Price Trends Growth Drivers Supply Analysis

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Copy of PAN Maharasthra Empanelled

MDINDIA HEALTH INSURANCE TPA PVT. LTD. Provider Management IN PAN Maharashtra Empanelled Hospital List Date : 05_10_2018 This has reference to captioned subject and inform you that the Cashless Facilities will only be available in PPN Hospitals (For Mumbai and Pune City), the list of the hospital is attached herewith. You are requested to kindly note of the same inform all Dy. CIROs so that they can avail this facility only in PPN Hospitals in case of Pune, Mumbai and other PPN Cities across India. Sr. No. Hospital Name Location City State Address Status PPN Hospital PPNCITY 1 Aashirwad Critical Care Unit And Multispeciality Hospital Mulund Mumbai Maharashtra Navinjyot , RRT Road, Mulund West Empanelled IN PPN Mumbai 2 Aastha Health Care Mulund Mumbai Maharashtra Mulund Colony, Off LBS Rd, Opp Chheda Petrol Pump Empanelled IN PPN Mumbai 3 Aastha Hospital Kandivali Mumbai Maharashtra 65, Balasinor Society, S.V.Road, Opp Fire Brigade, Kandivali W Empanelled IN PPN Mumbai 4 Aayush Eye Clinic Chembur Mumbai Maharashtra 201/202, Coral Classic, 20th Road, Near Ambedkar Garden, ChemburEmpanelled IN PPN Mumbai 5 Abhishek Nursing Home Ghatkopar Mumbai Maharashtra Jagriti CHS, Nr Maratha Mandir Co-op Bank, Bhatwadi Empanelled IN PPN Mumbai 6 Aditi Hospital Mulund Mumbai Maharashtra 185 - R, Alhad, P.K Road, Above Corporation Bank Mulund (W) Empanelled IN PPN Mumbai 7 Aditi Hospital Malad Mumbai Maharashtra 1st Floor, Param Ratan, Opp. Post Office, Jakeria Empanelled IN PPN Mumbai 8 Advanced Eye Hospital & Institute Sanpada Mumbai Maharashtra 30 the abbaires Sector 17 palm beach road sanpada Empanelled IN PPN Mumbai 9 Aggarwal Eye Hospital Andheri Mumbai Maharashtra 102/5, Ketayun Mansion, Shahaji Raje Marg, Above T Empanelled IN PPN Mumbai 10 Agrawal Eye Hospital Malad Mumbai Maharashtra 1st floor, maharaja apt, Malad (W), S V Road, opp. -

Estate 5 BHK Brochure

4 & 5 BHK LUXURY HOMES Hiranandani Estate, Thane Hiranandani Estate, Off Ghodbunder Road, Thane (W) Call:(+91 22) 2586 6000 / 2545 8001 / 2545 8760 / 2545 8761 Corp. Off.: Olympia, Central Avenue, Hiranandani Business Park, Powai, Mumbai - 400 076. [email protected] • www.hiranandani.com Rodas Enclave-Leona, Royce-4 BHK & Basilius-5 BHK are mortgaged with HDFC Ltd. The No Objection Certificate (NOC)/permission of the mortgagee Bank would be provided for sale of flats/units/property, if required. Welcome to the Premium Hiranandani Living! ABUNDANTLY YOURS Standard apartment of Basilius building for reference purpose only. The furniture & fixtures shown in the above flat are not part of apartment amenities. EXTRAVAGANTLY, oering style with a rich sense of prestige, quality and opulence, heightened by the cascades of natural light and spacious living. Actual image shot at Rodas Enclave, Thane. LUXURIOUSLY, navigating the chasm between classic and contemporary design to complete the elaborated living. • Marble flooring in living, dining and bedrooms • Double glazed windows • French windows in living room • Large deck in living/dining with sliding balcony doors Standard apartment of Basilius building for reference purpose only. The furniture & fixtures shown in the above flat are not part of apartment amenities. CLASSICALLY, veering towards the modern and eclectic. Standard apartment of Basilius building for reference purpose only. The furniture & fixtures shown in the above flat are not part of apartment amenities. EXCLUSIVELY, meant for the discerning few! Here’s an access to gold class living that has been tastefully designed and thoughtfully serviced, oering only and only a ‘royal treatment’. • Air-conditioner in living, dining and bedrooms • Belgian wood laminate flooring in common bedroom • Space for walk–in wardrobe in apartments • Back up for selected light points in each flat Standard apartment of Basilius building for reference purpose only. -

Reg. No Name in Full Residential Address Gender Contact No

Reg. No Name in Full Residential Address Gender Contact No. Email id Remarks 20001 MUDKONDWAR SHRUTIKA HOSPITAL, TAHSIL Male 9420020369 [email protected] RENEWAL UP TO 26/04/2018 PRASHANT NAMDEORAO OFFICE ROAD, AT/P/TAL- GEORAI, 431127 BEED Maharashtra 20002 RADHIKA BABURAJ FLAT NO.10-E, ABAD MAINE Female 9886745848 / [email protected] RENEWAL UP TO 26/04/2018 PLAZA OPP.CMFRI, MARINE 8281300696 DRIVE, KOCHI, KERALA 682018 Kerela 20003 KULKARNI VAISHALI HARISH CHANDRA RESEARCH Female 0532 2274022 / [email protected] RENEWAL UP TO 26/04/2018 MADHUKAR INSTITUTE, CHHATNAG ROAD, 8874709114 JHUSI, ALLAHABAD 211019 ALLAHABAD Uttar Pradesh 20004 BICHU VAISHALI 6, KOLABA HOUSE, BPT OFFICENT Female 022 22182011 / NOT RENEW SHRIRANG QUARTERS, DUMYANE RD., 9819791683 COLABA 400005 MUMBAI Maharashtra 20005 DOSHI DOLLY MAHENDRA 7-A, PUTLIBAI BHAVAN, ZAVER Female 9892399719 [email protected] RENEWAL UP TO 26/04/2018 ROAD, MULUND (W) 400080 MUMBAI Maharashtra 20006 PRABHU SAYALI GAJANAN F1,CHINTAMANI PLAZA, KUDAL Female 02362 223223 / [email protected] RENEWAL UP TO 26/04/2018 OPP POLICE STATION,MAIN ROAD 9422434365 KUDAL 416520 SINDHUDURG Maharashtra 20007 RUKADIKAR WAHEEDA 385/B, ALISHAN BUILDING, Female 9890346988 DR.NAUSHAD.INAMDAR@GMA RENEWAL UP TO 26/04/2018 BABASAHEB MHAISAL VES, PANCHIL NAGAR, IL.COM MEHDHE PLOT- 13, MIRAJ 416410 SANGLI Maharashtra 20008 GHORPADE TEJAL A-7 / A-8, SHIVSHAKTI APT., Male 02312650525 / NOT RENEW CHANDRAHAS GIANT HOUSE, SARLAKSHAN 9226377667 PARK KOLHAPUR Maharashtra 20009 JAIN MAMTA -

A-72EXP Bus Time Schedule & Line Route

A-72EXP bus time schedule & line map A-72EXP Rani Laxmibai Chowk (Sion) - Bhayander View In Website Mode Railway Station (E) The A-72EXP bus line (Rani Laxmibai Chowk (Sion) - Bhayander Railway Station (E)) has 2 routes. For regular weekdays, their operation hours are: (1) Bhayander Railway Station (E): 6:00 AM - 8:00 PM (2) Rani Laxmibai Chowk (Sion): 7:00 AM - 9:00 PM Use the Moovit App to ƒnd the closest A-72EXP bus station near you and ƒnd out when is the next A-72EXP bus arriving. Direction: Bhayander Railway Station (E) A-72EXP bus Time Schedule 33 stops Bhayander Railway Station (E) Route Timetable: VIEW LINE SCHEDULE Sunday 6:00 AM - 8:00 PM Monday 6:00 AM - 8:00 PM Rani Laxmibai Chowk Tuesday 6:00 AM - 8:00 PM Rani Laxmibai Chowk-Sion Road No 3, Mumbai Wednesday 6:00 AM - 8:00 PM Rani Laxmibai Chowk / Sion Railway Station Thursday 6:00 AM - 8:00 PM Friday 6:00 AM - 8:00 PM Naik Nagar Saturday 6:00 AM - 8:00 PM Nature Park / Pmgp Colony PGMP Road, Mumbai Dharavi Depot A-72EXP bus Info Dharavi Koliwada Direction: Bhayander Railway Station (E) Stops: 33 Kala Nagar (Bandra-E) Trip Duration: 59 min Sion Bandra Link Road, Mumbai Line Summary: Rani Laxmibai Chowk, Rani Laxmibai Chowk-Sion, Rani Laxmibai Chowk / Sion Railway Kala Nagar (Bandra-E) Station, Naik Nagar, Nature Park / Pmgp Colony, Ali Yavar Jung Marg, Mumbai Dharavi Depot, Dharavi Koliwada, Kala Nagar (Bandra-E), Kala Nagar (Bandra-E), Kherwadi Kherwadi Junction Junction, New Agripada, Hanuman Road (Vile Parle- E), Gundavli / Lion's Club, Ismail Yusuf College, New Agripada -

MUMBAI an EMERGING HUB for NEW BUSINESSES & SUPERIOR LIVING 2 Raigad: Mumbai - 3.0

MUMBAI AN EMERGING HUB FOR NEW BUSINESSES & SUPERIOR LIVING 2 Raigad: Mumbai - 3.0 FOREWORD Anuj Puri ANAROCK Group Group Chairman With the island city of Mumbai, Navi Mumbai contribution of the district to Maharashtra. Raigad and Thane reaching saturation due to scarcity of is preparing itself to contribute significantly land parcels for future development, Raigad is towards Maharashtra’s aim of contributing US$ expected to emerge as a new destination offering 1 trillion to overall Indian economy by 2025. The a fine balance between work and pleasure. district which is currently dominated by blue- Formerly known as Kolaba, Raigad is today one collared employees is expected to see a reverse of the most prominent economic districts of the in trend with rising dominance of white-collared state of Maharashtra. The district spans across jobs in the mid-term. 7,152 sq. km. area having a total population of 26.4 Lakh, as per Census 2011, and a population Rapid industrialization and urbanization in density of 328 inhabitants/sq. km. The region Raigad are being further augmented by massive has witnessed a sharp decadal growth of 19.4% infrastructure investments from the government. in its overall population between 2001 to 2011. This is also attributing significantly to the overall Today, the district boasts of offering its residents residential and commercial growth in the region, a perfect blend of leisure, business and housing thereby boosting overall real estate growth and facilities. uplifting and improving the quality of living for its residents. Over the past few years, Raigad has become one of the most prominent districts contributing The report titled ‘Raigad: Mumbai 3.0- An significantly to Maharashtra’s GDP. -

Maharashtra State Boatd of Sec & H.Sec Education Pune

MAHARASHTRA STATE BOATD OF SEC & H.SEC EDUCATION PUNE - 4 Page : 1 schoolwise performance of Fresh Regular candidates MARCH-2020 Division : MUMBAI Candidates passed School No. Name of the School Candidates Candidates Total Pass Registerd Appeared Pass UDISE No. Distin- Grade Grade Pass Percent ction I II Grade 16.01.001 SAKHARAM SHETH VIDYALAYA, KALYAN,THANE 185 185 22 57 52 29 160 86.48 27210508002 16.01.002 VIDYANIKETAN,PAL PYUJO MANPADA, DOMBIVLI-E, THANE 226 226 198 28 0 0 226 100.00 27210507603 16.01.003 ST.TERESA CONVENT 175 175 132 41 2 0 175 100.00 27210507403 H.SCHOOL,KOLEGAON,DOMBIVLI,THANE 16.01.004 VIVIDLAXI VIDYA, GOLAVALI, 46 46 2 7 13 11 33 71.73 27210508504 DOMBIVLI-E,KALYAN,THANE 16.01.005 SHANKESHWAR MADHYAMIK VID.DOMBIVALI,KALYAN, THANE 33 33 11 11 11 0 33 100.00 27210507115 16.01.006 RAYATE VIBHAG HIGH SCHOOL, RAYATE, KALYAN, THANE 151 151 37 60 36 10 143 94.70 27210501802 16.01.007 SHRI SAI KRUPA LATE.M.S.PISAL VID.JAMBHUL,KULGAON 30 30 12 9 2 6 29 96.66 27210504702 16.01.008 MARALESHWAR VIDYALAYA, MHARAL, KALYAN, DIST.THANE 152 152 56 48 39 4 147 96.71 27210506307 16.01.009 JAGRUTI VIDYALAYA, DAHAGOAN VAVHOLI,KALYAN,THANE 68 68 20 26 20 1 67 98.52 27210500502 16.01.010 MADHYAMIK VIDYALAYA, KUNDE MAMNOLI, KALYAN, THANE 53 53 14 29 9 1 53 100.00 27210505802 16.01.011 SMT.G.L.BELKADE MADHYA.VIDYALAYA,KHADAVALI,THANE 37 36 2 9 13 5 29 80.55 27210503705 16.01.012 GANGA GORJESHWER VIDYA MANDIR, FALEGAON, KALYAN 45 45 12 14 16 3 45 100.00 27210503403 16.01.013 KAKADPADA VIBHAG VIDYALAYA, VEHALE, KALYAN, THANE 50 50 17 13 -

Maha Eseva Kendra List

महा-ई-सेवा कᴂ 饍ा車ची यादी Sr. VLE Name Palghar CSC Address Location Pincode Mobile Maha E Sewa Kendra Nitin Bhaidas Rampur 1 Rampur Kosbad Road Near 401702 8237635961 Mothe (551636) Market Rampur Jayprakash Gholwad Gholwad Near 2 Ramchandra Gholwad 401702 9860891473 Jalaram Temple Gholwad Bari Bhika Bandu Parnaka Parnaka Parnaka Dahanu (M 3 401602 9637999157 Sonawane Dahanu Cl) Ganpat At-Haladpada Amboli 4 Sukhad Halapada 401606 9960227641 Shishane Road Haladpada Dhangda Nr Saideep Hospital At Post Malyan Tq Dhanu Amul Ramdas Dahanu (M 5 East Dist Thane-401602 401602 9967910609 Tandel Cl) Malyan Sai Deep Hospital Dahanu E Santosh Muskan S S Sanstha 6 Ramchandra 16,Sidhhi Complex,Kasa Kasa Kh. 401607 9049494194 Patil Dahanu Jawhar Road Gayatri Enterprizes, Muskan 16,Siddhicomplex, 7 Swayamrojgar 16,Siddhicomplex Dahanu Kasa Kh. 401607 9049494194 Seva Sahakari Jawhar Road Near Bank Of Maharashtra Kasa Jahir Kasim Maha E Seva Kendra 8 Vangaon 401103 9423533665 Shaikh Chinchani Road Vangaon Maha E Seva Kendra Jayvanti Dahanu (M 9 Dahanu Fort Near Ganesh 401601 9273039057 Rajendra Bari Cl) Mandir Tahsildar Office Maha E Seva Center Dhakti Dahanu Dhakti Dhakti 10 Kishor R Bari 401601 9860002524 Dahanu Bariwada Near Bus Dahanu Stop Maha E Seva Kendra Bordi Akshay 11 Shop No 511 Netaji Road Bordi 401701 8149107404 Bprakash Raut Opp Ram Mandir Bordi Muskan Maha E Seva Kendra 12 Swayamrojgar Ashagad 401602 7066822781 Ashagad Seva Sahakari Maha E-Seva Kendra 2 Prafful Dahanu-Vangaon Road 13 Jaywant Saravali 401602 8087930398 Near Savta Bridge Vaidya Ghungerpada At Dhundalwadi Darshana Dhundalwad 14 Dhundalwadi Talathi 401606 9765284663 Vilas Hilim i Office Ramij Kashim Maha E Seva Kendra 15 Aine 401103 9423533665 Shaikh Charoti Road Aina Maha E Seva Center Chinchani Vangaon Naka 01 Prathomasatv Bulding Chinchani 16 Kishor R Bari 401503 9860002524 Dahanu Khadi - Boisar (Ct) Road Near State Bank A.T.M. -

SR NO First Name Middle Name Last Name Address Pincode Folio

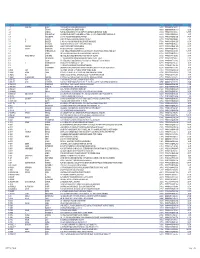

SR NO First Name Middle Name Last Name Address Pincode Folio Amount 1 A SPRAKASH REDDY 25 A D REGIMENT C/O 56 APO AMBALA CANTT 133001 0000IN30047642435822 22.50 2 A THYAGRAJ 19 JAYA CHEDANAGAR CHEMBUR MUMBAI 400089 0000000000VQA0017773 135.00 3 A SRINIVAS FLAT NO 305 BUILDING NO 30 VSNL STAFF QTRS OSHIWARA JOGESHWARI MUMBAI 400102 0000IN30047641828243 1,800.00 4 A PURUSHOTHAM C/O SREE KRISHNA MURTY & SON MEDICAL STORES 9 10 32 D S TEMPLE STREET WARANGAL AP 506002 0000IN30102220028476 90.00 5 A VASUNDHARA 29-19-70 II FLR DORNAKAL ROAD VIJAYAWADA 520002 0000000000VQA0034395 405.00 6 A H SRINIVAS H NO 2-220, NEAR S B H, MADHURANAGAR, KAKINADA, 533004 0000IN30226910944446 112.50 7 A R BASHEER D. NO. 10-24-1038 JUMMA MASJID ROAD, BUNDER MANGALORE 575001 0000000000VQA0032687 135.00 8 A NATARAJAN ANUGRAHA 9 SUBADRAL STREET TRIPLICANE CHENNAI 600005 0000000000VQA0042317 135.00 9 A GAYATHRI BHASKARAAN 48/B16 GIRIAPPA ROAD T NAGAR CHENNAI 600017 0000000000VQA0041978 135.00 10 A VATSALA BHASKARAN 48/B16 GIRIAPPA ROAD T NAGAR CHENNAI 600017 0000000000VQA0041977 135.00 11 A DHEENADAYALAN 14 AND 15 BALASUBRAMANI STREET GAJAVINAYAGA CITY, VENKATAPURAM CHENNAI, TAMILNADU 600053 0000IN30154914678295 1,350.00 12 A AYINAN NO 34 JEEVANANDAM STREET VINAYAKAPURAM AMBATTUR CHENNAI 600053 0000000000VQA0042517 135.00 13 A RAJASHANMUGA SUNDARAM NO 5 THELUNGU STREET ORATHANADU POST AND TK THANJAVUR 614625 0000IN30177414782892 180.00 14 A PALANICHAMY 1 / 28B ANNA COLONY KONAR CHATRAM MALLIYAMPATTU POST TRICHY 620102 0000IN30108022454737 112.50 15 A Vasanthi W/o G -

Jurisdiction Raigad Alibag.Pdf

CNTVTINNT JURISDICTION 'r ,r, .,r,:. ,,1, r r' .i T,. AIJBAGAIJBAG,. .rr.r,, ,:i .. L , ,., ...:i, . ,t .. , : L Court of Dirict and 1. Trial and Disposal of Session's cases and all Sessions Judge, Raigad-'special Cases arises in the area of Police Station Alibag Alibag, Mandawa Sagari, Revdanda, Poynad,, Pen, Wadkhal, Dadar Sagari, Nagothane, Murud 2. Appeals and Revision Petitions of rDecisions,/Orders passed by Adhoc-District, 'Magistrate, Raigad-Alibag, Chief Judicial, Magistrate, Raigad-Alibag, Judicial Magistrate of Sub-Division Alibag Pen and Murud. 3. Revision Petitions against Decisions,/Orders under Cr.P.C. Passed by Sub-Divisional Magistrate,/Additional District Magistrate of Sub- Division Alibag, Pen and Murud. Bail Application matters in the area of Police ,Station'4. Alibag, Mandawa Sagari, Revdanda, Poynad, Pen, Wadkhal, Dadar Sagari, Nagothane, Murud. 5. Application filled under section 408 Cr.P.C. 2 Court of District Judge- 1. Uearing & Disposal of all cases tr"rrsferred' 1 and Additional from District Coun. Session Judge, Raigad- Alibag 2. Trial & Disposal of cases relating to. M.O.C.C.A., E.C. Act., M.P.I.D. and case filed by C.B.I. under anti-corruption and N.D.P.S. arises iin the area of Police Station Alibag,r gryg6, Mandawa :Sagari, Revdanda, Poynad, Pen, Wadkhal, DadarDadar: . .:"l1t'Nagothane'*ulo:'Sagari, Nagothane, Murud. 3 Court of^^. District Judge- 1. Hearing A Oisposal oi all cases transferred 2 and Assistant Session from District Court. Judge, Raigad-Alibag 4 Coun of Adhoc District l. Hearing & Disposal of all cases transferred, Judge-1 and Assistant,from District Court. -

Police Station Wise Magistrate Raigad Alibag.Pdf

Police station wise Magisfiate 1. Alibag Police Station 2. Poynad Police Station 3. Revdanda Police Station Court of Chief Judicial Magistrate, Raigad 4. Mandawa Sagari Police Station 11 - Alibag 5. State Excise Depaftment Alibag & Flying Squad Police Station 6. Local Crime Branch 1. Alibag Police Station t2 Civil Judge, J. D. & J.M.F.C., Alibag 2. Poynad Police Station 3. Revdanda Police Station -tJ 2nd Jt. Civil Judge, J. D. & J.M.F.C., Alibag 4. Mandawa Sagari Police Station 3'd Jt. Civil Judge, J. D. & J.M.F.C., Alibag t4 5. State Excise Departrnent Alibag & Flying Squad Police Station l5 4sJt. Civil Judge, J. D. & J.M.F.C., Alibag 6. Local Crime Branch 1. Panvel Ciry Police Station t6 Jt. Civil Judge, Junior Divisioq Panvel 2. Panvel Town Police Station 1. Khandeshwar Police Stadon t7 2"d Civil Judge, J. D. & J.M.F.C., Panvel 2. NRI Sagari Police Station 1. Khargar Police Station 18 3'd Civil Judge, J. D. & J.M.F.C., Panvel 2. Navasheva Police Station 1. Kalamboli Police Station r9 4d Civil Judge, J. D. & J.M.F.C., Panvel 2. Kamothe Police Station 3. Taloia Police Station 1. Rasayani Police Station 2. State Excise Panvel City 3. State Excise Khalapur 4. State Excise Kadat 20 5d Civil Judge, J. D. & J.M.F.C., Panvel 5. State Excise Uran 6. State Excise Flying Squad No-2, Panvel 7. State Excise Flying Squad Thane 8. State Excise Flying Squad Mumbai L. Pen Police Station 2. Wadkhal Police Station 27 Civil Judge, J. -

A Detailed Property Analysis Report of Siddhi Highland Gardens in Thane

PROPINSIGHT A Detailed Property Analysis Report 40,000+ 10,000+ 1,200+ Projects Builders Localities Report Created On - 7 Oct, 2015 Price Insight This section aims to show the detailed price of a project and split it into its various components including hidden ones. Various price trends are also shown in this section. Project Insight This section compares your project with similar projects in the locality on construction parameters like livability rating, safety rating, launch date, etc. What is Builder Insight PROPINSIGHT? This section delves into the details about the builder and tries to give the user a perspective about the history of the builder as well as his current endeavours. Locality Info This section aims to showcase various amenities viz. pre-schools, schools, parks, restaurants, hospitals and shopping complexes near a project. Siddhi Highland Gardens Thane West, Mumbai 1.17 Cr onwards Livability Score 6.6/ 10 Project Size Configurations Possession Starts 15 Towers 2,3 Bedroom Apartment Jun `17 Pricing Comparison Comparison of detailed prices with various other similar projects Pricing Trends Price appreciation and trends for the project as well as the locality What is PRICE INSIGHT? Price versus Time to completion An understanding of how the current project’s prices are performing vis-a-vis other projects in the same locality Demand Comparison An understanding of how the strong/weak is the demand of current project and the current locality vis-a-vis others Price Trend Of Siddhi Highland Gardens Siddhi Highland Gardens -

THE ERA of TRANSCENDENCE Ane-Dombivli a FACT-FILE on the GROWTH of NAVI MUMBAI on the GROWTH of NAVI a FACT-FILE

Redefining Real Estate www.marathonrealty.com THE ERA OF TRANSCENDENCE ane-Dombivli A FACT-FILE ON THE GROWTH OF NAVI MUMBAI ON THE GROWTH OF NAVI A FACT-FILE Corporate Address: 702 Marathon Max, Mulund-Goregaon Link Road, Mulund West, Mumbai - 400080 www.marathonrealty.com Today, nobody fails to mention Thane-Dombivli when the subject of discussion is growth of infrastructure in Mumbai and its peripheries. Belapur, Panvel, Dronagiri and even the areas beyond them are taking rapid strides towards development. It is almost astounding to see this transformation take place. This is a compilation of evidences offering a glimpse into the making of the future. 2 3 2 3 INDEX 01 THANE-DOMBIVLI – REALTY 02 INFRASTRUCTURE Why Kalyan-Dombivli will drive Mumbai’s realty market now ........................................................................................................................................08 Kalyan-Dombivli-Taloja metro under consideration: Devendra Fadnavis .....................................................................................................................20 What is special about Thane real estate ................................................................................................................................................................................11 TMT starts new service from Thane to Dombivli west - Infrastructure ..........................................................................................................................21 Thane: A residential destination in sync with