Applied Microeconomics: Consumption, Production and Markets David L

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Principles of MICROECONOMICS an Open Text by Douglas Curtis and Ian Irvine

with Open Texts Principles of MICROECONOMICS an Open Text by Douglas Curtis and Ian Irvine VERSION 2017 – REVISION B ADAPTABLE | ACCESSIBLE | AFFORDABLE Creative Commons License (CC BY-NC-SA) advancing learning Champions of Access to Knowledge OPEN TEXT ONLINE ASSESSMENT All digital forms of access to our high- We have been developing superior on- quality open texts are entirely FREE! All line formative assessment for more than content is reviewed for excellence and is 15 years. Our questions are continuously wholly adaptable; custom editions are pro- adapted with the content and reviewed for duced by Lyryx for those adopting Lyryx as- quality and sound pedagogy. To enhance sessment. Access to the original source files learning, students receive immediate per- is also open to anyone! sonalized feedback. Student grade reports and performance statistics are also provided. SUPPORT INSTRUCTOR SUPPLEMENTS Access to our in-house support team is avail- Additional instructor resources are also able 7 days/week to provide prompt resolu- freely accessible. Product dependent, these tion to both student and instructor inquiries. supplements include: full sets of adaptable In addition, we work one-on-one with in- slides and lecture notes, solutions manuals, structors to provide a comprehensive sys- and multiple choice question banks with an tem, customized for their course. This can exam building tool. include adapting the text, managing multi- ple sections, and more! Contact Lyryx Today! [email protected] advancing learning Principles of Microeconomics an Open Text by Douglas Curtis and Ian Irvine Version 2017 — Revision B BE A CHAMPION OF OER! Contribute suggestions for improvements, new content, or errata: A new topic A new example An interesting new question Any other suggestions to improve the material Contact Lyryx at [email protected] with your ideas. -

Journal of Econometrics Consumption and Labor Supply

Journal of Econometrics 147 (2008) 326–335 Contents lists available at ScienceDirect Journal of Econometrics journal homepage: www.elsevier.com/locate/jeconom Consumption and labor supply Dale W. Jorgenson a,∗, Daniel T. Slesnick b a Department of Economics, Harvard University, Cambridge, MA 02138, United States b Department of Economics, University of Texas, Austin, TX 78712, United States article info a b s t r a c t Article history: We present a new econometric model of aggregate demand and labor supply for the United States. Available online 16 September 2008 We also analyze the allocation full wealth among time periods for households distinguished by a variety of demographic characteristics. The model is estimated using micro-level data from the Consumer JEL classification: Expenditure Surveys supplemented with price information obtained from the Consumer Price Index. An C81 important feature of our approach is that aggregate demands and labor supply can be represented in D12 D91 closed form while accounting for the substantial heterogeneity in behavior that is found in household- level data. As a result, we are able to explain the patterns of aggregate demand and labor supply in the Keywords: data despite using a parametrically parsimonious specification. Consumption ' 2008 Elsevier B.V. All rights reserved. Leisure Labor Demand Supply Wages 1. Introduction employed, we impute the opportunity wages they face using the wages earned by employees. The objective of this paper is to present a new econometric Cross-sectional variation of prices and wages is considerable model of aggregate consumer behavior for the United States. The and provides an important source of information about patterns model allocates full wealth among time periods for households of consumption and labor supply. -

Defining Assets When Purchasing an Existing Business By: Evan L

Defining Assets When Purchasing An Existing Business By: Evan L. Randall, Esq. and Jessica A. Neville, Esq. Thousands of businesses are purchased every year. The motivations for purchasing a business are as varied as the number of buyers: to expand the buyer’s existing business with a similar operation or to create new opportunities through a complimentary business. Perhaps the buyer seeks to change careers or add income to an existing one. And there is always the notion that buying an existing business avoids some of the risk associated with opening a new business. Business purchases are typically structured in one of two ways: a stock transfer or an asset purchase. A stock purchase involves buying the stock (or membership interest) of the company that owns the business. Typically, liabilities are assumed as well. An asset purchase involves just the assets of a company. In either format, determining what is being acquired is critical. This article focuses on some of the important categories of assets to consider in a business purchase: real estate, personal property, and intellectual property. Real Estate For many businesses (especially retail and restaurants) the real estate may be the most substantial asset. The seller either owns or leases the property, and there are different considerations for each alternative. If real estate is part of the sale, it will likely represent the bulk of the purchase price. If the business operates in leased premises, the seller would assign the lease to the buyer, and it is very likely that the landlord will need to consent to the assignment. -

Purchasing and Supply Chain Management 1 : Section 1

The Strategic Context for Competent Procurement 1. Introduction This study note is set in the context of the examination of those elements in the organisation that either have a significant impact on purchasing and supply management strategies or thinking and approaches that can make significant contributions to corporate strategy and the achievement of overall organisational corporate objectives. This section of module A attempts to examine the facets of organisational and business level strategy and seeks to set them in the context of purchasing and supply chain management in respect of their ability to aid or facilitate effectiveness and competence for the organisation. 2. Strategic Context Strategy is a very wide subject; there are many aspects to consider in the development of strategies and in making strategic decisions. No single definition exists for the term ‘strategy’. An investigation of the meaning of strategy has provided a summary of some of the definitions found in various texts: “ Strategy is not a detailed plan or program of instructions; it is a unifying theme that gives coherence and direction to the actions and decisions of an individual or organisation.” Grant 1998. A strategy according to this author is a plan for deploying resources in order to gain a better position for instance, competitively in the market. Strategy also can define what business the company is in or is to be in and the kind of company it is or is to be. “ What business is all about is . competitive advantage . .. The sole purpose of strategic planning is to enable a company to gain as efficiently as possible, a sustainable edge over its competitors. -

What Role Does Consumer Sentiment Play in the U.S. Economy?

The economy is mired in recession. Consumer spending is weak, investment in plant and equipment is lethargic, and firms are hesitant to hire unemployed workers, given bleak forecasts of demand for final products. Monetary policy has lowered short-term interest rates and long rates have followed suit, but consumers and businesses resist borrowing. The condi- tions seem ripe for a recovery, but still the economy has not taken off as expected. What is the missing ingredient? Consumer confidence. Once the mood of consumers shifts toward the optimistic, shoppers will buy, firms will hire, and the engine of growth will rev up again. All eyes are on the widely publicized measures of consumer confidence (or consumer sentiment), waiting for the telltale uptick that will propel us into the longed-for expansion. Just as we appear to be headed for a "double-dipper," the mood swing occurs: the indexes of consumer confi- dence register 20-point increases, and the nation surges into a prolonged period of healthy growth. oes the U.S. economy really behave as this fictional account describes? Can a shift in sentiment drive the economy out of D recession and back into good health? Does a lack of consumer confidence drag the economy into recession? What causes large swings in consumer confidence? This article will try to answer these questions and to determine consumer confidence’s role in the workings of the U.S. economy. ]effre9 C. Fuhrer I. What Is Consumer Sentitnent? Senior Econotnist, Federal Reserve Consumer sentiment, or consumer confidence, is both an economic Bank of Boston. -

Demand Composition and the Strength of Recoveries†

Demand Composition and the Strength of Recoveriesy Martin Beraja Christian K. Wolf MIT & NBER MIT & NBER September 17, 2021 Abstract: We argue that recoveries from demand-driven recessions with ex- penditure cuts concentrated in services or non-durables will tend to be weaker than recoveries from recessions more biased towards durables. Intuitively, the smaller the bias towards more durable goods, the less the recovery is buffeted by pent-up demand. We show that, in a standard multi-sector business-cycle model, this prediction holds if and only if, following an aggregate demand shock to all categories of spending (e.g., a monetary shock), expenditure on more durable goods reverts back faster. This testable condition receives ample support in U.S. data. We then use (i) a semi-structural shift-share and (ii) a structural model to quantify this effect of varying demand composition on recovery dynamics, and find it to be large. We also discuss implications for optimal stabilization policy. Keywords: durables, services, demand recessions, pent-up demand, shift-share design, recov- ery dynamics, COVID-19. JEL codes: E32, E52 yEmail: [email protected] and [email protected]. We received helpful comments from George-Marios Angeletos, Gadi Barlevy, Florin Bilbiie, Ricardo Caballero, Lawrence Christiano, Martin Eichenbaum, Fran¸coisGourio, Basile Grassi, Erik Hurst, Greg Kaplan, Andrea Lanteri, Jennifer La'O, Alisdair McKay, Simon Mongey, Ernesto Pasten, Matt Rognlie, Alp Simsek, Ludwig Straub, Silvana Tenreyro, Nicholas Tra- chter, Gianluca Violante, Iv´anWerning, Johannes Wieland (our discussant), Tom Winberry, Nathan Zorzi and seminar participants at various venues, and we thank Isabel Di Tella for outstanding research assistance. -

Commodity Lead Buyer Department: Purchasing Reports To

Position Description Job Title: Commodity Lead Buyer Department: Purchasing Reports to: Corporate Purchasing Manager Location: Greenfield, IN Prepared by: Corporate Purchasing Manager Approved By: Engineering & Purchasing Director Approval Date: April 15, 2016 SUMMARY Work closely with internal stakeholders and external suppliers to develop and implement strategic commodity plans for all assigned categories at the lowest total cost. This includes the development and coordination of key procurement strategies with the tactical/logistical buying team. ESSENTIAL DUTIES AND RESPONSIBILITIES • Lead the development of and execution of category management strategies for all assigned categories/commodities • In line with strategic objectives, lead the negotiations to select, appoint and steer a supply base that progresses the company objectives on quality, cost, delivery and innovation • Work with internal stakeholders to define requirements for sourcing objectives • Evaluate competitive offers and present sourcing options that meet business requirements • Partner with Global Category Leads on global sourcing projects • Ensure all selected suppliers are compliant to service level agreements • Lead the category and supplier spend management activities with respective spend areas • Conduct in depth cost and spend analysis in order to develop cost savings initiatives through various cost reduction options • Carry out administrative responsibilities that effectively manage projects and contracting activities • Lead and expedite vendor selection and purchasing decisions through appropriate competitive bid and strategic sourcing processes (leverage practices, bundling tools, etc) • Achieve all cost reduction savings targets • Monitor, manage and report on achievements on key purchasing indicators in line with department requirements • Immediately respond to unforeseen supply failures, working with manufacturing and supplier to avoid supply chain interruptions. Modernfold, Inc. -

Procurement Vs Purchasing: What Is the Difference?

Procurement vs Purchasing: What Is The Difference? Mark Twain said, “The difference between the almost right word and the right word is really a large matter—it’s the difference between the lightning bug and the lightning.” While purchasing may get materials in the door, professional procurement strategies can reduce a company’s purchase spend by an average of 8 to 12 percent per year, significantly impacting liquidity. Knowing the difference between procurement and purchasing pays off. https://planergy.com/blog/procurement-vs-purchasing/ 1 / 8 What is Purchasing? Purchasing is a simple transaction, when companies pay for and receive goods or services. Purchasing can be considered a subset of procurement. For a small business with no procurement department, this may mean a phone call to an office supply store when the supply of pens runs low or a new computer is needed. Small businesses often lack the purchasing power of a major enterprise and have no leverage with which to negotiate. A simple purchasing process is generally performed on a transactional basis with little strategy: 1. Placing the order Without strategy, goods and services are ordered as needed. Reactive purchasing comes with a host of money-wasting issues. Businesses that buy on demand without approved purchase orders (PO) typically lack oversight and budget control. 2. Supplier communications Most companies have a established list of suppliers they work with to purchase supplies. 3. Receiving of goods or services Purchasing requires receipt of goods and services. Good purchasing strategy includes protocols for recording and tracking purchases. https://planergy.com/blog/procurement-vs-purchasing/ 2 / 8 4. -

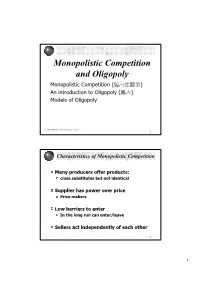

Monopolistic Competition and Oligopoly Monopolistic Competition (獨占性競爭) an Introduction to Oligopoly (寡占) Models of Oligopoly

Monopolistic Competition and Oligopoly Monopolistic Competition (獨占性競爭) An introduction to Oligopoly (寡占) Models of Oligopoly © 2003 South-Western/Thomson Learning 1 Characteristics of Monopolistic Competition Many producers offer products: close substitutes but not identical Supplier has power over price Price makers Low barriers to enter In the long run can enter/leave Sellers act independently of each other 2 1 Product Differentiation In perfect competition, product is homogenous In Monopolistic competition, Sellers differentiate products in four basic ways Physical differences and qualities • Shampoo: size, color, focus normal (dry) hair … Location • The number of variety of locations – Shopping mall: cheap, variety of goods – Convenience stores: convenience Accompanying services • Ex: Product demonstration, money back/no return Product image • Ex: High quality, natural ingredients … 3 Short-Run Profit Maximization or Loss Minimization Because products are different Each firm has some control over price demand curve slopes downward Many firms sell close substitutes, Raises price Æ lose customers Demand is more elastic than monopolist’s but less elastic than a perfect competitors 4 2 Price Elasticity of Demand The elasticity demand depends on The number of rival firms that produce similar products The firm’s ability to differentiate its product more elastic: if more competing firms Less elastic: differentiated product 5 Profit Maximization as MR=MC The downward-sloping demand curve MR curve • slopes downward and • below the demand curve Cost curves are similar to those developed before Next slide depicts the relevant curves for the monopolistic competitor 6 3 Profit Maximization In the short run, if revenue >variable cost Profits are max. as MR=MC. -

AP Macroeconomics: Vocabulary 1. Aggregate Spending (GDP)

AP Macroeconomics: Vocabulary 1. Aggregate Spending (GDP): The sum of all spending from four sectors of the economy. GDP = C+I+G+Xn 2. Aggregate Income (AI) :The sum of all income earned by suppliers of resources in the economy. AI=GDP 3. Nominal GDP: the value of current production at the current prices 4. Real GDP: the value of current production, but using prices from a fixed point in time 5. Base year: the year that serves as a reference point for constructing a price index and comparing real values over time. 6. Price index: a measure of the average level of prices in a market basket for a given year, when compared to the prices in a reference (or base) year. 7. Market Basket: a collection of goods and services used to represent what is consumed in the economy 8. GDP price deflator: the price index that measures the average price level of the goods and services that make up GDP. 9. Real rate of interest: the percentage increase in purchasing power that a borrower pays a lender. 10. Expected (anticipated) inflation: the inflation expected in a future time period. This expected inflation is added to the real interest rate to compensate for lost purchasing power. 11. Nominal rate of interest: the percentage increase in money that the borrower pays the lender and is equal to the real rate plus the expected inflation. 12. Business cycle: the periodic rise and fall (in four phases) of economic activity 13. Expansion: a period where real GDP is growing. 14. Peak: the top of a business cycle where an expansion has ended. -

Price Bargaining and Competition in Online Platforms: an Empirical Analysis of the Daily Deal Market

Price Bargaining and Competition in Online Platforms: An Empirical Analysis of the Daily Deal Market Lingling Zhang Doug J. Chung Working Paper 16-107 Price Bargaining and Channel Selection in Online Platforms: An Empirical Analysis of the Daily Deal Market Lingling Zhang University of Maryland Doug J. Chung Harvard Business School Working Paper 16-107 Copyright © 2016, 2018, 2019 by Lingling Zhang and Doug J. Chung Working papers are in draft form. This working paper is distributed for purposes of comment and discussion only. It may not be reproduced without permission of the copyright holder. Copies of working papers are available from the author. Funding for this research was provided by Harvard Business School and the institution(s) of any co-author(s) listed above. Price Bargaining and Competition in Online Platforms: An Empirical Analysis of the Daily Deal Market Lingling Zhang Robert H. Smith School of Business, University of Maryland, College Park, MD 20742, United States, [email protected] Doug J. Chung Harvard Business School, Harvard University, Boston, MA 02163, United States, [email protected] Abstract The prevalence of online platforms opens new doors to traditional businesses for customer reach and revenue growth. This research investigates platform competition in a setting where prices are determined by negotiations between platforms and businesses. We compile a unique and comprehensive data set from the U.S. daily deal market, where merchants offer deals to generate revenues and attract new customers. We specify and estimate a two-stage supply-side model in which platforms and merchants bargain on the wholesale price of deals. -

Accounts Payable Policy University of Iowa Purchasing Department Cover | Page

Payment Processing for Purchase Order Invoices Contents Payment Process ............................................................................................................................................................................... 1 Invoices ............................................................................................................................................................................................. 1 Invoice Number ...................................................................................................................................................................................... 1 Short Payments ...................................................................................................................................................................................... 1 Credit Memos ........................................................................................................................................................................................ 2 Voucher Reports ................................................................................................................................................................................ 2 Adjustment Voucher .............................................................................................................................................................................. 2 Delinquent Voucher Reports .................................................................................................................................................................