Minutes Special Committee On

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Senator Garrett Love Gray 38 Garrett.Love

Senator Garrett Love Gray 38 [email protected] Senator Tom Holland Douglas 3 [email protected] Senator Marci Francisco Douglas 2 [email protected] Senator Jeff Longbine Lyon 17 [email protected] Senator Clark Shultz McPherson 35 [email protected] Senator Pat Apple Miami 37 [email protected] Senator Jeff King Montgomery 15 [email protected] Senator Tom Arpke Saline 24 [email protected] Senator Michael O'Donnell Sedgwick 25 [email protected] Senator Les Donovan Sedgwick 27 [email protected] Senator Greg Smith Johnson 21 [email protected] Senator David Haley Wyandotte 4 [email protected] Senator Pat Pettey Wyandotte 6 [email protected] Senator Kay Wolf Johnson 7 [email protected] Representative Kent Thompson Allen 9 [email protected] Representative Will Carpenter Butler 75 [email protected] Representative Vern Swanson Clay 64 [email protected] Representative Adam Lusker Cherokee 2 [email protected] Representative Ed Trimmer Cowley 79 [email protected] Representative Blaine Finch Franklin 59 [email protected] Representative Allan Rothlisberg Geary 65 [email protected] Representative Marc Rhoades Harvey 72 [email protected] Representative John Ewy Hodgeman 117 [email protected] Representative Stephanie Clayton Johnson 19 [email protected] Representative Erin Davis Johnson 15 [email protected] Representative Brett Hildabrand Johnson 17 [email protected] -

Senator Elaine Bowers Cloud 36 [email protected]

Senator Elaine Bowers Cloud 36 [email protected] Senator Garrett Love Gray 38 [email protected] Senator Tom Holland Douglas 3 [email protected] Senator Jeff King Montgomery 15 [email protected] Senator Pat Apple Miami 37 [email protected] Senator Tom Arpke Saline 24 [email protected] Senator David Haley Wyandotte 4 [email protected] Senator Clark Shultz McPherson 35 [email protected] Senator Michael O'Donnell Sedgwick 25 [email protected] Senator Jeff Longbine Lyon 17 [email protected] Senator Pat Pettey Wyandotte 6 [email protected] Senator Les Donovan Sedgwick 27 [email protected] Senator Marci Francisco Douglas 2 [email protected] Representative Kent Thompson Allen 9 [email protected] Representative Will Carpenter Butler 75 [email protected] Representative Vern Swanson Clay 64 [email protected] Representative Adam Lusker Cherokee 2 [email protected] Representative Ed Trimmer Cowley 79 [email protected] Representative Allan Rothlisberg Geary 65 [email protected] Representative John Ewy Hodgeman 117 [email protected] Representative Stephanie Clayton Johnson 19 [email protected] Representative Erin Davis Johnson 15 [email protected] Representative Brett Hildabrand Johnson 17 [email protected] Representative Keith Esau Johnson 14 [email protected] Representative Emily Perry Johnson 24 [email protected] Representative James Todd -

Kansas Senators

KANSAS SENATORS J.R. Claeys (R) Dist. 24 2157 Redhawk Lane Salina, KS 67401 785-250-5758 (Cell) Capitol Office 224-E 785-296-7369 [email protected] Ethan Corson (D) Dist. 7 PO Box 8296 Prairie Village, KS 66208 785-414-9215 (Cell) [email protected] Capitol Office 125-E 785-296-7390 [email protected] Brenda S. Dietrich (R) Dist. 20 6110 SW 38th Terr. Topeka, KS 66610 785-861-7065 785-221-3853 (Cell) Capitol Office 223-E 785-296-7648 [email protected] John Doll (R) Dist. 39 2927 Cliff Place Garden City, KS 67846 620-271-5391 (Cell) [email protected] Capitol Office 237-E 785-296-7694 [email protected] Renee Erickson (R) Dist. 30 26 N. Cypress Drive Wichita, KS 67206 316-217-1308 (Cell) [email protected] Capitol Office 541-E 785-296-7476 [email protected] Michael A. Fagg (R) Dist. 14 1810 Terrace Dr. El Dorado, KS 67042 316-321-1690 316-377-7987 (Cell) [email protected] Capitol Office 234-E 785-296-7678 [email protected] Oletha Faust Goudeau (D) Dist. 29 PO Box 20335 Wichita, KS 67208 316-652-9067 316-210-4380 (Cell) [email protected] Capitol Office 135-E 785-296-7387 [email protected] Marci Francisco (D) Dist. 2 1101 Ohio Lawrence, KS 66044 785-842-6402 785-766-1473 (Cell) [email protected] Capitol Office 134-E 785-296-7364 [email protected] Beverly Gossage (R) Dist. -

Foulston Siefkin LLP

NEWSLETTERS KANSAS LEGISLATIVE INSIGHTS NEWSLETTER | JANUARY 17, 2020 2020 LEGISLATURE OPENS The 2020 Legislature had a full agenda as both chambers gaveled into session on Monday afternoon. The session opened slowly with organizational matters, the State of the State Address by Gov. Laura Kelly, and introduction of pre-filed bills and interim proposals. On Thursday, the House Appropriations Committee and Senate Ways and Means Committee had a joint meeting as the Governor’s budget was unveiled. The state’s improving financial picture will make funding new programs like Medicaid expansion an option along with the potential of some tax cuts. The Medicaid expansion compromise agreement between Gov. Kelly and Senate Majority Leader Sen. Jim Denning will improve chances for passage in the Senate despite concerns and opposition by some Republican Senators. House Republican leaders are still opposed and likely to try blocking consideration on the House floor despite support for expansion by a majority of House members. The Senate Public Health and Welfare Committee is holding hearings on SB 252 (see our reference to SB 252 and 246 below). Proponents will be heard on Jan. 23- 24, and opponents will be heard on Jan. 27-28. STATE OF THE STATE ADDRESS On Wednesday, Jan. 14, Gov. Kelly delivered her second State of the State address. Her areas of emphasis included funding education and the need to expand Medicaid. She wants Kansas to become the 37th state to do so. Among other areas highlighted were the need to address a comprehensive transportation plan, fiscal stability, modest tax cuts in specific areas, and a continued need to improve the social safety net. -

Report of the Joint Committee on Information Technology to the 2018 Kansas Legislature

JOINT COMMITTEE Report of the Joint Committee on Information Technology to the 2018 Kansas Legislature CHAIRPERSON: Representative Blake Carpenter VICE-CHAIRPERSON: Senator Mike Petersen OTHER MEMBERS: Senators Marci Francisco, Tom Holland, Dinah Sykes, and Caryn Tyson; and Representatives Pam Curtis, Keith Esau, Kyle Hoffman, and Brandon Whipple CHARGE The Committee is directed to: ● Review, monitor, and report on technology plans and expenditures; ● Review and monitor state agency and institution technology plans and expenditures; ● Make recommendations to the Senate Committee on Ways and Means and House Committee on Appropriations on implementation plans, budget estimates, and three-year strategic information technology plans of state agencies and institutions; ● Evaluate the status of the Kansas Eligibility Enforcement System project; ● Evaluate the status of cybersecurity preparedness within the State; ● Follow up with the Kansas Department of Commerce on activity related to the data breach that occurred in March 2017; ● Allow members of the private sector to present relevant information to the Committee; and ● Review information technology security reports and information technology project reports, in executive session, from the Legislative Division of Post Audit. December 2017 Joint Committee on Information Technology REPORT Conclusions and Recommendations The Committee agreed on the following recommendations to the 2018 Legislature: ● Request the Office of Information Technology Services (OITS) present a clear roadmap for the -

2004 Primary Election Results

Kansas Secretary of State Page 1 2004 Primary Election Official Vote Totals Race Candidate Votes Percent United States Senate D-Robert A. Conroy 61,052 55.9 % D-Lee Jones 48,133 44.0 % R-Samuel D. Brownback 286,839 86.9 % R-Arch Naramore 42,880 13.0 % United States House of Representatives 001 R-Jerry Moran 94,098 100.0 % United States House of Representatives 002 D-Nancy Boyda 36,771 100.0 % R-Jim Ryun 69,368 100.0 % United States House of Representatives 003 D-Dennis Moore 33,466 100.0 % R-Kris Kobach 39,129 44.0 % R-Patricia Lightner 10,836 12.1 % R-Adam Taff 38,922 43.7 % United States House of Representatives 004 D-Michael Kinard 14,308 73.0 % D-Marty Mork 5,279 26.9 % R-Todd Tiahrt 53,202 100.0 % Kansas Senate 001 D-Tom Kautz 2,007 58.8 % D-Galen Weiland 1,401 41.1 % R-Richard S. Karnowski 937 8.0 % R-Trent LeDoux 2,683 23.0 % R-Steve Lukert 3,381 29.0 % R-Dennis D. Pyle 4,642 39.8 % Kansas Senate 002 D-Marci Francisco 2,999 100.0 % R-Mark Buhler 3,221 63.0 % R-Don Johnson 1,889 36.9 % Kansas Senate 003 D-Jan Justice 3,036 71.5 % D-Edward (Ed) Sass 1,207 28.4 % R-Connie O'Brien 2,673 33.6 % R-Roger C. Pine 3,760 47.2 % R-Chuck Quinn 586 7.3 % R-Richard Rodewald 933 11.7 % Kansas Senate 004 D-David Haley 5,140 100.0 % Kansas Senate 005 D-Mark S. -

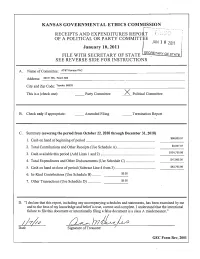

~)L1l~ Date Signature Oftreasurer

,., , .. A. Name of Committee: AT&T Kansas PAC --------------------------- Address: 220 E. 6th, Room 500 City and Zip Code: T_o_pe_ka_,_66_60_3 _ This is a (check one): __ Party Committee x Political Committee B. Check only ifappropriate: __Amended Filing __·Termination Report C. Summary (covering the period from October 22,2010 through December 31, 2010) $96,803.91 1. Cash on hand at beginning of period . 2. Total Contributions and Other Receipts (Use Schedule A) . $4,947.07 3. Cash available this period (Add Lines I and 2) . $101,750.98 4. Total Expenditures and Other Disbursements (Use Schedule C) : $17,985.00 5. Cash on hand at close of period (Subtract Line 4 from 3) . $83,765.98 6. In-Kind Contributions (Use Schedule B) . $0.00 7. Other Transactions (Use Schedule D) . $0.00 D. "I declare that this report, including any accompanying schedules and statements, has been examined by me and to the best of my knowledge and belief is true, correct and complete. I understand that the intentional failure to file this document or intentionally filing a false document is a class A misdemeanor." ~/~h ~)l1L~ Date Signature ofTreasurer GEe Form Rev, 2001 SCHEDULE A CONTRIBUTIONS AND OTHER RECEIPTS AT&T Kansas PAC (N arne of Party Committee or Political Committee) Occupation & Industry of Check Amount of Name and Address Individual Giving More Appropriate Box Cash, Check, Date of Contributor Than $150 Loan or CBlib Check L080 Other Other Receipt ING Direct $57.48 P. O. Box 60 10/31/2010 St. Cloud, MN 56302-0060 .f ING Direct $55.67 P.O. -

October 2020

October 2020 SPECIAL CONCERT ON THE LAWN: KANSAS CITY SYMPHONY Monday, October 12 @ 6:30 to 7:15 pm Musicians from the Kansas City Symphony are coming to the li- brary to perform a free outdoor chamber concert in our parking lot Meet the Candidates Forums and lawn! We can’t wait to share wonderful music with you on a Basehor Community Library has for the last several years beautiful evening! The musicians hosted Candidate Forums during election cycles. We would will be playing on a stage in the like to continue this tradition, but this year we are constrained parking lot, so if you wish to sit please bring your folding by the challenges of the pandemic. Our alternative to a live chairs or blankets. To protect attendees, Library staff, and the in-person forum is to hold the forums online, using the Zoom musicians, all are asked to maintain social distancing and wear platform. Meet the Candidates vying for the honor of masks. See you there! representing Basehor in the Kansas Legislature at two We are combining the Concert on the Lawn with a Food special forums, hosted by the library, to be broadcast live on Zoom. The programs will only be online. A moderated Drive for Basehor-Linwood Assistance Service. During this question and answer session will follow each candidate’s difficult time, food insecurity is a real problem in the Basehor opening remarks. community. If you have something to spare, please bring canned goods or personal hygiene items to the library during Candidates for Kansas House District #38 the KC Symphony concert on Monday, October 12 . -

Members of the Senate Judiciary Committee, I Sent an Email Last

From: Ronald R.Hein <[email protected]> Sent: Thursday, June 4, 2020 9:41 AM To: David Haley <[email protected]>; Dennis Pyle <[email protected]>; Elaine Bowers <[email protected]>; Eric Rucker <[email protected]>; Julia Lynn <[email protected]>; Mike Petersen <[email protected]>; Mike Thompson <[email protected]>; Molly Baumgardner <[email protected]>; Randall Hardy <[email protected]>; Richard Wilborn <[email protected]>; Vic Miller <[email protected]> Cc: Amy Siple <[email protected]>; Derek Hein 1861 <[email protected]>; Julie J.Hein <[email protected]>; John Monroe 1861 <[email protected]>; Merilyn Douglass <[email protected]>; Mitch Depriest 1861 <[email protected]> Subject: re: SB 7 Members of the Senate Judiciary Committee, I sent an email last night, see below, and committed the cardinal sin of not indicating who I represent on the issue. My comments below were on behalf of the Advanced Practice Nurses Association. I apologize for my error. Thanks, Ron Hein On Wednesday, June 03, 2020 8:11 PM, Ronald R. Hein wrote: Date: Wed, 03 Jun 2020 20:11:08 -0500 From: Ronald R. Hein To: Rick Wilborn <[email protected]> cc: Amy Siple <[email protected]>, David Haley <[email protected]>, Dennis Pyle <[email protected]>, Derek Hein 1861 <[email protected]>, Elaine Bowers <[email protected]>, Eric Rucker <[email protected]>, JJH, John Monroe 1861 <[email protected]>, Julia Lynn <[email protected]>, Merilyn Douglass <[email protected]>, Mike Petersen <[email protected]>, Mike Thompson <[email protected]>, .. -

Kansas Senate

In accordance with Kansas Statutes, the following candidates have been recommended by the Committee on Political Education of AFT-Kansas (KAPE COPE) for the 2016 General Election: Please note, where there is no candidate listed, a recommendation has not been made. Kansas Candidates below whose names are highlighted will face a general election opponent. A Union of Candidates below whose names are in blue are recommended Professionals but do NOT have a general election opponent. Kansas State Board of Education: District 2 Chris Cindric (D) District 4 Ann Mah (D) District 6 Aaron Estabrook (I) Deena Horst (R) District 8 District 10 Kansas Senate: SD 1 Jerry Henry (D) SD 15 Dan Goddard (R) SD 27 Tony Hunter (D) SD 2 Marci Francisco (D) Chuck Schmidt (D) SD 28 Keith Humphrey (D) SD 3 Tom Holland (D) SD 16 Gabriel Costilla (D) SD 29 Oletha Faust-Goudeau (D) SD 4 David Haley (D) SD 17 Susan Fowler (D) SD 30 Anabel Larumbe (D) SD 5 Bill Hutton (D) SD 18 Laura Kelly (D) SD 31 Carolyn McGinn (R) SD 6 Pat Pettey (D) SD 19 Anthony Hensley (D) SD 32 Don Shimkus (D) SD 7 Barbara Bollier (R) SD 20 Vicki Schmidt (R) SD 33 SD 8 Don McGuire (D) SD 21 Logan Heley (D) SD 34 SD 9 Chris Morrow (D) Dinah Sykes (R) SD 35 SD 10 Vicki Hiatt (D) SD 22 Tom Hawk (D) SD 36 Brian Angevine (D) SD 11 Skip Fannen (D) SD 23 Spencer Kerfoot (D) SD 37 SD 12 SD 24 Randall Hardy (R) SD 38 SD 13 Lynn Grant (D) SD 25 Lynn Rogers (D) SD 39 John Doll (R) SD 14 Mark Pringle (D) SD 26 Benjamin Poteete (D) SD 40 Alex Herman (D) Kansas House of Representatives: HD 1 HD 43 HD 85 Patty -

1. MINUTES Legislative Post Audit Committee July 31, 2017 Call to Order Welcome by the Chair. the Meeting Was Called to Order By

MINUTES Legislative Post Audit Committee July 31, 2017 Call to Order Welcome by the Chair. The meeting was called to order by Chair Barker at 9:04 a.m. in Room 112-N of the Statehouse. He welcomed new member Representative Dan Hawkins. Committee members present: Representative John Barker, Chair Senator Rob Olson, Vice-Chair Representative Tom Burroughs Senator Elaine Bowers Representative Dan Hawkins Senator Anthony Hensley Representative Don Schroeder Senator Laura Kelly Representative Ed Trimmer Senator Julia Lynn Approval of Minutes. Senator Olson moved approval of the April 28 minutes. Representative Trimmer seconded the motion; motion carried. Presentation of Staff Performance Audits Department of Corrections: Comparing the Merits of Lease and Bond Options for Replacing the Lansing Correctional Facility. This audit was presented by Meghan Flanders, Auditor. Agency officials present to respond to the audit included: Department of Corrections • Joe Norwood, Secretary • Mike Gaito, Director of Capital Improvements • Jimmy Caprio, Legislative Liaison Kansas Development Finance Authority (KDFA) • Jim MacMurray, Senior Vice President, Finance Senator Kelly asked if there was an estimate of the cost of taking the old facility out of service. Ms. Flanders said she would attempt to find out and report back to the committee. Senator Olson made a motion to accept the audit. Representative Burroughs seconded the motion; motion carried. All legislators will receive the audit highlights 1. document and the following committees will be notified that the committee thought the report might be of special interest: House Committees • Appropriations • Corrections and Juvenile Justice • Transportation and Public Safety Budget Senate Committees • Ways and Means • W&M Subcommittee on Corrections Other Committees • Joint Committee on Corrections and Juvenile Justice Oversight • Joint Committee on State Building Construction K-12 Education: Efficiency Audit of the Bucklin School District. -

2015 Corporate Political Contributions Report

Visa Inc. makes political contributions in strict compliance with applicable laws and the Visa Inc. Political Participation, Lobbying, and Contributions Policy. While corporations are not permitted to contribute to U.S. federal political campaigns or to national political parties, they can contribute to state and local candidates in many jurisdictions. Political contributions will not be given in anticipation of, in recognition of, or in return for any official act and corporate funds may not be used for any unlawful, improper or unethical purpose. The following is a list of political contributions Visa made during calendar 2015. The Company makes reasonable efforts to obtain from U.S. trade associations whose annual membership dues exceed $25,000 the portion of such dues that are used for political contributions. None of the organizations surveyed in 2015 reported that any portion of Visa’s dues were used for political expenditures. The political contributions listed are aggregated on a yearly basis and may reflect contributions to multiple campaign committees associated with a single legislator, and also may reflect primary and/or general election contributions. 2015 CORPORATE POLITICAL CONTRIBUTIONS REPORT 2015 U.S. STATE & LOCAL POLITICAL CONTRIBUTIONS Recipient Office Sought Jurisdiction Party Amount Dave Kerner Florida House Candidate District 87 FL House FL D $ 1,000.00 Kelli Stargel Campaign FL Senate FL R $ 1,000.00 John Legg Senate Campaign FL Senate FL R $ 1,000.00 Campaign of Joseph Abruzzo FL Senate FL D $ 1,000.00 Tom Lee Campaign FL Senate FL R $ 5,000.00 Citizens United for Liberty and Freedom FL House FL R $ 5,000.00 Re-Election of Cary Pigman FL House FL R $ 1,000.00 Matt Caldwell Campaign FL House FL R $ 1,000.00 Ross Spano Campaign FL House FL R $ 1,000.00 David Santiago FL House FL R $ 1,000.00 George R.