Robinhood Customer Agreement (June 22)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RHF Use and Risk Disclosures

RHF Use and Risk Disclosures IT IS IMPORTANT THAT YOU READ AND FULLY UNDERSTAND THE FOLLOWING RISKS OF TRADING AND INVESTING IN YOUR SELF-DIRECTED ROBINHOOD FINANCIAL ACCOUNT. Use of Self-Directed Trading Accounts. All Customer Accounts are self-directed. Accordingly, unless Robinhood Financial clearly identifies a communication as an individualized recommendation, Customers are solely responsible for any and all orders placed in their Accounts and understand that all orders entered by them are based on their own investment decisions or the investment decisions of their duly authorized representative or agent. Consequently, any Customer of Robinhood Financial agrees that, unless otherwise agreed to in writing, neither Robinhood Financial nor any of its employees, agents, principals or representatives: ● provide investment advice in connection with a Customer Account; ● recommend any security, transaction or order; ● solicit orders; ● act as a market maker in any security; ● make discretionary trades; and ● produce or provide research. To the extent research materials or similar information is available through Robinhood.com or the websites of any of its affiliates, these materials are intended for informational and educational purposes only and they do not constitute a recommendation to enter into any securities transactions or to engage in any investment strategies. General Risks of Trading and Investing. All securities trading, whether in stocks, exchange-traded funds (“ETFs”), options, or other investment vehicles, is speculative in nature and involves substantial risk of loss. Robinhood Financial encourages its Customers to invest carefully and to use the information available at the websites of the SEC at http://www.sec.gov and FINRA at http://FINRA.org. -

Proposed Plan of Distribution

UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION ADMINISTRATIVE PROCEEDING File No. 3-20171 : In the Matter of : PROPOSED PLAN OF : DISTRIBUTION Robinhood Financial, LLC, : : Respondent. : I. OVERVIEW 1. Purpose. This Proposed Plan of Distribution (“Plan”) has been developed pursuant to Rule 1101 of the Commission’s Rules on Fair Fund and Disgorgement Plans (“Commission Rules”), 17 C.F.R. § 201.1101. The Plan proposes a distribution of the civil money penalty paid by Robinhood Financial, LLC (“Robinhood” or “Respondent”) to customers who were harmed as a result of Robinhood’s false and misleading disclosures beginning July 1, 2016 through June 30, 2019, inclusive (“Harm Period”). 2. Background. On December 17, 2020, the Commission issued an Order Instituting Administrative and Cease-and-Desist Proceedings Pursuant to Section 8A of the Securities Act of 1933 and Section 15(b) of the Securities Exchange Act of 1934, Making Findings, and Imposing Remedial Sanctions and a Cease-and-Desist Order (the “Order”)1 against Robinhood. The Commission found material misrepresentations and omissions by Robinhood relating to its revenue sources, specifically its receipt of payments from certain principal trading firms, for routing Robinhood customer orders to them. In the Order the Commission found that Robinhood launched its retail brokerage business in 2015, and by mid-2018, it was one of the largest retail broker-dealers in the United States. One of Robinhood’s primary selling points was that it did not charge its customers trading commissions. In reality, however, “commission free” trading at Robinhood came with a catch: Robinhood’s customers received inferior execution prices compared to what they would have received from Robinhood’s competitors. -

IG Response to the Consultation on the Protection of Retail Investors in Relation to the Distribution of Cfds

IG Response to the Consultation on the Protection of Retail Investors in relation to the Distribution of CFDs. We would like to thank the CBI for giving us the opportunity to respond to the Consultation on the Protection of Retail Investors in relation to the Distribution of CFDs. This is an area that we feel very strongly about and we agree that as an industry we must take steps to protect retail clients. One of our main concerns is that the disproportionate implementation of investor protection measures may guide retail clients towards irresponsible firms that are outside the control or influence of the CBI, or indeed of any other EEA regulatory body. We hope that our response, including the quantitative analysis that has been provided and summarised within the appendices to this response, is useful and insightful and we ask that this information is given due consideration as part of the consultation process. 1. Which of the options outlined in this paper do you consider will most effectively and proportionately address the investor protection risks associated with the sale or distribution of CFDs to retail clients? Please give reasons for your answer. We believe that Option 2 would be the more effective and proportionate of the two options offered in CP107 (though we disagree with the details of the suggested leverage restriction regime included within that option – see answer 2(a), below). We think Option 1, a prohibition on the sale or distribution of CFDs to retail clients, would be a counterproductive and disproportionate measure that would be likely to lead to worse client outcomes – both for (i) the set of clients with sufficient understanding and a legitimate need to trade CFDs and (ii) vulnerable clients, for whom CFDs are unsuitable, who will be more likely to be successfully targeted by unscrupulous, unregulated firms. -

Thinkorswim Sharing

Reprinted from Technical Analysis of STOCK S & COMMODITIE S magazine. © 2014 Technical Analysis Inc., (800) 832-4642, http://www.traders.com PRODUCT REVIEW thinkorswim Sharing TD AMERITRADE, INC. SHORTENING THE found both within the thinkorswim AND AFFILIATES LEARNING CURVE platform and the thinkorswim web-based Website: www.thinkorswim.com, Traders who use thinkorswim as their trading platform: www.mytrade.com broker and trading, charting, and n thinkorswim is the actual trading Email: [email protected] analysis platform might just find that and analysis platform; a web and Product: Social media sharing all of those pertinent questions — and mobile version are also available tools and online community for more — can be answered within the thinkorswim users thinkorswim/MyTrade section of this n thinkorswim/Sharing is the broad, Price: Free for TD Ameritrade comprehensive analysis and trading descriptive name that encom- account holders platform. The platform already offers a passes all of the sharing features myriad of unique technical, analytical, linked to thinkorswim by Donald W. Pendergast Jr. and forecasting tools for serious trad- n thinkorswim/MyTrade is a web- ers and investors. Experienced traders site and section within the thinkor- nce an individual makes the using the thinkorswim/MyTrade tools swim platform where user-posted important decision to pursue the will have an eager audience of newer trades, ideas, and charts are dis- O goal of becoming a successful and maturing traders with whom they tributed to other MyTrade users trader, chooses a stock/option/forex/ can freely share their trade ideas, charts, commodity broker, and funds his ac- scans, watchlists, and chart layouts. -

The Law and Economics of Hedge Funds: Financial Innovation and Investor Protection Houman B

digitalcommons.nyls.edu Faculty Scholarship Articles & Chapters 2009 The Law and Economics of Hedge Funds: Financial Innovation and Investor Protection Houman B. Shadab New York Law School Follow this and additional works at: http://digitalcommons.nyls.edu/fac_articles_chapters Part of the Banking and Finance Law Commons, and the Insurance Law Commons Recommended Citation 6 Berkeley Bus. L.J. 240 (2009) This Article is brought to you for free and open access by the Faculty Scholarship at DigitalCommons@NYLS. It has been accepted for inclusion in Articles & Chapters by an authorized administrator of DigitalCommons@NYLS. The Law and Economics of Hedge Funds: Financial Innovation and Investor Protection Houman B. Shadab t Abstract: A persistent theme underlying contemporary debates about financial regulation is how to protect investors from the growing complexity of financial markets, new risks, and other changes brought about by financial innovation. Increasingly relevant to this debate are the leading innovators of complex investment strategies known as hedge funds. A hedge fund is a private investment company that is not subject to the full range of restrictions on investment activities and disclosure obligations imposed by federal securities laws, that compensates management in part with a fee based on annual profits, and typically engages in the active trading offinancial instruments. Hedge funds engage in financial innovation by pursuing novel investment strategies that lower market risk (beta) and may increase returns attributable to manager skill (alpha). Despite the funds' unique costs and risk properties, their historical performance suggests that the ultimate result of hedge fund innovation is to help investors reduce economic losses during market downturns. -

Annual Report 2017

20Annual Remuneration Report Remuneration | Report Financial Report 17Corporate Governance Report Remuneration Report Corporate Governance Report Governance Corporate | We are pioneers and game- changers, stimulated by the endless possibilities of re- en gineering banking. Financial Report | Constant innovation is our key to success. 2017 was especially marked by the implementation of cryptocurrency trading. Swissquote Annual Report 2017 Annual Report 2017 Content 02 Key figures 04 Swissquote share 06 Report to the shareholders 09 Financial Report 10 Consolidated financial statements 108 Report of the statutory auditor on the consolidated financial statements 113 Statutory financial statements 121 Proposed appropriation of retained earnings 122 Report of the statutory auditor on the financial statements 125 Corporate Governance Report 153 Remuneration Report 174 Report of the statutory auditor on the remuneration report 176 Global presence services/global offices The Swiss leader in online banking www.swissquote.com Annual Report 2017 1 Key figures 2017 2016 2015 2014 2013 Number of accounts 309,286 302,775 231,327 221,922 216,357 % change 2.2% 30.9% 4.2% 2.6% 7.3% Assets under custody in CHFm 1 23,240 17,864 11,992 11,562 10,083 % change 30.1% 49.0% 3.7% 14.7% 17.5% Client assets in CHFm 2 24,112 18,557 11,992 11,562 10,083 % change 29.9% 54.7% 3.7% 14.7% 17.5% Employees 593 550 524 532 507 % change 7.8% 5.0% –1.5% 4.9% 37.8% 1 Including cash deposited by clients 2 Including assets that are not held for custody purposes but for which the technology of the Group gives clients access to the stock market and/or that are managed by Swissquote (Robo-Advisory technology). -

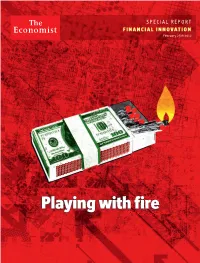

Playing with Fire

SPECIAL REPORT FINANCIAL INNOVATION February 25th 2012 Playing with fire SRFininnov1.indd 1 14/02/2012 15:09 SPECIAL REPORT FINANCIAL INNOVATION Playing with fire Financial innovation can do a lot of good, says Andrew Palmer. It is its tendency to excess that must be curbed FINANCIAL INNOVATION HAS a dreadful image these days. Paul CONTENTS Volcker, a former chairman of America’s Federal Reserve, who emerged 4 How innovation happens from the 2007-08 nancial crisis with his reputation intact, once said that The ferment of nance none of the nancial inventions of the past 25 years matches up to the ATM. Paul Krugman, a Nobel prize-winning economist-cum-polemicist, 5 Retail investors has written that it is hard to think of any big recent nancial break- The little guy throughs that have aided society. Joseph Stiglitz, another Nobel laureate, 6 Exchange-traded funds argued in a 2010 online debate hosted by The Economist that most inno- From vanilla to rocky road vation in the run-up to the crisis was not directed at enhancing the 9 High-frequency trading ability of the nancial sector to The fast and the furious perform its social functions. 11 Financial infrastructure Most of these critics have Of plumbing and promises market-based innovation in their sights. There is an enormous 12 Small rms amount of innovation going on On the side of the angels in other areas, such as retail pay- 13 Collateral ments, that has the potential to Safety rst change the way people carry and spend money. But the debate and hence this special reportfo- Glossary cuses mainly on wholesale pro- Finance has a genius for obscuring simple ducts and techniques, both be- ideas with technical jargon. -

Adame V. Robinhood Financial, LLC Et

Case 5:20-cv-01769 Document 1 Filed 03/12/20 Page 1 of 72 1 THE RESTIS LAW FIRM, P.C. William R. Restis, Esq. (SBN 246823) 2 [email protected] 402 W. Broadway, Suite 1520 3 San Diego, California 92101 Telephone: +1.619.270.8383 4 Counsel for Plaintiff and the Putative Class 5 [Additional Counsel Listed On Signature Page] 6 7 8 9 10 UNITED STATES DISTRICT COURT 11 12 FOR THE NORTHERN DISTRICT OF CALIFORNIA 13 SAN JOSE DIVISION 14 ALEXANDER ADAME, individually and on Case No: 15 behalf of all others similarly situated, 16 Plaintiff, CLASS ACTION COMPLAINT 17 v. 18 DEMAND FOR JURY TRIAL ROBINHOOD FINANCIAL, LLC, a Delaware 19 limited liability company, ROBINHOOD SECURITIES, LLC, a Delaware limited liability 20 Company, and ROBINHOOD MARKETS, INC., a Delaware corporation, 21 22 23 Defendants. 24 25 26 27 28 CLASS ACTION COMPLAINT Case 5:20-cv-01769 Document 1 Filed 03/12/20 Page 2 of 72 1 Plaintiff Alexander Adame (“Plaintiff”), individually and on behalf of all others similarly 2 situated, brings this putative Class aCtion against Defendants Robinhood Financial, LLC 3 (“Robinhood Financial”), Robinhood SeCurities, LLC (“Robinhood SeCurities”), and Robinhood 4 Markets, Inc. (“Robinhood Markets”) (colleCtively, “Robinhood”), demanding a trial by jury. 5 Plaintiff makes the following allegations pursuant to the investigation of Counsel and based upon 6 information and belief, except as to the allegations speCifiCally pertaining to himself, whiCh are 7 based on personal knowledge. ACCordingly, Plaintiff alleges as follows: 8 NATURE OF THE ACTION 9 1. Robinhood is an online brokerage firm. -

Information Circular Solicitation Of

Suite 2400, 1055 West Georgia Street Vancouver, British Columbia, V6E 3P3 Tel: (604) 681-8030 _________________________________________________ INFORMATION CIRCULAR As at October 28, 2020, unless otherwise noted FOR THE ANNUAL GENERAL AND SPECIAL MEETING OF THE SHAREHOLDERS TO BE HELD ON DECEMBER 17, 2020 SOLICITATION OF PROXIES This information circular is furnished in connection with the solicitation of proxies by the management of Voleo Trading Systems Inc. (the “Company”) for use at the Annual General and Special Meeting (the “Meeting”) of the Shareholders of the Company to be held at the time and place and for the purposes set forth in the Notice of Meeting and at any adjournment thereof. PERSONS OR COMPANIES MAKING THE SOLICITATION The enclosed Instrument of Proxy is solicited by management of the Company (“Management”). Solicitations will be made by mail and possibly supplemented by telephone or other personal contact to be made without special compensation by regular officers and employees of the Company. The Company does not reimburse Shareholders’ nominees or agents (including brokers holding shares on behalf of clients) for the cost incurred in obtaining from their principals, authorization to execute the Instrument of Proxy. No solicitation will be made by specifically engaged employees or soliciting agents. The cost of solicitation will be borne by the Company. None of the directors of the Company have advised that they intend to oppose any action intended to be taken by Management as set forth in this Information Circular. NOTICE-AND-ACCESS PROCESS In accordance with the notice-and-access rules under National Instrument 54-101 Communications with Beneficial Owners of Securities of a Reporting Issuer, the Company has sent its proxy-related materials to registered holders and non-objecting beneficial owners using notice-and-access. -

Subscriber Agreement Electronic (NYSE)-TDA 1120

EXHIBIT B AGREEMENT FOR MARKET DATA DISPLAY SERVICES (Nonprofessional Subscriber Status) TD Ameritrade Inc. ("Vendor") agrees to make "Market Data" available to you pursuant to the terms and conditions set forth in this agreement. By executing this Agreement in the space indicated below, you ("Subscriber") agree to comply with those terms and conditions. Section 1 sets forth terms and conditions of general applicability. Section 2 applies insofar as Subscriber receives and uses Market Data made available pursuant to this Agreement as a Nonprofessional Subscriber. SECTION 1: TERMS AND CONDITIONS OF GENERAL APPLICABILITY 1. MARKET DATA DEFINITION – For all purposes of this Agreement, "Market Data" means (a) last sale information and quotation information relating to securities that are admitted to dealings on the New York Stock Exchange ("NYSE*"), (b) such bond and other equity last sale and quotation information, and such index and other market information, as United States-registered national securities exchanges and national securities associations (each, an "Authorizing SRO") may make available and as the NYSE* may from time to time designate as "Market Data"; and (c) all information that derives from any such information. 2. PROPRIETARY NATURE OF DATA – Subscriber understands and acknowledges that each Authorizing SRO and Other Data Disseminator has a proprietary interest in the Market Data that originates on or derives from it or its market(s). 3. ENFORCEMENT – Subscriber understands and acknowledges that (a) the Authorizing SROs are third-party beneficiaries under this Agreement and (b) the Authorizing SROs or their authorized representative(s) may enforce this Agreement, by legal proceedings or otherwise, against Subscriber or any person that obtains Market Data that is made available pursuant to this Agreement other than as this Agreement contemplates. -

Rulemaking Petition Concerning Market Data Fees

December 6, 2017 VIA ELECTRONIC DELIVERY Mr. Brent J. Fields Secretary U.S. Securities and Exchange Commission 100 F Street, NE Washington, DC 20549-1090 RE: Petition for Rulemaking Concerning Market Data Fees Dear Mr. Fields: The undersigned capital market participants (the “Undersigned Firms”) respectfully petition the U.S. Securities and Exchange Commission (the “SEC”) to initiate rulemaking proceedings to require exchanges to disclose certain information concerning fees charged to market participants for equity market data, to institute a public notice and comment process before SEC approval or disapproval of exchange rule filings related to certain market data fees, and to conduct a thorough review of equity market data fee structure as it relates to the collection, distribution, and sale of market data. Exchanges Enjoy an Oligopoly over Equity Market Data Fees Under the Securities Acts Amendments of 1975, Congress granted broad authority to the SEC to establish a National Market System (“NMS”) for securities. Within this framework, exchanges effectively control the dissemination and sale of all equity market data—which securities trading and institutional firms have no choice but to purchase regardless of the cost if they want to remain competitive in the marketplace. This structure has led to accelerating and significant price escalation for market data. As required by the SEC’s Display Rule, vendors and broker-dealers are required to display consolidated data from all the market centers that trade a stock.1 In order to comply with the Display Rule, such vendors and broker-dealers must purchase and display consolidated data feeds distributed by securities information processors (“SIPs”), which are owned by the exchanges and operated pursuant to NMS plans. -

Staff Report on Algorithmic Trading in U.S. Capital Markets

Staff Report on Algorithmic Trading in U.S. Capital Markets As Required by Section 502 of the Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 This is a report by the Staff of the U.S. Securities and Exchange Commission. The Commission has expressed no view regarding the analysis, findings, or conclusions contained herein. August 5, 2020 1 Table of Contents I. Introduction ................................................................................................................................................... 3 A. Congressional Mandate ......................................................................................................................... 3 B. Overview ..................................................................................................................................................... 4 C. Algorithmic Trading and Markets ..................................................................................................... 5 II. Overview of Equity Market Structure .................................................................................................. 7 A. Trading Centers ........................................................................................................................................ 9 B. Market Data ............................................................................................................................................. 19 III. Overview of Debt Market Structure .................................................................................................