4. Wiki worth 15% of the course grade. The wiki is http://econ651spring2009.wikispaces.com/. a. On the second or third week of class, there will be an Excel spreadsheet with students assignments. Most of the assignments will be case studies or applications of course material. b. You will need to FIRST sign up on wikispaces.com and THEN sign up for the class wiki. Please sign up early. c. Grading will be based on (1) quality of the writing: Grammar and clarity (2) quality of references: Minimum of 4 academic journal/book references (3) quality of multiple choice questions that deal with the assigned topic (Minimum 5 questions) (4) A discussion on how to apply the topic to several in real world situations, d. There will be two grading periods. Students will be expected to make a least 8 well thought out comments on other students topics during Both grading periods (each comment must be on a different topic). This means there will be at least 16 comments this semester. MEMO 10 – AOL Time Warner RE: AOL Europe

Among the many decisions made every day by the managers of large corporations, perhaps the most bittersweet is to determine when it’s time to move on from a venture that has fallen short of its lofty goals, and second, determining the best way to go about it. And it appears that the management at Time Warner are mulling over this very decision, regarding their holdings in AOL Europe.

Background

Questions regarding AOL Europe’s viability as an entity are not new. In fact, from the outset in 1996, at AOL Europe’s inception as a partnership with minority owner Bertelsmann, AG (49.5%), the challenges faced by AOL Europe made it difficult to duplicate its success in the United States, and thus made the venture’s prospects appear far less than rosy. First, although Europe and the United States are perhaps comparable in many ways, the fact that Europe encompasses numerous independent cultures and languages presented a challenge for AOL to design content as generally appealing as had been its signature in the United States. Second, European customers faced higher costs than their American counterparts, as, in addition to AOL Europe’s access charges, European phone companies charged by the minute for time spent online. This disadvantage left the door partly open for the competition – and Telecom Italia, France Telecom, Telefonica (of Spain), and Deutsche Telekom are a few of Europe’s national companies that did not fail to capitalize on this opportunity, by bundling Internet service along with their existing phone service.

More recently, in 2001 AOL Europe’s viability was again questioned when it reported $600 million losses, despite the $800 million in revenues its 2.5 million subscribers produced. Unfortunately, the rain of bad news turned into a downpour, in the form of antitrust issues surrounding AOL Europe’s and Bertelsmann’s publishing and music groups – which constrained AOL Europe to spend $6.75 billion buying out Bertelsmann in order to resolve the concerns. Needless to say, these events did not comfortably answer the detractors’ questions about AOL Europe’s health and stability. Problem

As a result of these circumstances, AOL management is now receiving internal recommendations to sell its AOL Europe holdings, and, although no decision has been made, is contemplating how it would sell the relevant assets – whether in one all-inclusive sale, or by parsing them individually.

Considerations

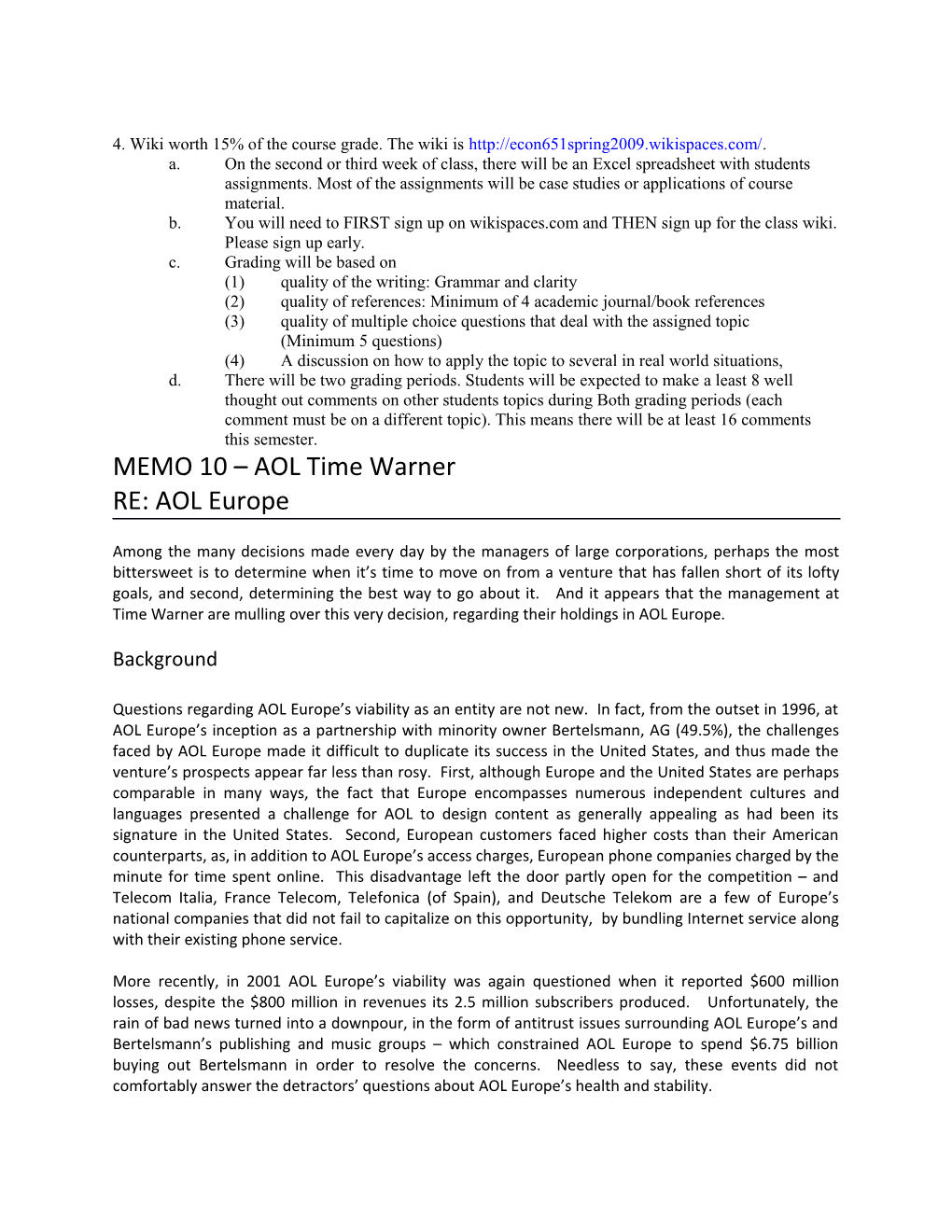

Before finalizing any decision regarding the sale of AOL Europe-related assets, management should pause and consider the much more favorable recent developments (at the supposed time of the Memo). As Figure 1 shows, both revenue and subscribership have increased since parting ways with Bertelsmann, and perhaps the questions surrounding AOL Europe’s formerly gloomy prospects have dissipated.

Figure 2 – Shows changes in AOL Europe’s Revenue & Subscribership before and after the Bertelsmann buyout.

A glance at these substantial increases in revenue and number of subscribers might be enough to cause management to reconsider the sale of its holdings in AOL Europe. Additionally, the fact that neither Yahoo nor Microsoft was initially profitable in Europe might also put the less-than-ideal snapshot of AOL Europe in context. However, if at length management decides to sell its holdings in AOL Europe, the next decision is how to go about doing it.

The main question regarding the assets sale is whether they would be sold piece-meal or in a collective deal; management is now contemplating which would be the better course.

Works Cited

1. Baye, Michael R. (2009) Managerial Economics and Business Strategy 6th Edition. St. Louis: McGraw-Hill Irwin 2. http://www.businessweek.com/technology/content/feb2002/tc2002021_2922.htm