No-Fault Auto Insurance: a Survey

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Auto –Accidents - What Is “No-Fault” Insurance?

AUTO –ACCIDENTS - WHAT IS “NO-FAULT” INSURANCE? If you are injured in a car accident who pays your medical bills? Believe it or not, your medical insurance carrier does not have the primary responsibility to pay your medical bills for injuries sustained in an automobile accident - The applicable automobile insurance carrier does. But remember, if your injuries or above a certain threshold you can still sue the person who cause your injuries for money damages above what the applicable automobile insurance carrier provides. In New York State each automobile insurance policy must provide coverage known as Personal Injury Protection (“PIP”) and typically referred to a “No-Fault” insurance. Medical bills, some or all of the injured party’s lost wages and other expenses are paid from this portion of the policy, whether or not the injured party caused the accident. So if were in a car accident driving your own vehicle and you are injured as a result of another person's negligence, the no-fault portion of your automobile insurance policy will cover your medical bills to the extent that you have coverage. If your coverage runs out other insurance will kick in. The New York State Insurance Law, requires that all automobile insurance policies issued in this state contain a Personal Injury Protection (“PIP”) or “No-Fault” endorsement with a minimum of $50,000.00 in coverage. Generally speaking, this coverage extends to the driver and passengers in a covered vehicle, as well as to a pedestrian struck by the covered vehicle. The coverage “kicks in” regardless of fault in connection with an accident; under most circumstances, a covered individual will be afforded certain enumerated benefits regardless of that individual’s fault in connection with the happening of the accident. -

Long-Term Care Insurance Policy

NEW YORK LIFE INSURANCE COMPANY 51 Madison Avenue, New York, NY 10010 New York Life, Long-Term Care Insurance (800) 224-4582 www.newyorklife.com Long-Term Care Insurance Policy FEDERAL TAX-QUALIFIED COVERAGE: THIS CONTRACT FOR LONG-TERM CARE INSURANCE IS INTENDED TO BE A FEDERALLY QUALIFIED LONG-TERM CARE INSURANCE CONTRACT AND MAY QUALIFY YOU FOR FEDERAL AND STATE TAX BENEFITS. THIS POLICY IS AN APPROVED LONG-TERM CARE INSURANCE POLICY UNDER CALIFORNIA LAW AND REGULATIONS. HOWEVER, THE BENEFITS PAYABLE BY THIS POLICY WILL NOT QUALIFY FOR MEDI-CAL ASSET PROTECTION UNDER THE CALIFORNIA PARTNERSHIP FOR LONG-TERM CARE. FOR INFORMATION ABOUT POLICIES AND CERTIFICATES QUALIFYING UNDER THE CALIFORNIA PARTNERSHIP FOR LONG-TERM CARE, CALL THE [HEALTH INSURANCE COUNSELING AND ADVOCACY PROGRAM AT THE TOLL-FREE NUMBER 1 (800) 434-0222. This Policy is a legal contract between You and New York Life Insurance Company (herein called We, Us, and Our). Please read this Policy carefully and in its entirety. It is issued in exchange for Your Application, and payment of required premiums. This is a long-term care insurance policy that covers Nursing Facility Care, Residential Care Facility, and Home and Community Based Care. 30 Day Free Look Period. Please examine Your Policy promptly. Within 30 days after delivery, You can return the Policy by first class United States mail to New York Life Insurance Company. Upon our receipt of Your Policy a full premium refund will be made to You within 30 days of the Policy’s return and coverage will be void from start. PARTICIPATING. -

Illinois Mandatory Insurance Brochure

The Illinois Department of Insurance regulates insur- IF YOU ARE INVOLVED ance companies, agencies and agents. It maintains a IN AN ACCIDENT Consumer Services Division that can answer your questions about auto insurance. If you have questions An accident report form must be filed with the Illinois or wish to file a complaint, please contact: Department of Transportation (IDOT) if damages exceed Mandatory Vehicle $500 or if injuries resulted from the accident. At-fault, Illinois Department of Insurance uninsured motorists are required to pay for damages 320 W. Washington St. they cause or face license plate registration and driver's Springfield, IL 62767-0001 INSURANCE license suspensions. www.state.il.us/ins/ The Secretary of State's office does not maintain insur- ance information for all registered motor vehicles. FOR MORE INFORMATION Insurance information is available only from the motorist involved in the accident or from the report filed with For more information about Illinois’ Mandatory Insur- IDOT. ance Law, please contact: For more information on reporting an accident, please Office of the Secretary of State contact: Mandatory Insurance Division 501 S. Second St. Illinois Department of Transportation 429 Howlett Bldg. Office of Planning and Programming Springfield, IL 62756-7000 Bureau of Data Collections 217-524-4946 2300 S. Dirksen Pkwy. Springfield, IL 62764 217-782-4518 PURCHASING INSURANCE Contact an insurance agent to buy liability insurance for your vehicle. Some companies do not sell insurance to vehicle owners who have been driving uninsured. If you have problems buying insurance, ask your insur- ance agent about the Illinois Automobile Insurance Plan. -

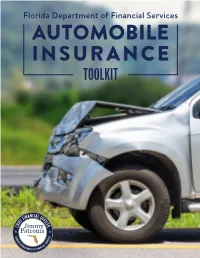

AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit

Florida Department of Financial Services AUTOMOBILE INSURANCE TOOLKIT Automobile Insurance Toolkit Insurance coverage is an integral part of a solid financial foundation. Insurance can help us recover financially after illness, accidents, natural disasters or even the death of a loved one. There are a wide variety of insurance products available and choosing the correct type and amount of coverage can be a challenge. This toolkit provides information to assist you with insuring your automobile and tips for settling an automobile insurance claim. TABLE OF CONTENTS Click a title or page number to navigate to a section. 01 Coverages & Minimum Requirements - 4 Coverage Descriptions - 5 Insurance Requirements for Special Cases - 8 02 Underwriting Guidelines - 11 Underwriting Factors That Cannot Affect Your Ability to Purchase Insurance - 11 Underwriting Factors That Affect Your Insurance Policy Premium - 12 Other Factors Affecting Your Premiums - 13 Shopping for Auto Insurance - 13 03 Automobile Claims - 14 Actions to Take Before and After an Auto Accident - 14 Disputing Claim Settlements - 16 04 Shopping for Coverage Checklist - 17 01 Coverages & Minimum Requirements In Florida, vehicle owners may be required to The second type of auto insurance is outlined in the purchase two types of auto insurance. Florida Financial Responsibility Law. It requires drivers The first type of auto insurance is outlined in the who have caused accidents involving bodily injury/death Florida Motor Vehicle No-Fault Law (s. 627.736, Florida or received certain citations, to purchase bodily injury Statutes). It requires every person who registers a liability (BI) coverage with minimum limits of $10,000 vehicle in Florida to provide proof they have personal per person and $20,000 per accident, referred to as injury protection (PIP) and property damage liability split limits. -

Motor Vehicle Insurance Fraud and Related Crimes

2017 Statewide Plan of Operation Detection, Prevention, Deterrence, and Reduction of Motor Vehicle Insurance Fraud and Related Crimes COPYRIGHT NOTICE Copyright 2017 by the New York State Division of Criminal Justice Services (DCJS) This publication may be reproduced without the express written permission of DCJS provided that this copyright notice appears on all copies or segments of the publication. The 2017 edition is published on behalf of the New York State Motor Vehicle Theft and Insurance Fraud Prevention by the: New York State Division of Criminal Justice Services Office of Program Development and Funding Alfred E. Smith Office Building 80 South Swan Street Albany, New York 12210 Table of Contents The Statewide Plan of Operation for Motor Vehicle Insurance Fraud Introduction ........................................................................................................... 1 Eligible Programs ................................................................................................. 1 Outline of Statewide Plan ..................................................................................... 1 Part I: Problem Identification of Motor Vehicle Insurance Fraud National Overview ................................................................................................ 3 Statewide Overview .............................................................................................. 3 Part II: Analysis of Motor Vehicle Insurance Fraud in New York State Statewide ............................................................................................................. -

What You Need to Know

What AutoAuto you InsuranceInsurance need to know A consumer information publication The Minnesota Department of Commerce has prepared this guide to help you better understand auto insurance. It gives you information on shopping for insurance, the different types of coverage, and a basic understanding of “no fault” coverage. The Minnesota Department of Commerce regulates insurance agents, agencies, adjusters, and companies operating in Minnesota. If they are licensed to do business in the State, they are responsible for adhering to the laws and rules that govern the industry. This guide does not list all of these regulations. If you have a question about your insurance, please contact the Department’s Consumer Response Team at 651-296-2488, or toll free 800-657-3602. Duplication of this guide is encouraged. Please feel free to copy this information and share it with others. Department of Commerce Auto Insurance can protect you from the financial costs of an accident or injury, provided you have the proper coverage. Yet many people are unclear about what their insurance policy cov- ers until it is too late. They may have difficulties settling a claim or face rate increases or termination of coverage. Auto Insurance I s ... Protection. Insurance is a way of transferring risk for a loss among a certain group of people. You, and others, pay premiums to an insurance company to be reimbursed if you have an acci- dent. The amount you can collect and under what circumstances are outlined in your policy. Required. Under most circumstances, a licensed vehicle in the state of Minnesota must have liability, personal injury protection, uninsured motorist, and underinsured motorist coverage. -

February 1, 2018 MASSACHUSETTS PRIVATE PASSENGER RESIDUAL MARKET AUTOMOBILE INSURANCE MANUAL

MASSACHUSETTS PRIVATE PASSENGER RESIDUAL MARKET AUTOMOBILE INSURANCE MANUAL SECTION I - GENERAL RULES RULE 1. ELIGIBILITY All individually owned vehicles registered under the Massachusetts Compulsory Motor Vehicle Law that are eligible for private passenger motor vehicle insurance under the rules of the Massachusetts Automobile Insurance Plan (MAIP) may be rated in accordance with this manual and written on the Massachusetts Automobile Insurance Policy. RULE 2. COVERAGES AND LIMITS The types of coverages available in the CAR Massachusetts Automobile Insurance Policy are: Compulsory Insurance Coverages Part 1 - Bodily Injury to Others The basic limits are $20,000 each person and $40,000 each accident. Part 2 - Personal Injury Protection The basic limit is $8,000 for each person. Refer to Rule 30 for available deductibles. Part 3 - Bodily Injury Caused By an Uninsured Auto The basic limits are $20,000 each person and $40,000 each accident. Increased limits are available. The limits may not exceed the limits of Part 5, or if Part 5 is not purchased, Part 1 of this policy. This coverage is excess over Personal Injury Protection. Part 4 - Damage to Someone Else’s Property The basic limit is $5,000 each accident. Increased limits are available. Optional Insurance Coverages Part 5 - Optional Bodily Injury to Others The basic limits are $20,000 each person and $40,000 each accident. Increased limits are available. Part 6 - Medical Payments The basic limit is $5,000 each person. Higher limits are available for all motor vehicles rated in this manual. Motorcycle limits are available from $500 to $25,000. This coverage is excess over Personal Injury Protection. -

60 Charged in Fall Insurance Fraud Sweep

___________________________________________________________________________________________________________________________________ October 2018 60 Charged in Fall Insurance Fraud Sweep October 2017. On November 13, Harper allegedly filed a claim indicating that 18 items were stolen from his vehicle. Harper • On October 9, 2018, allegedly provided Mark Folino was Allstate with fraudulent arrested in Lawrence receipts for mink coats County. According to and jackets the criminal complaint, purportedly valued at on March 13, 2018, at more than $43,000. approximately 12:49 Investigators spoke to the owner of the men’s PM, Folino rear-ended a store listed on the receipts. The owner State Farm insured allegedly advised that his store did not issue vehicle which was the receipts and did not sell coats at such high- attempting to make a end prices. Allstate denied the claim. Harper left hand turn into a was charged with one count of Insurance Fraud driveway. The complaint stated that when the (F3), one count of Theft by Deception (F3), one accident occurred, Folino was listed as an count of Forgery (F3) and one count of excluded driver on the Progressive Criminal Use of a Communication Facility (F3). Insurance vehicle policy shared by Folino and his wife. Approximately one hour after the • On October 25, 2018, accident, Folino’s wife allegedly added him to Kennesha Watson the policy as a covered driver. Folino allegedly was arrested in contacted Progressive later that day and filed Montgomery County. a claim for the accident, stating that the crash According to the occurred after he was added to the policy as a criminal complaint, on covered driver. However, the complaint stated September 20, 2017, that investigators reviewed the Pennsylvania Watson’s uninsured State Police incident report which confirmed vehicle was involved that the loss occurred prior to the policy in an accident. -

NYSDFS: NYSID Annual Report of the Superintendent of Insurance to The

Annual Report of the Superintendent of Insurance to the New York Legislature Calendar Year 2001 Governor George E. Pataki Superintendent of Insurance Gregory V. Serio www.ins.state.ny.us The One Hundred Forty-Third Annual Report of the Superintendent of Insurance A Report to the New York State Legislature for the Year Ending December 31, 2001 George E. Pataki Gregory V. Serio Governor Superintendent of Insurance www.ins.state.ny.us Data in this report are subject to small table-to-table variations. Such variations are attributable to the fact that data are retrieved at various times throughout the year. Selected portions of this report are available on the Department’s Web site at www.ins.state.ny.us This report is printed on recycled paper. L: gen/Annrpt00/Ar-oov2 TABLE OF CONTENTS Page I. MAJOR DEVELOPMENTS A. September 11……………….….………………………………………………………..… 1 B. Superintendent Serio Appointed…………………………………………….………… 2 C. Terrorism Exclusion......……………...........................................................…........... 2 D. Healthy NY………………………………………………………………………………….. 3 E. Speed to Market……………………………………………………………..…………..… 3 F. Gramm-Leach-Bliley Act…………………………………………………………………. 3 G. Automobile……………………………………………………………………………….… 4 H. Property/Casualty (Non-Auto)..….............…………………………………...........….. 5 I. Health………….……………….………...................................................................…... 5 J. Life.........…………………......……...……………………………................................…. 6 K. Consumer Services..............................................………………......................…..... -

The RAM Health Insurance Cooperative Is NOW Thriving

Health Insurance Cooperative The RAM Health Insurance Cooperative is NOW thriving – and growing – in 2020! The program offers RAM members: A 3% DISCOUNT OFF PREMIUM RATES FOR SMALL BUSINESSES IN THE SMALL GROUP MARKET (Groups of 1-50 employees) ACCESS TO EVERY SMALL GROUP PLAN OFFERED BY BCBSMA & ALMOST ALL SMALL GROUP PLANS OFFERED BY FALLON HEALTH DEFINED CONTRIBUTION OPTIONS TO ADDRESS THE NEEDS OF BOTH YOUR BUSINESS AND YOUR EMPLOYEES And for those members who choose a BCBSMA plan, the program also offers additional value-added benefits including: A WELLNESS PROGRAM WITH POTENTIAL EMPLOYEE INCENTIVES OF UP TO $300 AND AN OPPORTUNITY TO EARN 7.5% IN BACK END EMPLOYER INCENTIVES A FREE SUPPLEMENTAL HOSPITALIZATION POLICY FOR ALL SUBSCRIBERS, WHICH COVERS $750 FOR A HOSPITAL ADMISSION AND $150 EACH ADDITIONAL DAY UP TO 10 DAYS A FREE $10,000 LIFE INSURANCE POLICY FOR ALL SUBSCRIBERS Visit www.retailersma.org or call us at (617) 523-1900 to learn more! Health Insurance Cooperative Dear RAM Member, RAMHIC is a service of the Retailers Association of Massachusetts—the leading voice for more choice and fairer premiums for small businesses and their employees in the Massachusetts insurance market. RAMHIC is an important example of our efforts to deliver economic equality for Main Street. Since the adoption of universal healthcare in Massachusetts, small businesses have received disproportionate increases in their health insurance premiums compared to their large competitors and government programs. In response, RAM fought for the creation of small business group purchasing cooperatives designed to allow like-minded businesses to join together and negotiate with carriers for reduced premium rates based on the projected experience of the group. -

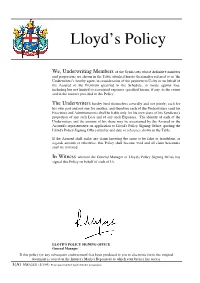

Lloyd's Policy Signing Office, Quoting the Lloyd's Policy Signing Office Number and Date Or Reference Shown in the Table

Lloyd’s Policy of the Syndicates whose definitive numbers We, Underwriting Members and proportions are shown in the Table attached hereto (hereinafter referred to as 'the Underwriters'), hereby agree, in consideration of the payment to Us by or on behalf of the Assured of the Premium specified in the Schedule, to insure against loss, including but not limited to associated expenses specified herein, if any, to the extent and in the manner provided in this Policy. The Underwriters hereby bind themselves severally and not jointly, each for his own part and not one for another, and therefore each of the Underwriters (and his Executors and Administrators) shall be liable only for his own share of his Syndicate's proportion of any such Loss and of any such Expenses. The identity of each of the Underwriters and the amount of his share may be ascertained by the Assured or the Assured's representative on application to Lloyd's Policy Signing Office, quoting the Lloyd's Policy Signing Office number and date or reference shown in the Table. If the Assured shall make any claim knowing the same to be false or fraudulent, as regards amount or otherwise, this Policy shall become void and all claim hereunder shall be forfeited. In Witness whereof the General Manager of Lloyd's Policy Signing Office has signed this Policy on behalf of each of Us. LLOYD'S POLICY SIGNING OFFICE General Manager If this policy (or any subsequent endorsement) has been produced to you in electronic form, the original document is stored on the Insurer's Market Repository to which your broker has access. -

Understanding How Insurance Works: a Case Study About Lucy (Guide) Cfpb Building Block Activities Understanding-How-Insurance-Works-Lucy Guide.Pdf

BUILDING BLOCKS TEACHER GUIDE Understanding how insurance works: A case study about Lucy Students read about how insurance works, then review a case study to see how insurance choices can affect personal finances for a rural young adult. Learning goals KEY INFORMATION Big idea Building block: When you purchase insurance, you are Executive Function transferring financial risk from yourself to an Financial knowledge and insurance company. decision-making skills Essential questions Grade level: High school (9–12) § What is the main benefit of choosing to Age range: 13–19 purchase insurance? Topic: Protect (Managing risk) § How do the insurance company and the policyholder share risks and costs? School subject: CTE (Career and technical education), Math, Physical education or Objectives health, Social studies or history Teaching strategy: Cooperative learning, § Understand how insurance works Simulation § Apply insurance policy specifics to a case study to evaluate costs and benefits Bloom’s Taxonomy level: Understand, Apply, Evaluate What students will do Activity duration: 45–60 minutes § Read about how the insurance process works and discover what roles the insurance STANDARDS company and the policyholders play. § Review information about specific types of Council for Economic Education Standard VI. Protecting and insuring insurance policy coverage and costs. Jump$tart Coalition Risk management and insurance – Standard 1 To find this and other activities go to: Consumer Financial Protection Bureau consumerfinance.gov/teach-activities 1 of 7 Winter 2020 § Evaluate a case study to see how one policyholder’s insurance choices affected her financially. § Write an advice email about the value of insurance in that policyholder’s life.