POLITECNICO DI TORINO Competitive Landscape

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

How Hyundai's Racing Cars Inspire Road Cars

How Hyundai’s racing cars inspire road cars: new episode of Are We There Yet? podcast • The sixth episode of Hyundai Motor’s podcast, Are We There Yet?, has been released • This episode features guests Till Wartenberg, Vice President and Head of N Brand Management and Motorsport Sub-division at Hyundai Motor Company, and Hyundai Motorsport Customer Racing driver Luca Engstler • Wartenberg and Engstler discuss the N brand’s commitment to cater to its younger customer base, as well as technology transfer from motorsport to N models and other Hyundai road-going cars • Listen and subscribe to the podcast here Offenbach, XX April 2021 – Hyundai Motor has released the sixth episode of its bi-weekly podcast, Are We There Yet?, hosted by motorsport and technology presenter Suzi Perry. In “How our racing cars inspire road cars”, Perry invites Till Wartenberg, Vice President and Head of N Brand Management and Motorsport Sub-division at Hyundai Motor Company, and Hyundai Motorsport Customer Racing driver Luca Engstler to discuss the latest developments of Hyundai’s N brand. In the sixth episode, Wartenberg and Engstler enlighten listeners on what N stands for and what it is striving to achieve for the Hyundai brand, how its younger target group influences the development of the company, as well as where N stands in this new era of electrification. Wartenberg recounts the announcements at Hyundai’s recent N Day event, including the world premiere of the all-new KONA N, the shift in N’s core message, and the brand’s commitment to electrification. “It was announced that we are expanding more with the N brand: we are thinking about electrification of N with whatever propulsion that might be feasible in the future. -

2020 Owner's Handbook & Warranty Information

USA USA 2020 Owner's Handbook & Warranty Information Printing : Sep. 16, 2019 Publication No. : NAALL-190911 Printed in Korea Hyundai USA ALL 20MY(Cover)190916.indd 1-3 2019-09-16 오전 8:42:12 IMPORTANT: FOR YOUR CONVENIENCE: Retain this Owner’s Handbook in your glovebox for reference relative to Consumer and Warranty Information. Tel. Your Salesperson is: Tel. Your Service Manager is: Tel. OWNER INFORMATION CHANGES: Your Parts Manager is: * If you change your address or if you are the second or subsequent owner of your HYUNDAI, please complete the Owner Information Change Card in the front of this handbook. SPEEDOMETER REPLACEMENT: Speedometer replaced on with miles on the odometer. (Date) Dealer Code: Name: Warranty Start Date: HYUNDAI Dealer Signature: Hyundai USA ALL 20MY(Cover)190916.indd 4-6 2019-09-16 오전 8:42:12 OWNER INFORMATION CHANGE CARD Check one: If you have changed your address or if you are the second or subsequent owner of your Change of Ownership Hyundai, please notify us immediately by completing and mailing this owner information Change of Address change card to: I no longer own this automobile as of / / Hyundai Customer Care Center It was: Hyundai Motor America Exported Sold PO Box 20850 Destroyed Stolen Fountain Valley, CA 92728 Miss Ms. Mrs. Mr. NEW OWNER INFORMATION CIRCLE LAST NAME FIRST M.I. APT. MAIL ADDRESS: NUMBER STREET ZIP CODE CITY/TOWN STATE - - Home Work Cell TELEPHONE NUMBER CIRCLE VEHICLE IDENTIFICATION: The VIN is located on the driver’s side of the dash. ODOMETER READING VEHICLE IDENTIFICATION NUMBER SIGNATURE 1 Hyundai USA ALL 20MY(Main)190916.indd 1 2019-09-16 오전 8:35:52 Hyundai USA ALL 20MY(Main)190916.indd 2 2019-09-16 오전 8:35:52 TABLE OF CONTENTS OWNER INFORMATION CHANGE CARD .............................................................................................................................. -

Comment 1 for ZEV 2008 (Zev2008) - 45 Day

Comment 1 for ZEV 2008 (zev2008) - 45 Day. First Name: Jim Last Name: Stack Email Address: [email protected] Affiliation: Subject: ZEV vehicles Comment: The only true ZEV vehicles are pure electric that chanrge on renewables Today 96% of the hydrogen is made from fossil fuels. This can be improved on but will take a long time. Today we already have very good Electric Vehicles liek the RAV4 with NiMH batteries that have lasted over 100,000 miles. Too bad Toyota stopped making it. We also have the Tesla and Ebox. Please do what is right. Jim Attachment: Original File Name: Date and Time Comment Was Submitted: 2008-02-16 11:19:59 No Duplicates. Comment 2 for ZEV 2008 (zev2008) - 45 Day. First Name: Star Last Name: Irvine Email Address: [email protected] Affiliation: NEV Owner Subject: MSV in ZEV regulations Comment: I as a NEV owner (use my OKA NEV ZEV about 3,000 miles annually) would like to see MSV (Medium Speed Vehicles) included in ZEV mandate so they can be available in California. I own two other vehicles FORD FOCUS and FORD Crown Vic. I my OKA NEV could go 35 MPH I would drive it at least twice as much as I currently do, and I would feel much safer doing so. 25 MPH top speed for NEV seriously limits its use and practicality for every day commuting. Attachment: Original File Name: Date and Time Comment Was Submitted: 2008-02-19 23:07:01 No Duplicates. Comment 3 for ZEV 2008 (zev2008) - 45 Day. First Name: Miro Last Name: Kefurt Email Address: [email protected] Affiliation: OKA AUTO USA Subject: MSV definition and inclusion in ZEV 2008 Comment: We believe that it is important that the ZEV regulations should be more specific in definition of "CITY" ZEV as to its capabilities and equipment. -

Efficient Dynamics

A subsidiary of BMW AG BMW U.S. Press Information For Release: Immediate Contact: Oleg Satanovsky BMW Product & Technology Spokesperson 201-307-3755 / [email protected] Alex Schmuck BMW Product & Technology Communications Manager [email protected] 201-307-3783 BMW Model Year 2020 Update Information. Woodcliff Lake, NJ – August 1, 2019… Information on design and technical changes, as well as changes to standard equipment, lines, packages and standalone options are included in this document. This document will be continuously updated with the most recent MY20 information as it becomes available. The following upholsteries on X5 (G05), X6 (G06), and X7 (G07) models are not currently (Aug 2019) available for order but will be re-introduced at a later date. • Canberra Beige Vernasca Leather • Cognac Vernasca Leather (available on G07 w/Captain’s Chairs only) • Extended Tartufo Merino Leather (available on G07 w/ Captain’s Chairs only) • Full Tartufo Merino Leather • Amarone Merino Leather Discontinued models for 2020 • BMW 3 Series GT • BMW 6 Series Gran Coupe - 2 - 2020 BMW i3 120Ah BMW i3 battery was upgraded from 94Ah to 120Ah for 2019. Electric only range increased up to 153 miles from 94Ah / 115 miles. 2019 BMW i3 120Ah press release. MY20 i3 information is still tba. 2020 BMW i8 Coupe and Roadster MY20 i8 Coupe and Roadster information is still tba. 2020 BMW 2 Series Coupe and Convertible Prices remain unchanged from 2019. MY20 2 Series Coupes and Convertibles began production in 3/2019. The M2 Competition was new for 2019. 2019 M2 Competition press release The MY20 2 Series receives a second refresh as of March 2019 and has been enhanced with the following features: • New darker taillights • New high-gloss black kidney frame on 230i • Cerium Grey kidney frame, badges, front/side air inserts on M240i • High-gloss black mirror caps on M240i Standard Equipment Changes: • Smoker’s Package has been removed from the standard profile for all 2 series. -

Presentation by Barbara Gonzalez

2011 DC Electric Vehicle Forum December 12, 2011 PEV’s Opportunities and Challenges Barbara M. Gonzalez Manager - Special Projects, NERC Advance Technology Pepco Holdings, Inc. Serving three states and Washington DC in the Mid-Atlantic US Combined Service Territory Transmission & Distribution – 90% of Revenue Competitive Energy / Other PHI Investments Regulated transmission and distribution is PHI’s core business. 1 Copyright 2011 Pepco Holdings, Inc. 1 PHI Business Overview PowerPower Delivery Delivery Electric Electric Gas Electric Customers 767,000 498,000 122,000 547,000 GWh 26,863 13,015 N/A 10,089 Mcf (000’s) N/A N/A 20,300 N/A Service 640 5,000 275 2,700 Area District of Columbia, Major portions Northern Southern (square miles) major portions of of Delmarva Delaware New Jersey & Prince George’s and Peninsula Geography Montgomery Counties Population 2.1 million 1.3 million .5 million 1.1 million PHI History with Electric Vehicles • Member of DOE Site Operator Program – Maintained a fleet of 6 all-electric conversion vehicles • Founding Member of EV America – Developed first utility standards for electric vehicles – Later turned over to DOE • GM PrEView Drive Program – 60 customer drivers for two weeks at a time – Installed over 75 Level 2 chargers • Toyota RAV4 EV Program • Ford Ranger EV Program 3 3 Plug-In Vehicles are coming…. Here • Penetration projections are inconsistent • Initial Impacts to infrastructure will be due to clustering • Significant penetration is still years away • Washington, DC region is expected to be an early target market for several manufacturers EPRI National Projection for Plug-In Vehicle Penetration OEM Deployment in the Washington, DC Region • Ford Transit Connect 2010 • Chevy Volt 2011 • Nissan Leaf 2011 • Ford Focus 2011 • Ford PHEV 2012 • Fisker Nina PHEV 2012 • Tesla 2012 • BMW Megacity 2013 4 Projections ……… In order to estimate demand for PEVs, population and number of vehicles per capita of the PHI service territories was used as a proxy for actual car sales. -

JD Power 2018 US Resale Value Awards

J.D. Power Honors Best Resale Value for Mass Market and Luxury Automotive Brands Lexus Earns the Most Awards for Best Resale Value COSTA MESA, Calif.: 22 Aug. 2018 — J.D. Power continues to turn robust insights into easily digestible information for consumers. The 2018 J.D. Power Resale Value Awards were presented to automotive manufacturers today, recognizing the best resale value across 24 model-level vehicle segments. “This marks the first time J.D. Power is utilizing our transaction database of customer insights to recognize brands and models with the best resale value,” said Jonathan Banks, Vice President of Vehicle Valuations & Analytics at J.D. Power. “We conducted this analysis to provide consumers with a resource that informs them of the depreciation cost they incur when purchasing a new vehicle, thus providing insight on the value of their purchase.” Model-Level Resale Value Awards The brand receiving the most model-level awards is Lexus (five model-level awards), followed by Honda and Toyota with four model-level awards each. The RAM 3500 also has the best resale value in the industry. • Lexus: Lexus IS; Lexus NX; Lexus LS; Lexus GS; and Lexus GX • Honda: Honda Civic; Honda Accord; Honda Odyssey; and Honda Fit • Toyota: Toyota Tundra; Toyota Tacoma; Toyota 4Runner; and Toyota Sienna • Porsche: Porsche Cayman; Porsche Boxster; and Porsche 911 • Subaru: Subaru WRX and Subaru Crosstrek • Dodge: Dodge Charger and Dodge Challenger Other models that rank highest in their respective segments are Acura ILX, Audi Q3, Cadillac Escalade, Chevrolet Tahoe, Jeep Wrangler, Land Rover LR4, and RAM 3500. -

Automotive Foundational Software Solutions for the Modern Vehicle Overview

www.qnx.com AUTOMOTIVE FOUNDATIONAL SOFTWARE SOLUTIONS FOR THE MODERN VEHICLE OVERVIEW Dear colleagues in the automotive industry, We are in the midst of a pivotal moment in the evolution of the car. Connected and autonomous cars will have a place in history alongside the birth of industrialized production of automobiles, hybrid and electric vehicles, and the globalization of the market. The industry has stretched the boundaries of technology to create ideas and innovations previously only imaginable in sci-fi movies. However, building such cars is not without its challenges. AUTOMOTIVE SOFTWARE IS COMPLEX A modern vehicle has over 100 million lines of code and autonomous vehicles will contain the most complex software ever deployed by automakers. In addition to the size of software, the software supply chain made up of multiple tiers of software suppliers is unlikely to have common established coding and security standards. This adds a layer of uncertainty in the development of a vehicle. With increased reliance on software to control critical driving functions, software needs to adhere to two primary tenets, Safety and Security. SAFETY Modern vehicles require safety certification to ISO 26262 for systems such as ADAS and digital instrument clusters. Some of these critical systems require software that is pre-certified up to ISO 26262 ASIL D, the highest safety integrity level. SECURITY BlackBerry believes that there can be no safety without security. Hackers accessing a car through a non-critical ECU system can tamper or take over a safety-critical system, such as the steering, brakes or engine systems. As the software in a car grows so does the attack surface, which makes it more vulnerable to cyberattacks. -

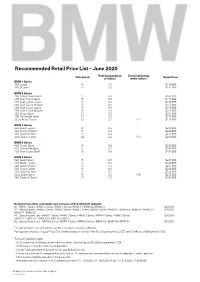

Recommended Retail Price List – June 2020

Recommended Retail Price List – June 2020 Fuel Consumption Electrical Energy VES (band) Retail Price (l/100km) (kWh/100km) BMW 1 Series 118i Luxury B 5.9 $139,888 118i M Sport B 5.9 $142,888 BMW 2 Series 216i Active Tourer Sport B 6.3 $141,888 216i Gran Tourer Sport B 6.5 $147,888 216i Gran Tourer Luxury B 6.5 $154,888 216i Gran Tourer M Sport B 6.5 $157,888 218i Gran Coupe Luxury B 5.9 $155,888 218i Gran Coupe M Sport B 5.9 $158,888 218i Coupe Sport C1 5.5 $161,888 218i Convertible Sport C1 5.8 $177,888 225xe Active Tourer B 2.4 17.4 $176,888 BMW 3 Series 320i Sedan Luxury B 6.3 $200,888 320i Sedan M Sport B 6.3 $206,888 330i Sedan M Sport B 6.4 $233,888 330e Sedan Luxury A2 2.2 15.4 $240,888 BMW 4 Series 420i Coupe Sport B 5.8 $200,888 420i Convertible Sport B 6.2 $242,888 420i Gran Coupe Sport B 5.8 $194,888 BMW 5 Series 520i Sedan Sport B 6.5 $237,888 520i Sedan Luxury B 6.5 $240,888 520i Sedan M Sport B 6.5 $251,888 530i Sedan Luxury B 6.5 $256,888 530i Sedan M Sport B 6.5 $274,888 530e Sedan Sport B 2.0 15.6 $272,888 540i Sedan M Sport C1 7.3 $345,888 Booking Fees (Non-refundable and inclusive of $10,000 COE deposit): A1. -

Mobile Air Conditioner Leakage Rates: Model Year 2018 (Aq-Mvp2-29I)

Mobile Air Conditioner Leakage Rates Model Year 2018 (Alphabetical List) Leakage Rate AC Charge Size Make Model (MY 2018) Type of Vehicle Percentage loss per year (grams/year) (grams) Buick Cascada Passanger Car 8.0 590 1.4 Buick Encore SUV 9.0 570 1.6 Buick Envision SUV 8.0 600 1.3 Chevrolet Corvette Passanger Car 8.3 600 1.4 Chevrolet Express (dual evaporator) Other 10.6 1410 0.8 Chevrolet Express Other 9.5 810 1.2 Chevrolet Sonic Passanger Car 9.8 540 1.8 Chevrolet Trax SUV 9.0 570 1.6 Chevrolet Volt Passanger Car 5.9 1100 0.5 Chevrolet City express cargo van Other 14.1 450 3.1 Ford Transit connect 1.6L GTDI Van/Wagon 7.4 680 1.1 Ford Transit connect 1.6L GTDI (dual evaporator) Van/Wagon 7.9 680 1.2 Ford Transit connect 2.5L Van/Wagon 7.3 680 1.1 Ford Transit connect 2.5L (dual evaporator) Van/Wagon 7.8 880 0.9 Ford Trnasit 3.2L Diesel I5 Van/Wagon 7.4 790 0.9 Ford Trnasit 3.2L Diesel I5 , 130" wheelbase (dual eVan/Wagon 8.1 1110 0.7 Ford Transit 3.2L Diesle I5, 148" wheelbase (dual eVan/Wagon 8.2 1110 0.7 Ford Transit 148" wheelbase ext body Van/Wagon 8.3 1110 0.7 Ford Transit 3.7L TIVAC, 3.5L GTDI V6, 3.7L TIVCTVan/Wagon 7.2 790 0.9 Ford Transit 3.7L TIVCT V6, 130" wheelbase (dual Van/Wagon 7.9 1110 0.7 Ford Transit 3.7L TIVCT V6, 148" wheelbase (dual Van/Wagon 8.0 1110 0.7 Ford Transit 3.5L GTDI V6, 148" Wheelbase ext boVan/Wagon 8.1 1110 0.7 Ford Transit 3.5L GTDI V6, 130" wheelbase (dual e Van/Wagon 7.9 1190 0.7 Ford Transit 3.5L GTDI V6 148 " wheelbase (dual e Van/Wagon 8.0 1190 0.7 Ford Transit 148" wheelbase ext body (dual evaporaVan/Wagon 8.1 1190 0.7 Ford Edge 2.0L I4 GTDI SUV 8.7 680 1.3 Ford Edge/MKX 2.7L V6 GTDI SUV 8.4 600 1.4 Ford Edge 3.5L v6 TiVCT SUV 8.4 680 1.2 Ford Taurus 3.5L GTDI Passanger Car 9.6 740 1.3 Ford Police interceptor Sedan3.5L GTDI Passanger Car 9.6 740 1.3 Ford Taurus 3.5L/3.7L TiVCT Passanger Car 9.8 650 1.5 Ford Police Interceptor Sedan 3.5L/3.7L TiVCT Passanger Car 9.8 650 1.5 Ford Explorer 2.3L GTDI (Dual evaporator) SUV 11.0 1280 0.9 Minnesota Pollution Control Agency • 520 Lafayette Rd. -

Product Catalogue 2017

PRODUCT CATALOGUE 2017 EXCELLENCE IN AUTOMOTIVE ENGINEERING CONTENTS INTRODUCTION 4 VEHICLE TRACKING 5 VEHICLE SECURITY 8 MOTORBIKE SECURITY 12 PARKING SENSORS 14 REAR SEAT ENTERTAINMENT 16 SPEED LIMITER AND CRUISE CONTROL 18 LED LIGHTING 20 VEHICLE CAMERA SYSTEMS 23 BLUETOOTH 24 NOTES 25 VESTATEC PRODUCT CATALOGUE 2017 3 DISTRIBUTED LINES AND SEAMLESS SOLUTIONS TAILORED DIRECTLY TO YOUR NEEDS Established in 1987, Vestatec celebrates its 30th anniversary this year. Today we are Tier 1 suppliers, supplying to the vehicle production line, to seven vehicle manufacturers and we are approved accessory suppliers to 14 brand in the UK. This experience allows us to provide tailored original equipment products to the specialist aftermarket. Our range of services include dedicated installation manuals, installer training, technical helpline and in-house field support team, enabling us to match the vehicle's manufacturer warranty. Whatever you need, we have the expertise and experience to deliver, every time. 4 VESTATEC PRODUCT CATALOGUE 2017 VEHICLE TRACKING From Europe’s number 1 telematics manufacturer, MetaSystem SPA (over 2 million units a year) Meta Trak is a state of the art connected car platform. The perfect combination of mobile App and in-vehicle hardware, delivering live vehicle tracking, driver scoring and multi vehicle access as well as old school stolen vehicle tracking. Meta Trak works seamlessly with any vehicle or machine, delivering peace of mind with always-on-tracking and fast theft alerts. 4 VESTATEC PRODUCT CATALOGUE 2017 VESTATEC PRODUCT CATALOGUE 2017 5 META TRAK VTS A Thatcham Category VTS Insurance Accredited GPS Tracking System. Mobile/Tablet App for IOS and Android, Web Platform with Locate on Demand, Driver Recognition Tags, Driver Card Not Present Alerts, 12 and 24 Volt Compatible, Waterproof, Transferable from Vehicle to Vehicle, Battery Disconnect Alerts, Tow-Away Alerts, Battery Low Alerts via Push Notification/ Email, Monitored by SOC. -

Hyundai Previews I30 Tourer and ‘SR’ Concept Collection at Australian International Motor Show

MEDIA RELEASE 18th October, 2012 Hyundai previews i30 Tourer and ‘SR’ concept collection at Australian International Motor Show The Australian International Motor Show 2012 will see Hyundai Motor Company Australia demonstrate the breadth of its brand character when it showcases two exciting concept cars; the Veloster Race Concept and the Veloster Street Concept. In addition, visitors to the show will preview the SR concepts for Accent and i30 together with the much anticipated i30 Tourer. A line-up of current Hyundai models, including recently launched new Santa Fe and Veloster Turbo will also be on display. New Sydney FC signing and ex-Socceroo Jason Culina and WBF women’s super featherweight champion Lauryn Eagle will be a special guest on the stand for media day. Celebrating Hyundai’s global partnership with football, an interactive FIFA zone will offer visitors to the stand the opportunity to play the all-new FIFA13 Playstation® game, and challenge their favourite Hyundai A-League team to an online match. Hyundai Motor Company Australia: Hall #3 / Stand #12 17 vehicles will be on display from Hyundai Motor Company Veloster Race Concept Car Based on the best-selling Veloster SR Turbo, the Race Concept is a nod to Hyundai’s association with Rally Sports, both in Australia and abroad, and has been is built to meet all FIA and CAMS Tarmac Rally regulations. Developed entirely in Australia, the Veloster Race Concept has been created by the same team who develop Hyundai’s local ride and handling tuning for Australian production vehicles. 1 The Race Concept makes extensive use of light weight components and high performance race parts including a fully stripped out interior, addition of multi-point roll cage, hydraulic handbrake, brake bias adjuster, 4-way adjustable suspension and a myriad of safety features. -

Road to Sustainability

Road to Sustainability 2020 Sustainability Report This report has been published as an interactive PDF, allowing readers Contents Reference Page Video Clip Related Link Homepage Facebook YouTube to move quickly and easily to pages in the report, and including shortcuts to the related web pages. Instagram Twitter 1 2 3 Introduction Sustainable Performance Sustainability Factbook Sustainability Magazine CEO Message Sustainability Management Materiality Analysis Global Network 003 015 078 Sustainability C.A.S.E Brand Vision Mid- to Long-term Goals Business Performance 1 . Clean mobility 004 017 079 2. Advanced technology Future Mobility Vision Facts & Figures 3 . Social values 005 Our Commitment Our System 081 Strategic Direction Smart Mobility-based Corporate Stakeholder Engagement 4. Empowered employees 006 Customer Experience Innovation Governance 092 Company Overview 018 072 GRI Index 007 Pursuing Eco-friendly Value Ethical and Compliance 093 throughout the Entire Value Chain Management Independent Assurance Statement 031 075 098 Special Feature Creating a Sustainable Risk Management COVID-19 Solidarity and Support About This Report Supply Chain 076 008 104 039 Building a Healthy Corporate Culture 047 Contributing to the Development of Local Communities 057 1 Introduction 2 Sustainable Performance 3 Sustainability Factbook Sustainability Magazine 003 CEO Message At the center of Hyundai Motor Company’s management philosophy is “humanity”. The same principle applies to “Progress for Humanity”, the brand We will overcome the crisis together. To secure a leadership position in the global vehicle electrification vision we adopted anew in 2019. We have also established “Strategy Hyundai will proactively respond to change by reprioritizing crisis market, we will develop electric vehicle-only platforms and 2025”, an action plan for achieving our vision of the future mobility management with liquidity at the front and minimize losses by further sharpen the competitive edge of our key drivetrain parts.