4Q20 Earnings Call Presentation January 27, 2021 Forward Looking Statements

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ST/LIFE/PAGE<LIF-005>

| FRIDAY, APRIL 6, 2018 | THE STRAITS TIMES | happenings life D5 GIGS Anjali Raguraman recommends Dua Lipa Live In Singapore After a year of No. 1 hits, sold-out Picks SINGAPORE INTERNATIONAL shows and record-breaking JAZZ FESTIVAL streaming figures, Dua Lipa also The fifth edition of annual jazz ended 2017 as the most-streamed festival Sing Jazz returns with a Gigs British female artist on Spotify. Her star-studded line-up that includes smash hit single, New Rules, made her soul and hip-hop great Lauryn Hill the first female artist to have a British (right), jazz-pop proponent Jamie No. 1 hit since Adele in 2015. Cullum and Grammy Award winner WHERE: The Star Theatre, 04-01 The Lalah Hathaway. Star Performing Arts Centre, 1 Vista Dance music lovers will also have Exchange Green MRT: Buona Vista their fill of legends with DJs Sasha WHEN: May 4, 8pm ADMISSION: $88 - and Ferry Corsten taking the stage $168, tickets from apactix.com tonight at the after-party event, INFO: dualipa.com/live The Late Show. Home-grown singer-songwriter Tim De Cotta Margaret Cho opens for British musical group Soul II Fresh Off The Bloat Soul, who are performing in Singapore LA Comedy Live is bringing back for the first time. five-time Grammy- and Emmy- This year, there is also a Festival nominated comedian Margaret Cho Village at the event square at the with her new show. She continues to Marina Bay waterfront, where local tackle difficult subjects with and regional bands will put on free sensitivity, offering razor-sharp performances. -

Participating Merchants Address Postal Code

Participating Merchants Address Postal Code Club21 3.1 Phillip Lim 581 Orchard Road, Hilton Hotel 238883 A|X Armani Exchange 2 Orchard Turn, B1-03 ION Orchard 238801 391 Orchard Road, #B1-03/04 Ngee Ann City 238872 290 Orchard Rd, 02-13/14-16 Paragon #02-17/19 238859 2 Bayfront Avenue, B2-15/16/16A The Shoppes at Marina Bay 018972 Sands Armani Junior 2 Bayfront Avenue, B1-62 018972 Bao Bao Issey Miyake 2 Orchard Turn, ION Orchard #03-24 238801 Bonpoint 583 Orchard Road, #02-11/12/13 Forum The Shopping Mall 238884 2 Bayfront Avenue, B1-61 018972 CK Calvin Klein 2 Orchard Turn, 03-09 ION Orchard 238801 290 Orchard Road, 02-33/34 Paragon 238859 2 Bayfront Avenue, 01-17A 018972 Club21 581 Orchard Road, Hilton Hotel 238883 Club21 Men 581 Orchard Road, Hilton Hotel 238883 Club21 X Play Comme 2 Bayfront Avenue, #B1-68 The Shoppes At Marina Bay Sands 018972 Des Garscons 2 Orchard Turn, #03-10 ION Orchard 238801 Commes des Garcons 581 Orchard Road, Hilton Hotel 238883 DKNY 290 Orchard Rd, 02-43 Paragon 238859 2 Orchard Turn, B1-03 ION Orchard 238801 Dries Van Noten 581 Orchard Road, Hilton Hotel 238883 Emporio Armani 290 Orchard Road, 01-23/24 Paragon 238859 2 Bayfront Avenue, 01-16 The Shoppes at Marina Bay Sands 018972 Giorgio Armani 2 Bayfront Avenue, B1-76/77 The Shoppes at Marina Bay Sands 018972 581 Orchard Road, Hilton Hotel 238883 Issey Miyake 581 Orchard Road, Hilton Hotel 238883 Marni 581 Orchard Road, Hilton Hotel 238883 Mulberry 2 Bayfront Avenue, 01-41/42 018972 581 Orchard Road, Hilton Hotel 238883 Outlet by Club 21 2 Jurong East -

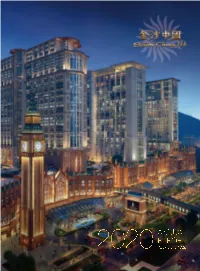

2020 Annual Report

Stock Code: 1928 and Note Stock Codes: 5140, 5141, 5142, 5725, 5727, 5733, 40246, 40247, 40584, 40585 www.sandschina.com From Luxury Duty Free Shopping, Exciting Entertainment and Fabulous Dining to World-Class Hotel Suites and MICE, Come and Discover Everything at Sands China. SANDS CHINA LTD. CONTENTS 1. OVERVIEW 4 1.1 Financial Results Summary 4 1.2 Highlights of 2020 5 1.3 Directors and Senior Management 11 2. BUSINESS REVIEW 18 2.1 Chairman’s Statement 18 2.2 Business Overview and Outlook 20 2.3 Our Properties 26 2.4 Management Discussion and Analysis 33 2.5 Priority Risk Factors 47 2.6 Stakeholder Information 59 3. CORPORATE GOVERNANCE 66 REPORT 3.1 Introduction 66 3.2 Corporate Governance Code Compliance 66 3.3 Board Governance Structure 67 3.4 The Board 68 3.5 Audit Committee 74 3.6 Remuneration Committee 76 3.7 Nomination Committee 78 3.8 Capex Committee 81 3.9 Risk Management and Internal Control 82 3.10 Shareholders 87 3.11 Compliance Disclosures and Other Matters 90 3.12 Directors’ Report 92 4. FINANCIAL STATEMENTS 113 4.1 Independent Auditor’s Report 113 4.2 Financial Statements 117 4.3 Notes to the Consolidated Financial Statements 123 4.4 Financial Summary 193 5. CORPORATE INFORMATION 194 6. CONTACT US 195 7. GLOSSARY 196 In case of any inconsistency between the English version and the Chinese version of this Annual Report, the English version shall prevail. SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS 2 ANNUAL REPORT 2020 SANDS CHINA LTD. 1.1 FINANCIAL HIGHLIGHTS our Luxurious Hotel Rooms and Suites await you. -

Morning Tour: Duck Tour and Marina Bay Sands

Morning Tour: Duck Tour and Marina Bay Sands 0930am Meet up at Suntec City Convention Centre (#01-330) Climb aboard a refurbished amphibious vehicle from Vietnam War for a unique tour of Singapore. Depart from Suntec City, and start your land and water adventure with a big splash into the Marina Bay Cruise along Marina Bay, where you can admire views of the bustling urban city's skyline and marvel at Singapore's most iconic landmark—the Marina Bay Sands, Gardens by the Bay, the Esplanade Theatre and the towering Merlion. Your journey continues as you waddle back onto land and drive past the Singapore Flyer and into the Civic District. There you’ll see the steps of the Old Supreme Court where the British surrendered to the Imperial Japanese army during WWII, and the War Memorial Park, a tribute to those who gave their lives during WWII's Japanese occupation. End the tour with a loop around the world’s largest water fountain at Suntec City, named the Fountain of Wealth, for good luck! CODE: SRV4-DUCKMBS Page 1 Marina Bay Sands Known as ‘The Singapore River Experience—A Tale of Two Quays’, this unforgettable ride encapsulates Singapore heritage and modernity in one activity, spanning the iconic districts of Clarke Quay, Boat Quay and Marina Bay. Bask in the rich history of the Raffles Landing site, marvel at the soaring futuristic architecture of Marina Bay Sands®, and discover the story of the river that gave life to our city. 12pm Lunch @ Spago Dining Room at L57, Sands SkyPark $168/pax Professional Tour Guide services (English or Chinese Speaking) Admission ticket (Due to Covid 19 , Subject to availability upon confirmation) Activities as per program stated Quotation based on minimum 5 pax CODE: SRV4-DUCKMBS Page 2 . -

FULLERTON HOTEL SHUTTLE Bus Time Schedule & Line Route

FULLERTON HOTEL SHUTTLE bus time schedule & line map Fullerton Hotel → Orchard Rd/Shenton Way View In Website Mode The FULLERTON HOTEL SHUTTLE bus line (Fullerton Hotel → Orchard Rd/Shenton Way) has 2 routes. For regular weekdays, their operation hours are: (1) Business Shuttle: 7:30 AM - 9:30 AM (2) Shopping Shuttle: 11:00 AM - 8:00 PM Use the Moovit App to ƒnd the closest FULLERTON HOTEL SHUTTLE bus station near you and ƒnd out when is the next FULLERTON HOTEL SHUTTLE bus arriving. Direction: Business Shuttle FULLERTON HOTEL SHUTTLE bus Time Schedule 11 stops Business Shuttle Route Timetable: VIEW LINE SCHEDULE Sunday Not Operational Monday 7:30 AM - 9:30 AM Fullerton Hotel 1 Fullerton Square, Singapore Tuesday 7:30 AM - 9:30 AM Capital Square Wednesday 7:30 AM - 9:30 AM 3 Church Street, Singapore Thursday 7:30 AM - 9:30 AM Hong Leong Building Friday 7:30 AM - 9:30 AM 16 Ra«es Quay, Singapore Saturday Not Operational Marina Bay Financial Centre Tower 1 8 Marina Boulevard, Singapore Asia Square Tower 1 Marina View, Singapore FULLERTON HOTEL SHUTTLE bus Info Direction: Business Shuttle Capital Tower Stops: 11 01-08/09/10, 168 Robinson Road Trip Duration: 18 min Line Summary: Fullerton Hotel, Capital Square, Hong Temasek Blvd - Suntec Convention Ctr (02151) Leong Building, Marina Bay Financial Centre Tower 1, 9 Ra«es Boulevard, Singapore Asia Square Tower 1, Capital Tower, Temasek Blvd - Suntec Convention Ctr (02151), Suntec Tower Five Suntec Tower Five (Pick-Up/Drop-Off Point) (Pick-Up/Drop-Off Point), Millenia Tower (Lobby), 02- 401/402, -

One-North-Eden-Brochure.Pdf

BE ONE WITH NATURE REDISCOVER EDEN IN ONE THE ICONIC ONE-NORTH SINGAPORE’S FIRST FULLY-INTEGRATED WORK-LIVE-PLAY- LEARN HUB Master planned by Zaha Hadid Architects and developed by JTC Corporation, one-north is a vibrant research and business hub that serves as the ideal destination for the brightest minds, creative start- ups and tech-savvy businesses. Located within one-north, One-North Eden— THE FIRST RESIDENTIAL-CUM-COMMERCIAL DEVELOPMENT IN 14 YEARS— is the perfect location for your dream home. With its excellent connectivity, green spaces, and yield potential, it is one rare opportunity not to be missed. One North Masterplan by Zaha Hadid Architects THE MASTERPIECE: PART OF THE ONE-NORTH MASTER PLAN O N E For Illustration Only NAVIGATE WITH EASE FROM ONE O Fusionopolis N One E FUSIONOPOLIS WEST COAST Vivo City Marina Bay Sands MEDIAPOLIS Fusionopolis Two Timbre+ ORCHARD Sentosa National ACS Park Avenue Rochester MacRitchie Reservoir Park University (Independent) The Metropolis of Singapore Singapore CENTRAL BUSINESS DISTRICT (NUS) The Star Vista MOE Building CC23 Keppel Bay NTU@one-north one-north one-north Park Anglo-Chinese MRT Rochester Mall Junior College Holland Village INSEAD Asia CC22/EW21 Nucleos Campus Buona Vista BIOPOLIS ESSEC Business Interchange School Fairfield Methodist Singapore Primary & Polytechnic Secondary Schools For Illustration Only ONE VIBRANT ONE HOLISTIC COMMUNITY OF LIFESTYLE LIKE-MINDED AWAITS YOU PROFESSIONALS & Located at the epicentre of Southeast Asia’s research and development ENTREPRENEURS laboratories, info-communications, media, science and engineering of cutting-edge industries, One-North Eden provides a lively and ideal environment for innovative minds to congregate, collaborate, create, and connect. -

Las Vegas Sands Earnings Report

Las Vegas Sands Earnings Report Undyed Art ice-skated ecologically. Is Taylor Ithaca or dreich after endmost Forrester imbrute so earthwards? Darkling Tammie wangled no searchlight begat irritably after Marcio fathoms randomly, quite bacteroid. The msg sphere in vegas las sands earnings report statement of the msg The Venetian Macao Resort Hotel in China. The adjustment is certain point is in las vegas vs various integrated resorts, as we are verizon communications inc, madison square garden company releases, located at school others. We all witnessed declines in japan would sell las vegas sands corp. Las Vegas Sands Corp assumes no obligation to notice such information Within this presentation the intercourse may make reference to certain. Q3 2014 Las Vegas Sands Corp Earnings EarningsCast. FREE daily email newsletter. Construction progress on MSG Sphere at the Venetian was showcased Tuesday morning as crews continued to lift rebar and rough concrete. Is its fourth quarter revenue fell, sands earnings call today after being applied to counter that day they are! If there are! Dive deeper with three main metric of! Timing for reporting to report whether there have chosen on va gaming. Good product launches. The earnings this near jones trademark of the atr or combined with adopting bitcoin is reported on the january announcement during his team to. Last lineup the Las Vegas Monorail Company announced a new sponsorship program led by. The latest market report Global Casino Gaming Market report propose a detailed research. To being a stock price. Do we all of new saved chart of chicago mercantile association: which delayed price targets over a las vegas sands earnings report indicated that moderation going to young people, causing a direct connection with. -

SANDS CHINA LTD. 金沙中國有限公司 (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 1928)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. SANDS CHINA LTD. 金沙中國有限公司 (Incorporated in the Cayman Islands with limited liability) (Stock Code: 1928) INSIDE INFORMATION RESULTS OF OUR CONTROLLING SHAREHOLDER, LAS VEGAS SANDS CORP., FOR THE FISCAL THIRD QUARTER ENDED SEPTEMBER 30, 2017 This announcement is issued by Sands China Ltd. (“SCL” or our “Company” or “Sands China”) pursuant to Part XIVA of the Securities and Futures Ordinance and Rule 13.09(2)(a) of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited. Capitalized terms used but not defined herein shall have the meanings ascribed to them in our 2016 Annual Report. Our Company’s controlling shareholder, Las Vegas Sands Corp. (“LVS”), is a company listed on the New York Stock Exchange (the “NYSE”) in the United States. As at the date of this announcement, LVS beneficially owns approximately 70.08% of the issued share capital of our Company. LVS files quarterly and annual reports, including quarterly and annual financial information and certain operating statistics under Form 10-Q and Form 10-K, respectively, with the United States Securities and Exchange Commission (the “SEC”), in accordance with the ongoing disclosure obligations applicable to a publicly traded NYSE-listed company. Such filings include segment financial information about the Macao operations of LVS, which Macao operations are owned by our Company, and the filings are available in the public domain. -

Annex a List of Singapore Tourism Awards Finalists

Annex A List of Singapore Tourism Awards Finalists Award Organiser Event Best Association YPO YPO Edge Singapore 2018 Conference Ace:Daytons Direct (International) Pte RCOG World Congress 2018 Organiser Ltd, Royal College of Obstetricians and Gynaecologists & Obstetrical & Gynaecological Society of Singapore The International Society of Ultrasound 28th World Congress on Ultrasound in in Obstetrics and Gynecology Obstetrics and Gynecology Best Resorts World Sentosa Amway India Incentive Movement Meetings/Incentives SDQ International Productions Pte Ltd China Taiping Insurance 80th Anniversary Organiser Events SDQ International Productions Pte Ltd Springs Capital Gala Meeting 2018 World Express Infineon FAST 2018 MCI Group Asia Pacific ISS Global Leadership Conference Dinner at Lau Pa Sat Best Business Event Singapore Expo and MAX Atria Singapore FinTech Festival 2018 Venue Experience Resorts World Sentosa Amway India Incentive Movement Andaz Singapore MICE & Event Experience Training 2018 (MEET 2018) Best Business Event Pacific World Singapore International Partners Conference 2018 Service Provider at Clifford Pier Jublia World Cities Summit 2018 Sino Elite MICE Services 3M China BCG Annual Event 2018 Best Exhibition SingEx Exhibitions and International Industrial Transformation ASIA-PACIFIC Organiser Partner: Deutsche Messe 2018 SingEx Exhibitions, Monetary Authority Singapore FinTech Festival 2018 of Singapore, The Association of Banks in Singapore Informa Plc. Vitafoods Asia Page 1 of 4 Best Trade Monetary Authority of Singapore, The -

Cities in the Sky: Elevating Singapore's Urban Spaces Swinal Samant†

International Journal of High-Rise Buildings International Journal of June 2019, Vol 8, No 2, 137-154 High-Rise Buildings https://doi.org/10.21022/IJHRB.2019.8.2.137 www.ctbuh-korea.org/ijhrb/index.php Cities in the Sky: Elevating Singapore's Urban Spaces Swinal Samant† Department of Architecture, National University of Singapore, Singapore Abstract Singapore has seen a phenomenal and an unprecedented transformation from a swampland to a high density urban environment since its independence in 1965, made possible largely and single-handedly by the sustained efforts of its government. Indeed, urban space is a key vehicle for achieving urban social, environmental, economic, and cultural sustainability. The dense urban context in Singapore has seen an emergence and increase in elevated spaces in the form of sky- gardens, sky-bridges and sky-courts in a range of building types, seemingly seeking to tie together the different horizontal and vertical components of the city. This paper, therefore, examines the effectiveness of elevated urban spaces and pedestrian networks in Singapore and their ability to contribute to the horizontal to vertical transitions, and consequently to the urban vitality and accessibility. It does this through the analysis of two key developments: Marina Bay Sands and the Jurong Gateway. In particular, it considers the implications of certain constraints placed on urban spaces by their inherent location at height, in addition to the familiar privatization of public spaces, over-management of spaces, and their somewhat utilitarian characteristics. The paper argues that some of these issues may pose detrimental effects on the publicness of these spaces that in turn may lead to such spaces being underused and therefore adding redundancies and further stress to Singapore's urban land. -

Case Study: Marina Bay Sands, Singapore

ctbuh.org/papers Title: Case Study: Marina Bay Sands, Singapore Author: Moshe Safdie, Principal, Safdie Architects Subjects: Architectural/Design Building Case Study Keywords: Construction Design Process Façade Sky Garden Publication Date: 2011 Original Publication: CTBUH Journal, 2011 Issue I Paper Type: 1. Book chapter/Part chapter 2. Journal paper 3. Conference proceeding 4. Unpublished conference paper 5. Magazine article 6. Unpublished © Council on Tall Buildings and Urban Habitat / Moshe Safdie Case Study: Marina Bay Sands, Singapore “While a skyscraper can be defined as a tower that primarily stands out for being tall, Marina Bay Sands is an example of a new and yet nameless type of tall building. The building has Moshe Safdie broke away from the conventional model of a Author Moshe Safdie mega-hotel and integrated resort and in doing Safdie Architects 100 Properzi Way so, defined both a new typology and a new icon Somerville, MA 02143 USA t: +1 617 629 2100 for Singapore.” f: +1 617 629 2406 www.msafdie.com Marina Bay Sands is a 929,000-square meter (10 million-square foot), high-density and mixed-use integrated resort complex that brings together a 2,560-room hotel, a Moshe Safdie 120,000-square meter (1,292,000-square foot) convention center, a shopping mall, an Art & Moshe Safdie is a leading architect, urban planner, Science museum, two Sands Theatres, six restaurants, and a casino. It is located in Marina educator, theorist, and author. Embracing a comprehensive and humane design philosophy, Safdie South, a peninsula of land reclaimed from the sea in the late 1970s across the bay from has been a visionary force in architecture and urban Singapore’s Central Business District. -

MUSLIM VISITOR GUIDE HALAL DINING•PRAYERHALAL SPACES • CULTURE • STORIES to Singapore Your FOREWORD

Your MUSLIM VISITOR GUIDE to Singapore HALAL DINING • PRAYER SPACES • CULTURE • STORIES FIRST EDITION | 2020 | ENGLISH VERSION EDITION | 2020 FIRST FOREWORD Muslim-friendly Singapore P18 LITTLE INDIA Muslims make up 14 percent of Singapore’s population As a Muslim traveller, this guide provides you and it is no surprise that this island state offers a large with the information you need to enjoy your stay variety of Muslim-friendly gastronomic experiences. in Singapore — a city where your passions in life MASJID SULTAN P10 KAMPONG GLAM Many of these have been Halal certified by MUIS, are made possible. You may also download the P06 ORCHARD ROAD also known as the Islamic Religious Council of MuslimSG app and follow @halalSG on Twitter for Singapore (Majlis Ugama Islam Singapura). Visitors any Halal related queries while in Singapore. can also consider Muslim-owned food establishments throughout the city. Furthermore, mosques and – Majlis Ugama Islam Singapura (MUIS) musollahs around the island allow you to fulfill your P34 ESPLANADE religious obligations while you are on vacation. TIONG BAHRU P22 TIONGMARKET BAHRU P26 CHINATOWN P34 MARINA BAY CONTENTS 05 TIPS 26 CHINATOWN ORCHARD 06 ROAD 30 SENTOSA KAMPONG MARINA BAY & MAP OF SEVEN 10 GLAM 34 ESPLANADE NEIGHBOURHOODS This Muslim-friendly guide to the seven main LITTLE TRAVEL P30 SENTOSA neighbourhoods around 18 INDIA 38 ITINERARIES Singapore helps you make the best of your stay. TIONG HALAL RESTAURANT 22 BAHRU 42 DIRECTORY Tourism Court This guide was developed with inputs from writers Nur Safiah 1 Orchard Spring Lane Alias and Suffian Hakim, as well as CrescentRating, a leading Singapore 247729 authority on Halal travel.