Sime Darby Property Profile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Micare Panel Gp List (Aso) for (October 2020) No

MICARE PANEL GP LIST (ASO) FOR (OCTOBER 2020) NO. STATE TOWN CLINIC ID CLINIC NAME ADDRESS TEL OPERATING HOURS REGION : CENTRAL 1 KUALA LUMPUR JALAN SULTAN EWIKCDK KLINIK CHIN (DATARAN KEWANGAN DARUL GROUND FLOOR, DATARAN KEWANGAN DARUL TAKAFUL, NO. 4, 03-22736349 (MON-FRI): 7.45AM-4.30PM (SAT-SUN & PH): CLOSED SULAIMAN TAKAFUL) JALAN SULTAN SULAIMAN, 50000 KUALA LUMPUR 2 KUALA LUMPUR JALAN TUN TAN EWGKIMED KLINIK INTER-MED (JALAN TUN TAN SIEW SIN, KL) NO. 43, JALAN TUN TAN SIEW SIN, 50050 KUALA LUMPUR 03-20722087 (MON-FRI): 8.00AM-8.30PM (SAT): 8.30AM-7.00PM (SUN/PH): 9.00AM-1.00PM SIEW SIN 3 KUALA LUMPUR WISMA MARAN EWGKPMP KLINIK PEMBANGUNAN (WISMA MARAN) 4TH FLOOR, WISMA MARAN, NO. 28, MEDAN PASAR, 50050 KUALA 03-20222988 (MON-FRI): 9.00AM-5.00PM (SAT-SUN & PH): CLOSED LUMPUR 4 KUALA LUMPUR MEDAN PASAR EWGCDWM DRS. TONG, LEOW, CHIAM & PARTNERS (CHONG SUITE 7.02, 7TH FLOOR WISMA MARAN, NO. 28, MEDAN PASAR, 03-20721408 (MON-FRI): 8.30AM-1.00PM / 2.00PM-4.45PM (SAT): 8.30PM-12.45PM (SUN & PH): DISPENSARY)(WISMA MARAN) 50050 KUALA LUMPUR CLOSED 5 KUALA LUMPUR MEDAN PASAR EWGMAAPG KLINIK MEDICAL ASSOCIATES (LEBUH AMPANG) NO. 22, 3RD FLOOR, MEDAN PASAR, 50050 KUALA LUMPUR 03-20703585 (MON-FRI): 8.30AM-5.00PM (SAT-SUN & PH): CLOSED 6 KUALA LUMPUR MEDAN PASAR EWGKYONGA KLINIK YONG (MEDAN PASAR) 2ND FLOOR, WISMA MARAN, NO. 28, MEDAN PASAR, 50050 KUALA 03-20720808 (MON-FRI): 9.00AM-1.00PM / 2.00PM-5.00PM (SAT): 9.00AM-1.00PM (SUN & PH): LUMPUR CLOSED 7 KUALA LUMPUR JALAN TUN PERAK EWPISRP POLIKLINIK SRI PRIMA (JALAN TUN PERAK) NO. -

Download Brochure

Essence of Impeccable Life Healthy Way of Life Wrapped in natural surroundings, Hijauan Saujana’s striking landscape adds to the joy of living in this serene haven. Break a sweat in the commodious gym amidst green views and tranquil water feature. Take pleasure in the harmonious equilibrium of lifestyle at Hijauan Saujana. Effortless Indulgence Achieving the balance between quiet relaxation and practicality belies the passion which has gone into Hijauan Saujana’s homes. Rejuvenate with the many facilities made available to you. Have a leisurely swim in the pool, or enjoy a good workout with a game of tennis. Take a breather after, and enjoy tea at the cafeteria in the clubhouse. A truly easeful and fulfilling experience. A Sight to Behold Amongst the Necessities Ara Damansara Tropicana Golf & Sime Darby Country Club Medical Centre Ara Damansara Citta Mall Police Station The Japanese School of Symphony Kuala Lumpur House g lan K L ah e b b em Aman Suria u L h ru r a a a B y ay a r Saujana Golf & uh D a Country Club Leb m a n s a J r a a l MBPJ Stadium a - P n u L c a h p o a n n g g a Glenmarie Golf & n Kelana Jaya T e Country Club r b a n g S Saujana Golf & Country Club u b n a ua n Kelab Golf ut g ek Temasya Negara ers a P Subang ay Industrial Park hr bu Le Shah Alam Giant Stadium Tesco Sime Darby Medical Centre Sime Darby Medical Centre Ara Damansara Carrefour Subang Subang Jaya Empire Parade Shopping Citta Mall Gallery Subang Jaya To complement your vivacious lifestyle, Hijauan Saujana offers a variety of amenities, ranging from golf clubs, medical facilities and F&B outlets to supermarkets, malls, sports facilities and education facilities all just a stone’s throw away. -

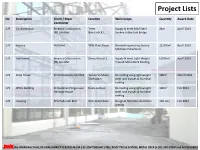

Project Lists

Project Lists No Description Client / Main Location Work Scope Quantity Award Date Contractor 175 Condominium Binastra Construction Treez Supply & erect Mild Steel 24m April’ 2013 (M) Sdn Bhd Bukit Jalil,K.L. Sunken Lobby Link Bridge 174 Factory YKGI Bhd YKGI Plant,Kapar. Dismantling existing factory 12,000m2 April’ 2013 Mild Steel Structures 173 Apartment Binastra Construction Danau Kota,K.L. Supply & erect Light Weight 6,000m2 April’ 2013 (M) Sdn Bhd Truss & Metal Deck Roofing 172 Shop House Penril Datability Sdn Bhd Taman Sri Muda, Re-roofing using light weight 280m2 March’2013 Shah Alam steel roof trusses & fix metal roofing 171 Office Building Perbadanan Pengurusan Kuala Lumpur. Re-roofing using light weight 300m2 Feb’2013 Heritage House steel roof trusses & fix metal roofing 170 Housing KPG Padu Sdn Bhd Nilai,N.Sembilan Design & fabricate steel drain 150 sets Feb’2013 grating DNK, We-MANUFACTURE,DESIGN,FABRICATE&INSTALL M.S & LIGHT WEIGHT STEEL ROOF TRUSS SYSTEM, METAL DECK & CEILLING STRIP and ACCESSORIES Project Lists No Description Client / Main Location Work Scope Quantity Award Date Contractor 169 Steel Support Frame for Archi-Foam Sdn Bhd Mont Kiara Kuala Design & build steel frame 3 mT Dec’2012 Condominium Lumpur support for light weight foam concrete 168 Ware House extension Kara Marketing (M) Sdn Puchong Selangor Design & build mild steel 30 mT Nov’2012 steel structure Bhd structure for warehouse extension 167 Shop Houses 24 Units Hong & Hong Groups Kota Kemuning, Design & build light weight steel 3,350 m2 Oct’2012 Sdn Bhd Shah Alam roof trusses & fax metal deck roofing 166 Workshop Muner Hanafiah Taman Tun Dr. -

Monitoring Slope Condition Using UAV Technology

Civil Engineering and Architecture 7(6A): 1-6, 2019 http://www.hrpub.org DOI: 10.13189/cea.2019.071401 Monitoring Slope Condition Using UAV Technology Norhayati Ngadiman*, Ibrahim Adham Badrulhissham, Mazlan Mohamad, Nurazira Azhari, Masiri Kaamin, Nor Baizura Hamid Department of Civil Engineering, Centre for Diploma Studies (CeDS), Universiti Tun Hussein Onn Malaysia (UTHM), Malaysia Received July 30, 2019; Revised September 30, 2019; Accepted December 10, 2019 Copyright©2019 by authors, all rights reserved. Authors agree that this article remains permanently open access under the terms of the Creative Commons Attribution License 4.0 International License Abstract Slope failure is a serious geologic hazard in there is a wide range in their predictability, rapidity of many countries in the world including Malaysia. In order to occurrence and movement, and ground area affected, all of prevent slope failure, the hazardous symptoms can be which relate directly to the consequences of failure [3]. detected early in slope monitoring process. Nowadays, There are several types of slope failures that can occur slope failure symptoms monitoring has been done by when the shear resistance along the slip plane is exceeded. human by on site observation at the slope spot and it is Slope falls, slope topples, landslides, flows and spreads of dangerous for the human safety. Furthermore, it takes slope are the types of slope failure. These can be caused by longer time to complete the investigation and some of the excessive load imposed at the slope crest or compromised data collected are inaccurate because human view is stability of the slope, and disturbed dimensions of the limited. -

Carey Island Mega Project Will Take Us Higher

Carey Island mega project will take us higher KUALA LUMPUR: The mega port industrial city project at Carey Island will ease the congestion and bottleneck at Port Klang, says Transport Minister Datuk Seri Liow Tiong Lai. He said the port city project, which is still in the planning stages, was a vital part of the Government’s effort to further boost the country’s position as the top hub in the region. “We will have a port city there, not just a port. It will give a boost to Carey Island, and this is our long-term plan,” he told the media at the launch of Pikom’s 9th Leadership Summit 2017, yesterday. The Carey Island Port is a massive port-industrial city project with infrastructure investments of more than RM200bil covering an area of over 100sq km – more than twice the size of Putrajaya. It was announced in January. Liow said the Government must start now or risk being left behind by other ports in the region. “We cannot be satisfied with the current 30 million TEUs (Twenty-foot Equivalent Units) of container cargo. Carey Island will carry an additional capacity of 30 million TEUs. “At the moment, both Northport and Westport can only handle 30 million TEUs so we need to implement the project as soon as possible,” he said. Liow, who is also the National Logistics Task Force chairman, said the development of Carey Island will cover more than 5,000 acres (2,000ha) off Port Klang, aimed at managing the traffic shipment across Asia. “We are hoping to draw cargo shipments from southern Thailand, and Sumatra in Indonesia to strengthen Port Klang’s position as the biggest hub in the region,” he said. -

Persada Brochure 231116.Pdf

230mm x 305mm (cover front) 230mm x 305mm (inside cover front) SETTING BENCHMARKS, ADDING VALUE Bandar Bukit Raja was launched in 2002 with a mixed residential development comprising of affordable, medium and higher end homes. As its planned evolution progresses, Bandar Bukit Raja has become a highly successful and sought-after model township that has now encompassed commercial, retail and Sime Darby Business Park as part of its integration ambition. Its vital position on the Greater Kuala Lumpur footprint ensures its continued importance in location, value and expandibility. Stage 3 (Future Development) A THRIVING COMMUNITY IN KLANG Stage 2 (Future Development) Sprawling over 4,405 acres, Bandar Bukit Raja is an integrated and P self-contained township in Klang. R O P Launched in 2002, it consists not O S only of residential properties but E D also commercial, institutional and W E industrial properties. S 125 acres T Town Park C O A The Bandar Bukit Raja community comes alive S within a well-planned layout and amenities that T E JALAN MERU offer accessible convenience and ease. A strategic Sales Gallery X P location and alluring living standards make it the R E preferred neighbourhood in Klang. S S W A Y NEW NORTH KLANG STRAITS BYPASS Shah Alam 62km 28km 7km 12km 28km 37km *Artist’s impression only COMMUNITY-LIVING FACILITIES Experience it all at Persada, the perfect setting for you and your family at Bandar Bukit Raja. Designed for your ideal living, Persada is the latest 2-storey link home development project by Sime Darby Property in Bandar Bukit Raja, an integrated and self-contained township in Klang. -

Pulih Sepenuhnya Pada 8:00 Pagi, 21 Oktober 2020 Kumpulan 2

LAMPIRAN A SENARAI KAWASAN MENGIKUT JADUAL PELAN PEMULIHAN BEKALAN AIR DI WILAYAH PETALING, GOMBAK, KLANG/SHAH ALAM, KUALA LUMPUR, HULU SELANGOR, KUALA LANGAT DAN KUALA SELANGOR 19 OKTOBER 2020 WILAYAH : PETALING ANGGARAN PEMULIHAN KAWASAN Kumpulan 1: Kumpulan 2: Kumpulan 3: Pulih Pulih Pulih BIL. KAWASAN sepenuhnya sepenuhnya sepenuhnya pada pada pada 8:00 pagi, 8:00 pagi, 8:00 pagi, 21 Oktober 2020 22 Oktober 2020 23 Oktober 2020 1 Aman Putri U17 / 2 Aman Suria / 3 Angkasapuri / 4 Bandar Baru Sg Buloh Fasa 3 / 5 Bandar Baru Sg. Buloh Fasa 1&2 / 6 Bandar Baru Sri Petaling / 7 Bandar Kinrara / 8 Bandar Pinggiran Subang U5 / 9 Bandar Puchong Jaya / 10 Bandar Tasek Selatan / 11 Bandar Utama / 12 Bangsar South / 13 Bukit Indah Utama / 14 Bukit Jalil / 15 Bukit Jalil Resort / 16 Bukit Lagong / 17 Bukit OUG / 18 Bukit Rahman Putra / 19 Bukit Saujana / 20 Damansara Damai (PJU10/1) / 21 Damansara Idaman / 22 Damansara Lagenda / 23 Damansara Perdana (Raflessia Residency) / 24 Denai Alam / 25 Desa Bukit Indah / 26 Desa Moccis / 27 Desa Petaling / 28 Eastin Hotel / 29 Elmina / 30 Gasing Indah / 31 Glenmarie / 32 Hentian Rehat dan Rawat PLUS (R&R) / 33 Hicom Glenmarie / LAMPIRAN A SENARAI KAWASAN MENGIKUT JADUAL PELAN PEMULIHAN BEKALAN AIR DI WILAYAH PETALING, GOMBAK, KLANG/SHAH ALAM, KUALA LUMPUR, HULU SELANGOR, KUALA LANGAT DAN KUALA SELANGOR 19 OKTOBER 2020 WILAYAH : PETALING ANGGARAN PEMULIHAN KAWASAN Kumpulan 1: Kumpulan 2: Kumpulan 3: Pulih Pulih Pulih BIL. KAWASAN sepenuhnya sepenuhnya sepenuhnya pada pada pada 8:00 pagi, 8:00 pagi, 8:00 -

Lifetime Generation Homes

FREEHOLD Lifetime Generation Homes In Nature’s Embrace In close proximity to a 125-acre town park, Azira homes feature a complete array of facilities on top of safety and security with its single entry and exit point. A Beautiful Life Our sustainably designed homes are set in the beautiful scenery of open gardens, promoting a wholesome lifestyle and family bonding. Enjoy a life of smiles and precious moments as you relax in the company of your loved ones. Preserving Memories Azira’s open plan layout is inspired by modern living to suit your lifestyle needs, allowing you to appreciate the things that matter most in life—cherished quality time with your family. Presenting a unique approach to modern urban living with a focus on sustainability, Bandar Bukit Raja homes feature specially crafted design principles to offer an elevation of everyday living. Natural Ventilation Natural Lighting In Harmony With Nature Multi-Generational Homes SITE PLAN Phase 2 Masterplan TO JALAN MERU INDUSTRIAL LOTS INDUSTRIAL LOTS TO PEKAN MERU / PUNCAK ALAM INDUSTRIAL LOTS WEST COAST EXPRESSWAY UNDER CONSTRUCTION JALAN MERU EAST ENTRANCE TOWN PARK CASIRA TOWN PARK TOWN PARK PERSADA JALAN SUNGAI PULOH SOUTH ENTRANCE TO KAPAR Azira 2-Storey Terrace Homes 20’ x 75’ 111 units A1 / A2 - Intermediate Unit E1 / E2 / E3 - End Unit C1 / C2 - Corner Unit Green Area A1/A2 E1/E2 INTERMEDIATE LOT END LOT Built Up: Built Up: 1,901 sqft 2,130 sqft 6100 6100 6700 6700 YARD ROOF YARD ROOF ABOVE BATH 1 BATH 2 ABOVE YARD BATH 1 BATH 2 GUEST GUEST YARD BATH BATH KITCHEN KITCHEN -

Edgeprop Malaysia's Best Managed And

Q1 FY2021 Financial Results Virtual Analyst Briefing | 28 May 2021 | 10.00am Table of Contents Title Page 1. Q1FY2021 Key Highlights (Financial & Operational) 3 – 4 2. Financial Performance for Q1FY2021 5 – 10 3. Operational Performance for Q1FY2021 11 - 16 4. Strategy Moving Forward 17 – 22 5. Investment Proposition 23 – 24 Q1FY2021 Quarterly Result Announcement and Briefing 2 Q1FY2021 Key Highlights (Financial) Resilience demonstrated by its Q1FY2021 financial performance Financial Performance Snapshot Segment Revenue Revenue Reported PBIT Reported PATAMI Leisure Property 14.1 Development RM589.5m RM97.9m RM60.6m (2.4%) 553.0 (93.8%) Financial Position* Investment & Asset Management 22.4 Cash Balances Total Equity (3.8%) Net Assets per RM589.5m RM746.3m RM9,346.4m Share Attributable to Owners of the Company Gross Gearing Net Gearing RM1.35 37.4% 29.5% *as at 31 March 2021 Q1FY2021 Quarterly Result Announcement and Briefing 3 Q1FY2021 Key Highlights (Operational) Sales achievement of RM630.2m, on track to meet FY2021 sales target of RM2.4b Operational Highlights • Robust digital marketing efforts led to healthy take-up rates of >90% for the new • Awards won for Sime Darby Property’s launches signature approach to develop communities • Sales achieved of RM630.2m; revenue visibility with RM1.7b in unbilled sales and with distinctive social and environmental RM0.8b in total bookings features 186 units launched with RM111m GDV in Q1FY2021 RM630.2m sales / 515 units sold (mostly residential landed of not new launches; ~ 29% of value) >90% -

Malaysia Port Klang Power Station Project (Phase 3 /Phase 3-Stage2)

Malaysia Port Klang Power Station Project (Phase 3 /Phase 3-Stage2) External Evaluator: Taro Tsubogo (KRI International Corp.) Tenaga Nasional Berhad1 Field Survey: March, 2006 1. Project Profile and Japan’s ODA Loan Location of the project site Port Klang (Kapar Phase 3) power station 1.1 Background With the high economic growth, energy demand in the Peninsular Malaysia had grown significantly over the last years with an annual growth rate of 11.4% to 3,447 MW in 1990. Although the growth pace was expected to slow down in the future, energy demand was forecasted to reach 10,448 MW in 2000 with an annual growth rate of 10.6%. Since total installed capacity in 1990 was still 4,576 MW, a serious energy shortage was expected to occur in the future. To fill this gap, construction and expansion of power plants was indispensable option. On the other hand, the Malaysian Government carried out “Four fuel diversification strategy” to enhance the use of indigenous resources and reduce petroleum dependency. The Sixth Malaysia Plan (1991-1995) also envisioned to augment gas supply. The project, to construct 1,000 MW multi-fuel fired power plant, was therefore expected to contribute to both increment of supply capacity and diversification of energy source. 1.2 Objectives The project’s objective was to meet the rapidly increasing demand for energy and assure stable energy supply in the Peninsular Malaysia through construction of a thermal power station (known as Kapar Phase 3 Plant) located adjacent to the existing plants in Port Klang area, and thereby contribute to further economic growth and reducing oil dependence of the country. -

Rm 35 (Zone 1)

Caj Penghantaran adalah termasuk kos petrol & tol. Kawasan penghantaran adalah untuk Lembah Klang sahaja. NO Postcodes Kawasan Kos Penghantaran 1 47100 Bandar Puteri/ Taman Puchong Hartamas/ Puchong 2 47120 Aman Putra/ Bandar Bukit Puchong 2 3 47130 D'Island Residence/ Taman Perindustrian Putra/ Puchong 4 47150 Bandar Metro Puchong/ Bistari Residensi/ Puchong 5 47160 Taman Indah Sri Puchong/ Taman Metro Puchong 6 47170 Bandar Puchong Jaya/ IOI 7 47180 Bandar Kinrara/ Puchong RM 35 8 47190 Taman Kandan Baru/ Taman Kinrara/ Puchong 9 47500 Bandar Sunway/ Subang Jaya (ZONE 1) 10 47600 Taman Perindustrian UEP/ USJ Sentral/ Subang Jaya 11 47610 Subang Jaya - USJ 5 - 8 12 47620 Subang Jaya - USJ 9 - 11 13 47630 Taman Indah Subang UEP/ Subang Jaya 14 40400 Jalan Ampang/ Shah Alam 15 40460 Bukit Kemuning/ Shah Alam 16 47650 Universiti Teknologi Mara (UiTM) Shah Alam 17 57000 Bandar Baru Seri Petaling, Bukit Jalil 18 58200 Bukit Indah 19 57100 Jalan Besar Salak Selatan, Jalan Sungai Besi 20 58100 Fairview Mansion, Bukit Pisang 21 59200 Bandar Mid - Valley 22 58000 Bedford Bussiness Park 23 50470 Jalan Stesen Sentral 5, Jalan Travers 24 50460 Bukit Petaling, Jalan Lapangan Terbang Lama 25 55200 Jalan Chan Sow Lin, Jalan Hang Tuah 26 50150 Jalan Changkat Stadium, Jalan Maharajalela 27 50000 Jalan Balai Polis, Jalan Petaling RM 15 28 50050 Balai Seni Lukis Negara, Central Square 29 50100 Bangunan Mara, Jalan Dang Wangi (ZONE 3) 30 50250 Jalan P. Ramlee, Menara KL 31 50200 Cangkat Bukit Bintang, Persiaran Raja Chulan 32 50450 Bangunan Angkasa Raya, -

First of All, I of Living Next to My Cyberjaya Campus at After

ANNUAL 20 12REPORT First of all, I DREAM of living next to my Cyberjaya Campus at After graduation, I look forward to working & living in the booming Iskandar area When I get married, I will be living close to my parents at Of course, I would want to bring up my children in an eco-paradise Finally, I plan to spend my golden years in a tranquil & luxurious setting Iskandar Malaysia Iconic residential towers Elevating luxury with high-rise residential towers that are both TM Southbay Plaza, Batu Maung M-city, Jalan Ampang M-Suites , Jalan Ampang architecturally impressive and One Lagenda, Cheras Icon Residence, Mont’ Kiara www.southbay.com.my 03-2162 8282 www.m-suites.com.my thoughtfully equipped with www.onelagenda.com.my www.icon-residence.com.my www.m-city.com.my lifestyle amenities. N 3º 9’23.37” E 101º 4’19.28” Johor Austine Suites, Tebrau Mah Sing i-Parc, Tanjung Pelapas The Meridin@Medini 07-355 4888 07-527 3133 1800-88-6788 / 07-355 4888 Lagenda@Southbay, Batu Maung Bayan Lepas Kuala Lumpur www.austinesuites.com.my www.mahsing.com.my www.mahsing.com.my 04-628 8188 N 1º 32’54” E 103º 45’5” N 1º 33.838’ E 103º 35.869’ N 1º 32’54” E 103º 47’5” www.southbay.com.my N 5º 17’7” E 100º 17’18” Johor Bahru Selangor Ferringhi Residence, Batu Ferringhi 04-628 8188 www.ferringhi-residence.com.my Dynamic integrated developments N 5º 17’7” E 100º 17’18” Combining commercial, residential and retail components within a Batu Ferringhi Cyberjaya development to provide discerning investors and residents alike with all of the lifestyle offerings of a modern venue.