1Q19 Earnings Call Presentation April 17, 2019 Forward Looking Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UBS AG (Incorporated with Limited Liability in Switzerland) Acting Through Its London Branch

3 June 2021 Hong Kong Exchanges and Clearing Limited (“HKEX”), The Stock Exchange of Hong Kong Limited (the “Stock Exchange”) and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. This document, for which we accept full responsibility, includes particulars given in compliance with the Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong Limited (the “Rules”) for the purpose of giving information with regard to us. We, having made all reasonable enquiries, confirm that to the best of our knowledge and belief the information contained in this document is accurate and complete in all material respects and not misleading or deceptive, and there are no other matters the omission of which would make any statement herein or this document misleading. This document is for information purposes only and does not constitute an invitation or offer to acquire, purchase or subscribe for the Warrants. The Warrants are complex products. Investors should exercise caution in relation to them. Investors are warned that the price of the Warrants may fall in value as rapidly as it may rise and holders may sustain a total loss of their investment. Prospective purchasers should therefore ensure that they understand the nature of the Warrants and carefully study the risk factors set out in the Base Listing Document (as defined below) and this document and, where necessary, seek professional advice, before they invest in the Warrants. -

ST/LIFE/PAGE<LIF-005>

| FRIDAY, APRIL 6, 2018 | THE STRAITS TIMES | happenings life D5 GIGS Anjali Raguraman recommends Dua Lipa Live In Singapore After a year of No. 1 hits, sold-out Picks SINGAPORE INTERNATIONAL shows and record-breaking JAZZ FESTIVAL streaming figures, Dua Lipa also The fifth edition of annual jazz ended 2017 as the most-streamed festival Sing Jazz returns with a Gigs British female artist on Spotify. Her star-studded line-up that includes smash hit single, New Rules, made her soul and hip-hop great Lauryn Hill the first female artist to have a British (right), jazz-pop proponent Jamie No. 1 hit since Adele in 2015. Cullum and Grammy Award winner WHERE: The Star Theatre, 04-01 The Lalah Hathaway. Star Performing Arts Centre, 1 Vista Dance music lovers will also have Exchange Green MRT: Buona Vista their fill of legends with DJs Sasha WHEN: May 4, 8pm ADMISSION: $88 - and Ferry Corsten taking the stage $168, tickets from apactix.com tonight at the after-party event, INFO: dualipa.com/live The Late Show. Home-grown singer-songwriter Tim De Cotta Margaret Cho opens for British musical group Soul II Fresh Off The Bloat Soul, who are performing in Singapore LA Comedy Live is bringing back for the first time. five-time Grammy- and Emmy- This year, there is also a Festival nominated comedian Margaret Cho Village at the event square at the with her new show. She continues to Marina Bay waterfront, where local tackle difficult subjects with and regional bands will put on free sensitivity, offering razor-sharp performances. -

Press-Release-On-Irs.Pdf

PRESS RELEASE Integrated Resorts to invest S$9 billion in new world-class attractions and experiences In view of the significant investments, exclusivity period for the two IRs extended to end-2030 Casino entry levy prices to increase by 50% Gaming tax rates to increase 1. The two Integrated Resorts (IRs) have committed around S$9 billion in non-gaming investments to build new world-class tourism and MICE facilities and attractions, many of which will be first-in-Singapore. The IRs’ investments will enhance the vibrancy and tourism appeal of their offerings to remain competitive with other destinations in the region, and bring in more than half a million additional visitors annually. Singaporeans can look forward to more lifestyle and entertainment options. The IR expansions will create up to 5,000 new jobs directly and benefit local businesses, including small and medium enterprises. IRs’ Expansion of Non-Gaming Facilities 2. Marina Bay Sands (MBS) will add to the Singapore skyline by constructing an iconic, new fourth tower adjacent to its existing three towers. The centrepiece of the expansion is a 15,000-seater state-of-the-art entertainment arena, which will host a mix of A-list artistes and events arising from MBS’ proposed collaboration with leading entertainment content providers. The expansion will also include a luxury all-suite hotel with approximately 1,000 rooms, topped with a sky roof. There will be additional MICE space for hosting world-class exhibitions and conventions. 3. Resorts World Sentosa (RWS) will expand Universal Studios Singapore with two new immersive environments – Minion Park and Super Nintendo World. -

Must Visit Attractions in Singapore"

"Must Visit Attractions in Singapore" Created by: Cityseeker 16 Locations Bookmarked Merlion Park "Singapore's National Emblem" Standing guard at the mouth of the Singapore River is the Merlion, a mythical beast that is a cross between a fish and a lion. The fish symbolizes Singapore's close association with the sea while the lion head refers to the legendary sighting of a lion during the discovery of ancient Singapore. Created in 1972 as a tourism icon, the Merlion is especially by Graham-H attractive in the evenings when it is illuminated and spouts water from its mouth. Today, it has moved 120 meters (393 feet) away from its original spot, adjacent to One Fullerton. A stroll through Merlion Park yields great views of Singapore's colonial district. +65 6736 6622 1 Fullerton Road, Singapore Marina Bay Sands Skypark "Experience Singapore from New Heights" A true marvel of engineering designed by the famous architect Moshe Safdie, the Marina Bay Sands Skypark is an open-air viewing deck perched 200 meters (656.168 feet) atop the Marina Bay Sands Hotel. This deck, shaped like a ship, almost seems to go against the law of gravity as it stretches on the 57th story above the hotel tower. The panoramic views by Sarah_Ackerman from of Singapore are staggering, and on a clear day, far-off islands belonging New York, USA. to Malaysia and Indonesia can be seen. The Skypark is the size of three football fields and also contains lush tropical gardens, souvenir stands and gourmet restaurants. Its main attraction is a spectacular infinity pool that seems as if it meets thin air at one of its longer edges. -

Participating Merchants Address Postal Code

Participating Merchants Address Postal Code Club21 3.1 Phillip Lim 581 Orchard Road, Hilton Hotel 238883 A|X Armani Exchange 2 Orchard Turn, B1-03 ION Orchard 238801 391 Orchard Road, #B1-03/04 Ngee Ann City 238872 290 Orchard Rd, 02-13/14-16 Paragon #02-17/19 238859 2 Bayfront Avenue, B2-15/16/16A The Shoppes at Marina Bay 018972 Sands Armani Junior 2 Bayfront Avenue, B1-62 018972 Bao Bao Issey Miyake 2 Orchard Turn, ION Orchard #03-24 238801 Bonpoint 583 Orchard Road, #02-11/12/13 Forum The Shopping Mall 238884 2 Bayfront Avenue, B1-61 018972 CK Calvin Klein 2 Orchard Turn, 03-09 ION Orchard 238801 290 Orchard Road, 02-33/34 Paragon 238859 2 Bayfront Avenue, 01-17A 018972 Club21 581 Orchard Road, Hilton Hotel 238883 Club21 Men 581 Orchard Road, Hilton Hotel 238883 Club21 X Play Comme 2 Bayfront Avenue, #B1-68 The Shoppes At Marina Bay Sands 018972 Des Garscons 2 Orchard Turn, #03-10 ION Orchard 238801 Commes des Garcons 581 Orchard Road, Hilton Hotel 238883 DKNY 290 Orchard Rd, 02-43 Paragon 238859 2 Orchard Turn, B1-03 ION Orchard 238801 Dries Van Noten 581 Orchard Road, Hilton Hotel 238883 Emporio Armani 290 Orchard Road, 01-23/24 Paragon 238859 2 Bayfront Avenue, 01-16 The Shoppes at Marina Bay Sands 018972 Giorgio Armani 2 Bayfront Avenue, B1-76/77 The Shoppes at Marina Bay Sands 018972 581 Orchard Road, Hilton Hotel 238883 Issey Miyake 581 Orchard Road, Hilton Hotel 238883 Marni 581 Orchard Road, Hilton Hotel 238883 Mulberry 2 Bayfront Avenue, 01-41/42 018972 581 Orchard Road, Hilton Hotel 238883 Outlet by Club 21 2 Jurong East -

The Londoner Hotel − “Discover the Londoner Macao” Terms and Conditions 1. This Offer Is Subject to Availability. 2. All R

The Londoner Hotel − “Discover The Londoner Macao” Terms and Conditions 1. This offer is subject to availability. 2. All rates are based on Single and/or Double occupancy. 3. Offer includes The Residence access offering breakfast buffet, afternoon tea and selected evening cocktails. 4. All cancellations or amendments must be made 48 hours before arrival. A charge equivalent to the Package first night price plus service charge will be imposed as late cancellation charge from credit card on file. 5. All reservation is required to guarantee by deposit or credit card during Chinese New Year (11-17 Feb, 2021), Ching Ming Festival and Easter Holiday (02-05 Apr, 2021), Labor Day (01 - 05 May, 2021), Tung Ng Festival (12-14 Jun, 2021), Mid-Autumn Festival (18-21 Sep, 2021), Chinese National Day (01-07 Oct, 2021), Christmas (24-26 Dec, 2021) and New Year’s Eve (31 Dec, 2021), no cancellation and amendment is allowed 72 hours prior to the arrival date. The deposit of the entire stay, tax, and service charge will be imposed 72 hours prior to arrival. A charge equivalent to the total room rental price plus service charge and government tax will be imposed once No- Show. 6. The Londoner Hotel and Venetian Orient Limited reserves the right to release the rooms for resale without prior notice if the credit card is invalid. 7. At least one occupant of the room must be 18 years old or above. 8. Rates are in HKD/MOP and subject to 10% service charge and 5% Government Tax. 9. Rates are based upon your length of stay. -

Proposed Re-Election of Retiring Directors and Proposed Granting of General Mandates to Repurchase Shares and to Issue New Shares and Notice of Annual General Meeting

475754 \ (Sands) \ 23/03/2018 \ M51 P.1 THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to any aspect of this circular or as to the action to be taken, you should consult a stockbroker or other registered dealer in securities, a bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Sands China Ltd., you should at once hand this circular, together with the enclosed form of proxy, to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. SANDS CHINA LTD. 金沙中國有限公司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 1928) PROPOSED RE-ELECTION OF RETIRING DIRECTORS AND PROPOSED GRANTING OF GENERAL MANDATES TO REPURCHASE SHARES AND TO ISSUE NEW SHARES AND NOTICE OF ANNUAL GENERAL MEETING A notice convening the Annual General Meeting of Sands China Ltd. to be held at The Venetian Macao-Resort-Hotel, Florence 2201 to 2302, Level 1, Estrada da Baia de N. Senhora da Esperanca, s/n, Taipa, Macao on Friday, May 25, 2018, at 11:00 a.m. -

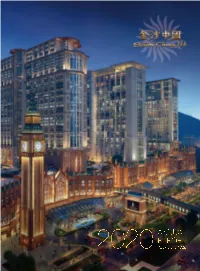

2020 Annual Report

Stock Code: 1928 and Note Stock Codes: 5140, 5141, 5142, 5725, 5727, 5733, 40246, 40247, 40584, 40585 www.sandschina.com From Luxury Duty Free Shopping, Exciting Entertainment and Fabulous Dining to World-Class Hotel Suites and MICE, Come and Discover Everything at Sands China. SANDS CHINA LTD. CONTENTS 1. OVERVIEW 4 1.1 Financial Results Summary 4 1.2 Highlights of 2020 5 1.3 Directors and Senior Management 11 2. BUSINESS REVIEW 18 2.1 Chairman’s Statement 18 2.2 Business Overview and Outlook 20 2.3 Our Properties 26 2.4 Management Discussion and Analysis 33 2.5 Priority Risk Factors 47 2.6 Stakeholder Information 59 3. CORPORATE GOVERNANCE 66 REPORT 3.1 Introduction 66 3.2 Corporate Governance Code Compliance 66 3.3 Board Governance Structure 67 3.4 The Board 68 3.5 Audit Committee 74 3.6 Remuneration Committee 76 3.7 Nomination Committee 78 3.8 Capex Committee 81 3.9 Risk Management and Internal Control 82 3.10 Shareholders 87 3.11 Compliance Disclosures and Other Matters 90 3.12 Directors’ Report 92 4. FINANCIAL STATEMENTS 113 4.1 Independent Auditor’s Report 113 4.2 Financial Statements 117 4.3 Notes to the Consolidated Financial Statements 123 4.4 Financial Summary 193 5. CORPORATE INFORMATION 194 6. CONTACT US 195 7. GLOSSARY 196 In case of any inconsistency between the English version and the Chinese version of this Annual Report, the English version shall prevail. SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS 2 ANNUAL REPORT 2020 SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS our Luxurious Hotel Rooms and Suites await you. -

Press Release Enjoy Spectacular Dragon Dances with a Twist, Fortune Animal Trail and More at Universal Studios Singapore and S.E.A

press release Enjoy Spectacular Dragon Dances with a Twist, Fortune Animal Trail and More at Universal Studios Singapore and S.E.A. Aquarium this Lunar New Year Universal Studios Singapore presents the all-new Fu Fighters show and Majestic Dragon Trail featuring favourite characters from all seven zones in the theme park S.E.A. Aquarium’s annual Gong SEA Fa Cai returns with iconic underwater dragon dance, Trail of Fortunes and new educational shark exhibition This February, Universal Studios Singapore will ring in the Lunar New Year with all-new performances and favourite characters dressed in their festive best while S.E.A. Aquarium’s annual Gong SEA Fa Cai celebration returns with its iconic underwater dragon dance performance and other festivities. PHOTO CREDITS: RESORTS WORLD SENTOSA. SINGAPORE, 26 January 2018 – From an all-new dragon dance procession featuring favourite movie characters to Singapore’s only underwater dragon dance performance amongst marine animals, guests heading to Universal Studios Singapore and S.E.A. Aquarium at Resorts World Sentosa are in for a treat as both attractions unveil festive offerings to ring in the Lunar New Year. From 9 to 28 February, guests can immerse in Chinese traditional performances with a twist, educational trails and more as Universal Studios Singapore and S.E.A. Aquarium celebrate the Year of the Dog with fun-filled festivities for the whole family. The attractions will sparkle in customary red and gold overlays, traditional lanterns hanging overhead and streetlamps festooned with auspicious Chinese characters to usher in good luck, prosperity and health. Universal Studios Singapore (9 to 25 February) NEW! Majestic Dragon Trail Trailblazing this year’s celebratory event at Universal Studios Singapore is the all-new Majestic Dragon Trail, a reimagined spectacle based on the traditional dragon dance. -

Morning Tour: Duck Tour and Marina Bay Sands

Morning Tour: Duck Tour and Marina Bay Sands 0930am Meet up at Suntec City Convention Centre (#01-330) Climb aboard a refurbished amphibious vehicle from Vietnam War for a unique tour of Singapore. Depart from Suntec City, and start your land and water adventure with a big splash into the Marina Bay Cruise along Marina Bay, where you can admire views of the bustling urban city's skyline and marvel at Singapore's most iconic landmark—the Marina Bay Sands, Gardens by the Bay, the Esplanade Theatre and the towering Merlion. Your journey continues as you waddle back onto land and drive past the Singapore Flyer and into the Civic District. There you’ll see the steps of the Old Supreme Court where the British surrendered to the Imperial Japanese army during WWII, and the War Memorial Park, a tribute to those who gave their lives during WWII's Japanese occupation. End the tour with a loop around the world’s largest water fountain at Suntec City, named the Fountain of Wealth, for good luck! CODE: SRV4-DUCKMBS Page 1 Marina Bay Sands Known as ‘The Singapore River Experience—A Tale of Two Quays’, this unforgettable ride encapsulates Singapore heritage and modernity in one activity, spanning the iconic districts of Clarke Quay, Boat Quay and Marina Bay. Bask in the rich history of the Raffles Landing site, marvel at the soaring futuristic architecture of Marina Bay Sands®, and discover the story of the river that gave life to our city. 12pm Lunch @ Spago Dining Room at L57, Sands SkyPark $168/pax Professional Tour Guide services (English or Chinese Speaking) Admission ticket (Due to Covid 19 , Subject to availability upon confirmation) Activities as per program stated Quotation based on minimum 5 pax CODE: SRV4-DUCKMBS Page 2 . -

FULLERTON HOTEL SHUTTLE Bus Time Schedule & Line Route

FULLERTON HOTEL SHUTTLE bus time schedule & line map Fullerton Hotel → Orchard Rd/Shenton Way View In Website Mode The FULLERTON HOTEL SHUTTLE bus line (Fullerton Hotel → Orchard Rd/Shenton Way) has 2 routes. For regular weekdays, their operation hours are: (1) Business Shuttle: 7:30 AM - 9:30 AM (2) Shopping Shuttle: 11:00 AM - 8:00 PM Use the Moovit App to ƒnd the closest FULLERTON HOTEL SHUTTLE bus station near you and ƒnd out when is the next FULLERTON HOTEL SHUTTLE bus arriving. Direction: Business Shuttle FULLERTON HOTEL SHUTTLE bus Time Schedule 11 stops Business Shuttle Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 7:30 AM - 9:30 AM Fullerton Hotel 1 Fullerton Square, Singapore Tuesday 7:30 AM - 9:30 AM Capital Square Wednesday 7:30 AM - 9:30 AM 3 Church Street, Singapore Thursday 7:30 AM - 9:30 AM Hong Leong Building Friday 7:30 AM - 9:30 AM 16 Ra«es Quay, Singapore Saturday Not Operational Marina Bay Financial Centre Tower 1 8 Marina Boulevard, Singapore Asia Square Tower 1 Marina View, Singapore FULLERTON HOTEL SHUTTLE bus Info Direction: Business Shuttle Capital Tower Stops: 11 01-08/09/10, 168 Robinson Road Trip Duration: 18 min Line Summary: Fullerton Hotel, Capital Square, Hong Temasek Blvd - Suntec Convention Ctr (02151) Leong Building, Marina Bay Financial Centre Tower 1, 9 Ra«es Boulevard, Singapore Asia Square Tower 1, Capital Tower, Temasek Blvd - Suntec Convention Ctr (02151), Suntec Tower Five Suntec Tower Five (Pick-Up/Drop-Off Point) (Pick-Up/Drop-Off Point), Millenia Tower (Lobby), 02- 401/402, -

Campaign Fact Book Former Whitechapel Bell Foundry Site Whitechapel, London

Campaign Fact Book Former Whitechapel Bell Foundry Site Whitechapel, London Compiled January 2020 Whitechapel Bell Foundry: a matter of national importance This fact book has been compiled to capture the breadth of the campaign to save the site of the Whitechapel Bell Foundry, which is currently threatened by a proposal for conversion into a boutique hotel. Re-Form Heritage; Factum Foundation; numerous community, heritage and bellringing organisations; and thousands of individuals have contributed to and driven this campaign, which is working to: reinstate modern and sustainable foundry activity on the site preserve and record heritage skills integrate new technologies with traditional foundry techniques maintain and build pride in Whitechapel’s bell founding heritage The site of the Whitechapel Bell Foundry is Britain’s oldest single-purpose industrial building where for generations bells such as Big Ben, the Liberty Bell, Bow Bells and many of the world’s great bells were made. Bells made in Whitechapel have become the voices of nations, marking the world’s celebrations and sorrows and representing principles of emancipation, freedom of expression and justice. As such these buildings and the uses that have for centuries gone on within them represent some of the most important intangible cultural heritage and are therefore of international significance. Once the use of the site as a foundry has gone it has gone forever. The potential impact of this loss has led to considerable concern and opposition being expressed on an unprecedented scale within the local area, nationally and, indeed, internationally. People from across the local community, London and the world have voiced their strong opposition to the developer’s plans and to the hotel use and wish for the foundry use to be retained.