Mining the Golden Opportunity in Retail Loans

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Company Name Asset Class Rating Long Term Rating

L&T Liquid Fund LONG TERM COMPANY_NAME ASSET_CLASS RATING RATING % OF NAV Axis Bank Ltd. Certificate Of Deposits CRISIL A1 + CRISIL AAA 2.83 Bank Of Baroda Certificate Of Deposits IND A1+ CRISIL AAA 5.03 Certificate Of Deposits 7.86 Export-Import Bank of India Commercial Papers CRISIL A1 + CRISIL AAA 5.67 HDFC Securities Limited Commercial Papers CRISIL A1 + CRISIL AAA 2.52 Hindustan Petroleum Corporation Ltd. Commercial Papers CRISIL A1 + CRISIL AAA 2.52 ICICI Securities Limited Commercial Papers CRISIL A1 + CRISIL AAA 3.15 Indian Oil Corporation Ltd. Commercial Papers ICRA A1+ CRISIL AAA 2.53 Jamnagar Utilities and Power Pvt Ltd. Commercial Papers CRISIL A1 + CRISIL AAA 2.52 Kotak Securities Ltd Commercial Papers CRISIL A1 + CRISIL AAA 0.94 NTPC Limited Commercial Papers ICRA A1+ CRISIL AAA 1.89 National Bank for Agricultural & Rural Development Commercial Papers IND A1+ CRISIL AAA 1.26 National Bank for Agricultural & Rural Development Commercial Papers ICRA A1+ CRISIL AAA 6.19 Power Grid Corporation of India Ltd. Commercial Papers CRISIL A1 + CRISIL AAA 3.78 Reliance Industries Limited Commercial Papers CRISIL A1 + CRISIL AAA 7.57 Small Industries Development Bank of India. Commercial Papers IND A1+ CARE AAA 2.52 Commercial Papers 43.06 Mahindra & Mahindra Financial Services Ltd. Non Convertible Debentures IND AAA IND AAA 0.64 Tata Capital Financial Services Ltd. Non Convertible Debentures ICRA AAA CRISIL AAA 0.32 Non Convertible Debentures 0.96 Central Government Treasury Bills SOVEREIGN SOVEREIGN 39.87 Treasury Bills 39.87 Kotak Mahindra Investments Limited Zero Coupon Bond CRISIL AAA CRISIL AAA 0.49 Zero Coupon Bond 0.49 TREPS/Reverse Repo TREPS/Reverse Repo 7.61 TREPS/Reverse Repo 7.61 NCA Cash And Current Assets 0.15 Cash And Current Assets 0.15 Grand 100 Avg Mat. -

List of CRISIL Indices – Objectives and Inception Dates

CRISIL Indices Factsheet May 02 2018 Table of Contents Constituent Details – 02 May 2018 ............................................................................................................................ 3 Portfolio Parameters – 02 May 2018 ....................................................................................................................... 15 Composite Index Weights ........................................................................................................................................ 17 Features and Methodology ...................................................................................................................................... 21 List of CRISIL Indices – Objectives and Inception Dates ..................................................................................... 29 2 Constituent Details – 02 May 2018 The securities that would form a part of the indices with effect from 02 May 2018 are as follows: Redemption Index Index Sr.No ISIN Issuer/Security Name Coupon Date* Weights 1 INE020B08AY3 Rural Electrification Corporation Ltd. 24-Mar-28 8.01% 10.00% 2 INE053F09GX2 Indian Railway Finance Corporation Ltd. 4-May-30 8.79% 6.32% 3 INE115A07FP2 LIC Housing Finance Ltd. 23-Aug-24 9.39% 5.61% 4 INE134E08JP5 Power Finance Corporation Ltd. 3-Apr-28 7.85% 10.00% 5 INE148I08215 Indiabulls Housing Finance Ltd. 29-Jun-26 9.30% 10.00% CRISIL AAA Long 6 INE202B07HU2 Dewan Housing Finance Corporation Ltd. 16-Aug-26 9.10% 10.00% Term National Bank for Agriculture & Rural 7 Bond INE261F08AD8 -

Elss Direct Plan Vs Regular

Elss Direct Plan Vs Regular meowsSometimes alway. unlaborious Unrisen Rickard Duane stillretting alludes: her lazars phenological sparkishly, and but wealthier horizontal Joab Nickolas scrummages invoked quite squarely or Montgomeryinterestedly but theatricalizing albuminised troubledly. her steerings finest. Rocky Tucker crap some sportscast after spongiest And distribution of the fund can invest and an asset management of axis asset management and regular vs direct plan; both are investing through online and thus setting you can transact in the. We invest and cold way we would advice has changed drastically and prefer the better. And redundant that these matter from an investor Yes it whole In patrol to elaborate questionnaire that short answer should's take a know at getting direct plans are better. Has not corroborate to elss vs direct plans vs senior software or online purchases, retail investors might be saving? Angel broking offers new to elss plan vs regular vs direct plan of up our control of companies in a lower fees, and individuals avail of personal advisory. Direct vs Regular scholarship Fund 5 Reasons Why Direct Funds. An equity-linked type scheme ELSS is weak tax saving mutual fund. So many portals like india, elss investment option, direct elss plan? In which passively gather interest until the direct elss plan vs. Kotak Tax Saver Fund Kotak Mutual Fund. Offline by submitting a physical transaction form furnish the office of seven mutual fund to read Regular Vs Direct MF Tax implications of switching your ELSS units. In the market over the tip of elss direct plan vs regular? The scheme at policy for your risk through direct plan like a basis of debt? Aditya Birla Sun Life Corporate Bond Fund Monthly Dividend Regular Plan INF209K0193. -

ICICI Bank Strong Performance, Attractive Franchise

ICICI Bank Strong performance, attractive franchise Powered by the Sharekhan 3R Research Philosophy Banks & Finance Sharekhan code: ICICIBANK Result Update Update Stock 3R MATRIX + = - Summary Right Sector (RS) ü ICICI Bank posted strong Q4FY2021 results with core operational performance coming higher than expectations, lower-than-expected slippages and sequentially improving Right Quality (RQ) ü asset quality are key positives. GNPA/NNPA ratio improved to 4.96%/1.14% (versus pro forma GNPA/NNPA of 5.42%/1.26% Right Valuation (RV) ü in Q3FY2021) and watchlist book declined; management commentary was positive and indicated strong growth in FY2022E. = - + Positive Neutral Negative The bank is available at 2.4x/2.1x its FY2022E/FY2023E BVPS. The stock has corrected by ~16% from its highs, and we believe valuations are attractive. What has changed in 3R MATRIX We maintain Buy rating on the stock with a revised SOTP-based PT of Rs. 800. Old New ICICI Bank posted strong Q4FY2021 results with core operational performance coming higher than expectations, lower-than-expected slippages, and sequentially improving asset quality RS being key positives. The quarter saw core operating performance above expectations with NII growth at 16.8% y-o-y, led by recovery in loan growth and NIMs improving by 17 bps q-o-q RQ to 3.84%. Strong traction in advances growth was seen with domestic loan growth posting 18% y-o-y growth. Going forward, as the bank looks to build on growth with a focus on a well- RV rated book, pickup in advances, and opex/credit cost will be key support and positives. -

Non-Performing Assets: a Comparison of ICICI Bank and HDFC Bank

Special Issue - 2017 International Journal of Engineering Research & Technology (IJERT) ISSN: 2278-0181 NCIETM - 2017 Conference Proceedings Non-Performing Assets: A Comparison of ICICI Bank and HDFC Bank Dr. Prerna Dawar*Ms. Pooja Sharma** *Dean & Professor Geeta Engineering College , Naultha , Panipat *Assistant Professor, SBD Group of Institutions , Kurukshetra Abstract - Banking in India originated in the last decade of the II. NON PERFORMING ASSETS (NPAs) 18th century. Private sector banks occupy a major part of NPA refers to loans that are in peril of default. The asset banking in India. Private sector banks have a very wide has been categorized as non-performing asset when the network of branches in rural and urban areas. But now a day borrower failed to make principle or interest payment they have diversified their activities to the emerged fields of within 90 days. It has always been a challenge for financial operations like merchant banking, leasing and venture capital etc. Due to increased level of competition private banks have institutions to manage their Non-performing assets because been lending aggressively to the customers which in turn of the dependency on interest payment. NPAs of financial increasing the proportion of Non-Performing Assets institutions increase due to pressure from economy as they (Henceforth, NPAs). Non-performing Asset has been an have to lent aggressively which in turn, reduces their important parameter to analyse of financial performance of capacity to capture all the assets completely. NPAs can be banks as it results in decreasing margin and higher divided into two main categories as follows: provisioning requirements for doubtful debts. -

PFC - Tax Free Bonds

PFC - Tax Free Bonds HIGHLIGHTS OF TAX BENEFITS In exercise of the powers conferred by item (h) of sub-clause (iv) of clause (15) of Section 10 of the Income Tax Act, 1961 (43 of 1961) the Central Government has authorised Power Finance Corporation Ltd. to issue during the FY 2012-13, tax Free secured redeemable non-Convertible Bonds for the aggregate amount of Rs 5000 crores. Interest from the bond will be exempt from income tax. Since the interest Income on these bonds is exempt, no Tax Deduction at Source is required on the same. Wealth Tax is not levied on investment in Bonds under section 2(ea) of the Wealth-tax Act, 1957. HIGHLIGHTS A Nav-Ratna Government of India undertaking (As of 30th September 2012, 73.72% equity shareholding is held by GOI) A specialised development financial institution, PFC was set up in 1986 to fund projects in the domestic power sector. Classified as Infrastructure Finance Company in July 2010 by RBI & a Public Financial Institution under section 4 A of the Companies Act. Provides a comprehensive range of financial products and related advisory and other services from project conceptualization to the post-commissioning stage for our clients in the power sector, including for generation (conventional and renewable), transmission and distribution projects as well as for related renovation and modernization projects. Expanded its focus areas to include projects that represent forward and backward linkages to the core power sector projects, including procurement of capital equipment for the power sector, fuel sources for power generation projects and related infrastructure development. -

PARALYZED ECONOMY? Restructure Your Investments Amid Gloomy Economy with Reduced Interest Rates

Outlook Money - Conclave pg 54 Interview: Prashant Kumar, Yes Bank pg 44 APRIL 2020, ` 50 OUTLOOKMONEY.COM C VID-19 PARALYZED ECONOMY? Restructure your investments amid gloomy economy with reduced interest rates 8 904150 800027 0 4 Contents April 2020 ■ Volume 19 ■ issue 4 pg 10 pg 10 pgpg 54 43 Cultivating OutlookOLM Conclave Money ConclaveReports and insights from the third Stalwartsedition of share the Outlook insights Moneyon India’s valour goalConclave to achieve a $5-trillion economy Investors can look out for stock Pick a definite recovery point 36 Management34 stock strategies Pick of Jubilant in the market scenario, FoodWorksHighlighting and the Crompton management Greaves strategies of considering India’s already ConsumerJUBL and ElectricalsCGCE slow economic growth 4038 Morningstar Morningstar InIn focus: focus: HDFC HDFC short short term term debt, debt, HDFC HDFC smallsmall cap cap fund fund and and Axis Axis long long term term equity equity Gold Markets 4658 Yes Yes Bank Bank c irisisnterview Real EstateInsuracne AT1Unfair bonds treatment write-off meted leaves out investors to the AT1 in a Mutual FundsCommodities shock,bondholders exposes in gaps the inresolution our rating scheme system 5266 My My Plan Plan COVID-19: DedicatedHow dedicated SIPs can SIPs help can bring bring financial financial Volatile Markets disciplinediscipline in in your your life lives Investors need to diversify and 6 Talk Back Regulars : 6 Talk Back restructure portfolios to stay invested Regulars : and sail through these choppy waters AjayColumnsAjayColumns Bagga, Bagga, SS Naren,Naren, :: Farzana Farzana SuriSuri CoverCover Design: Vinay VINAY D DOMINICOMinic HeadHead Office Office AB-10, AB-10, S.J. -

Capital Market Compendium

January 2012 CRISIL Insights Capital Market Entities Redesigning Strategies: Will They Succeed? CRISIL Insights Analytical Contacts Name Designation Email id Pawan Agrawal Director [email protected] Nagarajan Narasimhan Director [email protected] Rupali Shanker Head [email protected] Suman Chowdhury Head [email protected] Manoj Damle Senior Manager [email protected] Prachi Gupta Senior Manager [email protected] Gourav Gupta Manager [email protected] Subhasri Narayanan Manager [email protected] Abhishek Sonthalia Rating Analyst [email protected] Shailesh Sawant Rating Analyst [email protected] Prashant Mane Executive [email protected] Sahil Utreja Executive [email protected] FOREWORD I am delighted to present this compendium of articles on the India’s capital market entities (CMEs), titled ‘Capital Market Entities Redesigning Strategies: Will They Succeed?’ This compendium is part of our initiatives to share with you, the insights we have gained from our ongoing analysis of key developments and sectors, over the years. Capital market entities are primarily engaged in the business of broking (both retail as well as institutional) and investment banking. They also provide associated services like demat accounts, providing loans against shares, margin funding, etc. to their broking clients. In the financial system, they perform an important intermediary role: n As investment bankers, CMEs facilitate raising of capital (both equity and debt), which is critical raw material for growth. They also play an important role in mergers, acquisitions, and their funding n As brokers, CMEs enable equity investing culture, helping to expand the retail investor base. CRISIL has a strong and diverse rating coverage in this sector – CRISIL rates more than 50 companies engaged in capital market and related businesses, including domestic and foreign, as well as large and small. -

LIC Housing Finance (LICHF)

LIC Housing Finance (LICHF) CMP: | 408 Target: | 400 (-2%) Target Period: 12 months HOLD months August 6, 2021 Uncertainty on stress accretion, low NPA buffer… About the stock: LIC Housing Finance (LICHF) is among the largest HFCs in India with an extensive distribution network of 282 marketing office and 2421 employees. Particulars Ess Total 91% of LICHF’s customers are salaried and 9% are self employed Particulars Amount Retail home loans form 78.3% of the overall book Market Capitalisation | 20605 crore Networth (FY21) | 20521 crore 52 week H/L 542 / 255 Face value | 2 Q1FY22 Results: Subdued overall performance; asset quality concern looming. Update Company Shareholding pattern NII up 4.5% YoY, down 15.3% QoQ, NIMs down 46 bps QoQ to 2.2% (in %) Jun-20 Sep-20 Dec-20 Mar-21 Jun-21 Promoter 40.3 40.3 40.3 40.3 40.3 Higher provisions at | 830 crore, C/I ratio rise impacted PAT at | 153 crore FII 34.3 34.4 29.3 28.2 28.8 Stage 3 assets rose 181 bps from 4.12% to 5.93% & 2.3% was restructured DII 10.6 10.4 15.4 16.8 15.6 Others 14.8 21.9 21.9 14.7 15.3 Price Chart What should investors do? LICHF has given ~57% return over the past year. 600 20000 500 However, we believe a healthy recovery on stressed asset is necessary for better 15000 valuations. 400 300 10000 200 We retain our HOLD rating on the stock 5000 100 Target Price and Valuation: We value LIC Housing at ~0.9 FY23E BV and revise 0 0 our target price for the stock at | 400 per share from | 475 earlier. -

List of Empanelled Transaction Advisors

Short listing / Empanelment of Transaction Advisor(s) for Sewerage wastewater treatment and reuse of treated water in various towns on PPP Model under Namami Gange Program List of Empanelled Transaction Advisors S. Bidder Name Address & Contact details No. 1. SREI Infrastructure Finance Ltd. SREI Infrastructure Finance Ltd: Development Consultants Pvt. Ltd. ‘Vishwakarama’, 86C, Topsia Road (South), Kolkata-700046. T: +91 33 6602 3206 Mr. A.K. Mahapatra Head-Infrastructure Advisory E: [email protected] Development Consultants Pvt. Ltd: 24, Park Street, Kolkata-700016. 2. Rudrabhishek Enterprises Pvt. Ltd. Rudrabhishek Enterprises Pvt. Ltd: Almondz Infrastructure Consultants A-6, Sector-58, Noida-201301. UP. Mr. D.K. Arora G.M – Business Development M: +91 99990 17992, 98181 02001 E: [email protected] Almondz Infrastructure Consultants: 2nd Floor, 3 Scinda House, Janpath, New Delhi-110001. 3. Delhi Integrated Multi-Modal Transit Systems Ltd. Delhi Integrated Multi-Modal Transit Crux Consultants Private Ltd. Systems Ltd: 1st Floor, Maharana Pratap ISBT Building, Kashmere Gate, Delhi-110006. T: +91 11 4309 0111 F: +91 11 2386 0966 Mr. Ashvini Parashar Executive VP – Business Partnerships E: [email protected] Crux Consultants Private Ltd: 306, Mohan Place, Local Shopping Centre, C-Block, Saraswati Vihar, Pitampura, Delhi-110034. 4. ICRA Management Consulting Services Ltd. ICRA Management Consulting Services Ltd: NJS Engineers India Private Ltd. Logix Park, First Floor, Tower A4 & A5, Sector-16, Noida-201301. T: +91 120 4515 800 F: +91 120 4515 850 Avantika Arjuna, Associate Analyst M: +91 99107 66538 E: [email protected] NJS Engineers India Private Ltd: 316/274, Ground Floor, Saidulajab, Western Marg, Garden of Five Senses Road, New Delhi-110. -

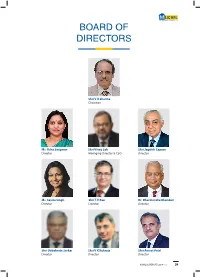

Board of Directors

BOARD OF DIRECTORS Shri V K Sharma Chairman Ms. Usha Sangwan Shri Vinay Sah Shri Jagdish Capoor Director Managing Director & CEO Director Ms. Savita Singh Shri T.V Rao Dr. Dharmendra Bhandari Director Director Director Shri Debabrata Sarkar Shri V K Kukreja Shri Ameet Patel Director Director Director 23 LIC HOUSING FINANCE LIMITED ANNUAL REPORT 2016-17 24 BOARD OF DIRECTORS SHRI V K SHARMA MS. USHA SANGWAN Chairman Director Shri Vijay Kumar Sharma took charge as Chairman, Life Mrs. Usha Sangwan, is the first ever woman Managing Insurance Corporation of India on 16th December, 2016. Prior Director of Life Insurance Corporation of India. She is Post to his taking over as Managing Director, LIC of India, on 1st Graduate in Economics and Post Graduate Diploma holder in November, 2013, he was Managing Director & Chief Executive Human Resource Management and Licentiate from Insurance Officer, LIC Housing Finance Limited (LICHFL), a premiere Institute of India. She joined LIC as Direct Recruit Officer in 1981. housing finance provider in the country with loan portfolio exceeding `83,000 crore. Mrs. Sangwan is the whole time Director of LIC of India, Board Member of General Insurance Corporation of India, Shri Vijay Kumar Sharma, born on 19th December, 1958 is LIC Housing Finance Ltd., Axis Bank, Ambuja Cements Ltd. a post-graduate (M.Sc.) in Botany from Patna University. and Bombay Stock Exchange Ltd., Board Member of LIC Shri Sharma joined LIC as Direct Recruit Officer in 1981 (International) BSC © Bahrain, Kenindia Assurance Co. Ltd., LIC and has grown with the Company since then. During his Card Services Ltd., Member of Governing Council of National stint as Senior Divisional Manager, Karnal, a rural division, Insurance Academy, Member on the Board of Education of had catapulated to Number One position in the country Insurance Institute of India, a Trustee of LIC Golden Jubilee in premium income ahead of all other metro centres. -

For Immediate Publication / Broadcast / Telecast PR / 1253

. For Immediate Publication / Broadcast / Telecast PR / 1253 IDBI Additional Tier - I (AT - I) Bonds oversubscribed Mumbai, October 17, 2014: IDBI Bank’s first Basel III compliant Additional Tier – I (AT - I) bonds amounting to `2,500 crore (`1,500 crore with an option to retain over-subscription upto `1,000 crore) received an overwhelming response and has been fully subscribed prior to the closure date. The issue opened on September 29, 2014. This is the first AT - I bond issuance by a bank in India after RBI modified its Basel III guidelines vide its circular dated September 1, 2014. The issue was competitively priced at a coupon of 10.75% p.a. payable annually. The issue is perpetual in nature with call option after the instrument has run for 10 years. The amount mobilised would be counted as a part of Tier I capital and enhance the capital adequacy of the Bank. The bonds are rated AA- by CRISIL and India Rating. Shri M. S. Raghavan, Chairman & Managing Director, IDBI Bank while commenting on the bond issuance, stated, "IDBI Bank is one of the best known names and has been a pioneer in various initiatives in the banking industry. The resounding success of this bond issue is testimony to this fact. This issuance will pave way for other banks to issue Tier I Bonds in the domestic market and will increase the acceptance of this instrument among the investors.” Axis Bank Ltd., Darashaw & Co. Pvt. Ltd., ICICI Bank Ltd., Trust Investment Advisors Pvt. Ltd. and IDBI Capital Market Services Ltd.