Cost of Doing Business in the Philippines

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Participating Robinsons Supermarket Branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST

Participating Robinsons Supermarket branches: STORE NAME ADDRESS ROBINSONS EASYMART AGUIRRE 330 AGUIRRE AVENUE CORNER TEHRAN ST. NOAH'S ARC BLDG. BF HOMES PARANAQUE CITY ROBINSONS EASYMART ALIMA BAY ALIMA BAY RESIDENCES AND COMMERCIAL COMPLEX IN GEN. EVANGELISTA ST. BRGY. ALIMA BACOOR CAVITE ROBINSONS EASYMART ANTIPOLO ROBINSONS EASYMART ANTIPOLO RODRIGUEZ ROAD BARANGAY SITIO PARUGAN SAN JOSE ANTIPOLO CITY ROBINSONS EASYMART ARNAIZ ARNAIZ AVENUE, LIBERTAD PASAY CITY PASAY 1300 ROBINSONS EASYMART E RODRIGUEZ SR 340 E. RODRIGUEZ SR. AVE COR. CORDILLERA ST. BRGY. DON MANUEL, QC ROBINSONS EASYMART FILINVEST BATASAN FILINVEST II GATE B SAN MATEO ROAD-BATASAN HILLS QUEZON HILLS CITY ROBINSONS EASYMART GREENGATE IMUS PHASE 3 GREEN GATE SUBDV. MALAGASANG 2A IMUS CAVITE ROBINSONS EASYMART KAMUNING #89 K1ST BARANGAY KAMUNING QUEZON CITY ROBINSONS EASYMART LAGRO SUNBEST BLDG. ASCENSION AVENUE BRGY. GREATER LAGRO, QUEZON CITY ROBINSONS EASYMART LOYOLA HEIGHTS #88 ROSA ALVERO ST. LOYOLA HEIGHTS QUEZON CITY ROBINSONS EASYMART MARILAO GROUND FLOOR OF CINDY SQUARE IN MC ARTHUR HIGHWAY, ABANGAN,NORTE,MARILAO BULACAN ROBINSONS EASYMART MARIPOSA ARCADE G/F MARIPOSA ARCADE A. MABINI ST. KAPASIGAN PASIG CITY ROBINSONS EASYMART MOONWALK LP G/F SAVER'S BUILDUING ALABANG ZAPOTE ROAD TALON 1 MOONWALK LAS PINAS CITY ROBINSONS EASYMART PILILIA RIZAL J.P. RIZAL STREET, BRGY. IMATONG, PILILLA, RIZAL ROBINSONS EASYMART POBLACION 888 SAN IGNACIO ST., BRGY. POBLACION I, SAN JOSE DEL MONTE BULACAN 3023 PHILIPPINES ROBINSONS EASYMART PROJECT 6 #54 EMERALD COURT BLDG. ROAD 8, PROJECT 6, QUEZON CITY ROBINSONS EASYMART SAN AGUSTIN-TANZA SAN AGUSTIN COR SAN FRANCISCO ST POBLACION 2 TANZA CAVITE 4108 PHILIPPINES ROBINSONS EASYMART SAN MATEO KAMBAL ROAD BRGY.GITNANG BAYAN 1 SAN MATEO, RIZAL ROBINSONS EASYMART SAVERS ROOSEVELT 192 SAVERS APPLIANCE DEPOT ROOSEVELT AVE. -

Intellectual Property Center, 28 Upper Mckinley Rd. Mckinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel

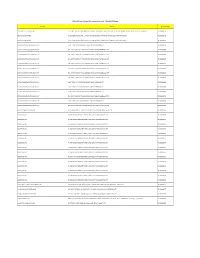

Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: September 13, 2016 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION .................................................................................................... 2 1.1 ALLOWED NATIONAL MARKS ............................................................................................................................................. 2 Intellectual Property Center, 28 Upper McKinley Rd. McKinley Hill Town Center, Fort Bonifacio, Taguig City 1634, Philippines Tel. No. 238-6300 Website: http://www.ipophil.gov.ph e-mail: [email protected] Publication Date: September 13, 2016 1 ALLOWED MARKS PUBLISHED FOR OPPOSITION 1.1 Allowed national marks Application No. Filing Date Mark Applicant Nice class(es) Number 19 1 4/2011/00015098 December BODY-SOLID BODY-SOLID, INC. [US] 28 2011 2 October RICEGARD AGRISOLUTIONS 2 4/2012/00502568 1 2012 BUTACHLOR 600EC PHILIPPINES INC [PH] 10 July BEIJING JINGDONG 360 DU 3 4/2013/00008085 JD.COM 35 2013 E-COMMERCE LTD [CN] 29 October 4 4/2013/00013041 ECOLIFE STEVE C. CHUA [PH] 7; 8; 11 and21 2013 13 ADVANCING ASIS INTERNATIONAL, INC. 5 4/2013/00013637 November SECURITY 35 and41 [US] 2013 WORLDWIDE 22 January INTEX MARKETING LTD. 6 4/2013/00500209 AIR LOCK 12; 20 and28 2013 [HK] 2 January 7 4/2014/00000002 INNOFLU NOVARTIS AG [CH] 5 2014 30 January 8 4/2014/00001283 YETI YETI COOLERS, LLC [US] 21 2014 21 OPTIMUS WITH 9 4/2014/00002306 February GUARDIAN SanDisk LLC [US] 9 2014 TECHNOLOGY MOBILE BUSINESS 25 INTEGRATION, LEISURE & 16; 18; 22; 25 10 4/2014/00002390 February PERYAHAN ENTERTAINMENT and35 2014 SYSTEMS, INC [PH] 7 March JIANGSU SANYUAN TIRE 11 4/2014/00002854 NJK 12 2014 CO., LTD [CN] 5 May AMOREPACIFIC 12 4/2014/00005423 AIRCELL 21 2014 CORPORATION [KR] 8 May 13 4/2014/00005720 JOY ESPERMA NOEL G. -

Bonchon Store List

Bonchon Store List RCBC Bankard-JCB Spend Anywhere Store Name Store Address SM MEGAMALL Unit 159-A, Bldg. A, Upper Ground Floor, SM Megamall, Mandaluyong City ROBINSONS GALLERIA Ground Floor, Food Court, Robinsons Galleria, Ortigas, Pasig City GREENHILLS PROMENADE Unit FC 4, Lower Level, Greenhills Promenade, GSC, Ortigas Avenue, San Juan City KATIPUNAN 2F Regis Center, 327 Katipunan Avenue, Quezon City SHANGRI-LA PLAZA Unit 48 Lower Ground Floor Level, Shangrila Plaza Mall, Edsa Shaw Boulevard, Mandaluyong City UNIVERSITY MALL TAFT Ground Floor University Mall, 2507 Taft Avenue, Malate, Manila TOMAS MORATO 2nd Floor Il Terrazo, Tomas Morato corner Scout Madrinan, Quezon City TRINOMA Level 1 Trinoma, Quezon City SM MALL OF ASIA G/F Space 100-101, SM Mall of Asia, Diokno Boulevard, Pasay City ALABANG TOWN CENTER Space 1011 Lower Ground Floor, New Wing, The Garden, Alabang Town Center, Alabang, Muntinlupa City GREENBELT Ground Floor, Greenbelt 1, Ayala Center, Paseo de Roxas, Brgy. San Lorenzo, Makati City AYALA TRIANGLE GARDEN Ground Floor Space 4, Ayala Triangle Gardens, Paseo de Roxas corner Makati Avenue, Makati Cty LUCKY CHINATOWN 3rd Floor Lucky Chinatown Mall, Reina Regente corner Dela Reina Sts., Brgy. 293, Zone 28, Binondo, Manila SM TAYTAY GF Building A, SM City Taytay, Manila East Road, Brgy. Dolores, Taytay, Rizal SM NORTH EDSA ANNEX 3/F SM North Edsa, The Annex, Quezon City HIGH STREET THE FORT Ground Level, 7th Avenue corner 28th St., One Parkade Building, Bonifacio High Street, Taguig City SM FAIRVIEW 2/F Main Building, Quirino Avenue corner Regalado St., Greater Lagro, Quezon City SM MANILA 4/F Unit 418, SM Manila, Concepcion corner Arroceros and San Marcelino Streets, Manila ROBINSONS MANILA 4/F Center Atrium, Robinsons Place Ermita, Manila EASTWOOD Unit H2A, Eastwood City Walk 1, Eastwood City, Libis, Quezon City SM DAVAO G/F The Annex, SM City Davao, Quimpo Blvd., Tulip Drive, Ecoland Subdivision Matina, Davao City UP TECHNOHUB 2/F Space No. -

1623400766-2020-Sec17a.Pdf

COVER SHEET 2 0 5 7 3 SEC Registration Number M E T R O P O L I T A N B A N K & T R U S T C O M P A N Y (Company’s Full Name) M e t r o b a n k P l a z a , S e n . G i l P u y a t A v e n u e , U r d a n e t a V i l l a g e , M a k a t i C i t y , M e t r o M a n i l a (Business Address: No. Street City/Town/Province) RENATO K. DE BORJA, JR. 8898-8805 (Contact Person) (Company Telephone Number) 1 2 3 1 1 7 - A 0 4 2 8 Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) NONE (Secondary License Type, If Applicable) Corporation Finance Department Dept. Requiring this Doc. Amended Articles Number/Section Total Amount of Borrowings 2,999 as of 12-31-2020 Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. 2 SEC Number 20573 File Number______ METROPOLITAN BANK & TRUST COMPANY (Company’s Full Name) Metrobank Plaza, Sen. Gil Puyat Avenue, Urdaneta Village, Makati City, Metro Manila (Company’s Address) 8898-8805 (Telephone Number) December 31 (Fiscal year ending) FORM 17-A (ANNUAL REPORT) (Form Type) (Amendment Designation, if applicable) December 31, 2020 (Period Ended Date) None (Secondary License Type and File Number) 3 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF CORPORATION CODE OF THE PHILIPPINES 1. -

Disclose the Name of Such Stock Exchange and the Class of Securities Listed Therein

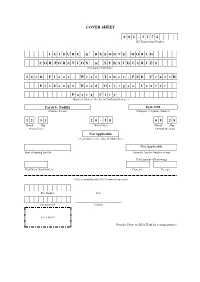

COVER SHEET 0 0 1 - 3 1 7 4 SEC Registration Number L E I S U R E & R E S O R T S W O R L D C O R P O R A T I O N & S U B S I D I A R I E S (Company’s Full Name) 2 6 t h F l o o r , W e s t T o w e r , P S E C e n t e R E x c h a n g e R o a d O r t i g a s C e n t e r P a s i g C i t y (Business Address: No. Street City/Town/Province) Carol V. Padilla 8634-2598 (Contract Person) (Company Telephone Number) 1 2 3 1 2 0 - I S 0 8 2 8 Month Day (Form Type) Month Day (Fiscal Year) (Annual Meeting) Not Applicable (Secondary License Type, If Applicable) Not Applicable Dept. Requiring this Doc. Amended Articles Number/section Total Amount of Borrowings Total No. of Stockholders Domestic Foreign To be accomplished by SEC Personnel concerned File Number LCU Document ID Cashier S T A M P S Remarks: Please use BLACK ink for scanning purposes. SECURITIES AND EXCHANGE COMMISSION SEC FORM 20-IS INFORMATION STATEMENT PURSUANT TO SECTION 20 OF THE SECURITIES REGULATION CODE 1. Check the appropriate box: [ ] Preliminary Information Statement [ / ] Definitive Information Statement 2. Name of Registrant as specified in its Charter: LEISURE & RESORTS WORLD CORPORATION 3. Province, country or other jurisdiction of incorporation or organization: PHILIPPINES 4. -

DOLE-NCR for Release AEP Transactions As of 7-16-2020 12.05Pm

DOLE-NCR For Release AEP Transactions as of 7-16-2020 12.05pm Company Address Transaction No. 3M SERVICE CENTER APAC, INC. 17TH, 18TH, 19TH FLOORS, BONIFACIO STOPOVER CORPORATE CENTER, 31ST STREET COR., 2ND AVENUE, BONIFACIO GLOBAL CITY, TAGUIG CITY TNCR20000756 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000178 3O BPO INCORPORATED 2/F LCS BLDG SOUTH SUPER HIGHWAY, SAN ANDRES COR DIAMANTE ST, 087 BGY 803, SANTA ANA, MANILA TNCR20000283 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000536 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000554 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000569 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000607 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000617 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000632 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000633 8 STONE BUSINESS OUTSOURCING OPC 5TH-10TH/F TOWER 3, PITX #1, KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000638 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY ROAD, TAMBO, PARAÑAQUE CITY TNCR20000680 8 STONE BUSINESS OUTSOURCING OPC 5-10/F TOWER 1, PITX KENNEDY -

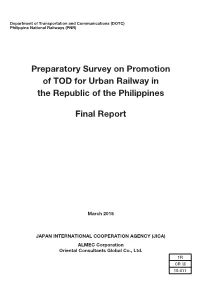

Preparatory Survey on Promotion of TOD for Urban Railway in the Republic of the Philippines Final Report Final Report

the Republic of Philippines Preparatory Survey on Promotion of TOD for Urban Railway in Department of Transportation and Communications (DOTC) Philippine National Railways (PNR) Preparatory Survey on Promotion of TOD for Urban Railway in the Republic of the Philippines Final Report Final Report March 2015 March 2015 JAPAN INTERNATIONAL COOPERATION AGENCY (JICA) ALMEC Corporation Oriental Consultants Global Co., Ltd. 1R CR(3) 15-011 TABLE OF CONTENTS EXECUTIVE SUMMARY MAIN TEXT 1. INTRODUCTION .......................................................................................................... 1-1 1.1 Background and Rationale of the Study ....................................................................... 1-1 1.2 Objectives, Study Area and Counterpart Agencies ...................................................... 1-3 1.3 Study Implementation ................................................................................................... 1-4 2 CONCEPT OF TOD AND INTEGRATED DEVELOPMENT ......................................... 2-1 2.1 Consept and Objectives of TOD ................................................................................... 2-1 2.2 Approach to Implementation of TOD for NSCR ............................................................ 2-2 2.3 Good Practices of TOD ................................................................................................. 2-7 2.4 Regional Characteristics and Issues of the Project Area ............................................. 2-13 2.5 Corridor Characteristics and -

Event Results

Brent International School Manila HY-TEK's MEET MANAGER 7.0 - 3:41 PM 9/14/2019 Page 1 42nd Brent Invitational Swim Meet - 9/14/2019 Results Event 1 Girls 8 & Under 25 SC Meter Freestyle Name Age Team Seed Time Finals Time Points 1 Leighton, Ella 8 Brent International School 18.31 18.44 7 2 Rivadelo, Bella 8 NordAngliaIntlSchoolMnl 22.98 18.59 5 3 Flegler, Lilika 8 Manila Japanese School 19.37 19.46 4 *4 Hoddinott, Senna 7 International School Manila 20.36 19.81 2 . 50 *4 Prashasnth, Draya 8 NordAngliaIntlSchoolMnl NT 19.81 2 . 50 6 Bate, Chiara Marie 8 International School Manila 19.83 20.17 1 7 Ratkai, Szoia 6 International School Manila 21.04 20.53 8 Akimoto, Wakana 7 Manila Japanese School 22.21 21.02 9 Georgiou, Angelica 7 International School Manila 21.41 21.13 10 Georgiou, Joanita 7 International School Manila 22.04 21.39 11 Nguyen, Quyen 7 International School Manila 21.63 21.45 *12 Ando, Shiori 7 Manila Japanese School 33.00 22.12 *12 Green, Emma 8 International School Manila 32.74 22.12 14 Martel, Anika 7 British School Manila 23.45 22.28 15 Endo, Hanna 7 International School Manila 21.44 22.49 16 Long, Caylin 7 British School Manila 27.70 22.70 17 Elliot Lopez, Tara 8 British School Manila 26.08 23.47 18 Wee, Mariana 6 British School Manila 32.58 24.36 19 Barber, Sienna 8 International School Manila 23.64 24.49 20 Quiñonero Lozano, Lucia 7 International School Manila 25.39 24.53 21 Power, Zara 7 British School Manila 24.99 24.72 22 Gane, Raynaya 7 British School Manila 26.57 24.79 23 Hayashi, Fumiko 7 International School Manila -

Domestic Branch Directory BANKING SCHEDULE

Domestic Branch Directory BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays cor Gen. Araneta St. and Aurora Blvd., Cubao, Quezon 1 Q.C.-Cubao Main 911-2916 / 912-1938 9:00 AM – 4:00 PM City 912-3070 / 912-2577 / SRMC Bldg., 901 Aurora Blvd. cor Harvard & Stanford 2 Q.C.-Cubao-Harvard 913-1068 / 912-2571 / 9:00 AM – 4:00 PM Sts., Cubao, Quezon City 913-4503 (fax) 332-3014 / 332-3067 / 3 Q.C.-EDSA Roosevelt 1024 Global Trade Center Bldg., EDSA, Quezon City 9:00 AM – 4:00 PM 332-4446 G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 4 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Elliptical Road cor. Kalayaan Avenue, Diliman, Quezon 920-3353 / 924-2660 / 5 Q.C.-Elliptical Road 9:00 AM – 4:00 PM City 924-2663 Aurora Blvd., near PSBA, Brgy. Loyola Heights, 421-2331 / 421-2330 / 6 Q.C.-Katipunan-Aurora Blvd. 9:00 AM – 4:00 PM Quezon City 421-2329 (fax) 335 Agcor Bldg., Katipunan Ave., Loyola Heights, 929-8814 / 433-2021 / 7 Q.C.-Katipunan-Loyola Heights 9:00 AM – 4:00 PM Quezon City 433-2022 February 07, 2014 : G/F, Linear Building, 142 8 Q.C.-Katipunan-St. Ignatius 912-8077 / 912-8078 9:00 AM – 4:00 PM Katipunan Road, Quezon City 920-7158 / 920-7165 / 9 Q.C.-Matalino 21 Tempus Bldg., Matalino St., Diliman, Quezon City 9:00 AM – 4:00 PM 924-8919 (fax) MWSS Compound, Katipunan Road, Balara, Quezon 927-5443 / 922-3765 / 10 Q.C.-MWSS 9:00 AM – 4:00 PM City 922-3764 SRA Building, Brgy. -

Weekend Banking Schedule BANKING SCHEDULE

Weekend Banking Schedule BANKING SCHEDULE Branch Name Present Address Contact Numbers Monday - Friday Saturday Sunday Holidays G/F, One Cyberpod Centris, EDSA Eton Centris, cor. 332-5368 / 332-6258 / 1 Q.C.-EDSA-Eton Centris 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM EDSA & Quezon Ave., Quezon City 332-6665 Unit 2, G/F Unimart Capitol Commons, Shaw Blvd. 10:00 AM – 7:00 10:00 AM – 7:00 2 Pasig-Capitol Commons 636-7465 / 631-3996 cor. Meralco Ave., Brgy. Oranbo, Pasig City PM PM Stall 3S-04, 168 Shopping Mall, Sta. Elena, Soler Sts., 3 Divisoria-168 Mall 254-5279 / 254-7479 9:00 AM – 4:00 PM 9:00 AM – 4:00 PM Binondo, Manila 4 Manila-Century Park Hotel G/F, Century Park Hotel, M. Adriatico cor. P. Ocampo 524-8385 / 525-3792 / 10:00 AM – 5:30 10:00 AM – 5:30 Upper Ground Level, Starmall Alabang, South 10:00 AM – 6:00 10:00 AM – 4:00 5 Muntinlupa-Starmall Alabang 828-5023 / 555-0668 Superhighway, Alabang, Muntinlupa City, 1770 PM PM 6:00 AM – 2:00 6:00 AM – 2:00 6:00 AM – 2:00 6 NAIA 1-Arrival Area Arrival Area Lobby, NAIA Terminal 1, Parañaque City 879-6040 / 831-2640 Open AM AM AM 832-2660 / 832-2606 7 NAIA 1-Departure Area Departure Area, NAIA Terminal 1, Parañaque City 4:30 AM – 8:00 PM 4:30 AM – 8:00 PM 4:30 AM – 8:00 PM Open (fax) NAIA Centennial Terminal 2, Northwing Level 879-5946 / 879-5949 / 8 NAIA 2-Departure Area 6:00 AM – 8:00 PM 6:00 AM – 8:00 PM 6:00 AM – 8:00 PM Open Departure Intl.,Bldg., Pasay City 879-5947 (fax) MIAA Trunk Line: 8777- Arrival Area , NAIA Terminal 3, Pasay City 6:00 AM – 6:00 6:00 AM – 6:00 6:00 AM – 6:00 9 NAIA 3-Arrival Area 888 loc. -

INFORMATION SHEET for INTERNAL TRAINING PURPOSES ONLY Come to Where Contemporary Lifestyles M Eet

INFORMATION SHEET FOR INTERNAL TRAINING PURPOSES ONLY COMe To WHERE CONTEMPORARY LIFESTYLEs M EET FOR INTERNAL TRAINING PURPOSES ONLY VERSION 1.0 AS OF MARCH 2015 A MASTER PLAN OF CONVERGENCE The core of Bonifacio Global City’s new center of gravity, Park Triangle, presents Alveo Land’s Park Triangle Residences. This sole condominium development in this dynamic destination, located at the corner of 32nd Street and 11th Avenue, offers unmatched proximity to premier schools, offices, and leisure scenes. A landmark tower among the few communities to rise above the area’s corporate row, it is also the only property in BGC with direct access to an Ayala mall. PARK TRIANGLE RESIDENCES ARTIST’S PERSPECTIVE FOR INTERNAL TRAINING PURPOSES ONLY FOR INTERNAL TRAINING PURPOSES ONLY VERSION 1.0 AS OF MARCH 2015 VERSION 1.0 AS OF MARCH 2015 BONIFACIO GLOBAL CITY An Ayala Land growth center with unmatched accessibility— perfect for a city where life comes together. Breakthrough ideas connecting, practices rooted in sustainability, a city that works. Infrastructure, city management, and green processes collaborating for an unparalleled living and working experience. At BGC’s new center of gravity, Park Triangle pulls you closer to a galaxy of urban conveniences orbiting your pivotal destination. BGC SkYLINE FOR INTERNAL TRAINING PURPOSES ONLY FOR INTERNAL TRAINING PURPOSES ONLY VERSION 1.0 AS OF MARCH 2015 VERSION 1.0 AS OF MARCH 2015 KALAYAAN AVENUE TO MAKATI/ORTIGAS MANILA JAPANESE SCHOOL 8TH AVE THE BRITISH SCHOOL MANILA ST. LUKE’S 34TH ST MEDICAL 38TH ST CENTER S&R MC HOME DEPOT TURF BGC ENERGY CENTER INTERNATIONAL CROSSROADS SCHOOL MANILA RIZAL DRIVE 5TH AVE 32ND ST SHANGRI-LA UP PROFESSIONAL AT THE FORT 7TH AVE SCHOOLS TRACK 30TH THE MINDMUSEUM EVERY ONE BONIFACIO NATION 9TH AVE TRESTON HIGH STREET BONIFACIO INTERNATIONAL HIGH STREET COLLEGE 30TH ST CARLOS P. -

School Membership Pack

SCHOOL MEMBERSHIP PACK 1. Introduction Letter p. 2 2. Membership Application Form p. 4 3. Pre-Membership Visit Survey Form p. 8 4. Candidate School Staff List Form p. 11 5. Pre-Membership Visit Report p. 12 6. Application Procedure Flowchart p. 29 7. FOBISIA Constitution p. 30 8. FOBISIA By-Laws p. 41 9. Pre-Membership Visit Document Checklist p. 60 10. Schedule of School Membership Fees p. 61 11. School Membership FAQs p. 62 FOBISIA Chair | Mr. Anthony Rowlands | [email protected] FOBISIA CEO | Mr. John Gwyn Jones | [email protected] Dear Applicant, RE INVITATION TO APPLY FOR FOBISIA MEMBERSHIP FOR YOUR SCHOOL Thank you for your interest in becoming a FOBISIA Member School. Membership is open to schools located in Asia that provide a British-type curriculum for a significant majority of students. To qualify as members, schools must satisfy the membership criteria as set out in FOBISIA’s Constitution and By-laws, and successfully complete the application process as set out in Regulation 6 of the Constitution. The governing body of a school must approve the application. To apply for membership of FOBISIA, please prepare a Letter of Intent, which is an official letter from the Head of School (max. one A4-page) providing some context for the application, e.g. history of the school, current status, reasons for wanting to join FOBISIA. Please also complete the following forms and email them, along with your Letter of Intent, to FOBISIA (To: [email protected] ): • Initial Application Form (F1) • Pre-Membership Visit Survey Form (F2) • Staff List Form (F3) Please ensure you retain a copy of these documents as they may be required for reference in a subsequent stage of the application process, should a Pre-Membership Visit be recommended by FOBISIA’s Membership Committee.