2019 Diversity Disclosure Practices: Women in Leadership Roles at TSX

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1 2 March 2021 Flutter Entertainment

2 March 2021 Flutter Entertainment plc - 2020 Preliminary Results Transformational year for Group; Earnings ahead of expectations Flutter Entertainment plc (the “Group”) announces preliminary results for year ended 31 December 2020. Reported1 Pro forma2 2020 2019 2020 2019 CC3 £m £m YoY % £m £m YoY % YoY % Group revenue4 4,398 2,140 +106% 5,264 4,144 +27% +28% Adjusted5 Group EBITDA6 excluding US 1,037 462 +125% 1,401 1,170 +20% +23% Adjusted Group EBITDA 889 425 +109% 1,231 1,089 +13% +16% Profit before tax 1 136 -99% Earnings per share7 29.3p 180.2p -84% Adjusted earnings per share 402.7p 298.4p +35% 496.6p 415.7p +19% Net debt at year end8 2,814 265 Operational highlights • Transformational year for Group - Unparalleled scale and diversification achieved following merger with The Stars Group, Inc (“TSG”) - Accelerated buy-out of minority shareholders in FanDuel at compelling valuation - Reinforced balance sheet to support investment and growth • Excellent momentum with 19% growth in recreational players9 across Group - Acceleration of channel shift from retail to online and increased share of entertainment spend • Further investment in safer gambling initiatives to ensure sustainable growth - Enhanced predictive technology; increase in safer gambling tool usage by customers - Advocating a customer driven approach to affordability • Merger integration progressing well - Australian integration complete, PokerStars strategy in place and core momentum maintained - Annualised cost synergies now expected to be £170m, up from £140m previously -

DFA Canada Canadian Vector Equity Fund - Class a As of July 31, 2021 (Updated Monthly) Source: RBC Holdings Are Subject to Change

DFA Canada Canadian Vector Equity Fund - Class A As of July 31, 2021 (Updated Monthly) Source: RBC Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of -

The Stars Group and FOX Sports Announce Historic U.S. Media and Sports Wagering Partnership

The Stars Group and FOX Sports Announce Historic U.S. Media and Sports Wagering Partnership May 8, 2019 Toronto and Los Angeles, May 8, 2019 – The Stars Group Inc. (Nasdaq: TSG)(TSX: TSGI) and FOX Sports, a unit of Fox Corporation (Nasdaq: FOXA, FOX), today announced plans to launch FOX Bet, the first-of-its kind national media and sports wagering partnership in the United States. The Stars Group and FOX Sports have entered a long-term commercial agreement through which FOX Sports will provide The Stars Group with an exclusive license to use certain FOX Sports trademarks. The Stars Group and FOX Sports expect to launch two products in the Fall of 2019 under the FOX Bet umbrella. One will be a nationwide free-to-play game, awarding cash prizes to players who correctly predict the outcome of sports games. The second product, which will be named FOX Bet, will give customers in states with regulated betting the opportunity to place real money wagers on the outcome of a wide range of sporting events in accordance with the applicable laws and regulations. In addition to the commercial agreement of up to 25 years and associated product launches, Fox Corporation will acquire 14,352,331 newly issued common shares in The Stars Group, representing 4.99% of The Stars Group’s issued and outstanding common shares, at a price of $16.4408 per share, the prevailing market price leading up to the commencement of exclusive negotiations. The Stars Group currently intends to use the aggregate net proceeds of approximately $236 million for general corporate purposes and to prepay outstanding indebtedness on its first lien term loans. -

FTSE Publications

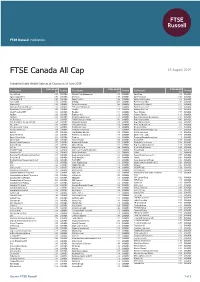

2 FTSE Russell Publications 19 August 2019 FTSE Canada All Cap Indicative Index Weight Data as at Closing on 28 June 2019 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Aecon Group 0.05 CANADA Element Fleet Management 0.19 CANADA Onex Corp 0.3 CANADA Agnico Eagle Mines 0.73 CANADA Emera Inc 0.58 CANADA Open Text Corp 0.65 CANADA Air Canada Cl B 0.25 CANADA Empire Co Cl A 0.26 CANADA Osisko Gold Royalties 0.1 CANADA Alacer Gold 0.06 CANADA Enbridge 4.35 CANADA Pan American Silver 0.16 CANADA Alamos Gold 0.14 CANADA Encana Corporation 0.46 CANADA Paramount Res Class A 0.02 CANADA Algonquin Power & Utilities Co 0.36 CANADA Endeavour Mining Corp. 0.07 CANADA Parex Resources Inc 0.14 CANADA Alimentation Couche-Tard B 1.63 CANADA Enerflex 0.07 CANADA Parkland Fuel Corp. 0.28 CANADA Allied Properties REIT 0.24 CANADA Enerplus 0.11 CANADA Pason Systems 0.07 CANADA AltaGas. 0.25 CANADA Enghouse Sys 0.06 CANADA Pembina Pipeline 1.14 CANADA Aphria Inc 0.09 CANADA Ensign Energy Services 0.03 CANADA Peyto Exploration & Development 0.03 CANADA Arc Resources 0.1 CANADA Fairfax Financial Holdings 0.81 CANADA Power Corp Canada 0.46 CANADA Artis Real Estate Investment Trust 0.07 CANADA Finning International 0.18 CANADA Power Financial Corp 0.32 CANADA Atco Class I 0.15 CANADA First Capital Realty 0.16 CANADA PrairieSky Royalty Ltd 0.2 CANADA ATS Automation Tooling 0.07 CANADA First Majestic Silver 0.08 CANADA Precision Drilling 0.03 CANADA Aurora Cannabis Inc 0.38 CANADA First National Financial 0.02 CANADA Premium Brands Holdings Corp 0.12 CANADA B2Gold 0.18 CANADA First Quantum Minerals 0.39 CANADA Pretium Resources 0.1 CANADA Bank of Montreal 2.93 CANADA FirstService Corporation 0.18 CANADA Quebecor Inc. -

United States Securities and Exchange Commission Form S-4 Newmont Goldcorp Corporation Newmont Usa Limited

Table of Contents As filed with the Securities and Exchange Commission on June 28, 2019 Registration No. 333- UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM S-4 REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 NEWMONT GOLDCORP CORPORATION NEWMONT USA LIMITED (Exact name of Registrant as specified in its charter) (Exact name of Registrant as specified in its charter) Delaware Delaware (State or other jurisdiction of incorporation or organization) (State or other jurisdiction of incorporation or organization) 1040 1040 (Primary Standard Industrial Classification Code Number) (Primary Standard Industrial Classification Code Number) 84-1611629 13-2526632 (I.R.S. Employer Identification No.) (I.R.S. Employer Identification No.) 6363 South Fiddler’s Green Circle 6363 South Fiddler’s Green Circle Greenwood Village, Colorado 80111 Greenwood Village, Colorado 80111 (303) 863-7414 (303) 863-7414 (Address, including zip code, and telephone number, including (Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices) area code, of Registrant’s principal executive offices) Nancy Lipson Executive Vice President and General Counsel Newmont Goldcorp Corporation 6363 South Fiddler’s Green Circle Greenwood Village, Colorado 80111 (303) 863-7414 (Name, address, including zip code and telephone number, including area code, of agent for service) With copies to: Laura M. Sizemore David M. Johansen White & Case LLP 1221 Avenue of the Americas New York, New York 10020 (212) 819-8200 Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable following the effective date of this registration statement. If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. -

Quarterly Commentary 18 AM Canadian Equity Portfolio March 31, 2020

Quarterly Commentary 18 AM Canadian Equity Portfolio March 31, 2020 18 AM Canadian Equity Highlights The 18 AM Canadian Equity portfolio is uniquely positioned, with 50/50 exposure to two focused style portfolios, Offence (growth and momentum) and Defence (income, quality and low risk). We manage the Offence and Defence styles independently, using 15-stock portfolios of companies that exhibit attractive balance sheet and income statement fundamentals (factors) of the respective style. As of the close of 2019, the 18 AM Canadian Equity portfolio reached a 6-year track record. Over that period, the portfolio realized objectives by: ✓ Outperforming the benchmark S&P/TSX Composite (TSX) in 5 of 6 calendar years, and overall since inception before fees. ✓ Experiencing a lower risk profile versus the TSX, evidenced by having both a lower volatility, and by losing less during calendar years when the index declined. ✓ Maintaining a fundamental profile that is superior to the benchmark across a variety of impactful factors as intended within each style, such as: i) a lower Price/Earnings ratio, ii) higher Return on Equity, iii) better Earnings Growth and iv) enhanced Yield. Details of the portfolio and style performance are shown in the following table. Since Inception Performance Q1 2020 1 Year 3 Year 5 Year Return Volatility Offence* -25.6% -20.0% -3.6% -2.1% 0.2% 14.1% Defence* -15.9% -7.7% 0.9% 4.1% 6.3% 10.0% Portfolio** -20.8% -13.9% -1.1% 1.1% 3.3% 11.1% Benchmark -20.9% -14.2% -1.9% 0.9% 2.8% 11.4% *The chart depicts performance data for the style portfolios managed by 18 AM and is for information purposes only. -

Women in Leadership at S&P/Tsx Companies

WOMEN IN LEADERSHIP AT S&P/TSX COMPANIES Women in Leadership at WOMEN’S S&P/TSX Companies ECONOMIC Welcome to the first Progress Report of Women on Boards and Executive PARTICIPATION Teams for the companies in the S&P/TSX Composite Index, the headline AND LEADERSHIP index for the Canadian equity market. This report is a collaboration between Catalyst, a global nonprofit working with many of the world’s leading ARE ESSENTIAL TO companies to help build workplaces that work for women, and the 30% Club DRIVING BUSINESS Canada, the global campaign that encourages greater representation of PERFORMANCE women on boards and executive teams. AND ACHIEVING Women’s economic participation and leadership are essential to driving GENDER BALANCE business performance, and achieving gender balance on corporate boards ON CORPORATE and among executive ranks has become an economic imperative. As in all business ventures, a numeric goal provides real impetus for change, and our BOARDS collective goal is for 30% of board seats and C-Suites to be held by women by 2022. This report offers a snapshot of progress for Canada’s largest public companies from 2015 to 2019, using the S&P/TSX Composite Index, widely viewed as a barometer of the Canadian economy. All data was supplied by MarketIntelWorks, a data research and analytics firm with a focus on gender diversity, and is based on a review of 234 S&P/TSX Composite Index companies as of December 31, 2019. The report also provides a comparative perspective on progress for companies listed on the S&P/TSX Composite Index versus all disclosing companies on the TSX itself, signalling the amount of work that still needs to be done. -

Mid-Year 2020 Metro Vancouver Office Market Report

Mid-Year 2020 Office Market Report Metro Vancouver, BC metro Vancouver Pandemic impact fails to materialize as downtown vacancy & absorption trends Vacancy Rate remains tight amid record-low suburban vacancy 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% redictions that the impacts from a global mid-year 2019, but was still less than the 5.1% 366,304 Ppandemic would fundamentally alter recorded just 24 months ago. Regional vacancy 2020F 4% the dynamics of Metro Vancouver’s office is forecasted to decline to 4% by year-end market failed to materialize at mid-year 2020 2020 due to a profound lack of new supply -26,019 as vacancy in the suburbs reached record both downtown and in the suburbs as well Mid-2020 4.7% 7.3% lows and downtown Vancouver continued to as a strong track record of preleasing. The post one of the tightest office vacancy rates latter helps insulate against notable spikes in 478,555 vacancy when new supply is added and force 2019 4.4% in North America despite an initial wave of sublease vacancy. New office development many existing businesses to consider existing activity throughout the region remained on head lease space or, at least in the case of 2018 5.1% 1,802,623 schedule with only minor delays due in large downtown Vancouver, the rising availability of part to the provincial government designating sublease opportunities. Downtown Vancouver construction as an essential service in its and, to a lesser extent, the suburbs, were 2017 8% 1,223,656 initial response to COVID-19 in March 2020. -

Manica Gautam Moved to Vancouver to Launch a Venture Capital Fund

FINANCIAL STAKES Manica Gautam moved to Vancouver to launch a venture capital fund. Now she helps run the Houssian family's investment firm B.C.’S MOST INFLUENTIALmoney WOMEN on the To mark our fifth annual tribute to female leaders making a difference, we celebrate women in finance or Kai Li, a finance professor atUBC Sauder School of Business, it’s become a familiar sight. In a typical year, about 50 percent of the school’s commerce undergraduates are female. But as third- year specialization approaches, relatively few women choose finance. Li, who teaches a course that readies students for Fthe investment banking industry, thinks there’s both a supply and a demand problem. “People who I invite as guest speakers, there are very few female role models, unfortunately,” she says. At the same time, investment banking’s long hours may not appeal to women seeking work-life balance. Despite such challenges, this province is home to a remarkable group of women working in financial roles. For our fifth annual B.C.’s Most Influential Women fea- ture, we again sought the advice of an expert panel (see p.47)—three of whose five members are women mak- ing their mark in finance—to identify names worthy of recognition. We defined finance broadly, to encompass every- one from CFOs and entrepreneurs to bank executives and money managers. As usual, our list is representa- tive, not exhaustive or definitive. The goal is to celebrate the achievements of female leaders at different career >>> BY NATHAN CADDELL, NICK ROCKEL + FELICITY STONE <<< 28 BCBUSINESS MARCH 2019 LINDSAY SIU ON LOCATION AT INTERNATIONAL PRIVATE VAULTS › MARCH 2019 BCBUSINESS 29 stages, hear some of their stories and show how big an 28 stocks tracked. -

Mount Allison University Endowment Fund Holdings As of December 31, 2017

Mount Allison University Endowment Fund Holdings As of December 31, 2017 Security Name Market Value ($Can) EQUITY HOLDINGS Canadian Holdings 5N PLUS INC $ 155 ABSOLUTE SOFTWARE CORP $ 851 ACADIAN TIMBER CORP $ 302 ADVANTAGE OIL & GAS LTD $ 283,788 AECON GROUP INC $ 1,728 AFRICA OIL CORP $ 684 AG GROWTH INTERNATIONAL INC $ 1,163 AGELLAN COMMERCIAL REAL ESTATE $ 349 AGF MANAGEMENT LTD $ 990 AGNICO-EAGLE MINES LTD $ 427,207 AGT FOOD AND INGREDIENTS INC $ 653 AIMIA INC $ 832 AIR CANADA INC $ 325,411 AIRBOSS OF AMERICA CORP $ 315 ALACER GOLD CORP $ 1,289 ALAMOS GOLD INC $ 2,216 ALAMOS GOLD INC NEW COM CLASS A $ 4,877 ALARIS ROYALTY CORP $ 1,107 ALGOMA CENTRAL CORP $ 330 ALIMENTATION COUCHE-TARD INC $ 98,854 ALIO GOLD INC $ 472 ALLIED PROPERTIES REAL ESTATE INVESTMENT TRUST $ 2,575 ALTIUS MINERALS CORP $ 1,233 ALTUS GROUP LTD/CANADA $ 1,916 ANDREW PELLER LTD $ 1,448 ARGONAUT GOLD INC $ 656 ARTIS REAL ESTATE INVESTMENT TRUST $ 1,539 ASANKO GOLD INC $ 209 ATCO LTD $ 119,947 ATHABASCA OIL COP $ 703 ATS AUTOMATION TOOLING SYSTEMS INC $ 1,769 AURICO METALS INC $ 311 AUTOCANADA INC $ 1,128 AVIGILON CORP $ 1,258 B2GOLD CORP $ 29,898 BADGER DAYLIGHTING LTD $ 1,525 BANK OF MONTREAL $ 725,449 BANK OF NOVA SCOTIA $ 2,019,757 BARRICK GOLD CORP $ 459,749 BAYTEX ENERGY CORP $ 1,213 BCE INC $ 791,441 BELLATRIX EXPLORATION LTD $ 94 BIRCHCLIFF ENERGY LTD $ 1,479 BIRD CONSTRUCTION INC $ 731 1 Mount Allison University Endowment Fund Holdings As of December 31, 2017 Security Name Market Value ($Can) BLACK DIAMOND GROUP LTD $ 95 BLACKBERRY LIMITED $ 151,777 BLACKPEARL RESOURCES INC $ 672 BOARDWALK REAL ESTATE INVESTMENT TRUST $ 1,610 BONAVISTA ENERGY CORP $ 686 BONTERRA ENERGY CORP $ 806 BORALEX INC $ 2,276 BROOKFIELD ASSET MANAGEMENT INCORPORATED $ 672,870 BROOKFIELD INFRASTRUCTURE PARTNERS L.P. -

BCI's 2018 Responsible Investing Annual Report

Responsible Investing Annual Report 2018 British Columbia Investment Management Corporation Table of Contents 2018 Highlights ...............................................................1 Private Markets .............................................................22 To Our Clients ..................................................................2 Mortgage ..................................................................23 BCI and Responsible Investing ......................................3 Real Estate ................................................................24 BCI's Responsible Investing Principles .........................4 Infrastructure & Renewable Resource ..................26 Climate Action .................................................................5 Private Equity ...........................................................27 Climate Action Plan ...................................................6 Corporate Updates & Collaboration ...........................28 Public Markets .................................................................8 Corporate Reporting & Disclosure ........................29 Public Equities ............................................................9 BCI's PRI Involvement .............................................30 Fixed Income ............................................................20 Collaboration ...........................................................32 Appendices ...................................................................34 1 — BCI's Policy Submissions .................................35 -

Week 16 Newsletter

The Sunday Investor Week 16: Ending April 17, 2020 An Introduction For subscribers, new and old. First of all, thank you to all my subscribers, including brand new ones and for those Basic fundamental metrics such as return on equity, price-earnings ratios, free cash who signed up to receive this newsletter almost a year ago when I first started The flow per share, earnings per share, and interest coverage ratios – they’re all freely Sunday Investor. Administering this website has brought out the true passion I available on many websites in the form of stock screeners, but even some of the have for the investing industry and each time I get a new subscriber, it motivates best stock screeners don’t allow you to filter for exactly what you need. me to keep going. I hope you find The Sunday Investor to be a reliable and useful source as you seek to achieve your investment goals. Here you will find the tools you need to keep track of your Canadian and U.S. equity holdings. I maintain a weekly total return tracker for all S&P/TSX Composite Prior to starting my website, I had been noticing a gap in the information the and S&P 500 issuers, and provide several fundamental monthly reports depending average investor has access to on popular investment and financial planning on your investment strategy. I routinely write about the importance of developing websites. While a lot of data is publicly available, many websites do a poor job of a low-volatile portfolio aimed at maximizing the Sharpe Ratio, behavioural finance compiling this information into a format that is easily digestible.