Freeway Public Golf Course

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LADIES GOLF in QUEENSLAND a Journey Through the Decades 1950S — 2010

LADIES GOLF IN QUEENSLAND A Journey Through the Decades 1950s — 2010 Golf is a game for life. Welcome to this story covering an era when women had their own national and state bodies, guiding the development of women’s golf with wisdom and expertise. Information and valuable knowledge was circulated to the golf clubs by these national and state bodies, ensuring all players, both junior and senior, were nurtured and supported. This is a personal story in which you will read about the culture of golf during this era, the work of the Australian Ladies Golf Union and the Queensland Ladies Golf Union, the major tournaments and promotions, my introduction to the game and my lifetime involvement as a player and as an administrator. Pam Langford — July 2021 Contents The Story Begins 1 The Culture of Golf — Early Days 2 Administration 4 The Australian Ladies Golf Union 6 Major ALGU Promotions and Tournaments 7 International Events 8 Major Queensland Tournaments 9 My Role as Delegate to the QLGU 10 The Story Concludes 14 The Story Begins To tell this story I have to start when I first became aware of the game of golf. I was about 10 to 12 years old, during the early 1950s, and my parents, George and Agnes Tait, talked and played golf as often as time would permit. My dad owned a Sports Store in Brisbane - Tait’s Sports Store - located in the Public Curator’s Arcade in Edward Street, Brisbane. Dad was a very keen sports person and before playing golf he was a State ranked tennis player. -

Victorian Support for Carers Program Providers

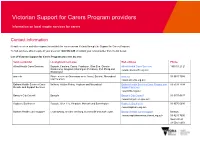

Victorian Support for Carers Program providers Information on local respite services for carers Contact information Respite services and other support is available for carers across Victoria through the Support for Carers Program. To find out more about respite in your area call 1800 514 845 or contact your local provider from the list below. List of Victorian Support for Carers Program providers by area Service provider Local government area Web address Phone Alfred Health Carer Services Bayside, Cardinia, Casey, Frankston, Glen Eira, Greater Alfred Health Carer Services 1800 51 21 21 Dandenong, Kingston, Mornington Peninsula, Port Phillip and <www.carersouth.org.au> Stonnington annecto Phone service in Grampians area: Ararat, Ballarat, Moorabool annecto 03 9687 7066 and Horsham <www.annecto.org.au> Ballarat Health Services Carer Ballarat, Golden Plains, Hepburn and Moorabool Ballarat Health Services Carer Respite and 03 5333 7104 Respite and Support Services Support Services <www.bhs.org.au> Banyule City Council Banyule Banyule City Council 03 9457-9837 <www.banyule.vic.gov.au> Baptcare Southaven Bayside, Glen Eira, Kingston, Monash and Stonnington Baptcare Southaven 03 9576 6600 <www.baptcare.org.au> Barwon Health Carer Support Colac-Otway, Greater Geelong, Queenscliff and Surf Coast Barwon Health Carer Support Barwon: <www.respitebarwonsouthwest.org.au> 03 4215 7600 South West: 03 5564 6054 Service provider Local government area Web address Phone Bass Coast Shire Council Bass Coast Bass Coast Shire Council 1300 226 278 <www.basscoast.vic.gov.au> -

City of Darebin Aboriginal Community 2009 Early Childhood Community Profile

Early Childhood Community Profile City of Darebin Aboriginal Community 2009 Early Childhood Community Profile City of Darebin Aboriginal Community 2009 This Aboriginal Early childhood community profile was prepared by the Office for Children and Portfolio CdiiCoordination, ini the h ViVictorian i Government G DDepartment of f EdEducation i and d EEarly l ChildhChildhood d DDevelopment. l The series of Early Childhood community profiles draw on data on outcomes for children compiled through the Victorian Child and Adolescent Monitoring System (VCAMS). The profiles are intended to provide local level information on the health, wellbeing, learning, safety and developmental outcomes of young Aboriginal children. They are published to aid Aboriginal organisations and local councils, as well as Best Start partnerships, with local service development, innovation and program planning to improve these outcomes. The Department of Human Services, the Department of Education and Early Childhood Development and the Australian Bureau of Statistics provided data for this document. Aboriginal Early Childhood Community Profile i Published by the Victorian Government DepartmentDepartment of Education and Early Childhood Development, Melbourne, Victoria, Australia. January 2010 © Copyright State of Victoria, Department of Education and Early Childhood Development, 2010 This publication is copyright. No part may be reproduced by any process except in accordance with the provisionsprovisions of the Copyright Act 19681968.. Principal author and analyst: Hiba -

50+ in Nillumbik Part 1

Australian Institute for Primary Care & Ageing March 2016 50+ in Nillumbik : A data story Report for Nillumbik agencies Part 1: Health and Wellbeing C ommissioned by the North East Primary Care Partnership ENQUIRIES Professor Yvonne Wells T 0 3 9479 5809 Lincoln Centre for F 03 9479 5977 Research on Ageing E [email protected] AIPCA La Trobe University Victoria 3086 Nillumbik: part 1 Health and wellbeing Australian Institute for Primary Care & Ageing College of Science, Health and Engineering La Trobe University A body politic and corporate ABN 64 804 735 113 The Australian Institute for Primary Care & Ageing (AIPCA) operates within the academic environment of La T robe University. La Trobe University is a Statutory Body by Act of Parliament. Postal Address Australian Institute for Primary Care & Ageing La Trobe University Victoria 3086 Melbourne (Bundoora) Campus Level 5 Health Sciences Building 2 La Trobe University Telephone: (61 - 3) 9479 3700 Facsimile: (61 - 3) 9479 5977 Email: [email protected] Online http://www.latrobe.edu.au/aipca Australian Institute for Primary Care & Ageing, La Trobe University 1 Nillumbik: part 1 Health and wellbeing Table of contents EXECUTIVE SUMMARY 7 INTRODUCTION 9 About us 9 Curate rather than create knowledge 9 About this project 10 What is different? 10 This report 10 Risk and protective factors 11 Data limitations 13 METHODOLOGY 14 ABOUT NILLUMBIK 15 AGE GROUPS 17 SOCIO - ECONOMIC STATUS 19 SUMMARY OF HEALTH AN D WELLBEING 21 KEY HEALTH OUTCOMES 22 Chronic disease 22 Diabetes 24 Dementia 27 -

Banyule City Council Aboriginal Heritage Study (1999)

BANYULE CITY COUNCIL Aboriginal Heritage Study PUBLIC EDITION prepared by: Brendan Marshall AUSTRAL HERITAGE CONSULTANTS 28 Anketell St Coburg 3058 February 1999 Note: This publication does not include specific information with regard to the location of Aboriginal heritage sites. That information has been provided to Banyule City Council on a confidential basis especially for use for site management purposes and in relation to the consideration of proposals for land use and development. EXPLANATORY NOTE The Aboriginal Heritage Study was considered by Banyule City Council at its meeting on 8 February 1999. At that meeting Council resolved not to adopt the recommendations of the Study which related to amendments to the Banyule Planning Scheme, but to liaise with the Department of Infrastructure and Aboriginal Affairs Victoria to determine the most appropriate way to include protection for Aboriginal sites in the Banyule Planning Scheme. Council also resolved to adopt Recommendations 1-15 of the Aboriginal Heritage Study. TABLE OF CONTENTS Acknowledgements Abstract INTRODUCTION 9 1.1 Preamble 9 1.2 Significance of Aboriginal Heritage 10 1.3 Scope 12 1.4 Planning Considerations 12 1.5 Project Aims 13 1.6 Report Organisation 14 1.7 The Wurundjeri 14 1.8 Aboriginal Archaeological Site Types 14 1.8.1 Stone Artefact Scatters 14 1.8.2 Isolated Artefacts 14 1.8.3 Scarred Trees 15 1.9 Other Possible Aboriginal Archaeological Site Types 15 1.9.1 Freshwater Shell Middens 15 1.9.2 Aboriginal Burials 15 1.9.3 Post-European Sites 15 1.10 Terms and Definitions -

The Long Game

The Long Game The Official Newsletter of the Golf Society of Australia Correspondence: 22 Surf Avenue, Beaumaris Vic 3193 Ph/Fx: 03 9589 5551 www.golfsocietyaust.com Long Game Editor: Moira Drew No 28, May 2008 Display at Australian Women’s Open —Kingston Inside this issue: Heath Golf Club, 31 January—3 February 2008 GSA Activities & Results 1-3 The Golf Society of Australia provided a display tent at the & 8 Women's Australian Open at Kingston Heath, in conjunction with President’s Report 3 the Australian Golf Heritage Society (previously the Golf Collectors' Society of Australia). New GSA Members 3 Similar displays have been mounted at men's Australian Open events and this was an ideal opportunity to highlight items in the Early golf in Kyneton 4 Museum collection relating to Australian women's golf. Around the traps 5 Amongst the hundreds of visitors during the tournament, Book Review: Tom 6-7 there were many familiar faces Morris of St Andrews Left: Louise Briers with GSA Golf Club Historians 7 Secretary, Janet Hibbins For the Diary: 23 June Dinner, Victoria GC Speaker: Will Johnson 18 August Right: A section of President's Trophy, the display Royal Melbourne GC Golf in the National Sports Museum at the MCG Golf is one of the 8 new sports featured in the ’multi-sports’ area of the new National Sports Museum at the MCG which opened to great fanfare on 12 March 2008. In our role as manager of the Museum Collection for Golf Australia, the Golf Society of Australia has been involved in all aspects of this project, in particular liaison with the producers of the exhibition. -

Wednesday, 5Th August, 2020 Virtual Meeting Hosted by Zoom

PO Box 89, Elwood, VIC 3184 incorporation number: A0034315X ABN: 18 683 397 905 Contact: [email protected] MTF website: www.mtf.org.au Minutes – General Meeting Wednesday, 5th August, 2020 Virtual meeting hosted by zoom Chair: Cr Jonathon Marsden 1. Welcome and introduction Cr Marsden opened the meeting, and welcomed members and guests. 2. Attendance and Apologies Present: Ben Rossiter Victoria Walks Melissa Backhouse VicHealth Shelley White VicHealth Cr Tom Melican City of Banyule Kathleen Petras City of Banyule Henry Lee City of Bayside Cr Bruce Lancashire City of Brimbank Jon Liston City of Brimbank Phillip Mallis City of Darebin Cr Jonathon Marsden City of Hobsons Bay Doug Rowland City of Hobsons Bay Alex Reid City of Kingston Cr Anna Chen City of Manningham Daniele Ranieri City of Manningham Thomas Hardie-Cogdon City of Manningham Richard Smithers City of Melbourne Cr Nic Frances-Gilley City of Melbourne Sam Romasko City of Melton Josh Fergeus City of Monash Damir Agic City of Moonee Valley Cr Natalie Abboud City of Moreland Simon Stainsby City of Moreland Claire Davey Mornington Peninsula Shire Council Tim Lecky City of Stonnington Cr Andrew Davenport City of Whitehorse Serman Uluca City of Whitehorse Russell Tricker City of Whittlesea Troy Knowling City of Whittlesea Michael Butler City of whittlesea Melissa Falkenberg City of Wyndham Julian Wearne City of Yarra Cr Jackie Fristacky City of Yarra Oliver Stoltz Chris Lacey Andrew Pringle Alison Wood Elina Lee Rachel Carlisle Department of Transport Raj Ramalingam VicRoads David Stosser MRCagney Greg Day Edunity Jane Waldock MTF Apologies Adam McSwain, City of Bayside Cr Andrea Surace, City of Moonee Valley 3. -

The Virginian

The Virginian Newsletter of the Virginia Golf Club Brisbane, Queensland IssueIssue 67 72- November May 2016 2014 From The President’s Desk Queensland, I have travelled around the state and visited clubs that don’t have a single employee. The mowing of the course and the operation of the bar is all handled by members giving up their time. I’ve even seen an “honour box” next to the first tee where you pay your Matt Toomey daily green fees. President As volunteers are so critical to the success of a golf club, I’d like to acknowledge all of those who help out at Virginia. I won’t list all of the Appointment of Secretary Manager names (for fear of leaving someone out) but we have members who serve on the Board, serve on Committees, assist the greens staff, help As you will hopefully be aware, the Board has appointed Michael with junior development, drive the drinks cart, run raffles, prepare the Crough as the Club’s new full-time Secretary Manager. newsletter, assist with pennant fundraising, assist with the pro-am, For the past 4 years, Michael has been the Secretary Manager of help organise golf and social events, and offer discounted services Gisborne Golf Club in Melbourne. Gisborne is of similar size to Virginia through their business. We also have members who provide (in terms of membership and revenue) and was recently ranked one of sponsorship and others who bring visitors to the Club at any the top 100 public access courses in the country by Golf Australia opportunity. -

Fixture List

2020 Riverlakes Golf Club Fixture List By Month: January February March April May June July August September October November December Page 1 of 24 2020 Riverlakes Golf Club – Fixtures January Date Day Event Status 2/1/2020 Thursday Single Stableford Ladies 2/1/2020 Thursday 9 Hole Comp - Stableford – All Day Open 4/1/2020 Saturday Single Stableford Open 7/1/2020 Tuesday Monthly Medal - Stroke Veterans 9/1/2020 Thursday Single Stableford Ladies 9/1/2020 Thursday 9 Hole Comp - Stableford – All Day Open 11/1/2020 Saturday Single Stableford Open 14/1/2020 Tuesday 4BBB Aggregate Veterans 16/1/2020 Thursday Single Stableford Ladies 16/1/2020 Thursday 9 Hole Comp - Stableford – All Day Open 18/1/2020 Saturday 4BBB Stableford – Men’s Goblet Qualifier Open 21/1/2020 Tuesday Single Stableford – Aussies v Rest Veterans 23/1/2020 Thursday 2 Ball Ambrose – Men’s Invite Ladies 23/1/2020 Thursday 9 Hole Comp - Stableford – All Day Open 25/1/2020 Saturday Australia Day 2 Ball Ambrose Shotgun Open (7am/12pm) 28/1/2020 Tuesday 2 Ball Ambrose Veterans 30/1/2020 Thursday Single Stableford Ladies 30/1/2020 Thursday 9 Hole Comp - Stableford – All Day Open February Date Day Event Status 1/2/2020 Saturday Stableford & Ladies Volkswagen Scramble Open 4/2/2020 Tuesday Monthly Medal - Stroke Veterans 6/2/2020 Thursday Monthly Medal – Stroke + Putts Ladies 6/2/2020 Thursday 9 Hole Comp - Stableford – All Day Open 8/2/2020 Saturday Monthly Medal - Stroke Open 9/2/2020 Sunday Stableford - Open Open 11/2/2020 Tuesday Single Stableford Veterans 13/2/2020 Thursday Single -

The Future of the Yarra

the future of the Yarra ProPosals for a Yarra river Protection act the future of the Yarra A about environmental Justice australia environmental Justice australia (formerly the environment Defenders office, Victoria) is a not-for-profit public interest legal practice. funded by donations and independent of government and corporate funding, our legal team combines a passion for justice with technical expertise and a practical understanding of the legal system to protect our environment. We act as advisers and legal representatives to the environment movement, pursuing court cases to protect our shared environment. We work with community-based environment groups, regional and state environmental organisations, and larger environmental NGos. We also provide strategic and legal support to their campaigns to address climate change, protect nature and defend the rights of communities to a healthy environment. While we seek to give the community a powerful voice in court, we also recognise that court cases alone will not be enough. that’s why we campaign to improve our legal system. We defend existing, hard-won environmental protections from attack. at the same time, we pursue new and innovative solutions to fill the gaps and fix the failures in our legal system to clear a path for a more just and sustainable world. envirojustice.org.au about the Yarra riverkeePer association The Yarra Riverkeeper Association is the voice of the River. Over the past ten years we have established ourselves as the credible community advocate for the Yarra. We tell the river’s story, highlighting its wonders and its challenges. We monitor its health and activities affecting it. -

7.5. Final Outcomes of 2020 General Valuation

Council Meeting Agenda 24/08/2020 7.5 Final outcomes of 2020 General Valuation Abstract This report provides detailed information in relation to the 2020 general valuation of all rateable property and recommends a Council resolution to receive the 1 January 2020 General Valuation in accordance with section 7AF of the Valuation of Land Act 1960. The overall movement in property valuations is as follows: Site Value Capital Improved Net Annual Value Value 2019 Valuations $82,606,592,900 $112,931,834,000 $5,713,810,200 2020 Valuations $86,992,773,300 $116,769,664,000 $5,904,236,100 Change $4,386,180,400 $3,837,830,000 $190,425,800 % Difference 5.31% 3.40% 3.33% The level of value date is 1 January 2020 and the new valuation came into effect from 1 July 2020 and is being used for apportioning rates for the 2020/21 financial year. The general valuation impacts the distribution of rating liability across the municipality. It does not provide Council with any additional revenue. The distribution of rates is affected each general valuation by the movement in the various property classes. The important point from an equity consideration is that all properties must be valued at a common date (i.e. 1 January 2020), so that all are affected by the same market. Large shifts in an individual property’s rate liability only occurs when there are large movements either in the value of a property category (e.g. residential, office, shops, industrial) or the value of certain locations, which are outside the general movements in value across all categories or locations. -

Annual Report 2019 Contents

ANNUAL REPORT 2019 CONTENTS PAGE PRESIDENT'S REVIEW 8 CHIEF EXECUTIVE OFFICER’S REPORT 12 AUSTRALIAN OLYMPIC COMMITTEE 20 OLYMPISM IN THE COMMUNITY 26 OLYMPIAN SERVICES 38 TEAMS 46 ATHLETE AND NATIONAL FEDERATION FUNDING 56 FUNDING THE AUSTRALIAN OLYMPIC MOVEMENT 60 AUSTRALIA’S OLYMPIC PARTNERS 62 AUSTRALIA’S OLYMPIC HISTORY 66 CULTURE AND GOVERNANCE 76 FINANCIAL STATEMENTS 88 AOF 2019 ANNUAL REPORT 119 CHAIR'S REVIEW 121 FINANCIAL STATEMENTS 128 Australian Olympic Committee Incorporated ABN 33 052 258 241 REG No. A0004778J Level 4, Museum of Contemporary Art 140 George Street, Sydney, NSW 2000 P: +61 2 9247 2000 @AUSOlympicTeam olympics.com.au Photos used in this report are courtesy of Australian Olympic Team Supplier Getty Images. 3 OUR ROLE PROVIDE ATHLETES THE OPPORTUNITY TO EXCEL AT THE OLYMPIC GAMES AND PROMOTE THE VALUES OF OLYMPISM AND BENEFITS OF PARTICIPATION IN SPORT TO ALL AUSTRALIANS. 4 5 HIGHLIGHTS REGIONAL GAMES PARTNERSHIPS OLYMPISM IN THE COMMUNITY PACIFIC GAMES ANOC WORLD BEACH GAMES APIA, SAMOA DOHA, QATAR 7 - 20 JULY 2019 12 - 16 OCTOBER 2019 31PARTNERS 450 SUBMISSIONS 792 COMPLETED VISITS 1,022 11SUPPLIERS STUDENT LEADERS QLD 115,244 FROM EVERY STATE STUDENTS VISITED AND TERRITORY SA NSW ATHLETES55 SPORTS6 ATHLETES40 SPORTS7 ACT 1,016 26 SCHOOL SELECTED TO ATTEND REGISTRATIONS 33 9 14 1 4LICENSEES THE NATIONAL SUMMIT DIGITAL OLYMPIAN SERVICES ATHLETE CONTENT SERIES 70% 11,160 FROM FOLLOWERS Athlete-led content captured 2018 at processing sessions around 166% #OlympicTakeOver #GiveThatAGold 3,200 Australia, in content series to be 463,975 FROM OLYMPIANS published as part of selection IMPRESSIONS 2018 Campaign to promote Olympic CONTACTED announcements.