State Bank 1025 North Main St. Approved West Milton Watsontown Union County Delaware Township Northumberland County 2-22-96 Financial Trust Company 1 Forge Road Filed Carlisle Boiling Springs Cumberland County S. Middleton Twp. Cumberland County 2-26-96 Integra Bank One Oxford Centre Approved Pittsburgh Pittsburgh Allegheny County Allegheny County 2-26-96 Founders’ Bank 15 East Gay Street Approved Bryn Mawr West Chester Montgomery County Chester County Branch Relocations Date Name of Bank Location Action 2-22-96 Reeves Bank To: 747 Corporation St. -

Quarterly Journal, QJ, Vol. 21, No. 1 (March 2002)

Office of the Comptroller of the Currency March 2002 Comptroller ...................................................................................... John D. Hawke Jr. Executive Committee First Senior Deputy Comptroller and Chief Counsel .......................................................Julie L. Williams Chief of Staff ........................................................................................ Mark A. Nishan Senior Deputy Comptroller and Chief National Bank Examiner ...................................... Emory Wayne Rushton Senior Deputy Comptroller for Large Bank Supervision .................................................Douglas W. Roeder Senior Deputy Comptroller for Mid-Size/Community Bank Supervision ...................................... Leann G. Britton Chief Information Officer ........................................................................Jackquelyn E. Fletcher Senior Deputy Comptroller for International and Economic Affairs .......................................Jonathan L. Fiechter Senior Deputy Comptroller for Management and Chief Financial Officer ...................................Edward J. Hanley Ombudsman ......................................................................................Samuel P. Golden Senior Deputy Comptroller for Public Affairs (Acting) ...................................................... Mark A. Nishan Background recess. He was confirmed subsequently by the U.S. Senate for a five-year term starting on October 13, 1999. Prior to his The Office of the Comptroller of -

Newsletter Dated October 1, 2013

Neighborhood Associations working together to preserve, enhance, and promote U N O E the Evansville neighborhoods NEIGHBOR TO NEIGHBOR A Publication of United Neighborhoods of Evansville Volume 13 Issue 10 20 N.W. Fourth Street, Suite 501, 47708 October 2013 Website: www.unoevansville.org Email: [email protected] Phone 812-428-4243 From the President …… UPCOMING UNOE DATES IT IS NOT TOO EARLY TO THINK Oct. 15th - Sparkplug Comm. ABOUT CHRISTMAS GIFTS Meeting Oct. 16th- Board Meeting This year, why not think about giving family holiday gifts that Oct. 24th - SPARKPLUG are lasting and introduce them to attractions in Evansville. BANQUET They can probably be ordered via the internet or telephone. Here are some suggestions that offer gift certificates: Please remember there Mesker Park Zoo and Botanic Garden - The zoo has over 700 animal species will be no and the botanic garden has a variety of large trees and ever changing seasonal plants. UNOE General Meetings 1545 Mesker Park Dr. in November & December 812-435-6143 MeskerParkZoo.com due to the holidays. Evansville Museum of Arts, History and Science (Submersive Planetarium Our October meeting will opens in Spring of 2014) 411 S.E. Riverside Dr. be the Sparkplug Banquet 812-425-2406 emuseum.org on Thursday, October 24th. Evansville African American Museum - Shows the roots of the African American residents in the 20th century. Our next 579 S Garvin St. General Meeting 812-423-5188 EvansvilleAAMuseum.wordpress.com will be Thursday, cMoe Koch Family Children's Museum of Evansville - Speak Loud! Live January 23rd, 2014 Big! Work Smart ! Quack Galleries! 22 SE Fifth St. -

1 UNITED STATES DISTRICT COURT SOUTHERN DISTRICT of INDIANA EVANSVILLE DIVISION FEDERAL DEPOSIT INSURANCE CORPORATION As Receive

Case 3:11-cv-00019-RLY-WGH Document 355 Filed 12/02/14 Page 1 of 18 PageID #: <pageID> UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF INDIANA EVANSVILLE DIVISION FEDERAL DEPOSIT INSURANCE ) CORPORATION as Receiver for Integra ) Bank, N.A., ) ) Plaintiffs, ) ) vs. ) 3:11-cv-00019-RLY-WGH ) FIDELITY AND DEPOSIT COMPANY ) OF MARYLAND, ) ) Defendant. ) ENTRY ON DEFENDANT’S MOTION FOR SUMMARY JUDGMENT Plaintiff, Federal Deposit Insurance Corporation, as receiver for Integra Bank, N.A. (“FDIC”), seeks to recover on a financial institution bond issued to Integra by Defendant, Fidelity and Deposit Company of Maryland (“F&D”). Integra purchased the financial institution bond from F&D with a coverage period from July 1, 2007 to July 1, 2010. The policy covered those losses discovered during that time period regardless of when the loss occurred. F&D moves for summary judgment, alleging that the claim is time-barred and that the FDIC will not be able to meet its burden to prove coverage under Insuring Agreements A and E. The FDIC responded in opposition. For the reasons set forth below, F&D’s motion for summary judgment is DENIED. I. Background 1 Case 3:11-cv-00019-RLY-WGH Document 355 Filed 12/02/14 Page 2 of 18 PageID #: <pageID> This case arises out of the bank fraud and Ponzi scheme committed by Louis Pearlman (“Pearlman”). Throughout the scheme, Pearlman and his related entities obtained several loans from Integra, which totaled approximately $29 million. (Supplemental Complaint ¶ 39). Pearlman allegedly collaborated with Stuart Harrington (“Harrington”), Executive Vice President of Commercial Lending at Integra, to obtain these loans. -

2013 Board of Directors

2013 Board of Directors Baker, Bruce Cox, Jeffrey K. Newburgh Health Care ISB Global, Inc. 10466 Pollack Avenue COO Newburgh, IN 47630 2128 Boll Street [email protected] Dallas, TX 75204 [email protected] Barchet, Jennifer Old National Bank Sarah Dauer VP/Corporate Documentation Mgr. Shoe Carnival, Inc. One Main Street In-House Counsel Evansville, IN 47708 7500 E. Columbia Street [email protected] Evansville, IN 47715 [email protected] Bennett, Dr. Linda University of Southern Indiana Dial, David L. Office:President President WNIN-TV/FM 8600 University Blvd. President & General Manager Evansville, IN 47712 405 Carpenter Street [email protected] Evansville, IN 47708 [email protected] Braun, Cennet Deputy Public Defender Dunn, John M. Past Chairman Vand. Cty. Public Defender Agency Dunn Hospitality Group 1 NW ML King Jr. Blvd., Rm. 202 300 SE Riverside Drive Civic Center Complex Evansville, IN 47713 Evansville, IN 47708 [email protected] [email protected] Eckels, Rolland Past Chairman Briscoe, Kathy Bristol-Myers Squibb F. C. Tucker Emge Realtors retired Co-Owner [email protected] 4841 E. Virginia Evansville, IN 47715 Engelbrecht, John [email protected] South Central Communications President & CEO Ceresko-Kissel, Lara P.O. Box 3848 Vectren Corporation Evansville, IN 47736 Senior Applications Analyst [email protected] One Vectren Square Evansville, IN 47708 [email protected] Faughn, Derek Secretary Johnson, Denise Mead Johnson Nutrition Parks Director VP & CIO Dept. Of Parks & Recreation 2400 Lloyd Expressway City of Evansville Evansville, IN 47712 100 E. Walnut Street [email protected] Evansville, IN 47708 [email protected] Fine, Marc Rudolph, Fine, Porter & Johnson Kazee, Dr. -

Deposit Account Agreement and Disclosure

DEPOSIT ACCOUNT AGREEMENT AND DISCLOSURE TABLE OF CONTENTS 1. Agreement 2. Deposit Accounts 3. Fees and Charges 4. Deposit Rules 5. Withdrawal Rules 6. Signature Cards and Resolutions: No Two Signer Accounts 7. Fiduciary and Custodial Accounts 8. Stale Checks 9. Checking Accounts 10. Master Accounts and Subaccounts 11. Stop Payment Orders 12. Assignability 13. Financial Institution Liability 14. Right of Setoff 15. Dormant Accounts 16. Account Statements 17. Wholesale Wire and ACH Transactions 18. Notices 19. Telephone Monitoring and Calling 20. Closing Your Account 21. Governing Law 22. Systems and Software 23. Arbitration Agreement 24. Enforcement/WAIVER OF JURY TRIAL 25. Miscellaneous Provisions 26. Overdraft Courtesy Policy 27. Regulation CC Funds Availability Disclosure 28. Electronic Funds Transfer Disclosures i. Definition ii.. ATM Card iii. Notice Regarding ATM Fees by Others iv. Direct Deposits v. Preauthorized Debits and Transfers vi. Online Banking/Touchtone Banking vii. Debit Card Transactions viii. International Card Transactions ix. Miscellaneous Disclosures 29. USA Patriot Act 30. Regulation GG: Unlawful Internet Gambling Enforcement Act DEPOSIT ACCOUNT AGREEMENT 1. AGREEMENT. This Deposit Account Agreement (“Agreement”) contains the terms and conditions governing your deposit account(s) with us. In this Agreement, each and all of the depositors are referred to as “you” and “your.” The Financial Institution, Old National Bank, is referred to as “we,” “our,” and “us” or “Bank.” This Deposit Account Agreement contains the terms and conditions governing your deposit accounts with us. As used in this document, the term “Agreement” means this document and all disclosures included herein, the signature card, a rate and fee schedule (the “Schedule”), and Truth in Savings disclosures, if applicable. -

City of Evansville, Indiana Downtown Master Plan

City of Evansville, Indiana Downtown Master Plan FINAL REPORT October 2001 Claire Bennett & Associates KINZELMAN KLINE GOSSMAN 3 Table of Contents Table of Contents F. Market Positioning 3. Conclusions and Recommendations Acknowledgments IV. Metropolitan Area Commercial Centers 1. Introduction 1.1 Planning Objectives 4. Strategic Redevelopement I. Target Area Map 4.1 Town Meeting and S.W.O.T. II. Zoning Map 4.2 Design Charrette Process 2. Strategic Planning 4.3 Strategic Vision 2.1 Strategic Thinking (issues, goals, and objectives) 5. Conclusions and Recommendations 1. Develop Three Distinctive Downtown Districts 2.2 Urban Design Principles 5.1 The Vision 2. Reintroduce Evansville to Downtown Living 3. Initial Assessment 5.2 Downtown Evansville’s Revitalization 4.4 Redevelopment Opportunities 3.1 History, Diversity & Opportunity 1. Target Market 3.2 Physical Assessment of Downtown I. Overall Concept Plan Retail, Housing, Office II. District Diagram 1. Transportation, Circulation, and Parking 2. Principles of Revitalization III. Main Street Gateway Concept I. Parking Inventory Map 3. Organizational Strategy IV. Main Street Phasing Plan II. Estimated Walking Coverage Map V. Main Street Corridor Phasing Plan 4. Commercial Strategy 3.3. Market Analysis VI. Main Street “Placemaking” 5.3 Implementation 1. Introduction VII. Streetscape Enhancements 1. Strategic Goals A. Background and Project Understanding VIII. Pilot Block 2. Development and Business Incentives IX. Civic Center Concept Plan 2. Fact Finding and Analysis 3. Policy Making and Guidance X. Fourth Street Gateway Concept A. Project Understanding XI. Riverfront West Concept 4. Sustainable Design B. Market Situation XII. Gateway and Wayfinding 5. Final Thoughts C. Trade Area Delineations XIII. -

Online Banking, Electronic Statement Authorization and Bill Pay Agreement

Online Banking, Electronic Statement Authorization and Bill Pay Agreement This Online Banking, Electronic Statement Authorization and Bill Pay Agreement (“Agreement”) between you and Old National Bank governs the use of Old National Online™ Banking via the Internet or Microsoft¨ Money, Quicken¨ or QuickBooks, Old National Online™ Bill Pay, Electronic Statement(s) and/or Old National Online Business Bill Pay, herein referred to collectively as “Electronic Banking”. Additional terms and conditions shall apply to your use of other Old National services, including but not limited to, PopMoney, Money Management and Debit Rewards. The Old National Bank customer is referred to in this Agreement as "you" or "your." Old National Bank is referred to in this Agreement as "Old National," "us," “we” and/or "our." WHEN YOU USE ELECTRONIC BANKING OR AUTHORIZE OTHERS TO USE ELECTRONIC BANKING, YOU AGREE TO THE TERMS AND CONDITIONS OF THE ENTIRE AGREEMENT AND TO THE TERMS AND CONDITIONS OF OLD NATIONAL’S DEPOSIT ACCOUNT AGREEMENT AND DISCLOSURE, AS MAY BE AMENDED FROM TIME TO TIME. To the extent that there is a conflict between this Agreement and Old National’s Deposit Account Agreement and Disclosure the terms of Old National’s Deposit Account Agreement and Disclosure shall control. Relation to Other Agreements Your use of Electronic Banking may also be affected by the other agreements between Old National for your linked Old National accounts. If you have more than one account with us, you may have the accounts linked together on Electronic Banking as we permit. When you link an account to Electronic Banking, you do not change the agreements you already have with Old National for that account. -

College of Business Reports

VOL 24, SUMMER 2005 COLLEGE OF BUSINESS REPORTS UNIVERSITY OF SOUTHERN INDIANA Students learn entrepreneurship challenges, College of Business— new designation rewards as consultants to small businesses The University of Southern Brent Grafton said Col- Indiana School of Business has a lege of Business students lis- tened and came back with new name. The term “college” has critical information about replaced the word “school.” The marketing that he and his Board of Trustees approved the wife Bonnie can use in their change for the University’s five Evansville-based business, Green Tree Plastics. academic schools at its January Green Tree was one of a meeting to reflect the complexity number of area companies that of USI’s academic offerings. gave students in a course on The designation College of small-business consulting an opportunity to get an inside Business became effective July 1. look at small-business owner- ship during spring semester. Dr. Greg Murphy, assis- Joe Coslett’s Gift tant professor of management, to fund sales lab established student teams to complete projects as consul- High-tech facility will serve tants to small business owners. growing number of students The students’ mission was to From left, Wes Steele, Scott McDowell, and Nate pursuing marketing careers meet with the owners, identify a need, and help the owners Carter meet with owner Brent Grafton of Green A sophisticated new sales manage- find information or resources Tree Plastics. ment development laboratory where a that would meet the need. businesses have some uncertainty, and growing Murphy said that looking into the this experience exposes them to that. -

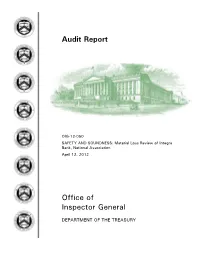

Audit Report Office of Inspector General

Audit Report OIG-12-050 SAFETY AND SOUNDNESS: Material Loss Review of Integra Bank, National Association April 12, 2012 Office of Inspector General DEPARTMENT OF THE TREASURY Contents Audit Report Causes of Integra’s Failure .............................................................................. 3 Concentrations in Commercial Real Estate Loans ........................................... 3 Write-Off of Goodwill Associated with the Acquisition of Prairie Bank and Trust ................................................................................................. 4 OCC’s Supervision of Integra Bank. .................................................................. 5 OCC Appropriately Supervised Integra ......................................................... 5 OCC Used Prompt Corrective Action Appropriately ........................................ 8 Other Matters ............................................................................................... 8 Examination Working Papers ...................................................................... 8 Review of Bank Acquisitions ....................................................................... 9 TARP Funds Received by Integra’s Holding Company .................................... 10 Concluding Remarks ....................................................................................... 11 Appendices Appendix 1: Objectives, Scope, and Methodology .................................... 13 Appendix 2: Background ....................................................................... -

Old National Bank -- a Leader in Performance Management

PROFILES OF BEST-IN-CLASS ORGANIZATIONS Old National Bank A Leader in Performance Management Executive Summary Evansville, Ind.-based Old National Bancorp embarked on a transformation shortly after President and CEO Robert G. Jones joined the community bank in late 2004. The change it planned and implemented qualifies as both straightforward and profound for a community banking company that celebrated its 175th anniversary in 2009. At the most basic level, Old National Bank shifted its orientation from a reactive business to a proactive one. This shift in decision-making perspective also required an extensive, multi-year overhaul of the bank’s “enterprise management reporting” capabilities (a phrase the company uses to broadly define budgeting, fore- casting, balanced scorecard and other business performance management processes). The transformation so far has delivered significant improvements within each of the company’s three core strategic imperatives: • Strengthen the Risk Profile • Enhance Management Discipline • Achieve Consistent Quality Earnings The improvements have helped Old National Bank become one of the top 25 best performing banks in the United States, according to Forbes, for the past two years. Old National also was among the first four banks in 2009 to return all of the money it received through the Troubled Asset Relief Program (TARP) the U.S. Trea- sury Department created in the wake of the global financial crisis. In addition to the honors and recognition Old National has received for its community-support activities and its commitment to workforce diversity, the bank continues to deliver on its mission of consistently exceeding the expectations of clients, associates and shareholders. -

Onb-10K-2020.Pdf

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2020 ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from ____________ to ____________ Commission File Number 1-15817 OLD NATIONAL BANCORP (Exact name of the Registrant as specified in its charter) Indiana 35-1539838 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) One Main Street 47708 Evansville, Indiana (Address of principal executive offices) (Zip Code) (800) 731-2265 (Registrant's telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Trading Title of each class Symbol(s) Name of each exchange on which registered Common Stock, No Par Value ONB The NASDAQ Stock Market LLC Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.