Quarterly Market Commentary December 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Teksavvy Solutions Inc. Consultation on the Technical and Policy

TekSavvy Solutions Inc. Reply Comments in Consultation on the Technical and Policy Framework for the 3650-4200 MHz Band and Changes to the Frequency Allocation of the 3500-3650 MHz Band Canada Gazette, Part I, August 2020, Notice No. SLPB-002-20 November 30, 2020 TekSavvy Solutions Inc. Reply Comments to Consultation SLPB-002-20 TABLE OF CONTENTS A. Introduction ____________________________________________________________ 1 B. Arguments for option 1 and against option 2 _________________________________ 1 a. Contiguity ______________________________________________________________ 1 b. Availability of ecosystem in the 3900: impacts on viability_________________________ 3 c. Moratorium ____________________________________________________________ 4 d. Arguments for Improvements to Option 1 _____________________________________ 4 C. 3800 MHz Auction _______________________________________________________ 5 a. Value _________________________________________________________________ 5 b. Procompetitive Measures _________________________________________________ 5 c. Tier 4 and 5 Licensing Area ________________________________________________ 6 TekSavvy Solutions Inc. Page 1 of 6 Reply Comments to Consultation SLPB-002-20 A. INTRODUCTION 1. TekSavvy Solutions Inc. (“TekSavvy”) is submitting its reply comments on ISED’s “Consultation on the Technical and Policy Framework for the 3650-4200 MHz Band and Changes to the Frequency Allocation of the 3500-3650 MHz Band”. 2. TekSavvy reasserts its position in favour of Option 1 in that Consultation document, and its strong opposition to Option 2, as expressed in its original submission. TekSavvy rejects Option 2 as disastrous both for WBS service providers’ ongoing viability and availability of broadband service to rural subscribers. 3. TekSavvy supports Option 1, wherein WBS Licensees would be allowed to continue to operate in the band of 3650 to 3700 MHz indefinitely as the only option that enables continued investment in rural broadband networks and continued improvement of broadband services to rural subscribers. -

Cologix Torix Case Study

Internet Exchange Case Study The Toronto Internet Exchange (TorIX) is the largest IX in Canada with more than 175 peering participants benefiting from lower network costs & faster speeds The non-profit Toronto Internet Exchange (TorIX) is a multi-connection point enabling members to use one hardwired connection to exchange traffic with 175+ members on the exchange. With peering participants swapping traffic with one another through direct connections, TorIX reduces transit times for local data exchange and cuts the significant costs of Internet bandwidth. The success of TorIX is underlined by its tremendous growth, exceeding 145 Gbps as one of the largest IXs in the world. TorIX is in Cologix’s data centre at 151 Front Street, Toronto’s carrier hotel and the country’s largest telecommunications hub in the heart of Toronto. TorIX members define their own routing protocols to dictate their traffic flow, experiencing faster speeds with their data packets crossing fewer hops between the point of origin and destination. Additionally, by keeping traffic local, Canadian data avoids international networks, easing concerns related to privacy and security. Above: In Dec. 2014, TorIX traffic peaked above 140 Gbps, with average traffic hovering around 90 Gbps. Beginning Today Launched in July 1996 Direct TorIX on-ramp in Cologix’s151 Front Street Ethernet-based, layer 2 connectivity data centre in Toronto TorIX-owned switches capable of handling Second largest independent IX in North America ample traffic Operated by telecom industry volunteers IPv4 & IPv6 address provided to each peering Surpassed 145 Gbps with 175+ peering member to use on the IX participants, including the Canadian Broke the 61 Gbps mark in Jan. -

BCE Inc. 2015 Annual Report

Leading the way in communications BCE INC. 2015 ANNUAL REPORT for 135 years BELL LEADERSHIP AND INNOVATION PAST, PRESENT AND FUTURE OUR GOAL For Bell to be recognized by customers as Canada’s leading communications company OUR STRATEGIC IMPERATIVES Invest in broadband networks and services 11 Accelerate wireless 12 Leverage wireline momentum 14 Expand media leadership 16 Improve customer service 18 Achieve a competitive cost structure 20 Bell is leading Canada’s broadband communications revolution, investing more than any other communications company in the fibre networks that carry advanced services, in the products and content that make the most of the power of those networks, and in the customer service that makes all of it accessible. Through the rigorous execution of our 6 Strategic Imperatives, we gained further ground in the marketplace and delivered financial results that enable us to continue to invest in growth services that now account for 81% of revenue. Financial and operational highlights 4 Letters to shareholders 6 Strategic imperatives 11 Community investment 22 Bell archives 24 Management’s discussion and analysis (MD&A) 28 Reports on internal control 112 Consolidated financial statements 116 Notes to consolidated financial statements 120 2 We have re-energized one of Canada’s most respected brands, transforming Bell into a competitive force in every communications segment. Achieving all our financial targets for 2015, we strengthened our financial position and continued to create value for shareholders. DELIVERING INCREASED -

2010-Annual-Report.Pdf

The Best 2010 ANNUAL REPORT Pick Organically Grown Strong Yields Highly Productive An outstanding record of distribution growth and value-creation. 6,651 Enterprise Value ($ Millions) 5,372 233 3,984 3,922 202 187 2,510 172 161 Annual Distributions Paid ($ Millions) 06 07 08 09 10 Table of Contents 08 Financial and Operating Highlights 14 Management’s Discussion and Analysis 123 Five-Year Historical Summary 09 Five-Year Growth Summary 83 Consolidated Financial Statements 124 Board of Directors 10 President’s Letter 87 Notes to Consolidated Financial Statements 126 Offi cers and Corporate Information Payout ratio Distribution growth per unit over 10 years Total return in 2010 Why are investors picking Inter Pipeline for their portfolio? It’s simple, really. Average Annual Total Return We’ve generated outstanding total returns over Unit price appreciation plus distributions the past decade, and have steadily increased 1 year ..................................46.4% cash distributions. 3 year ..................................31.6% We‘ve done it by focusing our investments on 5 year ..................................21.4% long-life energy infrastructure assets that deliver 7 year ..................................21.8% sustainable and predictable cash fl ow. Our assets are 10 year ................................22.2% managed safely and effi ciently by strong operational teams, and are primarily supported by long-term contracts with blue-chip customers. We’re well positioned to capture further opportunities by leveraging our competitively positioned infrastructure assets. We have a large inventory of organic growth projects under development which will provide steady cash fl ow in the years to come. That’s the investment value we create. 2010 ANNUAL REPORT 1 Our presence in the Canadian oil sands is unmatched, with three key petroleum transportation systems serving the heart of the Athabasca and Cold Lake oil sands regions. -

![List of Securities Eligible for Reduced Margin [Effective from November 24, 2020 Until Replaced by a Subsequent List]](https://docslib.b-cdn.net/cover/8637/list-of-securities-eligible-for-reduced-margin-effective-from-november-24-2020-until-replaced-by-a-subsequent-list-738637.webp)

List of Securities Eligible for Reduced Margin [Effective from November 24, 2020 Until Replaced by a Subsequent List]

Attachment #1 List of Securities Eligible for Reduced Margin [effective from November 24, 2020 until replaced by a subsequent list] Compiled by the Investment Industry Regulatory Page 1 of 21 September 30, 2020 Organization of Canada IIROC Notice 20-0225 Rules Notice – Technical – List of Securities Eligible for Reduced Margin List of Securities Eligible for Reduced Margin Attachment #1 Description Symbol Description Symbol ABSOLUTE SOFTWARE J ABT AUTOMOTIVE PPTY UN APR.UN BARRICK GOLD CORP ABX APTOSE BIOSCIENCES APS AIR CANADA VOTE & VV AC ALGONQUIN PWR & UTIL AQN ATCO LTD. CL I NV ACO.X ALGONQUIN PWR A PR AQN.PR.A ATCO LTD. CL II ACO.Y ALGONQUIN PWR D PR AQN.PR.D AUTOCANADA INC. ACQ ARGONAUT GOLD INC. J AR ANDREW PELLER A NV ADW.A AECON GROUP INC. ARE ANDREW PELLER LTD. B ADW.B ARC RESOURCES LTD. ARX AGNICO EAGLE MINES AEM ACUITYADS HLDGS J AT AG GROWTH INT'L INC. AFN ATS AUTOMATION TOOL ATA AGF MANAGEMENT B NV AGF.B ALIMENTATION CL A MV ATD.A ALAMOS GOLD INC. J AGI ALIMENTATION CL B SV ATD.B ATRIUM MTG INVEST AI ATLANTIC POWER ATP ALTUS GROUP LIMITED AIF ARITZIA INC. SV ATZ AIMIA INC. AIM AURYN RESOURCES J AUG AIMIA INC. SER 1 PR AIM.PR.A A&W REVENUE RYLTY UN AW.UN AIMIA INC. SER 3 PR AIM.PR.C ARTIS REIT UN AX.UN ALTAGAS LTD. ALA ARTIS REIT SER A PR AX.PR.A ALTAGAS LTD SR A PR ALA.PR.A ARTIS REIT SER E PR AX.PR.E ALTAGAS LTD SR B PR ALA.PR.B ARTIS REIT SER I PR AX.PR.I ALTAGAS LTD SR E PR ALA.PR.E ALEXCO RESOURCE J AXU ALTAGAS LTD SR G PR ALA.PR.G BADGER DAYLIGHTING BAD ALTAGAS LTD SR H PR ALA.PR.H BROOKFLD ASSET A LV BAM.A ALTAGAS LTD SR I PR ALA.PR.I BROOKFLD ASSET PR 32 BAM.PF.A ALTAGAS LTD SR K PR ALA.PR.K BROOKFLD ASSET PR 34 BAM.PF.B ALTAGAS LTD C PR USF ALA.PR.U BROOKFLD ASSET PR 36 BAM.PF.C ALTIUS MINERALS CORP ALS BROOKFLD ASSET PR 37 BAM.PF.D ALTIUS MINERALS PR ALS.PR.A BROOKFLD ASSET PR 38 BAM.PF.E ALITHYA GROUP J A SV ALYA BROOKFLD ASSET PR 40 BAM.PF.F AMEX EXPL IN AMX BROOKFLD ASSET PR 42 BAM.PF.G ANDLAUERHLTHCR GRPSV AND BROOKFLD ASSET PR 44 BAM.PF.H ALLIED PROP. -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

Morning News Call Canada

MORNING NEWS CALL Powered by Re uters Canada Edition Monday, April 26, 2021 TOP NEWS • Frustrated Canada presses White House to keep Great Lakes oil pipeline open Canada is pushing on several diplomatic fronts against the U.S. state of Michigan's efforts to close a cross-border oil pipeline, the second such dispute since Joe Biden became U.S. president in January, complicating the governments' efforts to work together to lower carbon emissions. • Shippers push for CP Railway to win bidding war for Kansas City Southern North America's freight rail customers, from grain shippers to logistics companies, are pushing for Canadian Pacific Railway to win a bidding war for Kansas City Southern over rival Canadian National Railway, eyeing stronger competition and swifter service. • Moderna vaccine to be reviewed for WHO emergency listing on April 30 - WHO spokesman Moderna's COVID-19 vaccine will be reviewed on April 30 by technical experts for possible WHO emergency-use listing, a World Health Organization spokesman told Reuters. • Health Canada finds Astrazeneca COVID-19 vaccines from Baltimore plant safe, of high quality Canada's health department said on Sunday the 1.5 million doses of the Astrazeneca COVID-19 vaccine imported from Emergent BioSolutions' Baltimore facility were safe and met quality specifications. • Canadian government to intervene to end potential Montreal port strike The Canadian government will intervene to end a potential strike at the country's second-largest port, the labour minister said on Sunday, as the clock ticked down to a walkout by Montreal dockworkers. BEFORE THE BELL Canada's main stock index futures fell, weighed by a drop in oil prices, as investors awaited a first-quarter earnings update from Canadian National Railway later in the day. -

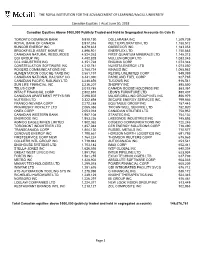

THE ROYAL INSTITUTION for the ADVANCEMENT of LEARNING/Mcgill UNIVERSITY

THE ROYAL INSTITUTION FOR THE ADVANCEMENT OF LEARNING/McGILL UNIVERSITY Canadian Equities │ As at June 30, 2018 Canadian Equities Above $500,000 Publicly Traded and Held in Segregated Accounts (in Cdn $) TORONTO DOMINION BANK 9,910,190 DOLLARAMA INC 1,209,739 ROYAL BANK OF CANADA 8,917,316 KELT EXPLORATION LTD 1,188,512 SUNCOR ENERGY INC 6,879,833 QUEBECOR INC 1,183,053 BROOKFIELD ASSET MGMT INC 4,896,921 ENERFLEX LTD 1,150,883 CANADIAN NATURAL RESOURCES 4,524,263 FIRST QUANTUM MINERALS LTD 1,145,213 CGI GROUP INC 4,482,828 MULLEN GROUP LTD 1,083,045 CCL INDUSTRIES INC 4,351,728 ENCANA CORP 1,073,348 CONSTELLATION SOFTWARE INC 4,212,781 NUVISTA ENERGY LTD 1,073,050 ROGERS COMMUNICATIONS INC 3,788,734 KINAXIS INC 1,065,983 ALIMENTATION COUCHE-TARD INC 3,581,197 RECIPE UNLIMITED CORP 949,389 CANADIAN NATIONAL RAILWAY CO 3,441,390 PARKLAND FUEL CORP 927,785 CANADIAN PACIFIC RAILWAY LTD 3,240,856 TUCOWS INC 916,541 SUN LIFE FINANCIAL INC 3,236,207 SHOPIFY INC 895,850 TELUS CORP 3,013,785 CANADA GOOSE HOLDINGS INC 883,361 INTACT FINANCIAL CORP 2,802,815 LEON'S FURNITURE LTD 880,407 CANADIAN APARTMENT PPTYS REI 2,498,502 MAJOR DRILLING GROUP INTL INC 856,979 NUTRIEN LTD 2,322,898 SECURE ENERGY SERVICES INC 799,566 FRANCO-NEVADA CORP 2,272,288 EQUITABLE GROUP INC 787,443 PRAIRIESKY ROYALTY LTD 2,065,386 TRICAN WELL SERVICE LTD 782,920 ONEX CORP 2,053,018 CANADIAN UTILITIES LTD 758,952 CANADIAN WESTERN BANK 1,987,108 STANTEC INC 754,132 ENBRIDGE INC 1,953,226 LASSONDE INDUSTRIES INC 745,893 AGNICO EAGLE MINES LIMITED 1,902,362 COGECO COMMUNICATIONS -

Stoxx® Canada Total Market Mid Index

STOXX® CANADA TOTAL MARKET MID INDEX Components1 Company Supersector Country Weight (%) EMERA Utilities Canada 3.01 BAUSCH HEALTH Health Care Canada 2.71 WSP GLOBAL Construction & Materials Canada 2.59 Teck Resources Ltd. Cl B Basic Resources Canada 2.48 Canadian Tire Corp. Ltd. Cl A Retail Canada 2.36 ALGONQUIN POWER & UTILITIES Utilities Canada 2.34 CAE Industrial Goods & Services Canada 2.27 CCL INDS.'B' Industrial Goods & Services Canada 2.12 CANADIAN APARTMENT PROP REIT Real Estate Canada 2.11 Kinross Gold Corp. Basic Resources Canada 2.11 TFI INTERNATIONAL Industrial Goods & Services Canada 2.04 LIGHTSPEED POS Technology Canada 1.97 AIR CANADA Travel & Leisure Canada 1.95 Cameco Corp. Energy Canada 1.93 INTER PIPELINE Energy Canada 1.83 TOROMONT INDUSTRIES Industrial Goods & Services Canada 1.81 TOURMALINE OIL Energy Canada 1.81 GILDAN ACTIVEWEAR Consumer Products & Services Canada 1.77 Blackberry Ltd Technology Canada 1.72 RITCHIE BROS.AUCTIONEERS (NYS) Consumer Products & Services Canada 1.68 WEST FRASER TIMBER Basic Resources Canada 1.62 FIRSTSERVICE Real Estate Canada 1.62 NORTHLAND POWER Utilities Canada 1.56 PAN AMER.SILV. (NAS) Basic Resources Canada 1.55 LUNDIN MINING Basic Resources Canada 1.53 ALTAGAS Utilities Canada 1.51 KEYERA CORP Energy Canada 1.51 IA FINANCIAL CORP Insurance Canada 1.51 EMPIRE 'A' Personal Care, Drug & Grocery Stores Canada 1.49 DESCARTES SYSTEMS GROUP Technology Canada 1.44 RIOCAN REIT.TST. Real Estate Canada 1.44 ONEX Financial Services Canada 1.44 TMX GROUP Financial Services Canada 1.41 ARC RESOURCES LTD Energy Canada 1.29 Element Fleet Management Corp. -

Bank of Montreal Canadian Q-Model® Principal at Risk Notes Series 17A

Bank of Montreal Canadian Q-Model® Principal at Risk Notes Series 17A Summary of Investment Portfolio as at December 1, 2016 Product Details Current Portfolio Holdings* Objective Ticker Company Name Composite Rank Sector Weight The Notes are designed for equity AC Air Canada 17 Industrial 4.79% investors seeking a return based on a ACO.X ATCO Ltd. I 8 Utilities 4.57% portfolio of Canadian large-cap stocks selected using the BMO Capital Markets BCE BCE Inc. 31 Communications 4.46% Quantitative Factor Model. BNS Scotiabank 1 Financial 5.12% BTO B2Gold Corp. 16 Basic Materials 4.43% Series 17A - Regular Accounts CM CIBC 4 Financial 5.13% Asset Class Canadian Equity ENF Enbridge Income Fund Holdings 7 Energy 4.70% Structure Debt Security FTS Fortis Inc. 24 Utilities 4.55% Discipline Quantitative IAG Industrial Alliance 13 Financial 5.47% IGM IGM Financial Inc. 20 Financial 4.99% Strategy Top 20/35 (Total Return) IPL Inter Pipeline Ltd. 12 Energy 4.83% Holdings 20 stocks LNR Linamar Corp. 15 Industrial 5.14% Code JHN 8040 MFC Manulife Financial Corp. 11 Financial 6.18% MG Magna International Inc. 5 Consumer (Cyclical) 5.12% Daily NAV $148.14 NA National Bank 2 Financial 5.44% Current Yield 3.32% PWF Power Financial 18 Financial 5.31% ETC Nil RY Royal Bank of Canada 14 Financial 5.21% SLF Sun Life Financial 3 Financial 5.72% Issue Date December 21, 2011 TD Toronto-Dominion Bank 9 Financial 5.27% Maturity Date December 21, 2016 THO Tahoe Resources 10 Basic Materials 3.55% Program Fee 1.75% per annum * Portfolio Holdings as of December 9, 2016 -

FERIQUE Canadian Equity Fund

C1 Contents C1 C2 SHORT-TERM-INCOME CANADIAN-BOND GLOBALLY-DIVERSIFIED-INCOME CONSERVATIVE MODERATE BALANCED GROWTH AGGRESSIVE-GROWTH CANADIAN-DIVIDEND-EQUITY CANADIAN-EQUITY AMERICAN-EQUITY EUROPEAN-EQUITY 20 ASIAN-EQUITY EMERGING-MARKETS INTERIM WORLD-DIVIDEND-EQUITY MANAGEMENT C4 REPORT of Fund Performance for the period ended June 30, 2020 EQUITY FUNDS FÉRIQUE Canadian Equity Fund This Interim Management Report of Fund Performance contains financial highlights but does not contain the complete interim or annual financial statements of the Fund. You can get a copy of the Interim Financial Statements at your request, and at no cost, by calling our Advisory Services at 514-788-6485 (toll-free 1-800-291-0337), by writing to us at Gestion FÉRIQUE, Place du Canada, 1010 de La Gauchetière Street West, Suite 1400, Montréal, Québec H3B 2N2, or by visiting our website at ferique.com or SEDAR at sedar.com. Unitholders may also contact us using one of these methods to request a copy of the Fund’s proxy voting policies and procedures, proxy voting disclosure record and quarterly portfolio disclosure. C2 There may be management fees and expenses associated with an investment in the Funds. Management expense ratios vary from one year to another. Please read the Prospectus before investing. Mutual funds are not guaranteed or covered by the Canada Deposit Insurance Corporation or another government deposit insurer. Their values fluctuate frequently and past performance may not be repeated. FÉRIQUE Funds are distributed by Services d’investissement FÉRIQUE since July 1, 2013 and used to be by National Bank Securities Inc., until June 30, 2013. -

Bell V. Cogeco: Unfair Competition – the “Best Internet Experience” Results in an Unfavorable Judicial Experience

Bell v. Cogeco: Unfair competition – the “best Internet experience” results in an unfavorable judicial experience October 28, 2016 Author Alain Y. Dussault Partner, Lawyer Partner, and Trademark Agent In the field of telecommunications, it is not uncommon to see competing Internet service providers engage in advertising war campaigns in order to attract new customers, particularly in this highly competitive market due to the small number of competitors. Competitors are prepared to do anything to attract consumers, perhaps even making their offered products and services appear more attractive than they are. It is in this context that the Superior Court of Ontario issued, in Bell Canada v. Cogeco Cable Canada, 2016 ONSC 6044 1, September 20, 2016, an interlocutory injunction against Cogeco Cable Canada, in order to cease any use of the advertising phrase “the best Internet experience in your neighborhood ” in its advertisements, on the grounds of false and misleading representations. Facts and background of the case Bell Canada (hereinafter “Bell”) and Cogeco Cable Canada (hereinafter “Cogeco”) are two competing Internet providers in Ontario. However, Bell and Cogeco do not use the same technology to provide their services to consumers. Specifically, Cogeco uses “Hybrid fiber coaxial cable” technology (Cable / HFC), while Bell uses “Digital subscriber lines” (DSL) technology. In addition to DSL, Bell also uses “Fiber to the home” (FTTH) through the entire province of Ontario while Cogeco offers this technology only in new residential neighborhoods. In August 2016, Cogeco announced its new brand identity as part of its advertising campaign for the Copyright (c) Lavery, de Billy, S.E.N.C.R.L.